Asian markets continued to ignore risk rally in US and trade mixed today. Sentiments are mildly weighed down by US-China tensions over Hong Kong. But reactions are so far limited. Euro and Dollar are mildly firmer in Asian session but major pairs and crosses are staying inside yesterday’s range. For the week, commodity currencies are the strongest ones so far, led by Canadian. Yen, Dollar and Swiss Franc are the worst on over optimism on economy reopening and coronavirus treatments.

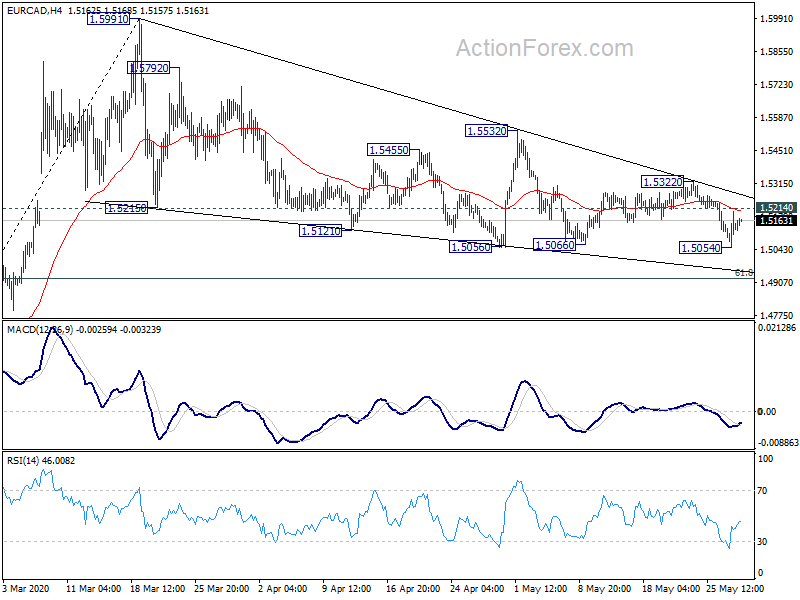

Technically, Euro is maintaining gains triggered by yesterday “Next Generation EU” recovery plan. But more is needed to confirm buying momentum. In particular, EUR/GBP is facing 0.9000 temporary top and break will resume the rise from 0.8670 to next fibonacci level at 0.9182. EUR/AUD is also eyeing 1.6763 minor resistance and break will confirm short term bottoming, as well as successful defending of 1.6597 key long term support. EUR/CAD could also attempts for a break of 1.5214 minor resistance and break will bring stronger rebound to 1.5322 resistance.

In Asia, currently, Nikkei is up 1.97%. Hong Kong HSI is down -1.24%. China Shanghai SSE is down -0.07%. Singapore Strait Times is down -0.17%. Japan 10-year JGB yield is down -0.0023 at 0. Overnight, DOW rose 2.21%. S&P 500 rose 1.48%. NASDAQ rose 0.77%. 10-year yield dropped -0.018 to 0.680.

HSI, Yuan down as Pompeo said HK no longer warrants special treatment

Hong Kong stocks tumble notably in Asian session today while off-shore Chinese Yuan also breached to a new low. US-China tensions intensified further over the proposed national security law for Hong Kong. (More details regarding the laws here). US Secretary of State Mike Pompeo told Congress on Wednesday that Hong Kong no longer qualifies for its special status as China has undermined the city’s autonomy so fundamentally.

Pompeo said China’s plan on the national security legislation was “only the latest in a series of actions that fundamentally undermine Hong Kong’s autonomy and freedoms… No reasonable person can assert today that Hong Kong maintains a high degree of autonomy from China, given facts on the ground. He certified to the Congress that Hong Kong no longer warrants treatment under U.S. laws “in the same manner as U.S. laws were applied to Hong Kong before July 1997.” “It is now clear that China is modeling Hong Kong after itself,” he added.

Separately, US also requested an emergency UN meeting over issue. Washington’s UN mission staid in a statement, that China’s proposal will “fundamentally undermine Hong Kong’s high degree of autonomy and freedoms as guaranteed under the Sino-British Joint Declaration of 1984, which was registered with the UN as a legally binding treaty… This is a matter of urgent global concern that implicates international peace and security.” However, it said that China has “refused to allow this virtual meeting to proceed”. “This is another example of the Chinese Communist Party’s fear of transparency and international accountability for its actions,” the US statement said.

China’s ambassador to the UN Zhang Jun just tweeted “Legislation on national security for Hong Kong is purely China’s internal affairs. It has nothing to do with the mandate of the Security Council.”

Despite today’s selloff, Hong Kong HSI is holding above this week’s low at 22519 so far. Technically, corrective rebound from 21139.26 should have completed at 24855.47 after rejection by 55 day EMA, and further decline is expected to retest this low. Nevertheless, break of 22519 support needs to happen first.

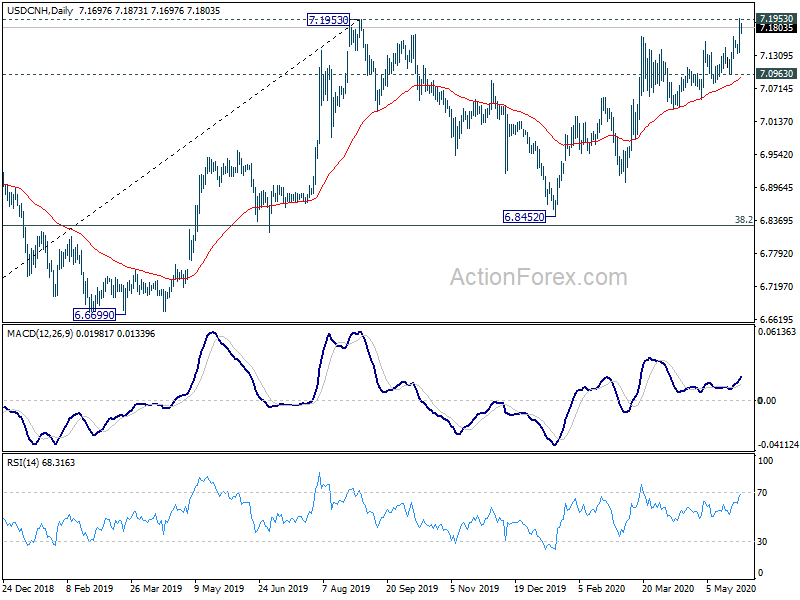

USD/CNH breached 7.1953 resistance to 7.1961, but there was no follow through buying there. We’d maintain that 7.1953 should provide technical resistance to limit upside, and bring another fall to extend the consolidation pattern. However, sustained trading above 7.1953 will indicate serious deterioration in US-China tension, which could prompt rather sharp selloff in Yuan to extend medium term up trend in USD/CNH.

Fed: Economic activity declines in all districts, falling sharply in most

Fed’s Beige Book economic report noted that “economic activity declined in all districts – falling sharply in most – reflecting disruptions associated with the COVID-19 pandemic.” Although many contacts expressed hope that overall activity would pick-up as businesses reopened, “the outlook remained highly uncertain and most contacts were pessimistic about the potential pace of recovery.”

Employment continued to “decrease in all Districts”. There were “challenges in bringing employees back to work”. Overall wage pressures were “mixed” as some firms cut wages while others implemented temporary wage increases for essential staff or to compete with unemployment insurance.

Pricing pressure varied but were “steady to down modestly on balance”. Weak demand weighed on selling prices. Several Districts also reported low commodity prices. But “supply chain disruptions and strong demand led to higher prices for some grocery items”.

RBA Lowe: Economy better than baseline, negative rates extraordinarily unlikely

RBA Governor Philip Lowe said that the economy could be “better than the baseline” scenario as forecast earlier this month. RBA projected that GDP could contract by -6% this year with unemployment rise to 9%. “With the national health outcomes better than earlier feared, it is possible that the economic downturn will not be as severe as earlier thought. Much depends on how quickly confidence can be restored,” he added.

Lowe also noted that the monetary stimulus package was working as expected. If we had to do more we could purchase more government bonds. But as things stand at the moment, we don’t see the need to doing more,” he said. He also reiterated negative interest rates were “extraordinarily unlikely”.

Released from Australia, Private capital expenditure dropped -1.5% in Q1, better than expectation of -2.7%.

New Zealand ANZ Business Confidence rose to -41.8, recovery going to be a long haul

New Zealand ANZ Business Confidence improved to -41.8 in May, up from May’s prelim reading of -45.6, and April’s -66.6. All industry stayed negative, worst in Agriculture at -82.1. Activity Outlook improved to -38.7, up from May’s prelim reading of -42.0, and April’s -55.1. Retail activity was worst at -45.3. Also, with the Activity Outlook stayed well below 2008.09 lows, and would “need to rise another 17 points just to reach its lows from the 2009 recession”.

ANZ also noted, “it’s a long way back to normality” while “the recession is just starting to make itself felt”. The economy needs to “reshape to face to the new reality”, in particular, the loss of international tourists “completely for now, but likely still at a hugely significant scale for years”. “Fiscal and monetary policy are doing what they can to cushion the blow and sow the seeds of recovery, but it’s going to be a long haul.”

Looking ahead

Eurozone confidence indicators will be the main features in European session, along with Germany CPI. Later in the day, US will release jobless claims again, with Q1 GDP revision, durable orders and pending home sales.

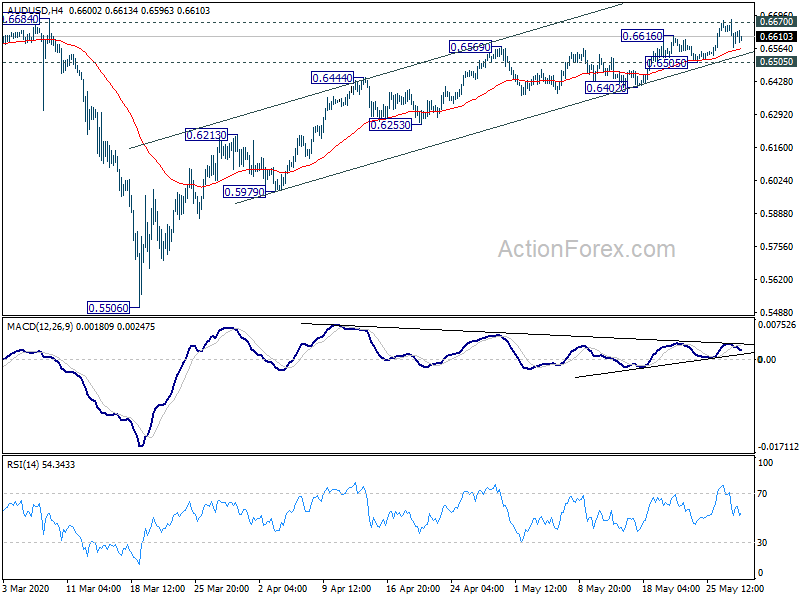

AUD/USD Daily Report

Daily Pivots: (S1) 0.6568; (P) 0.6624; (R1) 0.6680; More…

Intraday bias in AUD/USD is turned neutral with 4 hour MACD crossed below signal line. Focus remains on 0.6670 key resistance. Rejection from there, followed by 0.6505 support will indicate short term topping. Intraday bias will be turned back to the downside for 0.6402 support first. However, sustained break of 0.6670 will carry larger bullish implications and target 0.7031 resistance next.

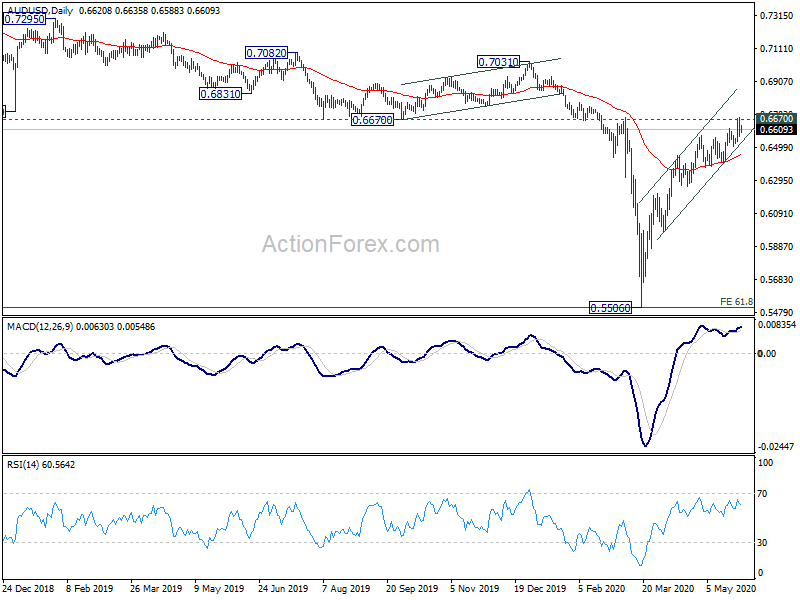

In the bigger picture,the larger down trend from 1.1079 (2011 high) might still extend. 61.8% projection of 1.1079 to 0.6826 from 0.8135 at 0.5507 is already met. Sustained break there will pave the way to 0.4773 (2001 low). On the upside, however, sustained break of 0.6607 will suggest medium term bottoming and turn focus to 0.7031 resistance next. Decisive break there will turn outlook bullish for 0.8135 (2017 high) next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 1:00 | NZD | ANZ Business Confidence May | -41.8 | -45.6 | ||

| 1:30 | AUD | Private Capital Expenditure Q1 | -1.50% | -2.70% | -2.80% | -2.60% |

| 9:00 | EUR | Eurozone Economic Sentiment Indicator May | 70.5 | 67 | ||

| 9:00 | EUR | Eurozone Industrial Confidence May | -25.4 | -30.4 | ||

| 9:00 | EUR | Eurozone Services Sentiment May | -28.4 | -35 | ||

| 9:00 | EUR | Eurozone Consumer Confidence May | -18.8 | -18.8 | ||

| 9:00 | EUR | Eurozone Business Climate May | -1.81 | |||

| 12:00 | EUR | Germany CPI M/M May P | -0.10% | 0.40% | ||

| 12:00 | EUR | Germany CPI Y/Y May P | 0.60% | 0.90% | ||

| 12:30 | CAD | Current Account (CAD) Q1 | -8.8B | |||

| 12:30 | USD | Initial Jobless Claims (May 22) | 2438K | |||

| 12:30 | USD | GDP Annualized Q1 P | -4.80% | -4.80% | ||

| 12:30 | USD | GDP Price Index Q1 P | 1.40% | |||

| 12:30 | USD | Durable Goods Orders Apr | -18.10% | -15.30% | ||

| 12:30 | USD | Durable Goods Orders ex Transportation Apr | -14.00% | -0.60% | ||

| 14:00 | USD | Pending Home Sales M/M Apr | -15.00% | -20.80% | ||

| 14:30 | USD | Natural Gas Storage | 81B | |||

| 15:00 | USD | Crude Oil Inventories | -5.0M |

{kind=link}