{kind=link}

Dollar found a modest bid early in the U.S. session after weekly jobless claims came in better than expected, offering a brief reminder that U.S. labor market conditions remain relatively resilient. The reaction, however, was restrained, and the greenback failed to generate meaningful follow-through. That muted response highlights the broader backdrop. Dollar remains the weakest performer of the week so far, and the rebound lacks conviction as markets slide deeper into holiday mode. With participation thinning sharply, price action is increasingly shaped by flows rather than fresh macro reassessment.

There is little in the way of new fundamental catalysts. In several markets, the long holiday weekend has effectively already begun, draining liquidity further. While low activity does not always translate into low volatility, directional conviction is clearly lacking. This quiet tone is likely to persist into next week as well. Many traders appear content to wait for the first full trading week of January before re-engaging, when heavyweight U.S. data such as non-farm payrolls return to the calendar and provide clearer signals.

Within FX, Aussie and Kiwi continue to vie for the top spot this week. Both currencies are being supported by early, tentative speculation that policy rates could eventually rise again in 2026, even if that discussion remains distant and conditional.

For the RBA, the debate centers on inflation risks. Price pressures have shown signs of re-acceleration, while the labor market remains somewhat tight, keeping the door ajar for future tightening even if no move is imminent.

For the RBNZ, the story is slightly different. Having eased much more aggressively through 2025, policymakers arguably have more scope to step back, creating room for markets to price a less dovish path down the line.

Technically, both AUD/USD and NZD/USD are pressing into key resistance zones. A decisive break would solidify the case for bullish trend reversal and likely extend gains into Q1.

Elsewhere, Yen ranks as the third-strongest currency, driven more by short covering and intervention caution than genuine trend change. Dollar trails at the bottom, followed by Euro and Loonie, with Sterling and Swiss Franc holding the middle ground.

Merry Christmas to our readers. We’ll be back on Monday, December 29.

US initial jobless claims fall to 214k vs exp 225k

US initial jobless claims fell -10k to 214k in the week ending December 20, below expectation of 225k. Four-week moving average of initial claims fell -750 to 217.5k. Continuing claims rose 38k to 1923k in the week ending December 13. Four-week moving average of continuing claims fell -5k to 1894k.

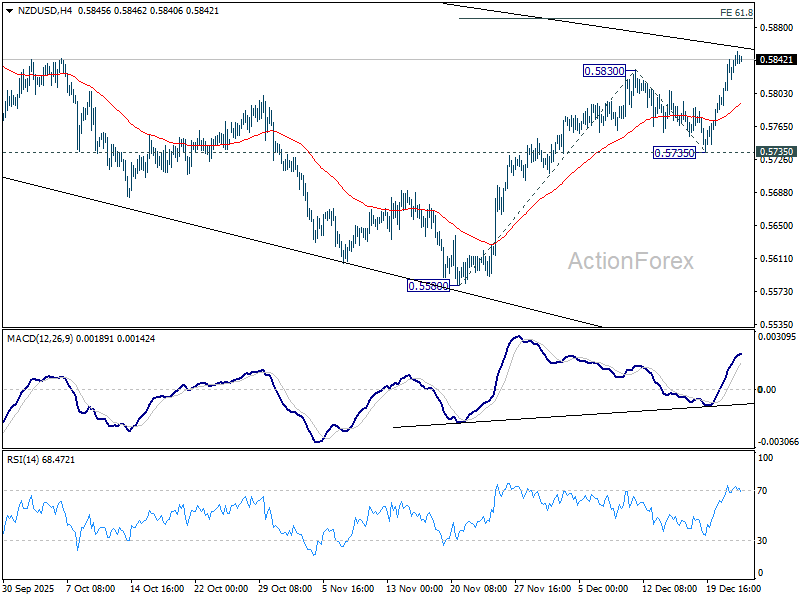

NZD/USD pops on early RBNZ hike speculations, 0.60 back on radar

NZD/USD is currently the standout performer of the week, rising around 1.5% and outperforming most major peers. The pair is extending its rebound from the November low, with momentum indicators pointing to an upside re-acceleration phase rather than a fading corrective bounce. Continued gains would reinforce the case that NZD/USD is already reversing the broader downtrend from the July high. Sustained push higher would open the path toward 0.60 handle.

Fundamental developments have turned more supportive in recent weeks. The most important shift came from the RBNZ, which signaled that the 25bp rate cut delivered in November was likely the final move of the easing cycle. That guidance marked a clear change in tone after months of downside growth concerns.

Subsequent data have largely validated the RBNZ’s stance. GDP rebounded a strong 1.1% qoq in Q3, more than offsetting the surprise -0.9% qoq contraction seen in Q2. Business sentiment has also surged, with ANZ Business Confidence jumping to its highest level in three decades in December.

These developments have fueled early speculation that the RBNZ could even consider rate hikes toward the end of 2026 if the recovery gains traction. However, that narrative remains premature and highly conditional on sustained improvement across the economy.

New RBNZ Governor Anna Breman has already pushed back firmly against talk of tightening, emphasizing that policy is not on a preset path. Indeed, pockets of weakness remain. The services sector continues to lag, with the BNZ Services index stuck at 46.9 in November.

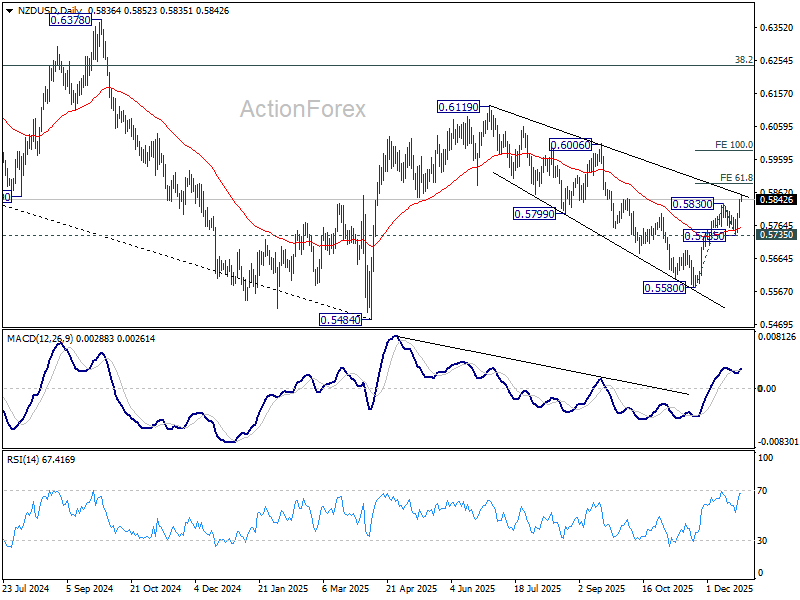

Technically, NZD/USD’s rise from 0.5580 resumed by breaking through 0.5830 support this week. The strong support from 55 D EMA is a clear near term bullish sign. Immediate focus is now on medium term falling trend line resistance (now at 0.5864). Sustained break there will reinforce the case that whole fall from 0.6119 has completed as a three-wave correction at 0.5580.

Further break of 61.8% projection of 0.5580 to 0.5830 from 0.5735 at 0.5890 would prompt upside acceleration to 0.6006 cluster resistance (100% projection at 0.5895). In any case, near term outlook will now stay bullish as long as 0.5735 support holds.

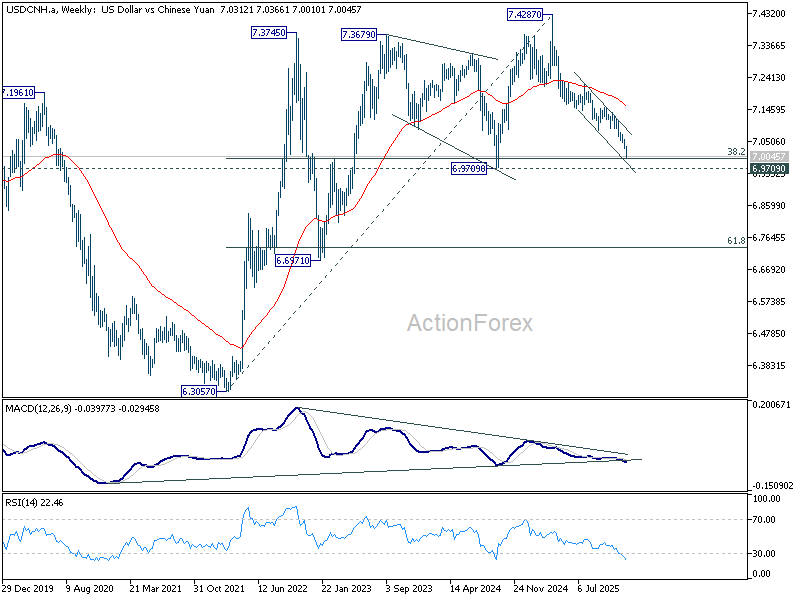

USD/CNH falls near 7 handle on Dollar weakness not Yuan strength, break seen as fragile

Offshore Chinese Yuan jumped sharply against Dollar in thin pre-holiday trading this week, driving USD/CNH to its lowest level in more than a year. But broader FX behavior points to Dollar weakness as the primary driver. Cross-rate performance supports that view. EUR/CNH has shown mostly sideways movement, suggesting Yuan strength is not uniform across major currencies. That casts doubt on the durability of any clean break below the 7 level in USD/CNH once liquidity improves.

Policy signals have nonetheless helped support sentiment. China’s decision to keep benchmark loan prime rates unchanged for a seventh straight month indicates that authorities see no immediate need for further monetary easing. The People’s Bank of China’s continued use of “cross-cyclical” policy tools adds to that message. By prioritizing smoothing over stimulus, and with bank margins already at record lows, policymakers appear content to wait until next year before considering more forceful support.

Seasonal factors are adding to Yuan demand. Year-end exporter conversions of foreign currency receipts into Yuan have increased spot demand. China’s strong bilateral trade surplus with the U.S., which exceeded USD 1 trillion in the first eleven months of the year, continues to provide an underlying flow-based cushion.

Still, structural limits remain clear. A stronger Yuan would weigh directly on exporters and growth by raising foreign-currency prices, increasing pressure on firms already dealing with soft demand. That vulnerability was highlight by the sharp deterioration in a private manufacturing activity index last month.

Geopolitical and trade considerations would further cap upside. With the U.S.–China tariff truce set to expire next year, renewed trade tension would likely force Chinese companies to discount more aggressively, making sustained Yuan appreciation counterproductive.

Technically, USD/CNH would be entering a key long term support zone between 6.9709 (2024 low) and 38.2% retracement of 6.3057 (2022 low) to 7.4287 (2025 high) at 6.9997. Strong support would be seen inside this zone to contain downside. On the upside, firm break of 7.0843 support turned resistance will confirm short term bottoming, and that the first leg of the pattern from 7.4287 has likely completed.

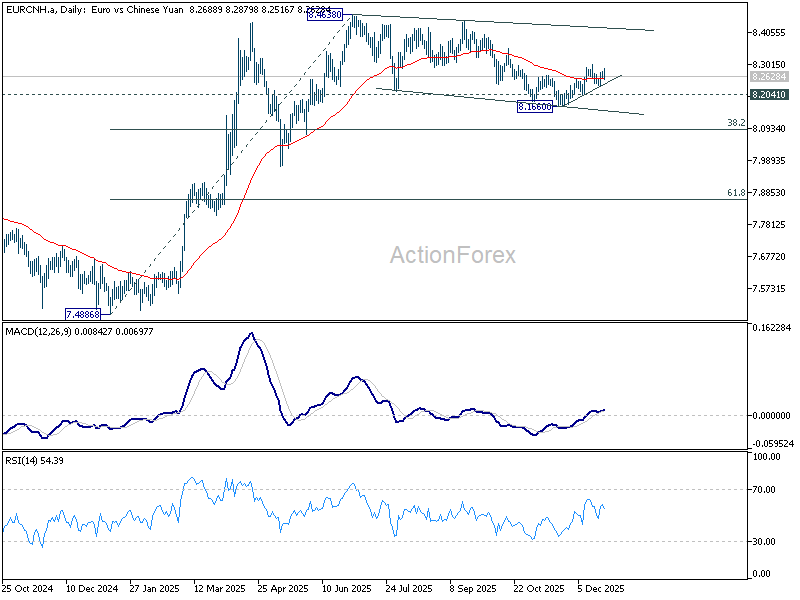

EUR/CNH gyrated higher after hitting 8.1660 in late November. Momentum waned as EUR/CNH struggled to clear 55 D EMA cleanly. Yet, further rise will remain in favor as long as 8.2041 support holds. Sustained trading above the 55 D EMA will pave the way to medium term falling trend line resistance.

However, break of 0.82041 support will argue that the recovery has completed and bring deeper fall through 0.81660 to resume the whole correction from 8.4648 (2025 high). Firm break of 8.1660 in EUR/CNH, however, together with decisive break of 6.9709 in USD/CNH, however, will be a strong sign of genuine underlying strength in Yuan.

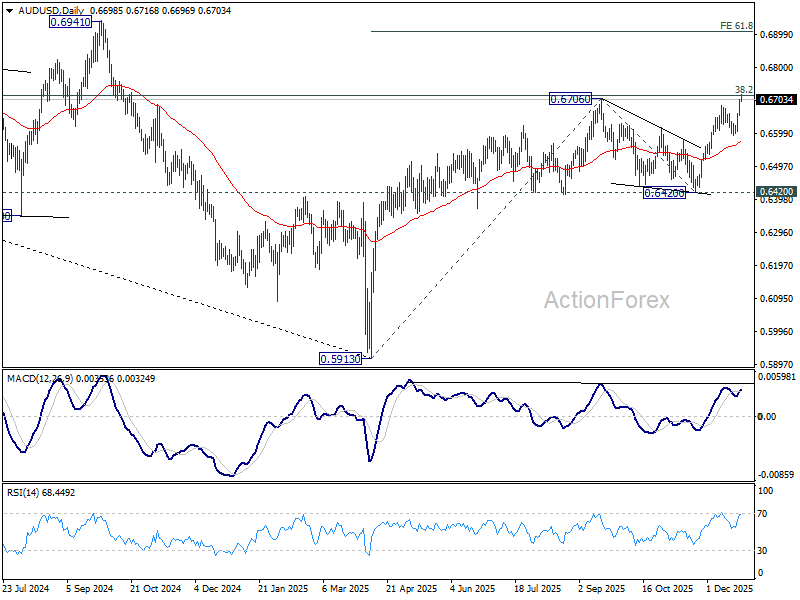

AUD/USD Daily Report

Daily Pivots: (S1) 0.6670; (P) 0.6686; (R1) 0.6719; More...

AUD/USD’s rally continues today and intraday bias stays on the upside. Sustained trading above 0.6707/13 will carry larger bullish implications. Next near term target will be 61.8% projection of 0.5913 to 0.6706 from 0.6420 at 0.6910. On the downside, below 0.6675 minor support will turn intraday bias neutral first. But For now, outlook will stay bullish as long as 0.6592 support holds, in case of retreat.

In the bigger picture, the break of multi-year falling trend line resistance suggests that rise from 0.5913 is possibly reversing whole down trend from 0.8006 (2021 high). Decisive break of 38.2% retracement of 0.8006 to 0.5913 at 0.6713 will solidify this case, and bring further rally to 61.8% retracement at 0.7206. On the downside, however, firm break of 0.6420 support will suggest rejection by 0.6713 and retain medium term bearishness.