Market reactions to the more hawkish than expected Fed projections were relatively muted. Stocks ended just slightly down while there was no buying momentum for Dollar. The greenback is staying as the worst performer for the week, followed by commodity currencies. Euro is leading Sterling and Swiss Franc as the strongest ones while Yen is mixed. Focuses will now turn to SNB, BoE and ECB rate decisions today.

Technically, Gold lost momentum again after spiking higher to 1824.31 earlier in the week. While further rise cannot be ruled out, loss of downside moment, as seen in bearish divergence condition in 4 hour MACD, could cap upside at 61.8% projection of 1616.51 to 1786.83 at 1728.48 at 1898.80. Break of 1777.42 support will confirm short term topping and bring deeper fall to 1728.48 support, and possibly below. If happens, that could be a signal of Dollar’s rebound too.

In Asia, at the time of writing, Nikkei is down -0.41%. Hong Kong HSI is down -1.16%. China Shanghai SSE is down -0.23%. Singapore Strait Times is down -0.24%. Japan 10-year JGB yield is down -0.0007 at 0.258. Overnight, DOW dropped -0.42%. S&P 500 dropped -0.61%. NASDAQ dropped -0.76%. 10-year yield rose 0.002 to 3.503.

Fed hikes 50bps, rate to hit 5.1% in 2023

Fed raised interest rate by 50bps to 4.25-4.50% as widely expected. The decision was unanimous.

Tightening bias is maintained as “the Committee anticipates that ongoing increases in the target range will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time”.

In the new median economic projections:

- Federal funds rate is projected to hit 5.1% in 2023, then falls back to 4.1% in 2024, and then 3.1% in 2015.

- Real GDP growth was revised down from 1.2% to 0.5% in 2023, from 1.7% to 1.6% in 2024, and unchanged at 1.8% in 2025.

- Unemployment rate was revised up from 4.4% to 4.6% in 2023, from 4.4^ to 4.6% in 2024, and from 4.3% to 4.5% in 2025.

- PCE inflation was revised up from 2.8% to 3.1% in 2023, 2.3% to 2.5% in 2024, a and from 2.0% to 2.1% in 2025.

- Core PCE inflation was revised up from 3.1% to 3.5% in 2023, 2.3% to 2.5% in 2024 and unchanged at 2.1% in 2025.

In the “dot plot”

- 17 policy makers expect interest rate to climb to 5.125% and above in 2023, with 7 expects 5.375% and above.

- 12 policy makers expect interest to fall back to 4.125% in 2024 and below.

More on Fed:

- Fed Review: FOMC Signals Fed Funds above 5% in 2023

- What to Make of December’s FOMC Meeting?

- FOMC Meeting Recap: Powell Presser Poses More Questions than Answers

- (FED) Federal Reserve Issues FOMC Statement

Australia employment grew 64k in Nov, participation rate back at record high

Australia employment grew 64.0k in November, much better than expectation of 19.4k. Unemployment rate was unchanged at 3.4%, matched expectations. Participation rate rose 0.2% to 66.8%. Monthly hours worked dropped -0.4% mom.

Bjorn Jarvis, head of labour statistics at the ABS, said: “The participation rate increased by 0.2 percentage points to 66.8 per cent in November, returning to the record high we saw in June 2022. It was 1.0 percentage point higher than before the pandemic.”

“The record high participation rate continues to show that it is a tight labour market, especially when coupled with very low unemployment.”

Japan continues trade deficit streak for the 16th month

Japan export rose 20.0% yoy to JPY 8838B in November, a record high, led by cars autos and mining machinery shipment to the US. Imports rose 30.3% yoy to JPY 10865B, also a record high, as led by imports of crude oil, coal and LNG.

Trade deficit came in at JPY -2.03T. That the 16th straight month of trade deficit, and the fourth month in a row at the JPY 2T level.

In seasonally adjusted term, exports dropped -1.4% mom to JPY 8787B. Imports dropped -5.3%mom to JPY 10520B. Trade deficit narrowed to JPY -1.73T, versus expectation of JPY -1.24T.

China retail sales down -5.9% yoy in Nov, industrial production up 2.2% yoy

China retail sales contracted -5.9% yoy in November, much worse than expectation of -3.9% mom. Industrial production grew 2.2% yoy, below expectation of 3.4% yoy. Fixed asset investment rose 5.3% ytd yoy, below expectation of 5.6%.

“The consumption market was under pressure in November due to the impact of Covid and other factors, and the decline in market sales widened,” said NBS statistician Fu Jiaqi.

“However, online consumption grew faster, retail sales of basic living goods increased relatively well, some upgraded consumption was higher than overall, and retail businesses such as supermarkets and convenience shops increased steadily.”

Previews on SNB, BoE and ECB

SNB, BoE and ECB rate decisions are the focuses of the day and all are expected to deliver 50bps rate hikes.

There are some talks that given SNB only meets every quarter, it may surprise the market by maintaining the pace of 75bps. But the balance is more towards a 50bps hike to 1.00%. Tightening bias should be maintained while some focuses will be on the rhetoric on Swiss Franc exchange rate.

BoE is expected to raise policy rate by 50bps to 3.50%. Some attention will be on the voting. Last month, only seven MPC members voted for the 75bps hike. Swati Dhingra voted for 50bps, while Silvana Tenreyro voted for 25bps.

ECB should raise the main refinancing rate by 50bps to 2.50%. Additionally, it would announce some key principles regarding quantitative tightening, but the details main only come later, probably at February’s meeting. The new economic projections would also be watched closely on the central banks view on the path of slowing inflation and recession.

Here are some previews for SNB, BoE and ECB:

- SNB Meets But Developments Elsewhere Could Carry More Weight for Swissie

- BoE Set for Another Rate Hike, But Divisions May Widen

- Bank of England Preview

- Bank of England Preview – Back to 50bp as BoE Nears End of Hiking Cycle

- ECB Rate Decision, How Sure is 50bps Hike?

- ECB Preview: Will Lagarde Deliver a Hawkish Surprise?

- Will the ECB Signal the Need for More Rate Hikes?

- ECB Preview – A Hawkish 50bp

On the data front

Canada will release housing starts. US will release jobless claims, retail sales, Empire State manufacturing, Philly Fed survey, industrial production and business inventories.

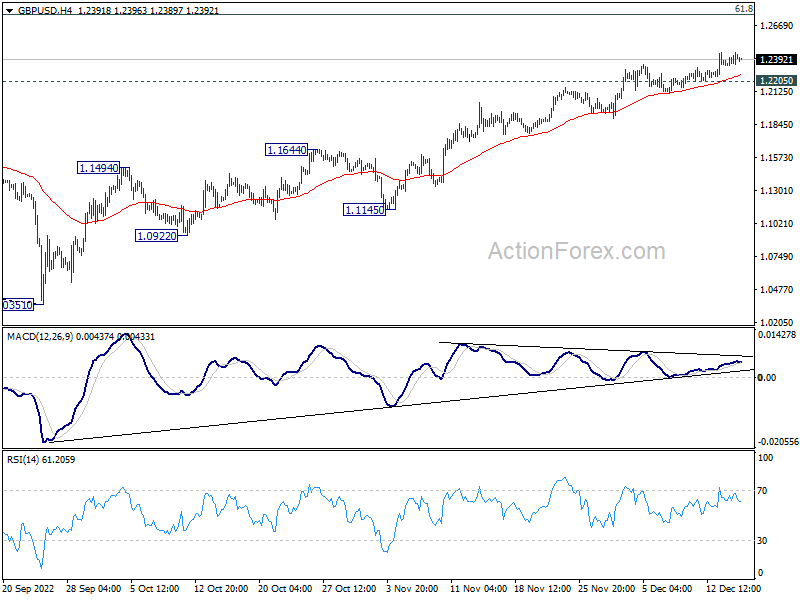

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2365; (P) 1.2405; (R1) 1.2469; More…

GBP/USD is losing upside momentum as seen in 4 hour MACD. But there is no sign of topping yet. Current rise from 1.0351 is still in progress to 1.2759 medium term fibonacci level next. However, on the downside, break of 1.2205 will indicate short term topping, and turn bias back to the downside for deeper pull back to 55 day EMA (now at 1.1860).

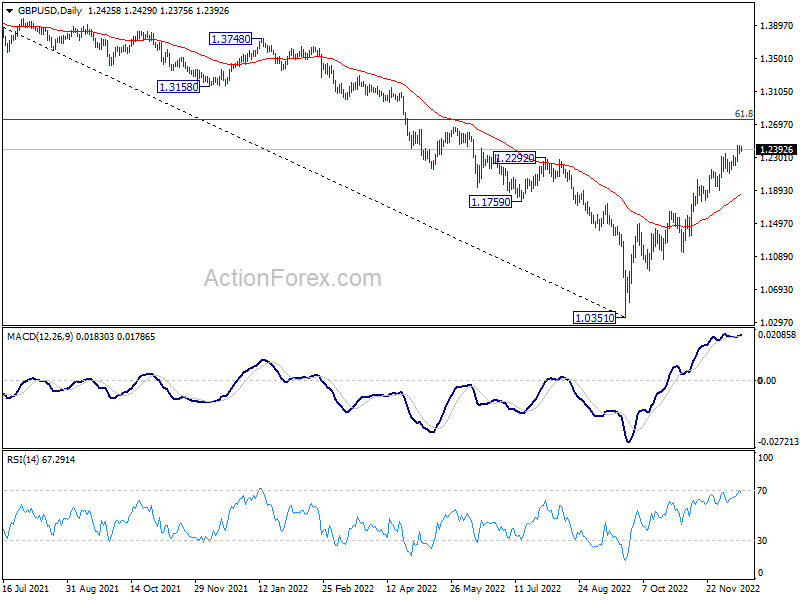

In the bigger picture, rise from 1.0351 medium term bottom is at least correcting whole down trend from 1.4248 (2021 high). Further rise is expected as long as 1.1644 resistance turned support holds. Next target is 61.8% retracement of 1.4248 to 1.0351 at 1.2759. Sustained break there will pave the way back to 1.4248. This will remain the favored case as long as 55 day EMA (now at 1.1860) holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | GDP Q/Q Q3 | 2.00% | 0.80% | 1.70% | 1.90% |

| 23:50 | JPY | Trade Balance (JPY) Nov | -1.73T | -1.24T | -2.30T | -2.21T |

| 00:00 | AUD | Consumer Inflation Expectations Dec | 5.20% | 6.00% | ||

| 00:30 | AUD | Employment Change Nov | 64.0K | 19.4K | 32.2K | 43.1K |

| 00:30 | AUD | Unemployment Rate Nov | 3.40% | 3.40% | 3.40% | |

| 02:00 | CNY | Industrial Production Y/Y Nov | 2.20% | 3.40% | 5.00% | |

| 02:00 | CNY | Retail Sales Y/Y Nov | -5.90% | -3.90% | -0.50% | |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Nov | 5.30% | 5.60% | 5.80% | |

| 04:30 | JPY | Tertiary Industry Index M/M Oct | 0.20% | 0.40% | -0.40% | |

| 08:30 | CHF | SNB Interest Rate Decision | 1.00% | 0.50% | ||

| 09:00 | CHF | SNB Press Conference | ||||

| 12:00 | GBP | BoE Interest Rate Decision | 3.50% | 3.00% | ||

| 12:00 | GBP | MPC Official Bank Rate Votes | 9–0–0 | 9–0–0 | ||

| 13:15 | CAD | Housing Starts Nov | 255K | 267K | ||

| 13:15 | EUR | ECB Main Refinancing Rate | 2.50% | 2.00% | ||

| 13:30 | USD | Initial Jobless Claims (Dec 9) | 230K | 230K | ||

| 13:30 | USD | Retail Sales M/M Nov | -0.10% | 1.30% | ||

| 13:30 | USD | Retail Sales ex Autos M/M Nov | 0.20% | 1.30% | ||

| 13:30 | USD | Empire State Manufacturing Index Dec | -0.2 | 4.5 | ||

| 13:30 | USD | Philadelphia Fed Manufacturing Survey Dec | -11.3 | -19.4 | ||

| 13:45 | EUR | ECB Press Conference | ||||

| 14:15 | USD | Industrial Production M/M Nov | 0.10% | -0.10% | ||

| 14:15 | USD | Capacity Utilization Nov | 79.80% | 79.90% | ||

| 15:00 | USD | Business Inventories Oct | 0.40% | 0.40% | ||

| 15:30 | USD | Natural Gas Storage | -21B |

{kind=link}