Live Comments

US ISM Manufacturing Hits Three-Year High, Employment Returns to Growth

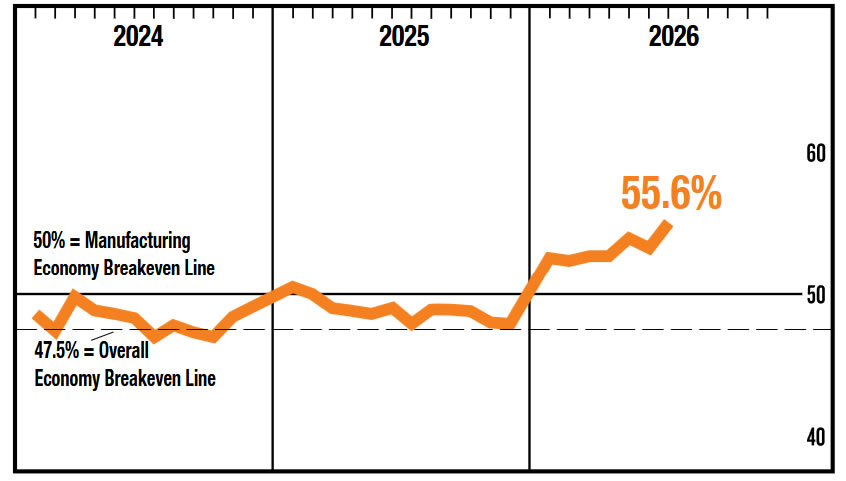

US manufacturing gathered further momentum in July, with the ISM Manufacturing PMI rising to 55.6 from 53.3, its highest reading since May 2022 and well above market expectations. According to ISM, the latest reading is historically consistent with annualized real GDP growth of around 2.8%, reinforcing signs that the US economy entered the third quarter on a solid footing despite elevated interest rates and geopolitical uncertainty.

The improvement was broad-based, led by a sharp acceleration in production. The Production Index jumped 6.3 points to 58.5, its highest level in almost five years, extending expansion to a ninth consecutive month. The labor market also showed renewed strength, with the Employment Index climbing to 52.8 from 49.7, returning to expansion territory for the first time in 33 months and reaching its highest level since August 2022. Together with stronger new orders and export demand, the survey points to improving manufacturing activity rather than a temporary rebound.

Inflation pressures, however, remained an important feature of the report. Although the Prices Index eased to 71.1 from 73.0, it remained firmly elevated. ISM said price increases continued to be driven by higher steel and aluminum costs, tariffs on imported goods and rising petroleum-based product prices linked to the Middle East conflict. Just over half of respondents reported paying higher prices in July, down from June but still indicative of widespread cost pressures across the manufacturing sector.

The report strengthens the case that the US economy remains resilient while inflation risks have yet to disappear. For the Federal Reserve, the combination of stronger production, expanding employment and still-elevated input prices leaves the door open to another rate hike should inflation remain stubborn.

Economic Data

| Indicator | Actual | Expected | Previous |

|---|---|---|---|

| ISM Manufacturing PMI | 55.6 | 54.0 | 53.3 |

| S&P Global Manufacturing PMI | 53.9 | 53.8 | 53.8 |

| Production | 58.5 | — | 52.2 |

| New Orders | 56.7 | — | 56.0 |

| Employment | 52.8 | — | 49.7 |

| Prices Paid | 71.1 | 70.0 | 73.0 |

| New Export Orders | 53.0 | — | 48.5 |

| Backlog of Orders | 55.0 | — | 50.5 |

Key Takeaways

- ISM Manufacturing PMI jumped from 53.3 to 55.6, the highest reading since May 2022, pointing to a further acceleration in US factory activity.

- ISM estimates the July PMI is historically consistent with 2.8% annualized real GDP growth, suggesting manufacturing continues to support overall economic expansion.

- Production surged from 52.2 to 58.5, its highest level in nearly five years, while the Employment Index returned to expansion at 52.8, its first expansionary reading in 33 months.

- Demand remained healthy, with New Orders rising to 56.7, New Export Orders returning to expansion at 53.0, and Backlog of Orders climbing to 55.0, indicating factories continue to receive more work than they can immediately process.

- Inflation pressures eased only modestly. Prices Paid fell from 73.0 to 71.1 but remained elevated, with respondents continuing to cite tariffs, higher steel and aluminum prices, and Middle East-related energy costs as key drivers.

- Overall, the report portrays an economy with strong manufacturing momentum and persistent inflationary pressures, giving the Fed greater flexibility to tighten policy if upcoming inflation data fail to improve.

Fed’s Williams Looks Beyond Oil Shock, Focuses on Core Inflation Trend

New York Fed President John Williams said he remains confident inflation will gradually resume its decline, arguing that the recent surge in energy prices is unlikely to derail the broader disinflation process. Speaking to Reuters on Friday, Williams said that if energy prices and tariffs have peaked and the economy remains resilient, "some of the big drivers that pushed up inflation... will not be at play as much," while "some of the disinflationary forces that we've been seeing should reassert themselves." He added that his personal forecast is for inflation to ease during the second half of this year and decline further next year.

Rather than focusing on temporary supply shocks, Williams emphasized that the Fed is watching whether underlying inflation is returning sustainably toward target. "I am... focused quite a bit on what are we seeing in the core inflation data over the next several months," he said, adding that policymakers need evidence inflation is on "a disinflationary path consistent with us achieving our 2% inflation goal on a sustained basis by 2028." Williams reiterated that the current policy stance is "well positioned" following last week's decision to leave the federal funds target range unchanged at 3.50%-3.75%.

Still, Williams made clear that the Fed remains prepared to tighten policy again if inflation fails to cooperate. "If the economy is not on a trajectory that will bring inflation back down to 2%... it would absolutely be appropriate to act," he said. While acknowledging uncertainty surrounding the Middle East conflict, Williams said he does not expect it to generate persistent inflationary pressure under his base case, assuming shipping disruptions eventually ease. He also stressed that the Fed will make its own policy assessment rather than follow financial market pricing, saying it would "absolutely not" be bound by investors' expectations.

Key Takeaways

- Williams remains confident that inflation will continue to ease, expecting disinflationary forces to reassert themselves if energy prices and tariffs stabilize.

- The Fed's primary focus has shifted to core inflation, with Williams emphasizing that the next several months of underlying inflation data will determine whether inflation is on a sustainable path back to the 2% target.

- He reaffirmed that current monetary policy is "well positioned" after last week's decision to leave rates unchanged at 3.50%-3.75%.

- Despite his constructive inflation outlook, Williams made clear that further rate hikes remain on the table if inflation fails to move convincingly toward target.

- Williams views the inflation impact of the Middle East conflict as likely temporary under his base case, assuming shipping disruptions eventually ease.

- He also stressed that the Fed will not be guided by market pricing, reiterating that policy decisions will be based on the Fed's own assessment of incoming economic data.

UK PMI Manufacturing at Four Month Low, but Faster Output Growth Points to Resilient Recovery

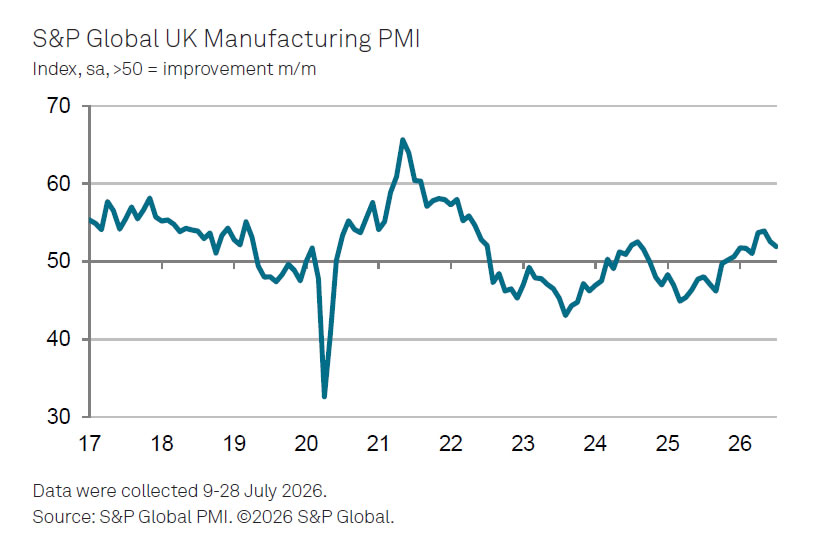

The UK's manufacturing sector lost some momentum in July, with the final S&P Global Manufacturing PMI easing to 51.9 from 52.5 in June, its lowest level in four months. Even so, the index remained above the 50 threshold for a ninth consecutive month, indicating that the sector continues to expand despite a moderation in the pace of improvement.

The details of the survey painted a more encouraging picture than the headline suggested. Manufacturing output rose for a fourth straight month, with production growth accelerating to its fastest pace in nearly two years as stronger market conditions boosted new orders and export demand. Four of the five PMI components remained consistent with improving operating conditions, while the decline in the headline index mainly reflected a sharp reduction in stocks of purchases, slower hiring and a smaller deterioration in supplier delivery times. Growth, however, remained uneven, with medium and large manufacturers outperforming smaller firms, where production declined modestly.

S&P Global also pointed to improving supply and cost conditions. Input cost inflation slowed to a five-month low as supply-chain delays eased to their weakest level since the outbreak of the Middle East conflict, offering manufacturers some relief after months of disruption. Although hiring growth nearly stalled, the first increase in backlogs of work in more than four years suggests labor demand could strengthen if new orders continue to improve. Still, business confidence remained subdued, with geopolitical developments, global trade tensions and the new UK government's industrial and tax policies likely to shape the outlook in the months ahead.

Economic Data

| Indicator | Actual | Previous |

|---|---|---|

| Manufacturing PMI | 51.9 | 52.5 |

| Manufacturing Output | Near 2-year high | Expanded |

| New Orders | Expanded | Expanded |

| New Export Orders | Accelerated | Expanded |

| Employment | Increased | Increased |

| Input Cost Inflation | 5-month low | Higher |

Market Takeaways

- Manufacturing PMI eased from 52.5 to 51.9, a four-month low, but remained above the 50 threshold for a ninth consecutive month, signalling continued expansion.

- Factory output accelerated to its fastest pace in almost two years, supported by stronger domestic and export demand.

- The softer headline PMI largely reflected lower stocks of purchases, slower hiring and a smaller deterioration in supplier delivery times rather than weaker demand.

- Input cost inflation slowed to a five-month low, while supply-chain delays eased to their lowest since the outbreak of the Middle East conflict, providing relief for manufacturers.

- Employment growth nearly stalled despite stronger production, although the first increase in backlogs of work in more than four years suggests hiring could improve if demand remains firm.

- The recovery remained uneven, with medium and large manufacturers outperforming smaller firms, where production continued to decline modestly.