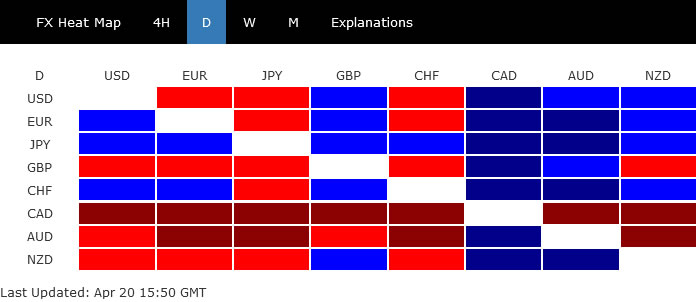

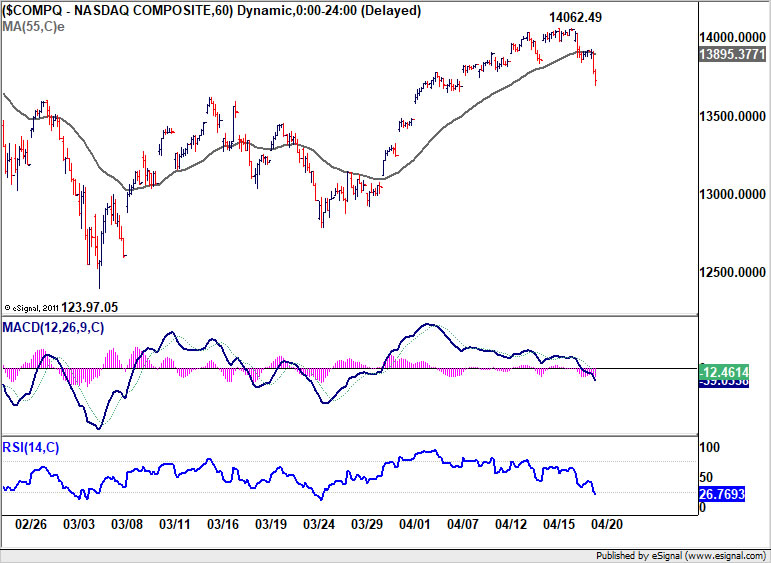

Ethereum’s rally has gathered strong pace and the cryptocurrency is now on track towards its record high. The move comes as Bitcoin remains stuck in consolidation, unable for now to decisively break its own record, as traders await the next catalyst.

Both assets are drawing support from the improved clarity around US cryptocurrency policy. However, Ethereum’s outperformance appears tied to larger institutional inflows, with big investors playing catch-up. In particular, Ethereum’s dominant role in stablecoin infrastructure leaves it uniquely positioned to benefit as digital dollar transactions expand under a more certain regulatory regime.

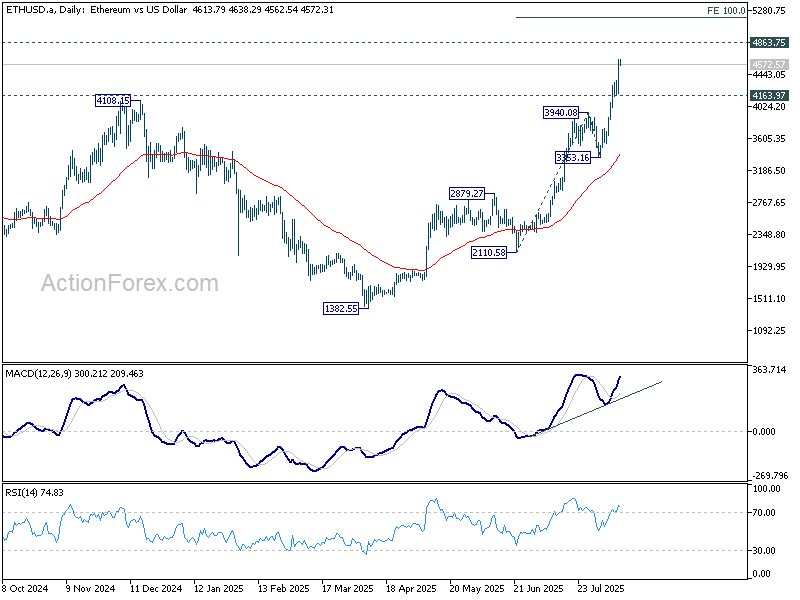

Technically, Ethereum’s near-term outlook stays bullish while above 4,163.97 support. Firm break of 4,863.75 record high would open the way toward 100% projection of 2,110.58 to 3,940.08 from 3,353.16 at 5,128.66.

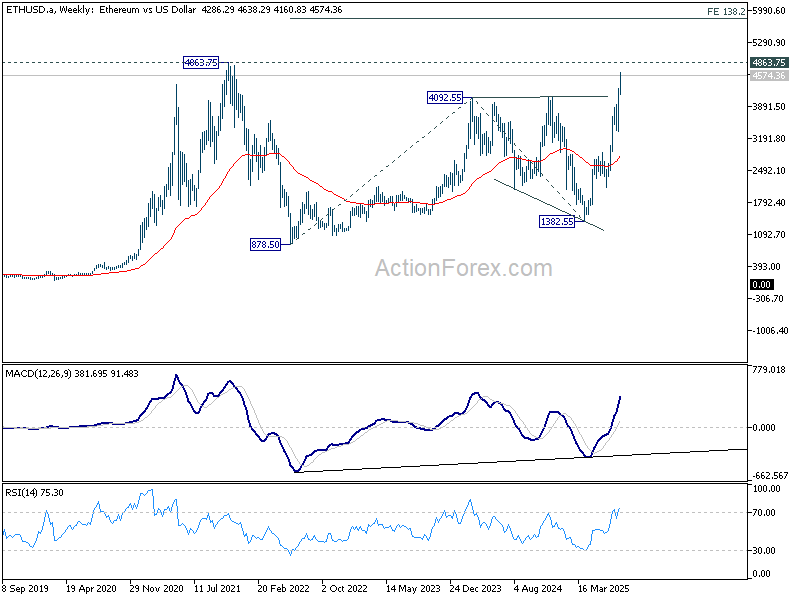

On the broader horizon, a clean break above 4,163.97 also sets up a medium term move move toward 138.2% projection of 878.5 to 4,092.55 from 1,382.55 at 5,824.36.

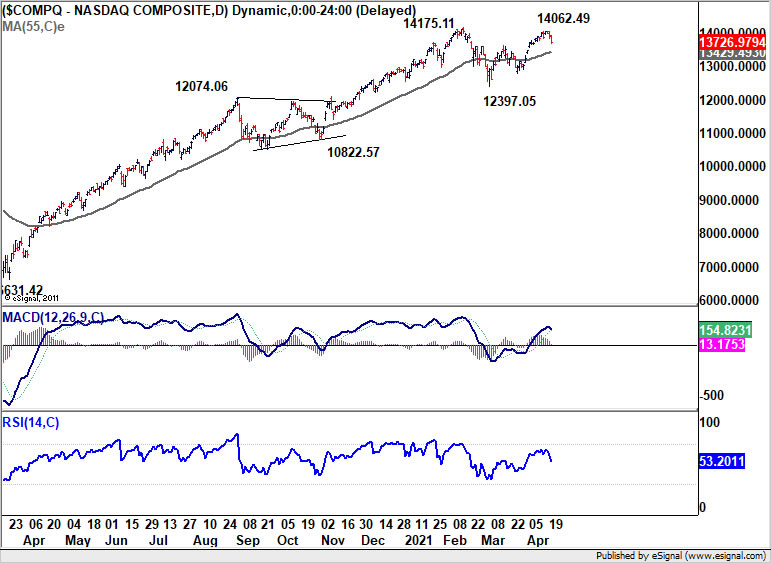

Bitcoin, meanwhile, is likely to see more consolidation below 123,231 in the near term. The broader outlook remains bullish while above 111,889 support, with the long-term uptrend expected to resume sooner or later.

However, Bitcoin may face strong resistance just below 100% projection of 49,008 to 109,571 from 74,373 at 134,936, which could act as a cap before any sustained move higher.

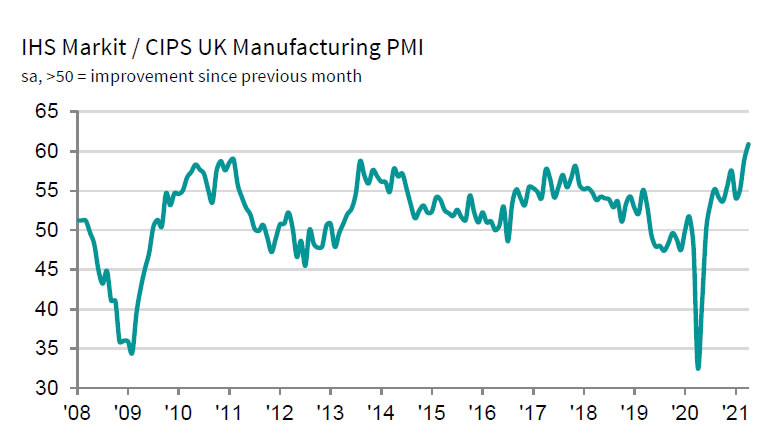

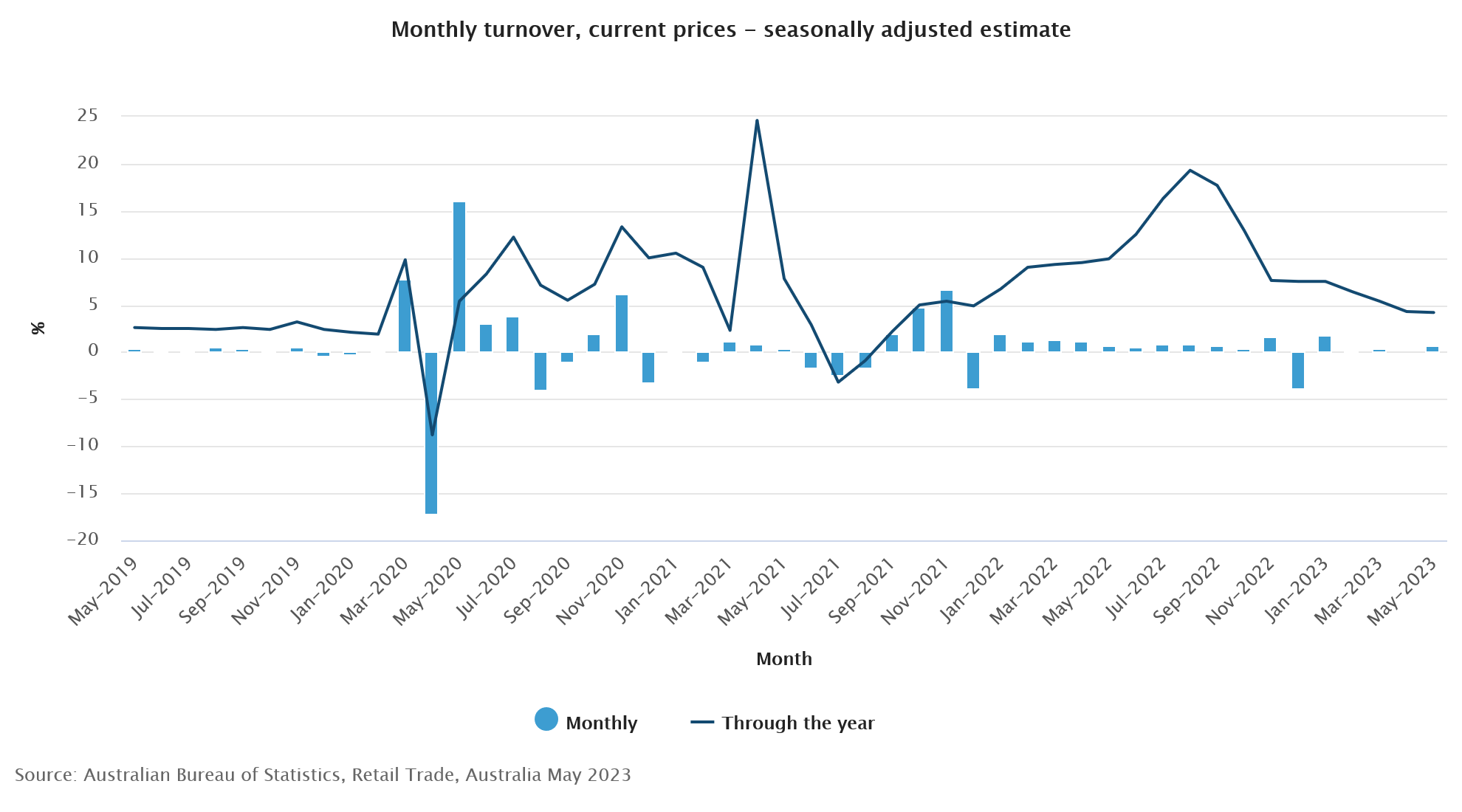

US ISM manufacturing dropped to 57.1, corresponds to 2.9% annualized GDP growth

US ISM manufacturing dropped from 58.6 to 57.1 in March, below expectation of 58.4. Prices jumped from 75.6 to 87.1, above expectation of 76.0. Employment also rose from 52.9 to 56.3, above expectation of 53.7.

ISM said: “The past relationship between the Manufacturing PMI and the overall economy indicates that the Manufacturing PMI for March (57.1 percent) corresponds to a 2.9-percent increase in real gross domestic product (GDP) on an annualized basis.”

Full release here.