The markets are trading in mild risk averse mode ahead of quarter end. There are some worries of financial decoupling of US and China even though it’s just at very preliminary stage. But selloff is limited with support from improvements in Chinese PMIs. Yen is trading generally firmer. On the other hand, New Zealand Dollar is additionally pressured by its own poor business confidence data, followed by Australian as second weakest. Dollar is mixed for now, awaiting some important data in the week ahead.

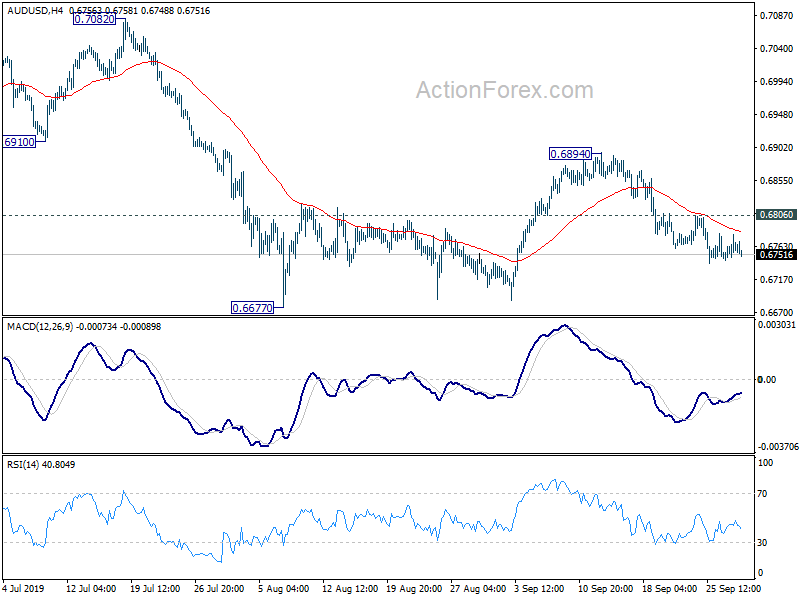

Technically, Sterling’s weakness will be a focus today. GBP/USD is pressing 1.2283 support while GBP/JPY is pressing 132.17 support. Break of these level will pave the way to 1.1958 and 126.54 lows respectively. Australian Dollar will also be an interesting one to watch ahead of tomorrow’s RBA rate cut. AUD/USD is on track to retest 0.6677 low as long as 0.6806 minor resistance holds. EUR/AUD is also in favor to break through 1.6301 to 1.6786, as long as 1.6128 minor support holds.

In Asia, Nikkei is currently down -0.79%. Hong Kong HSI is up 0.70%. China Shanghai SSE is down -0.16%. Singapore Strait Times is down -0.21%. Japan 10-year JGB yield is up 0.0178 at -0.216.

US Treasury: Not contemplating blocking Chinese companies from listing at this time

US Treasury spokesperson Monica Crowley partially denied the report that US is considering to de-list some Chinese companies from US exchanges. She said in a statement that “the administration is not contemplating blocking Chinese companies from listing shares on U.S. stock exchanges at this time.”

The statement was in response to a Bloomberg report that White House economic adviser Larry Kudlow was leading deliberations regarding a potential “financial decoupling” of US and China. Options discussed included forced delisting of Chinese companies, imposition of investment in China by US government pension funds, and limits on value of Chinese companies in US managed indexes. However, it’s later said that the deliberations are at very early stage, without even a time line.

Separately, Reuters reported that Nasdaq is already cracking down on IPO s of small Chinese companies, by tightening restrictions and slowing down approvals. The new listing rules raised the average trading volume requirements for a stock. Additionally, Nasdaq could delay listing of a company that does not demonstrate a strong enough nexus to the US capital markets. While not being directly targeted, small Chinese IPOs have experienced longer waiting times and scrutiny.

China manufacturing PMIs improved, but trade uncertainties still weigh

China Caixin Manufacturing PMI improved to 51.4 in September, up from 50.4 and beat expectation of 50.2. That’s also the highest reading since February 2018, signalling a recovery in the sector. Markit noted there were stronger increases in output and total new orders. However, new export business continued to decline. Staffing levels remained broadly unchanged.

Zhengsheng Zhong, Director of Macroeconomic Analysis at CEBM Group said: “The recovery in China’s manufacturing industry in September benefited mainly from the potential growth of domestic demand. The trade conflicts between China and the U.S. had a notable impact on exports, production costs and confidence of enterprises. Compared with growth in new orders, the employment situation recovered only a bit, indicating that structural issues may exist in the labor market. Central policymakers have recently been emphasizing the strong growth in the domestic market. Faster construction of infrastructure projects, better implementation of upgrading the industrial sector, and tax and fee cuts are likely to offset the influence of the subdued overseas demand and soften the downward pressure on China’s economic growth.”

Also released, the NBS PMI Manufacturing rose to 49.8 in September, up from 49.5 and beat expectation of 49.7. While there was and improvement, the sector remained in contraction for the fifth straight months. Total new orders improved and swung back to growth, indicating improving domestic demand. But new export orders dropped for the 16th month. Meanwhile factories continued to cut jobs with employment sub-index largely unchanged at 47.0.

BoJ: Not reached an impasse on monetary policy measures

Summary of opinions at September 18-19 BoJ meeting, BoJ warned that the “contrast between the manufacturing and nonmanufacturing sectors has become more evident” at home and abroad. Downside risks to the global economy “have been increasing further” mainly in Europe due to Brexit.

Also, ” it is becoming necessary to pay closer attention to the possibility that the inflation momentum will be lost”. BoJ needs to “reexamine economic and price developments” at the next monetary policy meeting (MPM).

It is also important for BoJ to “communicate with an emphasis that it has not reached an impasse on monetary policy measures”. Additionally, with regard to a negative interest policy, “its impact on the overall economy should be considered first, rather than on banks’ business conditions.”

Also released, industrial production dropped -1.2% mom in August, below expectation of -0.5% mom. Retail sales rose 2.0% yoy in August, above expectation of 0.9% yoy. Weak production data reconfirm that impact from global slowdown on exports. Strength of retail sales might partly be due to pre sales tax hike effect and could wane ahead.

New Zealand business confidence dropped -53.5, no impact from RBNZ’s rate cut

New Zealand ANZ Business Confidence dropped to -53.5 in September, down from -52.3. That’s also the worst reading since April 2008. Agriculture scored weakest confidence at -75.6 while manufacturing was best at -46.2. Activity outlook also dropped to -1.8, down from -0.5. Activity outlook was worst in construction at -7.1, best at services at -0.6.

ANZ noted that RBNZ will be “disappointed that its unexpectedly large 50bp cut in the Official Cash Rate last month does not appear to have had much impact on business’ sentiment or investment and employment intentions.” And, “prolonged lack of confidence is starting to feed its way through the economy and is threatening the tight labour market.” Also, “this gradual but prolonged economic slowdown is at risk of ceasing to be about the data and starting to become about the people.

A busy week with RBA, ISMs, NFP, PMIs etc

RBA rate decision is one of the major focuses in a very busy week. The central bank is generally expected to cut interest rate again, by -25bps to 0.75%. The underlying theme is clear that the Australian economy can support an unemployment rate of below 5% without inflation concern. Unemployment did drifted up further to 5.3% while inflation staying below target. Governor Philip Lowe also indicated recently that at the meeting, “we will again take stock of the evidence … the Board is prepared to ease monetary policy further if needed …”. From Australia, performance of manufacturing and services, and retail sales would also be released.

US will also release ISM manufacturing, non-manufacturing and non-farm payroll report. Currently, fed fund futures are only pricing in 44.9% chance another rate cut by Fed on October 30, and around 70% chance by December 11. That is, that markets are not so sure if Fed will continue with its mid-cycle adjustment. Upcoming data, as well as the result of US-China trade negotiations in October would be crucial.

Elsewhere, there will be PMIs from China, Eurozone inflation and unemployment rate, UK PMIs, Canada GDP, Japan Tankan survey featured too.

Here are some highlights for the week:

- Monday: BoJ summary of opinions, Japan industrial production, retail sales, housing starts; New Zealand ANZ business confidence, building permits; Australian MI inflation gauge, private sector credit; China official PMIs, Caixin PMI manufacturing; Germany retail sales, CPI, unemployment; Eurozone unemployment rate; Swiss KOF; UK Q2 GDP final, M4 money supply, mortgage approvals, current account; Canada RMPI, IPPI; US Chicago PMI.

- Tuesday: RBA rate decision, Australia AIG manufacturing, building approvals. Japan unemployment rate, tankan survey; Swiss retail sales; Eurozone PMI manufacturing final, CPI flash; UK PMI manufacturing; Canada GDP, PMI manufacturing; US ISM manufacturing, construction spending.

- Wednesday: UK BRC shop price, construction PMI; Japan consumer confidence, monetary base; US ADP employment.

- Thursday: Australia AIG services, trade balance; Eurozone PMI services final, PPI, retail sales; UK PMI services; US Challenger job cuts, jobless claims, ISM non-manufacturing, factory orders.

- Friday: Australia retail sales; Canada trade balance, Ivey PMI; US non-farm payrolls, trade balance.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.6746; (P) 0.6763; (R1) 0.6781; More…

With 0.6806 minor resistance intact, further decline is expected in AUD/USD. Corrective rise from 0.6677 should have completed with three waves up to 0.6984. Firm break of 0.6677 will resume larger down trend. On the upside, above 0.6806 will bring recovery. But in any case, risk will stay on the downside as long as 0.6894 resistance holds.

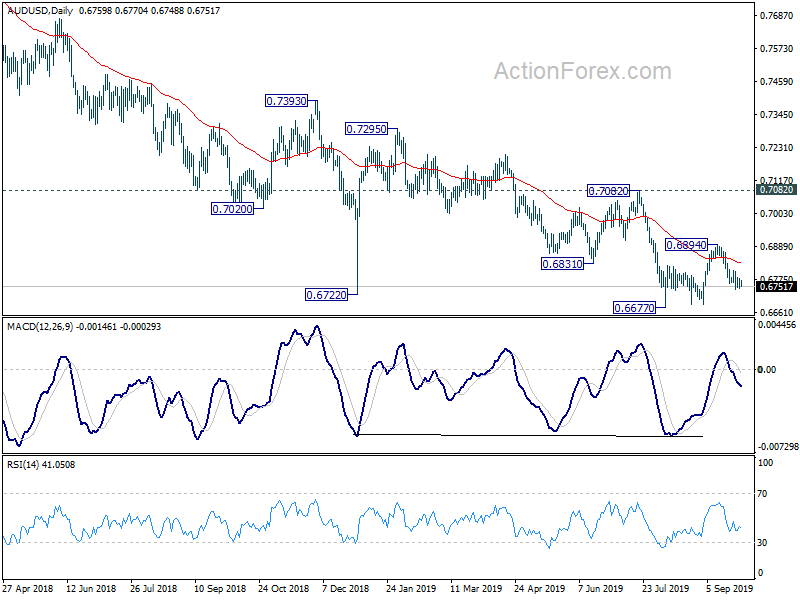

In the bigger picture, decline from 0.8135 (2018 high) is seen as resuming the long term down trend from 1.1079 (2011 high). Next target is 0.6008 (2008 low). On the upside, break of 0.7082 resistance is needed to be the first sign of medium term bottoming. Otherwise, outlook will remain bearish even in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits M/M Aug | 0.80% | -2.70% | -1.30% | |

| 23:50 | JPY | BoJ Summary of Opinions | ||||

| 23:50 | JPY | Industrial Production M/M Aug P | -1.20% | -0.50% | 1.30% | |

| 23:50 | JPY | Retail Trade Y/Y Aug | 2.00% | 0.90% | -2.00% | |

| 0:00 | NZD | ANZ Business Confidence Sep | -53.5 | -58.5 | -52.3 | |

| 1:00 | CNY | Manufacturing PMI Sep | 49.8 | 49.7 | 49.5 | |

| 1:00 | CNY | Non-Manufacturing PMI Sep | 53.7 | 54.2 | 53.8 | |

| 1:30 | AUD | Private Sector Credit M/M Aug | 0.20% | 0.30% | 0.20% | |

| 1:45 | CNY | Caixin Manufacturing PMI Sep | 51.4 | 50.2 | 50.4 | |

| 5:00 | JPY | Housing Starts Y/Y Aug | -7.10% | -6.10% | -4.10% | |

| 6:00 | EUR | Germany Retail Sales M/M Aug | 0.60% | -2.20% | ||

| 7:00 | CHF | KOF Leading Indicator Sep | 94.5 | 97 | ||

| 7:55 | EUR | Germany Unemployment Change Sep | 4K | 4K | ||

| 7:55 | EUR | Germany Unemployment Rate Sep | 5% | 5% | ||

| 8:30 | GBP | Net Lending to Individuals (GBP) M/M Aug | 5.1B | 5.5B | ||

| 8:30 | GBP | GDP Q/Q Q2 F | -0.20% | -0.20% | ||

| 8:30 | GBP | Mortgage Approvals Aug | 67K | 67K | ||

| 8:30 | GBP | M4 Money Supply M/M Aug | 0.40% | 0.70% | ||

| 8:30 | GBP | M4 Money Supply Y/Y Aug | 2.70% | |||

| 8:30 | GBP | Current Account (GBP) Q2 | -19.2B | -30.0B | ||

| 9:00 | EUR | Unemployment Rate Aug | 7.50% | 7.50% | ||

| 12:00 | EUR | Germany CPI M/M Sep P | -0.20% | |||

| 12:00 | EUR | Germany CPI Y/Y Sep P | 1.40% | 1.40% | ||

| 12:30 | CAD | Industrial Product Price M/M Aug | -0.20% | -0.30% | ||

| 12:30 | CAD | Raw Material Price Index Aug | 1.30% | 1.20% | ||

| 13:45 | USD | Chicago PMI Sep | 50.5 | 50.4 |

{kind=link}