Asian markets showcased a mild risk-off tone today, in the wake of lower closes in US markets overnight. However, the forex arena remains comparatively tranquil with major currency pairs and crosses largely confined within the previous day’s trading range. Lingering apprehensions regarding a potential rate hike by the Fed have resurfaced following robust US services data. Yet, the odds of a subsequent rate increase in either November or December—assuming a pause this month—continue to oscillate around the 50% mark. This ambiguity is poised to persist unless the new economic projections by Fed provide a more definitive direction.

For the week, Dollar stands tall as the dominant currency. Nonetheless, there’s a perceptible hesitation among buyers, suggesting a reluctance to propel the greenback any higher from its current position. Canadian Dollar trails closely as the second strongest, with Euro coming in third. On the flip side, Australian Dollar languishes at the bottom, feeling the pressure by lackluster Chinese trade figures. New Zealand Dollar and Yen aren’t faring much better, positioned as the second and third weakest currencies respectively. Meanwhile, Sterling and Swiss Franc are presenting a mixed performance.

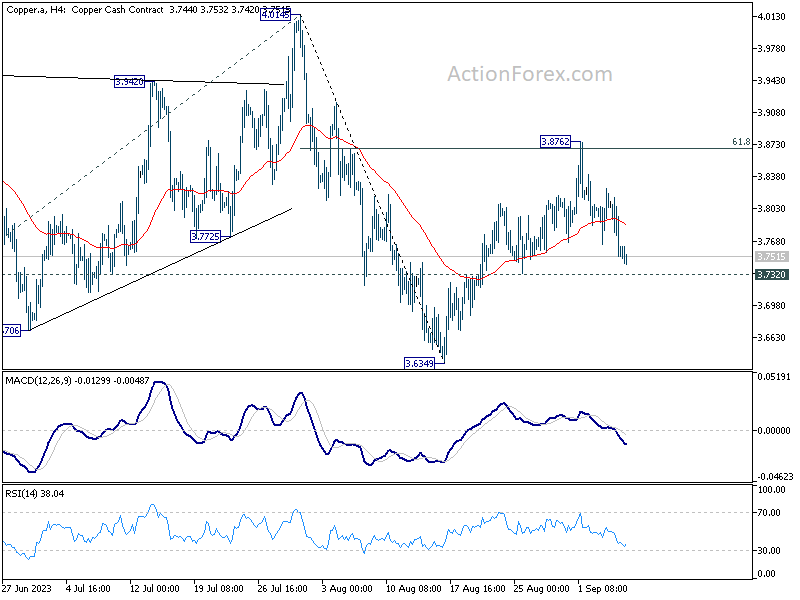

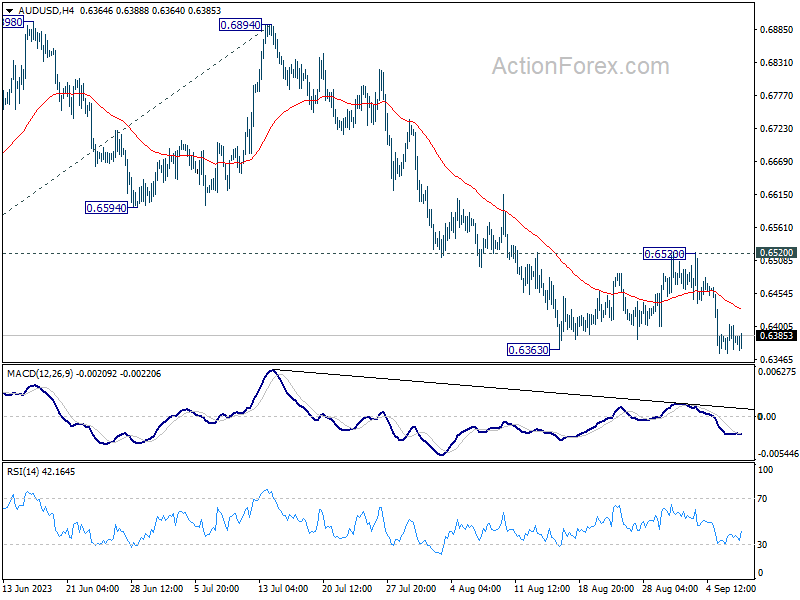

Technically, Copper’s rebound from 3.6349 was admittedly stronger than expected. But the rejection by 61.8% retracement of 4.0145 to 3.3649 and the structure still argues that it’s a corrective move. Break of 3.7320 support will indicate that fall from 4.015 is ready to resume through 3.6349. If realized, AUD/USD might follow and have enough momentum to move away from 0.6363 support finally.

In Asia, Nikkei closed down -0.73%. Hong Kong HSI is down -1.24%. China Shanghai SSE is down -1.06%. Singapore Strait Times is down -0.22%. Japan 10-year JGB yield is up 0.0042 at 0.660. Overnight, DOW dropped -0.57%. S&P 500 dropped -0.70%. NASDAQ dropped -1.06%. 10-year yield rose 0.022 to 4.290.

BoJ Nakagawa sees positive developments, but loose monetary policy still needed

BoJ Board member Junko Nakagawa struck a cautiously optimistic tone today about the Japanese economy, citing “positive developments” and “signs of change in corporate price and wage-setting behavior.”

However, she was quick to note that the country has not yet achieved its price target “in a stable, sustainable fashion.”

Nakagawa noted that there are chances inflation could accelerate beyond initial expectations. However, she also warned of the potential for inflation to decelerate once the pass-through effects of higher costs begin to moderate.

The policymaker underscored the need for BoJ to maintain its ultra-loose monetary policy for the time being, citing the prevailing economic uncertainty.

RBA Lowe cautions against complacency in managing inflation risks

In his final public speech as RBA Governor, Philip Lowe stated that for inflation to average around 2.5%, wage increases should typically align with productivity growth plus an additional 2.5%. He sees it as a “reasonable benchmark”, even it’s “not a hard and fast rule”.

Lowe’s recent attention has been particularly focused on the risk associated with the current period of high inflation. Specifically, he warned of the peril that “wages growth and profits running ahead of the rate that is consistent with a sustainable return of inflation to target.”

In such a scenario, he cautioned, inflation would become “sticky,” necessitating “tighter monetary policy and more economic pain later on.”

Lowe acknowledged that recent data offers some level of comfort but emphasized the importance of remaining alert to these inflation risks. Rise in productivity growth, he noted, would be a welcome development as it would facilitate stronger growth in both nominal and real wages and profits.

China’s exports and imports continue to contract, Yuan weakness persists

In August, China reported a fourth consecutive monthly contraction in exports, dropping -8.8% yoy to USD 284.9B. However, the contraction was narrower than market’s expectation of a -9.5% yoy decline and an improvement from July’s -14.5% yoy fall.

Imports also shrank by -7.3% yoy to USD 216.5B, beating expectations of -9.4% yoy decline and improving from July’s -12.4% yoy drop. This marks a consistent trend of contracting imports every month in 2023 compared to the year-ago period.

Despite these figures beating expectations, trade surplus shrank from USD -80.6B to USD -68.4B, almost in line with expectation of USD -60.0B.

While the narrowing contraction in exports and imports could be seen as a mildly positive development, it doesn’t significantly alter the broader narrative of economic cooling in China.

Offshore Chinese Yuan continued its decline today, sparking questions about the timing and intent of potential interventions by Chinese authorities.

USD/CNH’s correction from 7.3491 should have completed at 7.2387 already. Rise from there is likely resuming the larger up trend 6.6971. From a pure technical perspective, USD/CNH should be ready to rise through 7.3745 (2022 high) to 61.8% projection of 6.8100 to 7.2853 from 7.1154 at 7.4091.

However, this raises two crucial questions: when will the Chinese authorities step in to intervene in the currency markets, and what will be the nature of such intervention—i.e., whether they aim to set a floor for Yuan or merely slow its depreciation.

Looking ahead

Swiss foreign currency reserves, France trade balance, Italy retail sales, and Eurozone GDP revision will be release in European session.

Later in the day, Canada building permits and Ivey PMI, US jobless claims and non-farm productivity will be featured.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6358; (P) 0.6382; (R1) 0.6405; More…

Intraday bias in AUD/USD stays mildly on the downside for the moment. Current decline is part of the whole fall from 0.7156, next target is 100% projection of 0.7156 to 0.6457 from 0.6894 at 0.6195. On the upside, break of 0.6520 resistance is needed to indicate short term bottoming. Otherwise, risk will stay on the downside in case of recovery.

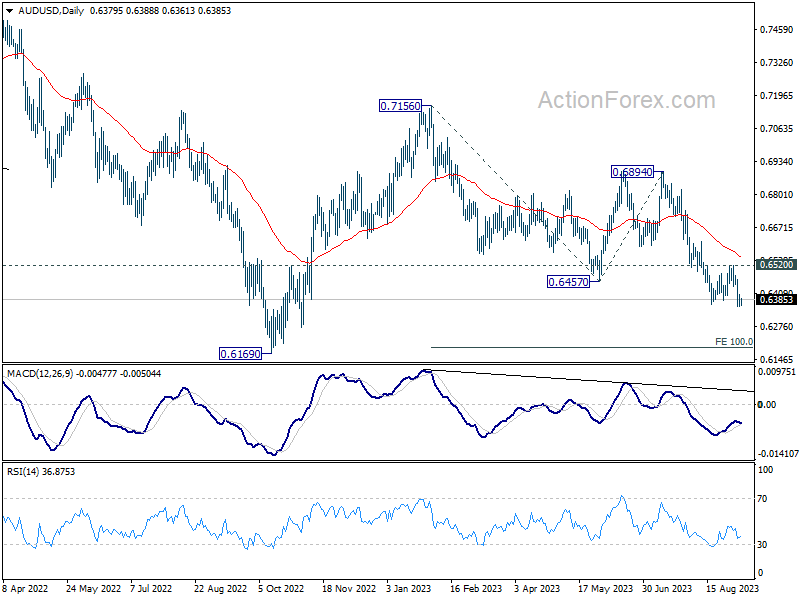

In the bigger picture, current development argues that the down trend from 0.8006 (2021 high) is still in progress. Decisive break of 0.6169 will target 61.8% projection of 0.8006 to 0.6169 to 0.7156 at 0.6021. This will now remain the favored case as long as 0.6894, in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Manufacturing Sales Q2 | 0.20% | -2.80% | -2.50% | |

| 01:30 | AUD | Trade Balance (AUD) Jul | 8.04B | 10.05B | 11.32B | 10.27B |

| 03:00 | CNY | Trade Balance (USD) Aug | 68.4B | 68.0B | 80.6B | |

| 03:00 | CNY | Trade Balance (CNY) Aug | 488B | 494B | 576B | |

| 05:00 | JPY | Leading Economic Index Jul P | 107.6 | 107.9 | 109.1 | |

| 05:45 | CHF | Unemployment Rate Aug | 2.10% | 2.10% | 2.10% | |

| 06:00 | EUR | Germany Industrial Production M/M Jul | -0.80% | -0.40% | -1.50% | |

| 06:45 | EUR | France Trade Balance (EUR) Jul | -6.8B | -6.7B | ||

| 07:00 | CHF | Foreign Currency Reserves (CHF) Aug | 698B | |||

| 08:00 | EUR | Italy Retail Sales M/M Jul | 0.20% | -0.20% | ||

| 09:00 | EUR | Eurozone GDP Q/Q Q2 | 0.30% | 0.30% | ||

| 12:30 | CAD | Building Permits M/M Jul | 7.50% | 6.10% | ||

| 12:30 | USD | Initial Jobless Claims (Sep 1) | 235K | 228K | ||

| 12:30 | USD | Nonfarm Productivity Q2 | 3.50% | 3.70% | ||

| 12:30 | USD | Unit Labor Costs Q2 | 1.80% | 1.60% | ||

| 14:00 | CAD | Ivey PMI Aug | 49.2 | 48.6 | ||

| 14:30 | USD | Natural Gas Storage | 38B | 32B | ||

| 15:00 | USD | Crude Oil Inventories | -1.8M | -10.6M |

{kind=link}