Commodity currencies recover mildly in Asian session but remain the worst performing ones for the week. Markets seemed to have priced in RBNZ standing pat well already. New Zealand Dollar recovered very quickly after initial spike following the announcement. On the other hand, Swiss Franc, Yen and to a lesser extent are still the strongest ones, digesting this week’s gains. Focus will now turn to inflation data from UK and Canada, and then FOMC minutes.

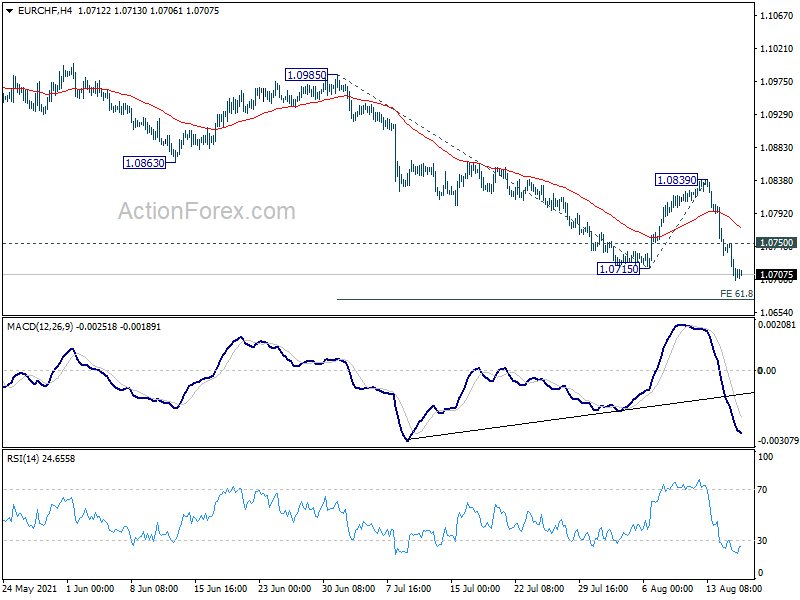

Technically, EUR/CHF has broken 1.0715 support while EUR/JPY also took out 128.58 support. Both developments suggest resumption of recent decline. EUR/USD also showed some weakness by breaching 1.1705 support. Sustained trading below there could spark downside acceleration, which would be reflected in EUR/CHF and EUR/JPY too.

In Asia, at the time of writing, Nikkei is up 0.57%. Hong Kong HSI is up 0.63%. China Shanghai SSE is up 0.40%. Singapore Strait Times is up 1.00%. Japan 10-year JGB yield is up 0.002 at 0.011. Overnight, DOW dropped -0.79%. S&P 500 dropped -0.71%. NASDAQ dropped -0.93%. 10-year yield rose 0.001 to 1.258.

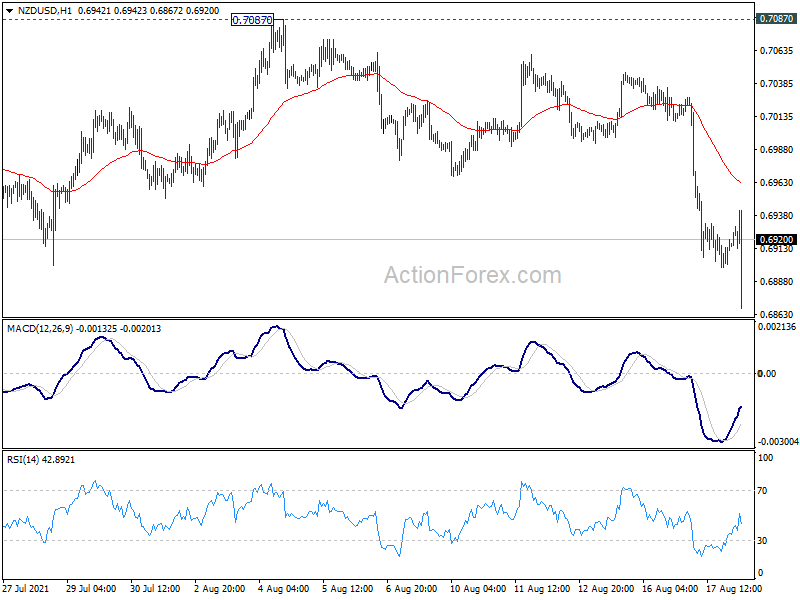

RBNZ keeps rate unchanged on heightened uncertainty. NZD spikes lower and recovered

RBNZ kept Official Cash Rate unchanged at 0.25% today, instead of raising it. The decision was “made in the context of the Government’s imposition of Level 4 COVID restrictions on activity across New Zealand.” Nevertheless, it reiterated that the “least regrets policy stance” was still to “further reduce the level of monetary stimulus”. But the Committee agreed to stand pat at this meeting “given the heightened uncertainty with the country in a lockdown.”

In the summary record, it’s also noted that committee members “now had more confidence that rising capacity pressures will feed through into inflation, and that employment is at its maximum sustainable level.” They concluded that “they could continue removing monetary stimulus”, following haling the LSAP program in July.

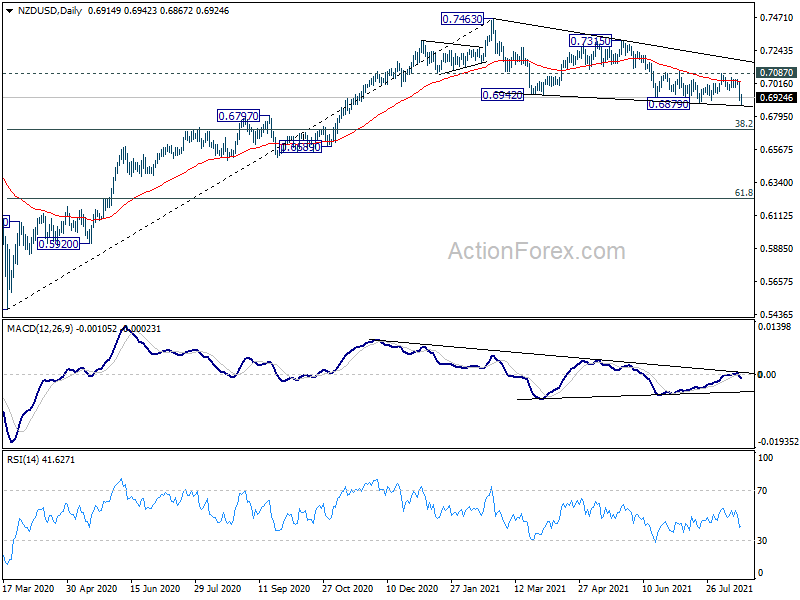

NZD/USD spiked lower to 0.6867 after the announcement but quickly recovered. Outlook stays bearish as long as 0.7087 resistance holds. Sustained break of 0.6879 support will extend the fall from 0.7463 to 38.2% retracement of 0.5467 to 0.7463 at 0.6701.

Also from New Zealand, PPI input accelerated to 3.0% qoq in Q2, up from 2.1% qoq, well above expectation of 0.5% qoq. PPI output jumped to 2.6% qoq, up from 1.2% qoq, above expectation of 0.1% qoq.

Australia leading index dropped to 1.3 in Jul, still consistent with above trend growth

Australia Westpac-MI leading index dropped from 1.36% to 1.30% in July. The index is still consistent with above trend growth over the next 3 to 9 months. Nevertheless, Westpac also said, “no Leading Index can accurately predict the impact of sudden virus lockdowns, although the direct effects of measures will start to become more apparent in the August Index.”

Also, with the deteriorating outlook in New South Wales and Melbourne due to lockdowns, West pact has revised down Q3 GDP forecast to a contraction of -2.6%, to be followed by 2.6% growth in Q4, and very strong growth of 5.0% in 2022.

Westpac added that RBA would likely to “take the same approach” as August in September meeting. That is, there would be no response to the current lockdown risks. However, it added, “we certainly cannot rule out a policy change in September especially if, as we assess, developments have raised some questions as to the vulnerability and timing of the expected recovery.

Also released, Wage price index rose 0.4% qoq in Q2, below expectation of 0.6% qoq.

Japan exports rose 37.0% yoy in Jul, imports rose 28.5% yoy

Japan export rose 37.0% yoy to JPY 7356B in July, slightly below expectation of 39.0% yoy. By region, exports to China rose 18.9% yoy, led by chip-making equipment and plastic. Exports to the US grew 26.8% yoy, led by exports of cars, car parts and motors. Imports rose 28.5% yoy to JPY 6915B, below expectation of 35.1% yoy. Trade balance came in at JPY 441B.

In seasonally adjusted term, exports was unchanged at JPY 7049B. Imports dropped -1.6% mom to 6997B. Trade balanced reported a surplus of JPY 52.7B.

Also from Japan, machinery orders dropped -1.6% mom in June, versus expectation of -2.8% mom.

Fed Powell: People and businesses have improvised and learned to adapt to COVID

Fed Chair Jerome Powell said yesterday that “it’s not yet clear whether the Delta strain will have important effects on the economy; we’ll have to see about that.” While COVID is “still with us,” he said, “people and businesses have improvised and learned to adapt.”

The pandemic is “still casting a shadow on economic activity. We cannot declare victory yet,” Powell said. But “many companies … have adapted their business models to the new world,”

Separately, Minneapolis Fed President Neel Kashkari said it’s “reasonable” to start tapering later this year. “There’s a lot of public discussion about, will it be at the end of this year, will it be the beginning of next year: Those seem like reasonable ranges of deliberation, but ultimately it will be driven by the data,” he added.

Looking ahead

UK CPI and PPI will be a main focus in European session while Eurozone will release CPI final. Later in the day, Canada will also release CPI. US will release housing starts and building permits, as well as FOMC minutes.

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.0692; (P) 1.0722; (R1) 1.0744; More….

EUR/CHF’s break of 1.0715 support suggests resumption of fall from 1.1149. Intraday bias is back on the downside for 61.8% projection of 1.0985 to 1.0715 from 1.0839 at 1.0672 first. Break will target 100% projection at 1.0569 next. On the upside, break of 1.0750 minor resistance will turn intraday bias neutral and bring consolidations. But outlook will stay bearish as long as 1.0839 resistance holds.

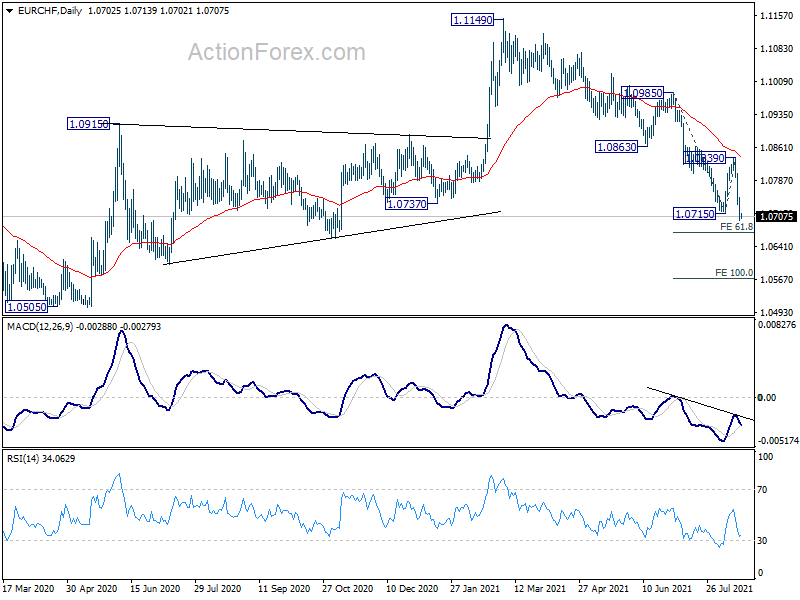

In the bigger picture, rebound from 1.0505 (2020 low) should have completed at 1.1149 already. The three-wave corrective structure argues that the downtrend from 1.2004 (2018 high) is not over yet. Medium term outlook will now stay bearish as long as 55 week EMA (now at 1.0865) holds. Break of 1.0505 low would be seen at a later stage.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | PPI Input Q/Q Q2 | 3.00% | 0.50% | 2.10% | |

| 22:45 | NZD | PPI Output Q/Q Q2 | 2.60% | 0.10% | 1.20% | |

| 23:50 | JPY | Trade Balance (JPY) Jul | 0.05T | 0.12T | -0.09T | -0.06T |

| 23:50 | JPY | Machinery Orders M/M Jun | -1.50% | -2.80% | 7.80% | |

| 00:30 | AUD | Westpac Leading Index M/M Jul | -0.10% | -0.06% | ||

| 01:30 | AUD | Wage Price Index Q/Q Q2 | 0.40% | 0.60% | 0.60% | |

| 02:00 | NZD | RBNZ Rate Decision | 0.25% | 0.50% | 0.25% | |

| 03:00 | NZD | RBNZ Press Conference | ||||

| 06:00 | GBP | CPI M/M Jul | 0.30% | 0.50% | ||

| 06:00 | GBP | CPI Y/Y Jul | 2.20% | 2.50% | ||

| 06:00 | GBP | Core CPI Y/Y Jul | 2.20% | 2.30% | ||

| 06:00 | GBP | RPI M/M Jul | 0.30% | 0.70% | ||

| 06:00 | GBP | RPI Y/Y Jul | 3.70% | 3.90% | ||

| 06:00 | GBP | PPI Input M/M Jul | 1.20% | -0.10% | ||

| 06:00 | GBP | PPI Input Y/Y Jul | 10.80% | 9.10% | ||

| 06:00 | GBP | PPI Output M/M Jul | 0.40% | 0.40% | ||

| 06:00 | GBP | PPI Output Y/Y Jul | 4.80% | 4.30% | ||

| 06:00 | GBP | PPI Core Output M/M Jul | 0.30% | |||

| 06:00 | GBP | PPI Core Output Y/Y Jul | 2.70% | |||

| 09:00 | EUR | Eurozone CPI Y/Y Jul F | 2.20% | 2.20% | ||

| 09:00 | EUR | Eurozone CPI – Core Y/Y Jul F | 0.70% | 0.70% | ||

| 12:30 | USD | Housing Starts Jul | 1.60M | 1.64M | ||

| 12:30 | USD | Building Permits Jul | 1.61M | 1.59M | ||

| 12:30 | CAD | CPI M/M Jul | 0.40% | 0.30% | ||

| 12:30 | CAD | CPI Y/Y Jul | 3.40% | 3.10% | ||

| 12:30 | CAD | CPI Common Y/Y Jul | 1.80% | 1.70% | ||

| 12:30 | CAD | CPI Median Y/Y Jul | 2.40% | 2.40% | ||

| 12:30 | CAD | CPI Trimmed Y/Y Jul | 2.50% | 2.60% | ||

| 14:30 | USD | Crude Oil Inventories | -1.5M | -0.4M | ||

| 18:00 | USD | FOMC Minutes |

{kind=link}