A new round of US tariffs on Chinese imports took effect today and market reactions are rather muted. Trump stepped up his hard-line rhetorics and tweeted he’s in no rush to make a trade deal. Yet investors shrug off such comments. Sterling also paid little attention to UK GDP and production data. Instead, Canadian Dollar steals the show with strong April job data.

For now, Canadian Dollar is the strongest one for today, followed by Swiss Franc and then Kiwi. Dollar is the worst performing one followed by Yen. However, for the week, Yen remains the strongest one, followed by Swiss Franc on risk aversion. Sterling is the weakest on Brexit impasse, followed by Kiwi and then Aussie.

In Europe, currently, FTSE is up 0.26%. DAX is up 0.71%. CAC is up 0.39%. German 10-year yield is up 0.008 at -0.039, staying negative. Earlier in Asia, Nikkei dropped -0.27%. Hong Kong HSI rose 0.84%. China Shanghai SSE rose 0.31%. Singapore Strait Times rose 0.12%. Japan 10-year JGB yield rose 0.0019 to -0.044.

Canada added 106.5k jobs, unemployment rate dropped to 5.7%

Canadian Dollar jumps sharply after stellar job data. The employment market grew 106.5k in April, well above expectation of 15.0k. Unemployment rate dropped to 5.7%, down from 5.8% and beat expectation of 5.8%. On year-over-year basis, employment grew 2.3% or 426k, with 248k in full-time and 170k in part-time jobs. Employment grew in four provinces of Ontario, Quebec, Alberta and Price Edward Island.

US CPI rose to 2.0%, core CPU rose to 2.1% in April

US headline CPI rose to 2.0% yoy in April, up from 1.9% yoy but missed expectation of 2.1% yoy. Core CPI rose to 2.1% yoy, up from 2.0% yoy and matched expectations.

Trump will use China tariffs to buy US farm products, building new infrastructure, on healthcare…

In a series of tweets today, Trump indicates he’s now in no rush to seal the trade deal with China, given that new tariffs are already in plan. Trump said “Talks with China continue in a very congenial manner – there is absolutely no need to rush – as Tariffs are NOW being paid” going “directly to the Treasury”.

And, additionally Trump said with over USD 100B in tariffs, “we will buy agricultural products from our Great Farmers, in larger amounts than China ever did, and ship it to poor & starving countries in the form of humanitarian assistance.”

Also, “If we bought 15 Billion Dollars of Agriculture from our Farmers, far more than China buys now, we would have more than 85 Billion Dollars left over for new Infrastructure, Healthcare, or anything else. China would greatly slow down, and we would automatically speed up!”

UK GDP grew 0.5% qoq in Q1, but March contracted -0.1% mom

UK GDP grew 0.5% qoq in Q1, up from Q4’s 0.2% qoq and matched expectations. Annually, GDP grew 1.8% yoy, up from Q4’s 1.4%. Looking at the details, production had a noticeable pickup by 1.4. But services growth slowed to just 0.3%. Construction growth increased to 1.0%. Output of agriculture, forestry and fishing sector fell by 1.8%.

However, in March GDP contracted -0.1% mom, below expectation of 0.0% mom. Index of services dropped -0.1% mom. Index of production rose 0.7% mom. Manufacturing rose 0.9% mom. Construction dropped -1.9% mom. Agriculture dropped -0.1% mom.

UK Chancellor of Exchequer Philip Hammond hailed that 0.5% growth in Q1 GDO was good news, with growth in all major sectors. He added, “we’re investing billions in our infrastructure and skills to boost jobs & wages”.

Also from UK, industrial production rose 0.7% mom, 1.3% yoy, versus expectation of 0.1% mom, 0.4% yoy. Manufacturing production rose 0.9% mom, 2.6% yoy, versus expectation of 0.0% mom, 1.1% yoy. Visible trade deficit narrowed to GBP -13.65B, slightly smaller than expectation of -13.7B. Construction output dropped -1.9% mom, versus expectation of -0.9% mom.

ECB Praet: World norm challenged by power politics

ECB chief economist Peter Praet said a prepared speech that “the notion that the euro provides stability and security has been weakened by the gaps in our governance framework”. Thus, “it is not surprising that claims that countries would be better off outside the euro find a sympathetic audience.”

To him, the long run solution most likely involves “deeper fiscal integration”. In the short run, Praet urged to “complete banking union”. While the SSM has moved Eurozone towards the goal, “for deep cross-border integration to develop, effective institutions for public risk-sharing need also to be in place.”

Praet also pointed out that “rules and norms” of international relations government since WWII are being challenged and replaced by “new power politics where large economies try to impose their will on smaller ones”. And in such a world ” it is undeniable that the EU amplifies the sovereignty of its members.:.

Also, Brexit also underling the pros and cons of EU membership. And, “it is now established that leaving the EU presents a trade-off: countries either have to follow the rules they could once set; or they have accept a diminished level of market access, and ultimately lower welfare for their people.”

Released from Germany, trade surplus widened to EUR 20.0B in March versus expectation of EUR 19.4B.

BoJ opinions: Clarification on forward guidance strengthens confidence in powerful easing

Summary of opinions at the April 24-25 BoJ Monetary Policy Meeting is released today. At the statement of that meeting, BoJ added clarification of forward guidance for policy rates. It noted that BoJ intended to keet current levels of interest rates at least through around spring 2020.

The summary of opinions noted that “in order to strengthen public confidence in continuing with powerful monetary easing, it is appropriate to clarify forward guidance for policy rates, such as through making clear the specific period for which extremely low levels of interest rates will be maintained.” Also, it is appropriate to consider revising forward guidance for policy rates, given, for example, that uncertainties regarding overseas economies have heightened compared to the time of its introduction.

Meanwhile BoJ also noted “there is a possibility that a further decline in interest rates will result in a greater risk of inducing side effects on the real economy, rather than positive effects”. But BoJ dismissed the argument that QQE led to deterioration in banks’ profitability. It’s noted monetary easing has “brought about economic improvement, an increase in lending, a decline in credit costs, and an increase in profits stemming from stocks and bonds”.

Release from Japan, household spending rose 2.1% yoy in March, above expectation of 1.6% yoy. But labor cash earnings dropped sharply by -1.9% yoy, well below expectation of -0.50%.

RBA SoMP: Slight downgrade of inflation, no imminent need to cut rates

In the Statement of Monetary Policy, RBA noted that the economy has “slowed” and inflation “remains “low”. Also, “subdued” growth in household income and “adjustment” in housing markets affected consumer spending and residential construction. Still, labor market is “performing reasonably well”. Underlying inflation came in lower than expected in Q1 and “with pricing pressures subdued across much of the economy”.

Looking at the new economic projections, 2019 growth forecasts was revised down notably from 2.75% to 2.00%. But 2020 growth expectation was unchanged. Unemployment rate will stay longer at 5.00% through Dec 2020. Headline CPI was expected hit 2.00% in Dec 2019 and stay there throughout. Core CPI is revised slightly to 1.75% in Dec 2019 and 2.00% in Dec 2020.

All in all, while 2019 growth is expected to undershoot, it’s expected to pick up quickly. The downward revision in core CPI was just showed a slower pickup back to target, not anything disastrous. Based on this outlook, RBA still has a lot of room to wait and see the developments, before cutting interest rates.

- GDP growth year average: 2019 at 2.00%, revised down from 2.75%; 2020 at 2.75%, unchanged.

- Unemployment rate: Dec 2019 at 5%, unchanged; Dec 2020 at 5%, revised up from 4.75%.

- CPI: Dec 2019 at 2.00%, revised up from 1.75%; Dec 2020 at 2.00%, down from 2.25%.

- Trimmed mean inflation:Dec 2019 at 1.75%, revised down from 2.00%; Dec 2020 at 2.00%, revised down from 2.25%.

RBNZ Bascand: Economy growing below potential, needs to be pumped up

RBNZ Deputy Governor Geoff Bascand said the economy is growing less than potential of 2.8%. And, there’s just not enough pressure to get inflation up. “We think capacity pressures will just become a little less,” he said. “There is pressure there, there’s just not enough pressure to get inflation up. We need growth to be around 3% or more to keep being at or approaching our targets.”

Nevertheless, he added “nobody’s talking gloom here” even though it was “getting a bit harder” to meet the inflation target. He said “the headwinds have become a bit stronger, the global economy has become a bit weaker, the domestic economy seems to have softened.” Hence, “we’re going to be drifting away a little bit, not staying as close, there’s more chance of inflation ebbing than rising”.

And, “because of that, we ended up coming to a view that we needed to help pump it up a bit more.”

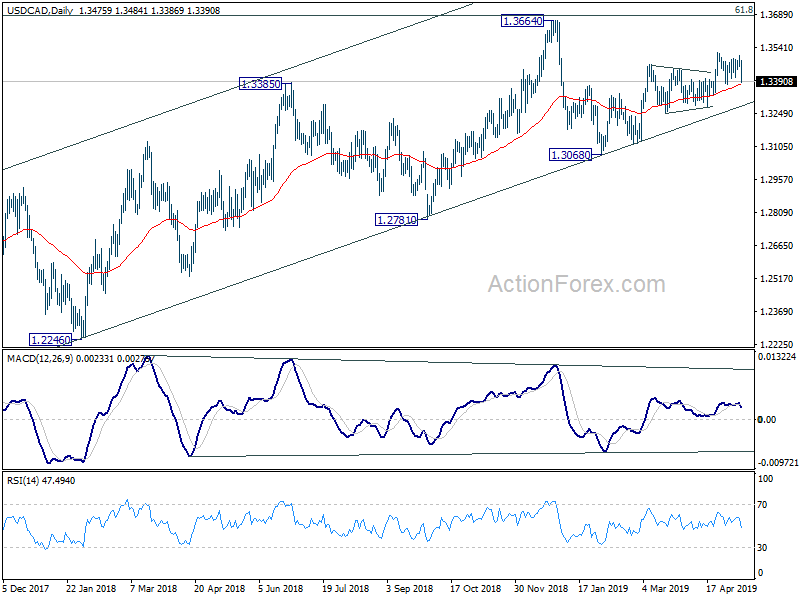

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3456; (P) 1.3480; (R1) 1.3502; More…

USD/CAD dives sharply as fall from 1.3505 accelerates. Still, outlook is unchanged that price actions from 1.3521 are seen as a corrective pattern. While break of 1.3376 minor support cannot be ruled out, downside should be contained above 1.3274 support to bring rise resumption. On the upside, firm break of 1.3521 will resume the whole rise from 1.3068 to retest 1.3664 high. However, decisive break of 1.3274 support will indicate completion of 1.3068 and turn outlook bearish.

In the bigger picture, USD/CAD is staying well inside medium term rising channel (support at 1.3278). Thus, the up trend from 1.2061 (2017 low) should be in progress. On the upside, decisive break of 61.8% retracement of 1.4689 (2016 high) to 1.2061 at 1.3685 will pave the way to 78.6% retracement at 1.4127 next. This will remain the favored case as long as 1.3068 support holds. However, sustained break the channel support will be the first sign of medium term reversal. Firm break of 1.3068 would confirm.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Consensus | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Overall Household Spending Y/Y Mar | 2.10% | 1.60% | 1.70% | |

| 23:30 | JPY | Labor Cash Earnings Y/Y Mar | -1.90% | -0.50% | -0.80% | -0.70% |

| 23:50 | JPY | BOJ Summary of Opinions | ||||

| 01:30 | AUD | RBA Statement on Monetary Policy May | ||||

| 06:00 | EUR | German Trade Balance (EUR) Mar | 20.0B | 19.4B | 18.7B | |

| 08:30 | GBP | GDP M/M Mar | -0.10% | 0.00% | 0.20% | |

| 08:30 | GBP | GDP Q/Q Q1 P | 0.50% | 0.50% | 0.20% | |

| 08:30 | GBP | Total Business Investment Q/Q Q1 P | 0.50% | -0.70% | -0.90% | |

| 08:30 | GBP | Industrial Production M/M Mar | 0.70% | 0.10% | 0.60% | |

| 08:30 | GBP | Industrial Production Y/Y Mar | 1.30% | 0.40% | 0.10% | 0.40% |

| 08:30 | GBP | Manufacturing Production M/M Mar | 0.90% | 0.00% | 0.90% | 1.00% |

| 08:30 | GBP | Manufacturing Production Y/Y Mar | 2.60% | 1.10% | 0.60% | 1.20% |

| 08:30 | GBP | Construction Output M/M Mar | -1.90% | -0.90% | 0.40% | |

| 08:30 | GBP | Visible Trade Balance (GBP) Mar | -13.65B | -13.7B | -14.1B | |

| 08:30 | GBP | Index of Services 3M/3M Mar | 0.30% | 0.40% | 0.40% | |

| 12:30 | CAD | Building Permits M/M Mar | 2.10% | 2.30% | -5.70% | -5.10% |

| 12:30 | CAD | Net Change in Employment Apr | 106.5K | 15.0K | -7.2K | |

| 12:30 | CAD | Unemployment Rate Apr | 5.70% | 5.80% | 5.80% | |

| 12:30 | USD | CPI M/M Apr | 0.30% | 0.40% | 0.40% | |

| 12:30 | USD | CPI Y/Y Apr | 2.00% | 2.10% | 1.90% | |

| 12:30 | USD | CPI Core M/M Apr | 0.10% | 0.20% | 0.10% | |

| 12:30 | USD | CPI Core Y/Y Apr | 2.10% | 2.10% | 2.00% |

{kind=link}