Both Dollar and Canadian are under tremendous selling pressure after respective central bank announcements overnight. Fed chair Jerome Powell did signal a pause after yesterday’s rate cut. Yet, his message was too non-committal and let Dollar bulls dissatisfied. On the other hand, BoC was clearly more dovish than expected and raised the possibility of an “insurance’ rate cut. New Zealand and Australian Dollars are the strongest for today, as both are lifted by notable improvements in some economic data. Also, US and China are still on track to complete phase one trade deal despite cancellation of APEC summit in Chile. Yen stays mixed after BoJ stands pat and changed the forward guidance to indicate clear easing bias.

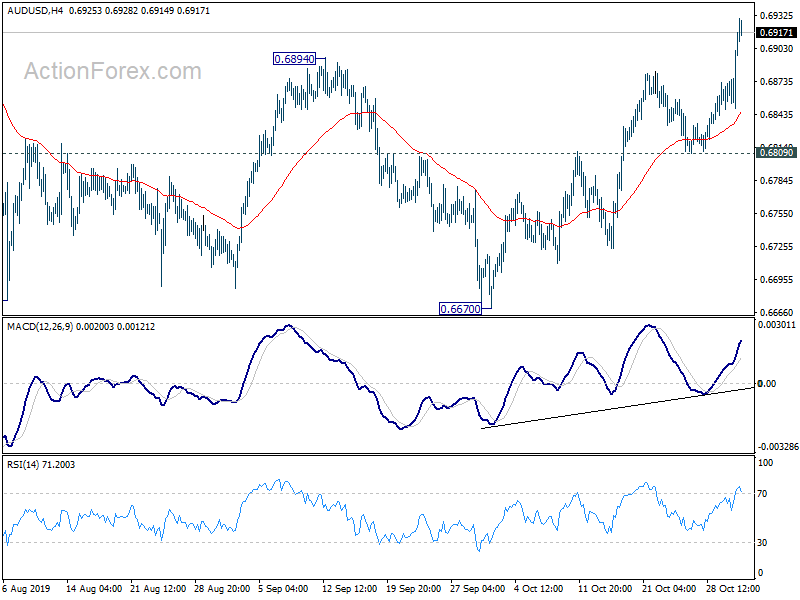

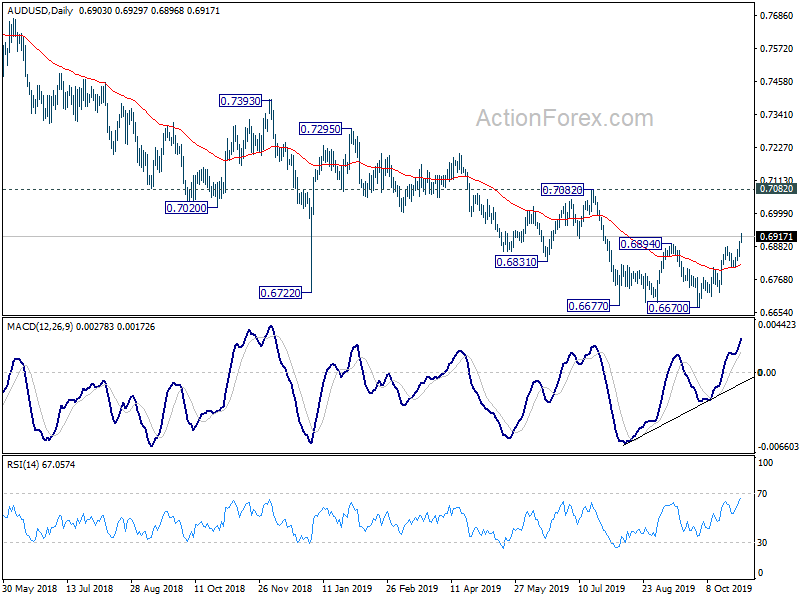

Technically, AUD/USD’s strong break of 0.6894 resistance, with upside acceleration, is now an early signal of medium term bullish reversal. Further rise would be seen to 0.7082 resistance, which is the rest test. EUR/AUD is on track to 1.6074 support first and break will target 1.5905 low. USD/CHF’s steep decline now puts focus back to 0.9841 support. Break will complete a head and should top pattern (ls: 0.9983, h: 1.0027, rs: 0.9970) which is a clear bearish sign. EUR/USD is also eyeing 1.1179 resistance and break will resume recent rally from 1.0879.

In Asia, Nikkei rose 0.37%. Hong Kong HSI is up 0.83%. China Shanghai SSE is down -0.35%. Singapore Strait Times is up 0.69%. Japan 10-year JGB yield is down -0.0208 at -0.141. Overnight, DOW rose 0.43%. S&P 500 rose 0.33% to 3046.77 after hitting new record at 3050.10. NASDAQ rose 0.33%. 10-year yield dropped -0.037 to -1.798.

Dollar bears took control as Fed’s pause seen as non-committal

After some post FOMC volatility, Dollar bears took over the markets overwhelmingly and sent the greenback sharply lower. The key takeaway was that while Fed Chair Jerome Powell indicated a pause after overnight’s rate cut to 1.50-1.75%, he was non-committal. There was a brief lift to Dollar as he said “monetary policy is in a good place”, and it would take a “material reassessment” of the outlook for considering another rate cut again.

However, Powell did stick to script that current stance of monetary policy is likely to “remain appropriate as long as incoming information about the economy remains broadly consistent with our outlook.” It’s also mentioned in the statement the timing of future adjustments will be based on “realized and expected economic condition”, taking in to account “a wide range of information” including domestic job and inflation data, as well ass international developments. That is, Fed is maintaining a highly data-dependent approach, without closing the door for further cuts.

Trade development is something that Fed will closely monitor. Powell said “We have that Phase One potential agreement with China which, if signed and put into effect, could have the effect of reducing trade tensions and reducing uncertainty. That would bode well for business confidence and perhaps activity over time.” If the economy was to experience “a sustained reduction in trade tensions, a broad reduction in trade tensions, and a resolution of these uncertainties, that would bode well for business sentiment.

More on FOMC:

- Fed Signals to Pause after a Third Rate Cut

- Northern Exposure: FOMC Moves from Pre-emptive to Reactive Stance

- FOMC Delivers Third Rate Cut In As Many Meetings

- FOMC Review Fed Is Playing The Waiting Game

- FOMC Recap: Hawkish Cut Delivered, Punters Ponder Powell’s Pontificating

- Fed Cuts Rates, But Signals Insurance May be Starting to Pay Off

- (FED) Federal Reserve Issues FOMC Statement

Loonie pressured as BoC turned dovish after standing pat.

BOC turned dovish in the October meeting, while maintaining the policy rate unchanged at 1.75%. For the first time, the central bank discussed about “insurance” rate cut, citing trade war’s damage to business investment and exports. The announcement sent the loonie lower, giving half of the gains made earlier this month.

More on BoC:

- Turning Dovish, BOC Discussed about Insurance Rate Cut for First Time In October

- Bank Of Canada Leaves Rates Unchanged, Lowers Guidance

- Bank of Canada Holds, But Is Increasingly Worried About Risks

Aussie jumps after strong building permits and receding RBA cut bets

Australian Dollar surges broadly today firstly with the help from post FOMC selloff in Dollar. In the background, Aussie has been riding on optimism towards US-China trade negotiations recently. The strong housing data today also eased concerns of a renewed downturn in the housing markets. Building permits rose 7.6% mom in September, way above expectations of 0.1% mom. Other data, while missed, were not disastrous. Private sector credit rose 0.2% mom in September versus expectation of 0.3% mom. Import price index rose 0.4% qoq in Q3 versus expectation of 0.5% qoq.

As Westpac noted in a report today, RBA should stand pat at its next meeting on November 5. Market pricing of a December cut also dropped from 80% back on October 4 to 25%. But most notably, market pricing of a February cut halved from 100% on October 4 to 50% today. While the pricing of February cut was not Westpac concurs with, that’s a factor in driving the Aussie higher today.

Also from down under, New Zealand building permits rose 7.2% mom in September, above expectation of 2.3% mom. ANZ business confidence rose to -42.4 in October, above expectation of -53.5.

BoJ stands pat, new forward guidance indicates clear easing bias

BoJ left monetary policy unchanged today as widely expected, but stepped up its signal for more easing ahead. Under the yield curve control framework, short term policy interest rate was held at -0.1%. Also, the central back will continue to increase monetary base at JPY 80T a year, with purchases of JGB to keep 10-year yield at around 0%. The decision was made by 7-2 vote, with Y. Harada and G. Kataoka dissenting as usual.

The forward guidance was changed to: “As for the policy rates, the Bank expects short- and long-term interest rates to remain at their present or lower levels as long as it is necessary to pay close attention to the possibility that the momentum toward achieving the price stability target will be lost.” Previously, BoJ said its committed to keep “current ultra-low rates for an extended period of time, at least until the spring of 2020.” It’s a clear message that BoJ is ready to cut interest rates again any time if outlook deteriorates further.

At the post meeting press conference, Governor Haruhiko Kuroda confirmed that the new forward guidance aimed at clarifying the stance that “policy bias is leaning towards additional monetary easing.” Regarding the tools, BoJ could “cut interest rates, increase asset buying or accelerate the pace of increase in base money”.

Also from japan, industrial production rose 1.4% mom in September, above expectation of 0.4% mom. Housing starts dropped -4.9% yoy in September, above expectation of -6.7% yoy. Consumer confidence rose to 36.2, above expectation of 35.5.

China PMI manufacturing dropped to 49.3, sixth straight months in contraction

China NBS PMI Manufacturing dropped to 49.3 in October, down from 49.8 and missed expectation of 49.8. It’s the sixth straight month of contraction reading. Looking at some details, new export orders dropped for the 17th month to 47.0, down from 48.2. Employment improved slightly but remain deep in contraction at 47.3, up fro 47.0. NBS PMI Non-Manufacturing dropped to 52.8, down from 53.7 and missed expectation of 53.7. It’s also the lowest reading since February 2016.

The overall set of data suggests that while China’s growth is already at lowest pace in 30 years, there is not sign of a turn around yet. The improvements seen back in the end of Q3 were just ripples in a down trend, rather than the start of sustained recovery. The official PMIs will likely remain sluggish in the coming months while a Phase 1 US-China trade deal is unlikely to provide any immediate lift.

Elsewhere

Germany retail sales rose 0.1% mom in September, below expectation of 0.3% mom. Eurozone will release GDP, unemployment rate and CPI flash in European session. Later in the day, Canada will release GDP, IPPI and RMPI. US will release personal income and spending, jobless claims and Chicago PMI.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.6866; (P) 0.6884; (R1) 0.6918; More…

AUD/USD rises to sa high as 0.6929 so far as rebound from 0.6670 extends. The break of 0.6894 resistance complete a double bottom pattern (0.6677, 0.6670), which is also an early sign of medium term bullish reversal. Intraday bias is now on the upside for retesting 0.7082 key resistance next. On the downside, break of 0.6809 support is needed to signal completion of the rise. Otherwise, outlook will stay cautiously bearish in case of retreat.

In the bigger picture, the case of medium term bullish reversal is building up with bullish convergence condition in weekly MACD. But there is no clear confirmation yet. As long as 0.7082 resistance holds, larger down trend from 0.8135 (2018 high) is still expect to continue to 0.6008 (2008 low). However, decisive break of 0.7082 will confirm medium term bottoming and bring stronger rally.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits M/M Sep | 7.20% | 2.30% | 0.80% | 0.90% |

| 23:50 | JPY | Industrial Production M/M Sep P | 1.40% | 0.40% | -1.20% | |

| 0:00 | NZD | ANZ Business Confidence Oct | -42.4 | -54.1 | -53.5 | |

| 0:01 | GBP | GfK Consumer Confidence Oct | -14 | -13 | -12 | |

| 0:30 | AUD | Private Sector Credit M/M Sep | 0.20% | 0.30% | 0.20% | |

| 0:30 | AUD | Import Price Index Q/Q Q3 | 0.40% | 0.50% | 0.90% | |

| 1:30 | AUD | Building Permits M/M Sep | 7.60% | 0.10% | -1.10% | -0.60% |

| 2:00 | CNY | Manufacturing PMI Oct | 49.3 | 49.8 | 49.8 | |

| 2:00 | CNY | Non-Manufacturing PMI Oct | 52.8 | 53.7 | 53.7 | |

| 3:30 | JPY | BoJ Interest Rate Decision | -0.10% | -0.10% | -0.10% | |

| 3:30 | JPY | BoJ Outlook Report Q3 | ||||

| 5:00 | JPY | Housing Starts Y/Y Sep | -4.90% | -6.70% | -7.10% | |

| 5:00 | JPY | Consumer Confidence Index Sep | 36.2 | 35.5 | 35.6 | |

| 7:00 | EUR | Germany Retail Sales M/M Sep | 0.10% | 0.30% | 0.50% | -0.10% |

| 7:45 | EUR | France CPI M/M Oct P | -0.30% | -0.40% | ||

| 7:45 | EUR | France CPI Y/Y Oct P | 1.10% | 1.10% | ||

| 10:00 | EUR | GDP Q/Q Q3 P | 0.10% | 0.20% | ||

| 10:00 | EUR | Unemployment Rate Sep | 7.40% | 7.40% | ||

| 10:00 | EUR | CPI Y/Y Oct P | 0.70% | 0.80% | ||

| 10:00 | EUR | CPI – Core Y/Y Oct P | 1.00% | 1.00% | ||

| 11:00 | EUR | Italy GDP Q/Q Q3 P | 0.20% | 0.00% | ||

| 11:30 | USD | Challenger Job Cuts Y/Y Oct | -24.80% | |||

| 12:30 | CAD | GDP M/M Aug | 0.20% | 0.00% | ||

| 12:30 | CAD | Raw Material Price Index Sep | -1.80% | |||

| 12:30 | CAD | Industrial Product Price M/M Sep | 0.60% | 0.20% | ||

| 12:30 | USD | Personal Spending Sep | 0.30% | 0.10% | ||

| 12:30 | USD | Personal Income M/M Sep | 0.30% | 0.40% | ||

| 12:30 | USD | PCE – Price Index M/M Sep | 0.10% | 0.00% | ||

| 12:30 | USD | PCE – Price Index Y/Y Sep | 1.40% | 1.40% | ||

| 12:30 | USD | Core PCE – Price Index M/M Sep | 0.10% | 0.10% | ||

| 12:30 | USD | Core PCE – Price Index Y/Y Sep | 1.70% | 1.80% | ||

| 12:30 | USD | Initial Jobless Claims (Oct 25) | 215K | 212K | ||

| 12:30 | USD | Employment Cost Index Q3 | 0.70% | 0.60% | ||

| 13:45 | USD | Chicago PMI Oct | 47.6 | 47.1 | ||

| 14:30 | USD | Natural Gas Storage | 73B | 87B |

{kind=link}