Dollar weakness continues to dominate FX markets, with the greenback staying under pressure across the board. he spotlight is on which currencies are capitalizing the most. Yen is stealing the show, along with sharp rally in the Nikkei as AI-fueled optimism sends semiconductor shares surging. Swiss Franc and Aussie are also firming, while the Kiwi and Loonie lag. Euro and Sterling are steady in the middle of the pack, with their earlier bullish momentum taking a breather.

Economic data from the US did little to reverse the greenback’s decline. Finalized Q1 GDP was revised down to -0.5%, reinforcing concerns about underlying growth momentum. Durable goods orders surprised to the upside at 16.4%, but that strength was concentrated in a 48% surge in transportation equipment—most likely driven by tariff frontloading. Jobless claims fell more than expected, but signs of labor market resilience were not enough to shift the rate cut narrative.

Earlier today, Japan’s Nikkei surged to a five-month high, with tech and chip-related stocks outperforming amid robust investor appetite linked to artificial intelligence demand. Despite pressure on automakers tied to slowing progress in US-Japan trade negotiations, the broader index rallied.

Technically, the break of trend line resistance solidifies that case medium term correction from 4246.77 has completed with three waves down to 30792.74. Further rally is expected in Nikkei as long as 38026.32 support holds. Break of 40398.23 will bring retest of 42426.77.

In Europe, at the time of writing, FTSE is up 0.24%. DAX is up 0.36%. CAC is down -0.01%. UK 10-year yield is down -0.02 at 4.464. Germany 10-year yield is down -0.023 at 2.549. Earlier in Asia, Nikkei rose 1.65%. Hong Kong HSI fell -0.61%. China Shanghai SSE fell -0.22%. Singapore Strait Times rose 0.32%. Japan 10-year JGB yield rose 0.02 to 1.425.

US durables rise 16.4% mom in May, transportation surges 48.3% mom

US durablg goods orders rose 16.4% mom to USD 343.6B in May, well above expectation of 6.8% mom. Ex-transport orders rose 0.5% mom, above expectation of 0.1% mom. Excluding defense, new orders increased 15.5% mom. Transportation equipment, up five of the last six months, led the increase, by 48.3% mom to USD 145.3B.

US initial jobless claims fall to 236k vs exp 247k

US initial jobless claims fell -10k to 236k in the ween ending June 21, below expectation of 247k. Four-week moving average of initial claims fell -750 to 245k.

Continuing claims rose 37k to 1974k in the week ending June 14, the highest level since November 6, 2021. Four-week moving average of continuing claims rose 17k to 1941k, highest since November 20, 2021.

BoE’s Bailey: Policy still restrictive to squeeze out sticky inflation

BoE Governor Andrew Bailey said in a speech today that while the UK has made notable progress on disinflation, monetary policy remains restrictive to “squeeze out remaining persistence in inflationary pressures”.

Speaking weeks ahead of the August policy meeting, Bailey stressed the presence of “two-sided risks” to inflation. He emphasized that a “gradual and careful approach” remains appropriate and monetary policy is “not on a pre-set path”.

Germany’s Gfk consumer sentiment falls to -20.3, mood sours slightly as precautionary saving picks up

German consumer sentiment slipped slightly in July, with the Gfk index easing from -20.0 to -20.3, missing expectations of a recovery to -19.0.

The drop came despite a strong rebound in the economic expectations component, which surged seven points to 20.1—its highest since the early stages of the Ukraine war. Income expectations also improved for the fourth consecutive month, rising to 12.8.

Yet the consumer climate remains weighed down by caution. The willingness-to-buy index was subdued at -6.2. The notable jump in the savings indicator to 13.9, the highest since April 2024, suggests that households are still holding back on discretionary spending.

GfK’s Rolf Bürkl pointed to rising savings as a key drag, reflecting continued uncertainty and a lack of confidence in making large purchases.

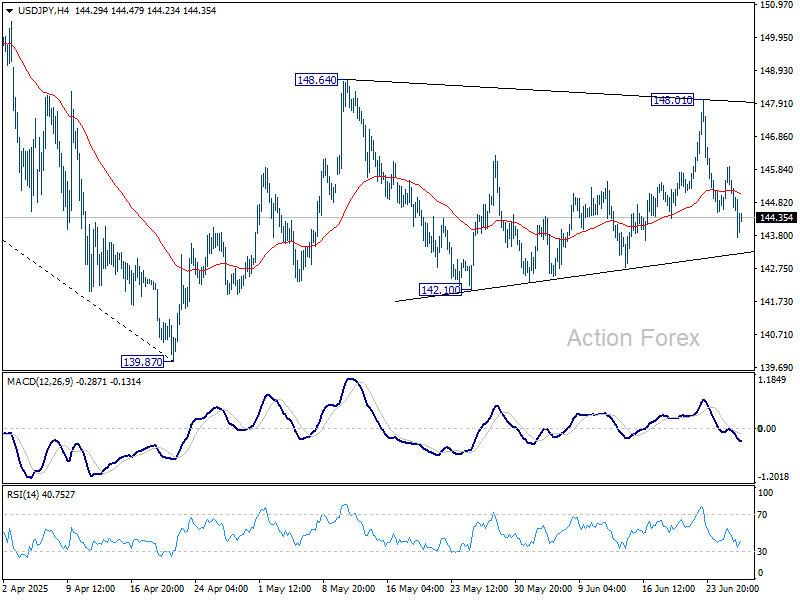

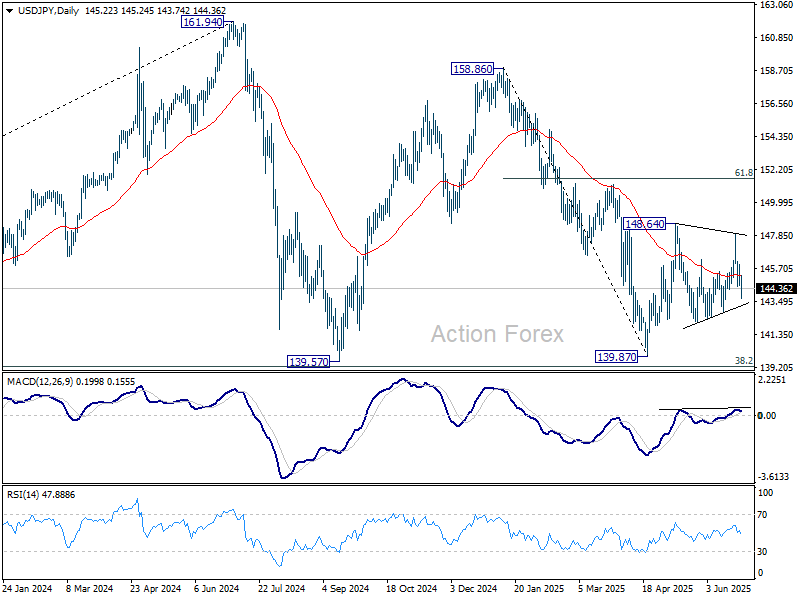

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 144.59; (P) 145.27; (R1) 145.93; More…

USD/JPY’s fall from 148.01 extends lower today, but stays above 142.10 support. Intraday bias remains neutral and further rise is still in favor. On the upside. firm break of 148.64 will resume the rise from 139.87 to 61.8% retracement of 158.86 to 139.87 at 151.22. However, break of 142.10 will bring deeper fall back to retest 139.87 low.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

{kind=link}