The forex markets saw limited movement in Asian session today, with most major pairs and crosses remaining within yesterday’s range. While Aussie is trading slightly higher, there is no decisive momentum. For the week, Kiwi is currently the strongest, followed by Euro and then Aussie. Meanwhile, Yen is performing worst, followed by Dollar and Swiss Franc. It’s overall a risk-on setting, thanks to rebound in US stocks overnight. However, it remains to be seen if this trend will continue in coming days.

On technical front, Bitcoin’s sharp decline today has raised doubts about underlying risk appetite. The main question is whether there is enough buying power to push it through structural resistance at 25198 and confirm a bullish trend reversal. On the other hand, a break of support at 21357 would indicate rejection by 25198 and completion of the rebound from 15452. If that were to happen, a deeper fall could be expected, potentially back towards this low. Such a development could also be accompanied by a deeper selloff in NASDAQ, which leads risk markets lower, and supports Dollar.

In Asia, Nikkei closed up 1.55%. Hong Kong HSI is up 1.01%. China Shanghai SSE is up 0.41%. Singapore Strait Times is up 0.16%. Japan 10-year JGB yield is up 0.0121 at 0.509. Overnight, DOW rose 1.05%. S&P 500 rose 0.76%. NASDAQ rose 0.73%. 10-year yield rose 0.079 to 4.073.

Fed Waller: May need rate above 5.1-5.4% if data continue to be too hot

Fed Governor Christopher Waller said that “a barrage of data” in February has challenged high view that FOMC was “making progress in moderating economic activity and reducing inflation.”

“It could be that progress has stalled, or it is possible that the numbers released last month were a blip,” he said.

“If job creation drops back down to a level consistent with the downward trajectory seen late last year and CPI inflation pulls back significantly from the January numbers and resumes its downward path, then I would endorse raising the target range for the federal funds rate a couple more times, to a projected terminal rate between 5.1 and 5.4 percent,” he said.

“On the other hand, if those data reports continue to come in too hot, the policy target range will have to be raised this year even more to ensure that we do not lose the momentum that was in place before the data for January were released,” he added.

Fed Collins: We will need to do some additional rate increases

Boston Fed President Susan Collins said yesterday, “we will need to do some additional rate increases and exactly what the right amount is really needs to be dependent on a holistic review of the information that we receive.”

“It will be important to hold there for some time because it takes a while for the effects of tighter financial conditions to work through the economy,” she added.

“We’ve seen some early signs that wage and price pressures might be slowing,” she said. “But we’ve also seen some evidence that high inflation” remains, particularly in some areas of services.

Fed Bostic: There is the case we need to go higher

Atlanta Fed President Raphael Bostic said yesterday, “there is the case that could be made that we need to go higher” on interest rate.

“Consumer spending is strong and labor markets remain quite tight and that those suggest that the economy’s strength could be a bit more than people think, which means we might need to do more.”

“I’m going to stay open to any possibility that if data come in stronger than expected then I will adjust my policy trajectory,” Bostic said.

BoE Pill: Current momentum in economic activity may be slightly stronger than anticipated

In a speech yesterday, BoE Chief Economist Huw Pill said that “current momentum in economic activity may be slightly stronger than anticipated.”

“CPI inflation is projected to fall to below the 2% target by the end of the forecast horizon”, he said. But “there are considerable uncertainties around this outlook.”

“Upside risks arise in large part from the possibility that domestic inflationary pressures prove more persistent than anticipated, owing to so-called ‘second round effects’ in price, cost and wage setting behaviour,” he explained.

“The latest data for private sector regular pay growth – which was published after the MPC’s forecast was finalised – surprised slightly to the upside.”

Nevertheless, “some high-frequency indicators of wages have fallen quite sharply recently”.

“The MPC will continue to monitor indications of persistence in domestic inflationary pressures closely, with a focus on developments in the labour market, in wage dynamics, in services price inflation and in measures of underlying inflation and inflation expectations.”

China PMI services rose to 55.0, composite rose to 54.2

China Caixin PMI Services rose from 52.9 to 55.0 in February, above expectation of 54.7. That’s also the highest reading since April 2021. PMI Composite rose from 51.1 to 54.2, highest since May 2021.

Wang Zhe, Senior Economist at Caixin Insight Group said: “Both manufacturing and services activity recovered gradually. Production, demand, including external demand, and employment all grew, with services activity showing a stronger recovery than manufacturing output. Input costs and prices charged remained stable, and business owners were highly optimistic.”

Looking ahead

Germany trade balance, France industrial output, Eurozone PMI services final and PPI, UK PMI services final will be released in European session. Later in the day, US ISM services is the main focus. Canada will release building permits and labor productivity.

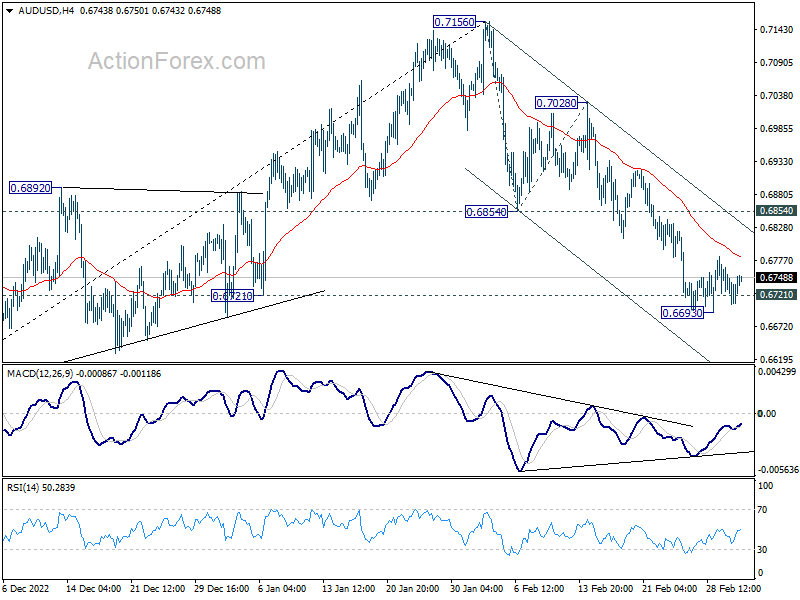

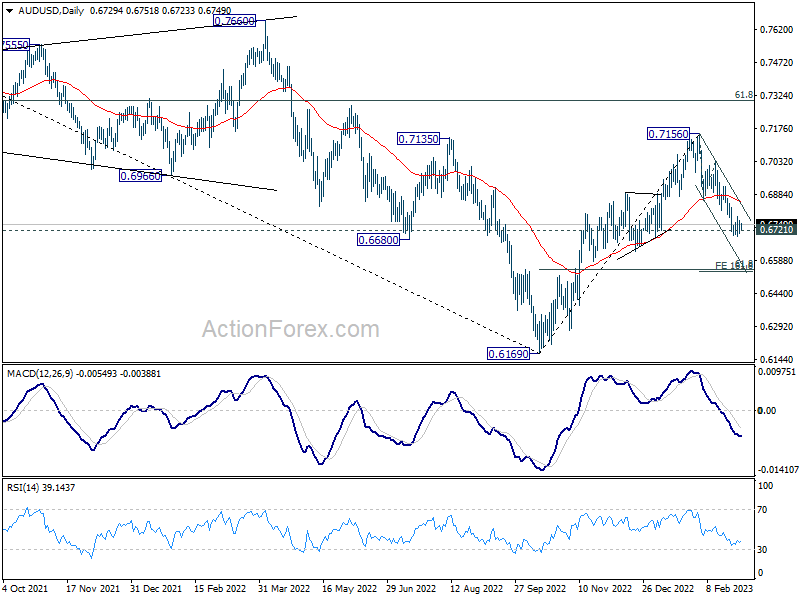

AUD/USD Daily Report

Daily Pivots: (S1) 0.6703; (P) 0.6734; (R1) 0.6762; More…

AUD/USD is staying in tight range above 0.6693 low and intraday bias remains neutral. Deeper decline is expected as long as 0.6854 support turned resistance holds. Break of 0.6693 will resume the fall from 0.7156 to 161.8% projection of of 0.6854 to 0.7028 from 0.6854 at 0.6539. Nevertheless, firm break of 0.6854 will argue that such decline is finished, and revive near term bullishness.

In the bigger picture, focus is now on 0.6721 structural support. Sustained break there will argue that whole rise from 0.6169 (2022 low) has completed at 0.7156, after rejection by 55 month EMA (now at 0.7179). Deeper decline would then be see back to 61.8% retracement of 0.6169 to 0.7156 at 0.6546, even as a corrective fall. Nevertheless, strong rebound from current level will retain medium term bullishness for another rise through 0.7156 later.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Core Y/Y Feb | 3.30% | 3.30% | 4.30% | |

| 23:30 | JPY | Unemployment Rate Jan | 2.40% | 2.50% | 2.50% | |

| 01:45 | CNY | Caixin Services PMI Feb | 55 | 54.7 | 52.9 | |

| 07:00 | EUR | Germany Trade Balance (EUR) Jan | 11.2B | 10.0B | ||

| 07:45 | EUR | France Industrial Output M/M Jan | -0.2 | 1.10% | ||

| 08:45 | EUR | Italy Services PMI Feb | 52.4 | 51.2 | ||

| 08:50 | EUR | France Services PMI Feb F | 52.8 | 52.8 | ||

| 08:55 | EUR | Germany Services PMI Feb F | 51.3 | 51.3 | ||

| 09:00 | EUR | Eurozone Services PMI Feb F | 53 | 53 | ||

| 09:30 | GBP | Services PMI Feb F | 53.3 | 53.3 | ||

| 10:00 | EUR | Eurozone PPI M/M Jan | -0.30% | 1.10% | ||

| 10:00 | EUR | Eurozone PPI Y/Y Jan | 28.60% | 24.60% | ||

| 13:30 | CAD | Building Permits M/M Jan | 1.70% | -7.30% | ||

| 13:30 | CAD | Labor Productivity Q/Q Q4 | 0.20% | 0.60% | ||

| 14:45 | USD | Services PMI Feb F | 50.5 | 50.5 | ||

| 15:00 | USD | ISM Services PMI Feb | 54.4 | 55.2 |

{kind=link}