Live Comments

Fed’s Musalem: It’s Okay to Surprise Markets With a Rate Move

St. Louis Fed President Alberto Musalem said he favored raising interest rates by 25bps at last week's FOMC meeting, arguing that acting gradually now would be preferable to risking more aggressive tightening later. Musalem is not a voting member of FOMC this year, so his preference was not among the three formal dissents against the decision to hold rates steady. Speaking in Brazil on Thursday, Musalem said inflation is likely to remain too high relative to Fed's 2% target over coming year if policy stays unchanged. "Earlier gradual incremental interest rate increases are preferable, less disruptive, less costly than potentially later, more abrupt interest rate changes," he said.

Musalem also pushed back against idea that Fed should hesitate simply because financial markets are not positioned for higher rates. While acknowledging that he closely monitors market signals, he said policymakers should follow their economic assessment regardless of prevailing expectations. "If you think that now is the time to change policy in whatever direction, you ought to change that policy, irrespective of what's priced into markets," Musalem said, adding that "there are times or moments when it's okay to surprise the market." His comments are particularly relevant as investors have moved toward pricing a September hold following falling oil prices and optimism over reopening Strait of Hormuz.

Musalem's broader argument was that Fed has little reason to tolerate elevated inflation in hope that stronger productivity eventually resolves price pressures. "It is crucial that monetary policy put a meaningful restraint on underlying inflation, rather than tolerating somewhat higher inflation today to pursue productivity growth tomorrow," he said, warning there is "fertile ground for inflation expectations to potentially become unanchored." With financial conditions supportive, asset prices elevated and labor market characterized by "solid payroll growth," Musalem sees room to tighten policy before inflation becomes harder to contain. His stance therefore adds to hawkish pressure inside Fed just as markets increasingly bet that September will bring another hold.

Key Takeaways

- St. Louis Fed President Alberto Musalem favored a 25bps rate hike at last week's FOMC meeting, arguing current policy may not be restrictive enough to bring inflation sustainably back to 2%.

- Musalem favors earlier, gradual tightening, saying incremental increases now would be "less disruptive" and "less costly" than potentially larger rate moves later.

- He stressed that market pricing should not dictate Fed decisions, saying policymakers should act when warranted "irrespective of what's priced into markets."

- Musalem added that "there are times or moments when it's okay to surprise the market," a notable warning as investors increasingly lean toward a September hold.

- He rejected tolerating above-target inflation in hope that future productivity gains will solve the problem, warning such an approach could put Fed credibility and anchored inflation expectations at risk.

- With economy resilient, financial conditions supportive and labor market stable, Musalem sees room for Fed to focus on inflation rather than wait for clearer economic weakness before tightening.

US Initial Jobless Claims Edge Up to 119k, but Layoffs Remain Limited

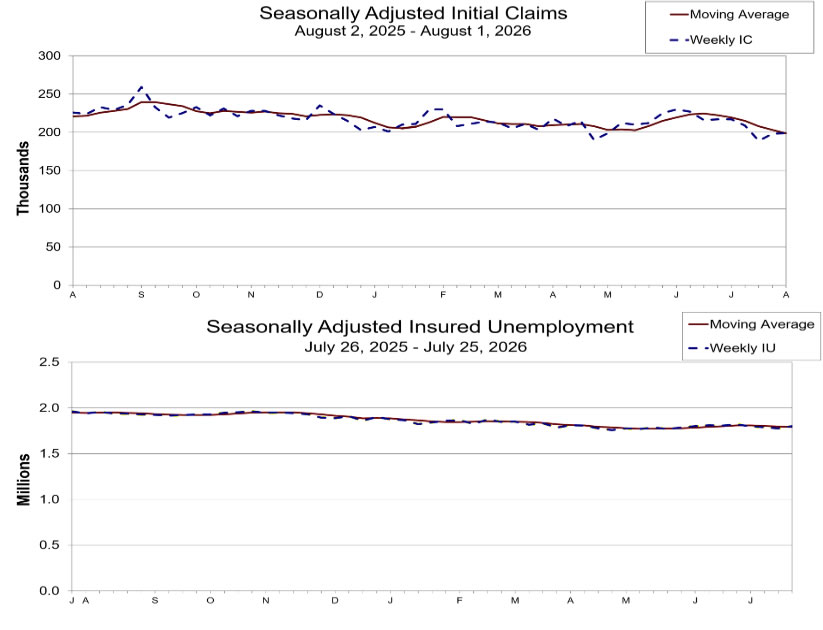

US initial jobless claims remained near historically low levels in the latest week, reinforcing the view that layoffs continue to be limited despite signs of slower hiring elsewhere in the labor market. Initial claims rose by just 1,000 to 199,000 in the week ended August 1, slightly below market expectations of 203,000. The previous week's figure was revised up modestly to 198,000, while the four-week moving average declined to 198,750, suggesting underlying labor market conditions remain broadly stable.

Continuing claims painted a slightly softer picture, rising 24,000 to 1.801 million in the week ended July 25, although the insured unemployment rate held steady at 1.2%. The increase suggests unemployed workers may be taking slightly longer to find new jobs, but the overall level remains consistent with a labor market that is cooling gradually rather than weakening abruptly.

The latest figures fit with other recent labor market indicators showing a "low-hire, low-fire" environment. While ADP employment and the ISM Services Employment Index pointed to softer hiring momentum, weekly claims continue to show employers are reluctant to shed workers.

Data Summary

| Indicator | Latest | Previous |

|---|---|---|

| Initial Jobless Claims | 199K | 198K |

| Market Expectation | 203K | — |

| 4-Week Average | 198.8K | 203.3K |

| Continuing Claims | 1.801M | 1.777M |

| 4-Week Avg. Continuing Claims | 1.791M | 1.796M |

| Insured Unemployment Rate | 1.2% | 1.2% |

Key Takeaways

- Initial jobless claims edged up to 199K, remaining below the 200K mark and beating expectations of 203K, indicating layoffs remain historically low.

- The four-week moving average fell to 198.8K, suggesting there has been no meaningful deterioration in underlying labor market conditions.

- Continuing claims rose by 24K to 1.801 million, hinting that unemployed workers may be taking slightly longer to secure new jobs.

- The insured unemployment rate held steady at 1.2%, reinforcing the picture of a labor market that remains fundamentally resilient.

- The report supports the recent "low-hire, low-fire" narrative emerging from JOLTS, ADP and Fed officials—hiring has slowed, but employers are generally reluctant to lay off workers.

Eurozone Retail Sales Fall -0.3% MoM in June as Food and Non-Food Demand Weakens

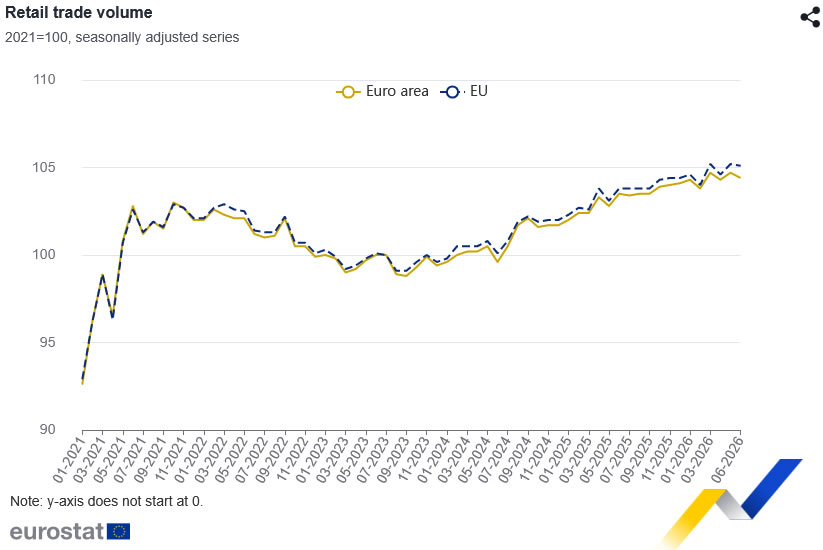

Eurozone retail sales weakened in June, adding to signs that household demand remains fragile despite improving business surveys. Retail trade volume fell -0.3% mom after rising 0.4% in May. Sales across EU declined -0.1% following 0.6% growth. On annual basis, retail sales still increased 0.7% yoy in Eurozone and 1.2% across EU, indicating consumer spending has not collapsed but continues to lack consistent momentum.

Weakness was broad across core spending categories. In Eurozone, food, drinks and tobacco sales fell -0.5% mom, while non-food sales declined -0.4%. Automotive fuel provided only offset, rising 1.5%. Pattern was similar across EU, where food sales dropped -0.4%, non-food purchases fell -0.3%, and fuel sales increased 1.7%. That composition suggests consumers remained cautious on discretionary and everyday spending even as driving-related demand improved.

National data also pointed to uneven conditions across region. Finland, Romania and Germany recorded largest monthly declines, while Luxembourg, Portugal, Croatia and Sweden posted strongest gains. For ECB, softer retail activity supports patience on further tightening, particularly while policymakers assess whether easing pipeline inflation can continue without renewed pressure from energy markets.

Data Summary

Eurozone Retail Sales

| Indicator | June 2026 | May 2026 | Trend |

|---|---|---|---|

| Total Retail Sales (m/m) | -0.3% | +0.4% | ▼ Weaker |

| Retail Sales (y/y) | +0.7% | — | ▲ Annual growth |

| Food, Drinks & Tobacco | -0.5% | +0.4% | ▼ Lower |

| Non-food (ex. Automotive Fuel) | -0.4% | +0.5% | ▼ Lower |

| Automotive Fuel | +1.5% | -1.8% | ▲ Rebounded |

EU Retail Sales

| Indicator | June 2026 | May 2026 | Trend |

|---|---|---|---|

| Total Retail Sales (m/m) | -0.1% | +0.6% | ▼ Weaker |

| Retail Sales (y/y) | +1.2% | — | ▲ Annual growth |

| Food, Drinks & Tobacco | -0.4% | +0.4% | ▼ Lower |

| Non-food (ex. Automotive Fuel) | -0.3% | +0.9% | ▼ Lower |

| Automotive Fuel | +1.7% | -1.4% | ▲ Rebounded |

Largest Monthly Changes by Member State

| Largest Declines | m/m | Largest Gains | m/m |

|---|---|---|---|

| Finland | -1.5% | Luxembourg | +2.5% |

| Romania | -1.2% | Portugal | +1.7% |

| Germany | -1.1% | Croatia | +1.5% |

| Sweden | +1.5% |

Key Takeaways

- Eurozone retail sales fell 0.3% m/m in June after a 0.4% increase in May, while EU retail sales slipped 0.1% following 0.6% growth.

- Despite the monthly setback, retail sales remained higher than a year earlier, rising 0.7% y/y in the Eurozone and 1.2% y/y across the EU.

- The decline was broad-based, with both food, drinks and tobacco (-0.5%) and non-food products (-0.4%) weakening in the Eurozone.

- Automotive fuel sales rose 1.5% in the Eurozone and 1.7% in the EU, partially offsetting softer spending elsewhere.

- Germany, Finland and Romania recorded the largest monthly declines, highlighting continued weakness in several major consumer markets.

- The report suggests household demand remains subdued, reinforcing the divergence between improving business surveys and still-cautious consumers.