Live Comments

China’s Manufacturing Expansion Slowed, but Three Trends Offer Encouragement

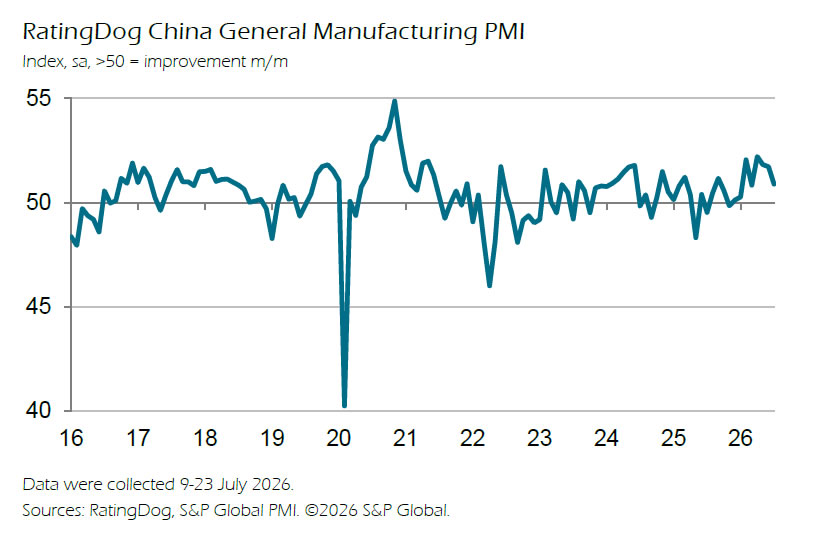

China's private manufacturing sector remained in expansion territory for an eighth consecutive month in July, although growth moderated from June. The RatingDog China General Manufacturing PMI eased to 50.9 from 51.7, the lowest reading in four months, but still signaled improving operating conditions. The current expansion matches the longest stretch of manufacturing growth in five years, with all five PMI components contributing positively for a second straight month.

The slowdown reflected softer growth across several key indicators rather than a reversal in activity. Total new orders continued to rise for a fourteenth consecutive month—the longest expansion since 2018—though the pace eased. Manufacturing output also expanded for an eighth straight month at a slower rate, while new export orders returned to growth after two months of contraction, providing a positive signal for external demand. Employment increased for a second consecutive month, although hiring remained modest.

Inflation pressures continued to ease, offering manufacturers some relief. Input cost inflation slowed to a six-month low, while firms largely kept selling prices unchanged despite higher costs. The survey also pointed to a mixed inventory picture, with companies continuing to build input stocks while reducing purchasing activity for the first time since November 2025, suggesting earlier inventory accumulation may be sufficient for near-term production needs. Looking ahead, business confidence improved slightly on expectations of stronger demand, new product launches and capacity expansion, although RatingDog expects manufacturing growth to remain positive but moderate in the coming months.

Economic Data

| Indicator | Actual | Expected | Previous |

|---|---|---|---|

| Manufacturing PMI | 50.9 | — | 51.7 |

| New Orders | Expanded (14th consecutive month) | — | Expanded |

| New Export Orders | Returned to expansion | — | Contracted |

| Manufacturing Output | Expanded (8th consecutive month) | — | Expanded |

| Employment | Modest increase | — | Increased |

| Input Cost Inflation | Six-month low | — | Higher |

| Output Prices | Broadly unchanged | — | Increased marginally |

Market Takeaways

- Manufacturing PMI eased from 51.7 to 50.9, marking a four-month low but remaining above the 50 threshold for an eighth consecutive month, matching the longest expansion in five years.

- Domestic demand remained resilient, with total new orders rising for a fourteenth straight month—the longest growth streak since 2018.

- New export orders returned to expansion after two months of contraction, suggesting external demand improved at the start of the third quarter.

- Cost pressures continued to ease, with input price inflation slowing to a six-month low while firms largely kept selling prices unchanged.

- Inventory dynamics were mixed. Companies continued to build input stocks for an eighth consecutive month but reduced purchasing activity for the first time since November 2025, indicating existing inventories were sufficient to support near-term production.

- Business confidence strengthened slightly as firms anticipated firmer demand, new product launches and expanded production capacity in the year ahead.

Japan PMI Manufacturing Finalized at 54.5, AI Demand Offsets Middle East Headwinds

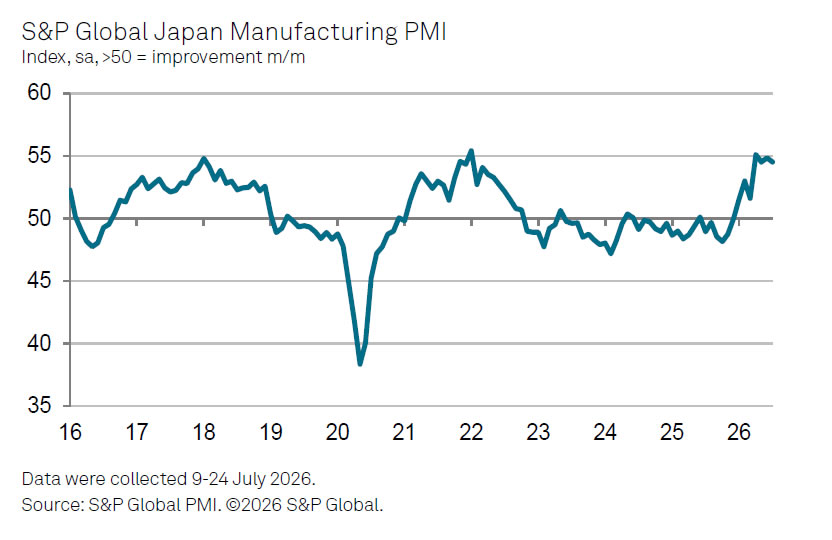

Japan's manufacturing sector remained firmly in expansion territory in July, with the final S&P Global Manufacturing PMI edging down slightly to 54.5 from 54.8 in June. While the headline index eased marginally, it still pointed to a seventh consecutive month of improving business conditions as the sector entered the second half of the year with robust momentum.

The survey highlighted broad-based strength beneath the headline figure. Manufacturing output posted its strongest increase in nearly 12-and-a-half years as firms responded to the steepest rise in new orders in four-and-a-half years. According to S&P Global, many companies linked the improvement to stronger global demand for semiconductors and expanding AI-related manufacturing activity. Firms also stepped up hiring, but the surge in production and order inflows led to mounting capacity pressures, prompting a sharp increase in purchasing activity and inventory accumulation.

At the same time, geopolitical risks continued to shape business conditions. Companies reported building inventories in response to the conflict in the Middle East, driving the fastest increase in input stocks in more than two years. Although input cost inflation moderated from June, it remained elevated and continued to feed through to higher selling prices. The survey therefore points to a manufacturing sector benefiting from powerful structural demand drivers, while still contending with supply-chain and inflation risks stemming from geopolitical uncertainty.

Economic Data

| Indicator | Actual | Previous |

|---|---|---|

| Manufacturing PMI | 54.5 | 54.8 |

| Production | Strongest growth in nearly 12½ years | Expanded |

| New Orders | Strongest rise in 4½ years | Expanded |

| Employment | Solid increase | Increased |

| Input Costs | Rose at a marked but softer pace | Sharper increase |

| Selling Prices | Rose substantially | Increased |

Market Takeaways

- Manufacturing PMI eased only marginally from 54.8 to 54.5, remaining firmly in expansion territory for a seventh consecutive month.

- Output recorded its strongest increase since early 2014, supported by the steepest rise in new orders in four-and-a-half years, pointing to robust underlying demand.

- Survey respondents highlighted stronger global demand for semiconductors and AI-related manufacturing as key drivers of the rebound.

- Firms continued to hire, but rapid growth in production and orders intensified capacity pressures, prompting the fastest increase in purchasing activity since April 2022 and the quickest inventory build-up in more than two years.

- While input cost inflation moderated from June, cost pressures remained elevated due in part to the Middle East conflict, allowing manufacturers to continue raising selling prices.

Australia Manufacturing PMI Finalizes at Six-Month High, Yet Inflation and Supply Risks Limit Confidence

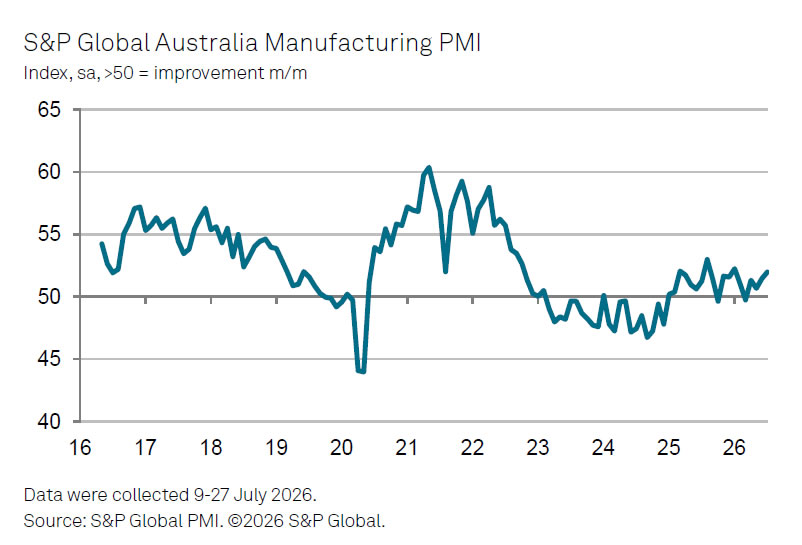

Australia's manufacturing sector showed further signs of recovery in July, with S&P Global Australia Manufacturing PMI finalized at 52.0, up from 51.5 in June and the strongest reading since January. The sector has now remained in expansion territory for four consecutive months, supported by renewed growth in both production and new orders as business conditions improved at the start of the second half of the year.

The details of the survey suggest the recovery is beginning to broaden, albeit only gradually. Factory output expanded for the first time in six months, while new orders returned to growth for the first time since February. However, both increases were only marginal, indicating that underlying demand remains subdued. Manufacturers also continued to face elevated input costs and supply-side pressures, preventing a stronger rebound despite the improvement in headline activity.

S&P Global's Economics Director Andrew Harker said the latest data offered reassurance that the sector was recovering from the disruption caused by the Middle East conflict, but stressed that the improvement remained tentative. He warned that renewed deterioration in the region could quickly rekindle inflationary and supply pressures, leaving the nascent recovery vulnerable. The survey therefore points to improving business conditions, but also underscores that manufacturers remain highly exposed to geopolitical developments that could influence both inflation and the broader economic outlook.

Economic Data

| Indicator | Actual | Previous |

|---|---|---|

| Manufacturing PMI | 52.0 | 51.5 |

| Output | Returned to growth | Contracted |

| New Orders | Returned to growth | Contracted |

| Business Conditions | Improved at fastest pace since January | Improved |

Market Takeaways

- Manufacturing PMI rose from 51.5 to 52.0, marking the strongest expansion since January and extending the sector's expansion streak to four months.

- Output increased for the first time in six months, while new orders returned to growth for the first time since February, suggesting the manufacturing downturn linked to the Middle East conflict is easing.

- Despite the stronger headline reading, both output and demand expanded only marginally, indicating the recovery remains fragile rather than broad-based.

- Persistent price and supply-chain pressures continue to weigh on manufacturers, leaving the sector vulnerable to renewed geopolitical disruptions.

- The survey reinforces the view that Australia's manufacturing sector is stabilizing, but the durability of the recovery will depend heavily on whether inflation and supply pressures ease further.