Australian Dollar finds itself on a broad-based downward trajectory following RBA’s decision to maintain interest rates unchanged. Despite maintaining a tightening bias, RBA’s announcement fell short of some speculations for a more hawkish outcome. In contrast, fellow commodity currencies, New Zealand Dollar and Canadian Dollar, continue to display strength. Kiwi is bracing for the upcoming RBNZ rate hike tomorrow, while Loonie rides the wave of this week’s oil price rally.

Across the currency market, Dollar emerges as the week’s weakest performer so far, trailed by Yen and Swiss Franc. Market sentiment appears to be leaning towards a risk-on scenario. Euro and British Pound are mixed but look poised to extend their recent rallies against the US Dollar.

On the technical front, WTI crude oil garners significant attention. While it has yet to firmly break through the 80 mark, its pullback from this week’s high of $81.54 remains modest. A sustained break of 80.82 resistance level could signal a bullish trend reversal, potentially pushing prices up to next resistance at 94.25. Murmurs of WTI crude oil climbing back to 100 has also started to circulate. Nevertheless, an extended rally might trigger a complex chain reaction, impacting inflation and interest rate expectations, which could then reverberate through stock and bond markets.

In Asia, at the time of writing, Nikkei is up 0.31%. Hong Kong HSI is down -0.64%. China Shanghai SSE is up 0.24%. Singapore Strait Times is up 0.79%. Japan 10-year JGB yield is up 0.215 at 0.392. Overnight, DOW rose 0.98%. S&P 500 rose 0.37%. NASDAQ dropped -0.27%. 10-year yield dropped -0.064 to 3.430.

RBA holds cash rate steady, maintains tightening bias

RBA has decided to keep the cash rate target unchanged at 3.60% amid ongoing uncertainty, but maintained its tightening bias. The central bank stated that some further tightening might be necessary, depending on developments in the global economy, household spending, inflation, and the labor market outlook.

In the official statement, RBA noted, “The Board expects that some further tightening of monetary policy may well be needed to ensure that inflation returns to target.”

RBA’s central forecast anticipates inflation to decline over the next couple of years, reaching around 3% by mid-2025. The statement highlighted that “medium-term inflation expectations remain well anchored, and it is important that this remains the case.”

Despite the slowing growth in the Australian economy, labor market remains very tight. However, as economic growth slows, RBA expects unemployment to increase. The Board remains alert to the risk of a “price-wages spiral”, given the limited spare capacity in the economy and the historically low rate of unemployment.

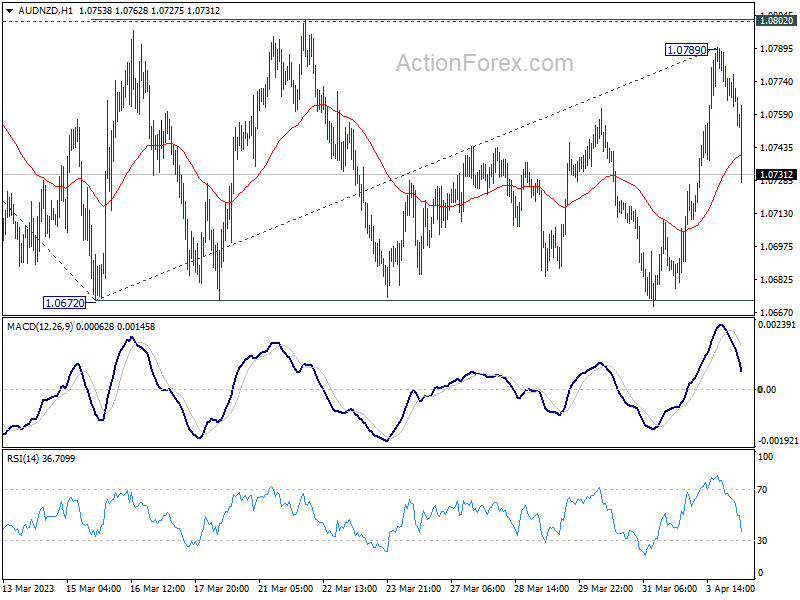

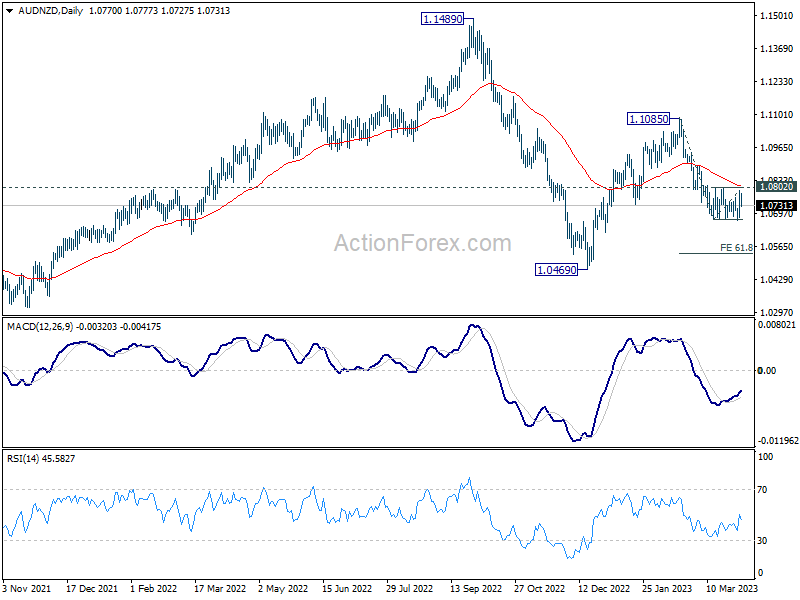

AUD/NZD falling back towards 1.0672 after RBA

AUD/NZD falls notably after RBA announced to leave interest rates unchanged. Yesterday’s rebound was primarily driven by speculation of a hawkish surprise from RBA. However, with RBA’s decision now public, market focus shifts to RBNZ upcoming rate hike and whether the statement would be hawkish enough to push AUD/NZD below 1.0672 short-term bottom.

From a technical perspective, the near-term outlook for AUD/NZD remains bearish as the 1.0802 resistance level remains intact, further supported by the currency pair’s rejection by the 55 day EMA. The decline from 1.1085 is expected to resume sooner rather than later, and a firm break below 1.0672 level would confirm resumption of the fall. This could ultimately lead the currency pair towards 61.8% projection of 1.1085 to 1.0672 from 1.0789 at 1.0534.

Fed Cook weighs economic momentum against headwinds

In a speech yesterday, Fed Governor Lisa Cook discussed her considerations for the future path of monetary policy, weighing the implications of stronger economic momentum against potential headwinds from recent banking developments.

Cook explained, “On the one hand, if tighter financing conditions restrain the economy, the appropriate path of the federal funds rate may be lower than it would be in their absence. On the other hand, if data show continued strength in the economy and slower disinflation, we may have more work to do.”

Regarding Fed’s strategy on rate hikes, Cook mentioned that FOMC has been raising rates in smaller increments, aiming for a sufficiently restrictive monetary policy to return inflation to 2% over time. She emphasized the benefit of taking smaller steps, as it allows Fed to observe economic and financial conditions and evaluate the cumulative effects of their policy actions.

Cook also touched on FOMC’s recent adjustments to its forward guidance on the path of the policy rate in its March statement. The committee shifted from anticipating “ongoing increases” to stating that “some additional policy firming may be appropriate.” Cook believes this communication is suitable as Fed seeks to calibrate monetary policy amid uncertainty about the economic outlook.

SNB Schlegel reiterates commitment to price stability and willingness to intervene

SNB Vice Chairman Martin Schlegel emphasized the central bank’s commitment to price stability in an interview with Swiss broadcaster SRF yesterday. He stated, “Our mandate is crystal clear, and that is price stability,” adding that SNB will do everything possible to bring inflation back to the target range of 0 to 2%.

Although Schlegel refrained from making any forecasts, he noted that SNB’s inflation forecasts are higher now than they were in December, adding that the central bank is prepared to “continue to raise interest rates” if necessary.

Schlegel also addressed SNB’s willingness to sell foreign currencies in order to strengthen Swiss franc. He said, “We said quite clearly at the last assessment that we are also prepared to sell foreign currencies, to actually strengthen the franc.”

He revealed that SNB had already sold CHF 27B worth of foreign currencies in the last quarter, asserting that the bank will continue to monitor the exchange rate and intervene if necessary.

Looking ahead

Germany trade balance and Eurozone PPI will be released in European session. Later in the day, Canada building permits and US factor orders will be featured.

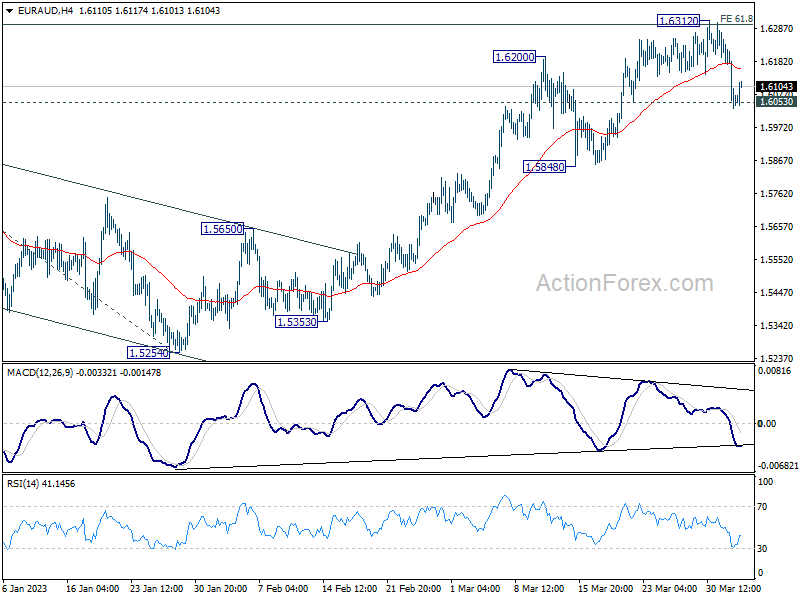

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5988; (P) 1.6114; (R1) 1.6192; More…

EUR/AUD recovers after drawing support from 1.6053 and intraday bias remains neutral first. Focus stays on 0.6389/6434 cluster resistance zone. Decisive break there will carry larger bullish implications. However, firm break of 1.6053 will confirm short term topping, after rejection by the mentioned resistance. Intraday bias will be turned back to the downside for 1.5848 support and possibly below.

In the bigger picture, focus stays on 1.6389/6434 cluster resistance (38.2% retracement of 1.9799 to 1.4281 at 1.6389). Sustained break there should confirm that whole down trend from 1.9799 (2020 high) has completed. Further rally should then be seen to 61.8% retracement at 1.7691. However, rejection by this cluster resistance will make medium term outlook neutral at best.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:00 | NZD | NZIER Business Confidence Q1 | -66 | -70 | ||

| 23:50 | JPY | Monetary Base Y/Y Mar | -1.00% | 2.00% | -1.60% | |

| 04:30 | AUD | RBA Interest Rate Decision | 3.60% | 3.60% | 3.60% | |

| 06:00 | EUR | Germany Trade Balance (EUR) Feb | 16.9B | 16.7B | ||

| 09:00 | EUR | Eurozone PPI M/M Feb | -0.30% | -2.80% | ||

| 09:00 | EUR | Eurozone PPI Y/Y Feb | 13.50% | 15.00% | ||

| 12:30 | CAD | Building Permits M/M Feb | 2.20% | -4.00% | ||

| 14:00 | USD | Factory Orders M/M Feb | -0.30% | -1.60% |

{kind=link}