Sterling weakens broadly today as surprised contraction in Q2 UK GDP raised concerns of recession. In the background, risk of no-deal Brexit continues to weigh on sentiments. Canadian Dollar is suffering some renewed selling in early US session after worse than expected job data. Dollar is not much better though as core PPI slowed. On the other hand Yen and Swiss Franc are the strongest today, as risk sentiments turned soft, and German 10-year yield hits new record low of -0.605.

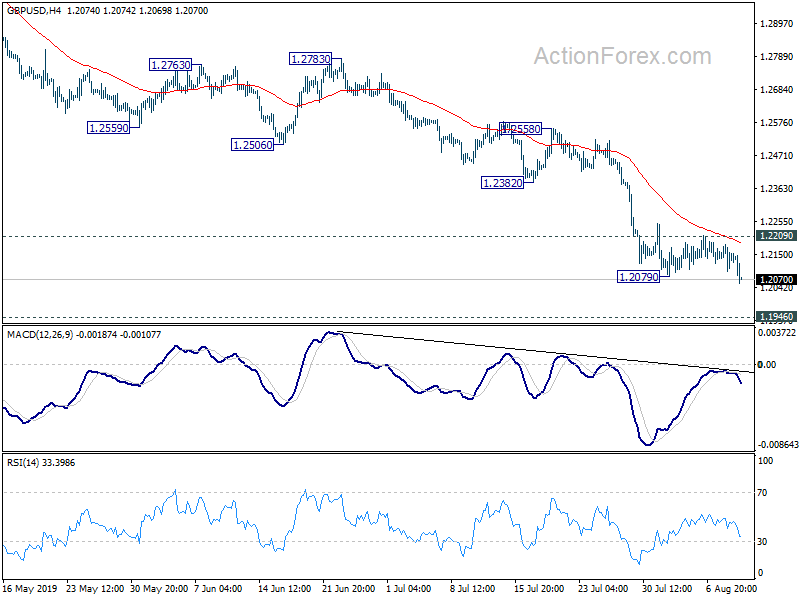

Technically, GBP/USD breaks 1.2079 to resume recent decline and should target 1.1946 low next. GBP/JPY breaks 128.11 to resume recent fall to 122.36 low. EUR/GBP is picking up some upside momentum for 0.9305 key resistance next. With selloff in Canadian Dollar, USD/CAD could have a test on 1.3345 temporary top and break will resume recent rebound from 1.3016.

In Europe, FTSE is down -0.04%. DAX is down -1.07%. CAC is down -0.84%. German 10-year yield is down -0.022 at -0.577. Earlier in Asia, Nikkei rose 0.44%. Hong Kong HSI dropped -0.69%. China Shanghai SSE dropped -0.71%. Japan 10-year JGB yield dropped -0.029 to -0.219.

Canada unemployment rate rose to 5.7%, US PPI unchanged at 1.7%, core PPI slowed to 2.1%

Canada employment dropped -24.2k in July, worse than expectation of 10.0k. Unemployment rate rose to 5.7%, up from 5.5%, above expectation of 5.5%. Also from Canada housing starts dropped to 222k in July, above expectation of 210k.

From US, PPI rose 0.2% mom, 1.7% yoy in July, matched expectation. PPI core dropped -0.1% mom, slowed to 2.1% yoy in July, below expectation of 0.2% mom, 2.3% yoy.

UK GDP contracted -0.2% in Q2, first contraction since 2012

UK GDP surprisingly contracted by -0.2% qoq in Q2, worse than expectation of 0.0% qoq. That’s also the first quarterly contraction since 2012. Over the year, GDP grew 1.2% yoy, slowed from Q1’s 1.8% yoy and missed expectation of 1.4% yoy. Looking at some details, services sector provided the only positive contribution to GDP growth, with 0.1% qoq growth. Production sector contracted sharply by -1.4% qoq, driving by sharp decline in manufacturing output. In June, GDP rose 0.0% mom, below expectation of 0.1% mom.

Chancellor of the Exchequer Sajid Javid said, “this is a challenging period across the global economy, with growth slowing in many countries. But the fundamentals of the British economy are strong – wages are growing, employment is at a record high and we’re forecast to grow faster than Germany, Italy and Japan this year.” And, “the government is determined to provide certainty to people and businesses on Brexit – that’s why we are clear that the UK is leaving the EU on October 31.”

Also released from UK, industrial production dropped -0.1% mom, -0.6% yoy in June, versus expectation of -0.2% mom, -0.3% yoy. Manufacturing production dropped -0.2% mom, -1.4% yoy, versus expectation of -0.2% mom, -1.1% yoy. Visible trade deficit narrowed to GBP -7.0B in June versus expectation of GBP -11.3B.

German DIHK: A weak zero growth in export this year is already a success

German exports dropped -8.0% yoy to EUR 106.1B in June. Imports dropped -4.4% yoy to EUR 89.3B. Trade surplus came in at EUR 16.8B. In calendar and seasonally adjusted, trade surplus narrowed to EUR 18.1B.

After Federal Statistical Office’s release, German Chamber of Industry and Commerce (DIHK) warned that export cannot do more to the economy in the second half. Ending the year with a “weak zero” growth in export is already a “success”.

Foreign trade chief of DIHK,Volker Treier, said “increasing protectionism and a noticeably weakening global economy are placing a direct burden on the export-strong German economy”. In particular, “US trade conflict with China and the tenacious struggle for Brexit are unsettling investors worldwide – and are clouding prospects, especially for the many German capital goods producers.”

And, “if we were to end the year with a weak zero – and thus with the worst result since the financial crisis – that would be a great success considering the conflict-laden and crisis-ridden global economy.”

Japan GDP grew 0.4% in Q2, solid investments despite weak exports

Japan GDP grew 0.4% qoq in Q2, well above expectation of 0.1% qoq. Annualize growth rate slowed from 2.8% to 1.8%, but beat expectation of 0.5%. Looking at some details, private consumption, which accounts for around 60% of GDP, grew 0.6% qoq. Capital expenditure was solid and grew 1.5% qoq, accelerated from 0.4% qoq in Q1. Exports were weak but contracted just 0.1% qoq.

The set of data argues that uncertainty from global trade war has relatively controlled impacts on the economy. In particular, companies were not prompted to rein in investment spending. This echoed BoJ’s assessment that global uncertainties had so far limited impact on the Japanese economy. Though, domestic demand would weaken ahead later in the year due to the planned sales tax hike. That’s something BoJ policymakers need to continue to monitor.

Also from Japan, M2 rose 2.4% yoy in July versus expectation of 2.3% yoy.

China PPI turned negative as trade war hurt demand

Headline CPI in China accelerated to 2.8% yoy in July, from 2.7% a month ago. Same as previous months, the key driver of inflation was food prices, which jumped 9.1% yoy in July. In June, food prices also rose 8.3% yoy. Of which, pork prices soared 27% yoy and fresh fruit prices skyrocketed 39.1%. Non-food price actually slowed -0.1 percentage point to 1.3%.

Core inflation, excluding food and energy prices, steadied for a third consecutive month at 1.6%. These signaled that higher inflation does not reflect improvement in Chinese economy. Rather the rising food price would affect consumer expenditure in other items, exacerbating slowdown in the economy.

As we had expected, PPI fell back to deflation for the first time since August 2016. Prices in the oil and gas exploration industry plunged -8.3%, while prices for oil, coal and other fuel processing industries declined -5.1%.

The US- China trade war has hurt demand for China’s manufacturing activities and shipment of raw materials. It is not surprising to see PPI go deeper in the negative territory as trade war has intensified.

More in China’s PPI Returns to Deflation, PBOC Probably Cuts Rate in September.

RBA Lowe said economy reached a gentle turning point, but growth forecasts revised down

In the “Opening Statement to the House of Representatives Standing Committee on Economics“, RBA Governor Philip Lowe said “there are signs the economy may have reached a gentle turning point”. The economic outlook is supported by lower interest rates, tax cuts, weaker exchange rate, stabilization of housing markets, improvement in resources sector and infrastructure spending. Thus, “consistent with this, we are expecting the quarterly GDP growth outcomes to strengthen gradually after a run of disappointing numbers,” Lowe said.

Though, for now, Lowe reiterated that “It is reasonable to expect an extended period of low rates will be needed to achieve the Board’s employment and inflation objectives.” And, at the Q&A session, Lowe also noted that “it’s possible we end up at the zero lower bound” on interest rates. He added “it’s unlikely but it is possible” and RBA is “prepared to do unconventional things if circumstances warranted.”.

In the new economic forecasts, 2019 year end growth was revised down from 2.75% to 2.50%. 2020 year-end growth was unchanged at 2020%. 2021 year-end growth was expected to pick up to 3.00%. Unemployment rate forecasts for 2019 and 2002 year-end were revised up from 5.00% to 5.25%. Unemployment was expected to drop to 5.00% in 2021 year end. Headline CPI forecasts were also revised down from 2.00% to 1.75% at both 2019 and 2020 year-end, before picking up to 2.00% at 2021 year-end.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2093; (P) 1.2137; (R1) 1.2180; More…

GBP/USD’s break of 1.2079 temporary low suggests fall resumption. Intraday bias is back on the downside for 1.1946 low. Break will target 100% projection of 1.4376 to 1.2391 from 1.3381 at 1.1396. On the upside, above 1.2209 minor resistance will turn intraday bias neutral and bring consolidations again first.

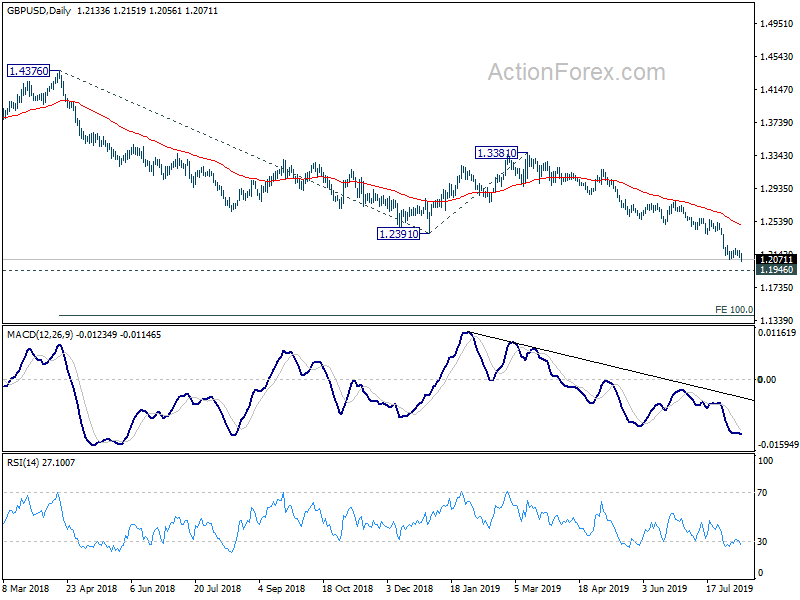

In the bigger picture, down trend from 1.4376 (2018 high) is extending towards 1.1946 low. We’d be cautious on bottoming there. But decisive break will resume down trend from 2.1161 (2007 high) to 61.8% projection of 1.7190 to 1.1946 from 1.4376 at 1.1135. In any case, medium term outlook will stay bearish as long as 1.3381 resistance holds, in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Consensus | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Japan Money Stock M2+CD Y/Y Jul | 2.40% | 2.30% | 2.30% | |

| 23:50 | JPY | GDP Q/Q Q2 P | 0.40% | 0.10% | 0.60% | |

| 23:50 | JPY | GDP Deflator Y/Y Q2 P | 0.40% | 0.40% | 0.10% | |

| 01:30 | CNY | CPI Y/Y Jul | 2.80% | 2.70% | 2.70% | |

| 01:30 | CNY | PPI Y/Y Jul | -0.30% | 0.00% | 0.00% | |

| 01:30 | AUD | RBA Statement on Monetary Policy | ||||

| 05:45 | CHF | Unemployment Rate Jul | 2.30% | 2.30% | 2.30% | |

| 06:00 | EUR | German Trade Balance (EUR) Jun | 18.1B | 18.5B | 18.7B | |

| 08:30 | GBP | GDP M/M Jun | 0.00% | 0.10% | 0.30% | |

| 08:30 | GBP | GDP Q/Q Q2 P | -0.20% | 0.00% | 0.50% | |

| 08:30 | GBP | GDP Y/Y Q2 P | 1.20% | 1.40% | 1.80% | |

| 08:30 | GBP | Industrial Production M/M Jun | -0.10% | -0.20% | 1.40% | |

| 08:30 | GBP | Industrial Production Y/Y Jun | -0.60% | -0.30% | 0.90% | 0.50% |

| 08:30 | GBP | Manufacturing Production M/M Jun | -0.20% | -0.20% | 1.40% | |

| 08:30 | GBP | Manufacturing Production Y/Y Jun | -1.40% | -1.10% | 0.00% | -0.20% |

| 08:30 | GBP | Construction Output M/M Jun | -0.70% | -0.40% | 0.60% | 0.30% |

| 08:30 | GBP | Construction Output Y/Y Jun | -0.20% | 0.20% | 1.70% | 1.30% |

| 08:30 | GBP | Index of Services 3M/3M Jun | 0.10% | 0.20% | 0.30% | 0.20% |

| 08:30 | GBP | Visible Trade Balance (GBP) Jun | -7.0B | -11.3B | -11.5B | |

| 12:15 | CAD | Housing Starts Jul | 222K | 210K | 246K | |

| 12:30 | CAD | Net Change in Employment Jul | -24.2K | 10.0K | -2.2K | |

| 12:30 | CAD | Unemployment Rate Jul | 5.70% | 5.50% | 5.50% | |

| 12:30 | USD | PPI M/M Jul | 0.20% | 0.20% | 0.10% | |

| 12:30 | USD | PPI Y/Y Jul | 1.70% | 1.70% | 1.70% | |

| 12:30 | USD | PPI Core M/M Jul | -0.10% | 0.20% | 0.30% | |

| 12:30 | USD | PPI Core Y/Y Jul | 2.10% | 2.30% | 2.30% |

{kind=link}