Chinese Yuan saw a sharp uptick after PBoC announced a substantial 200 bps cut in foreign exchange reserve requirement ratio to 4% from 6%, effective September 15. According to PBoC, the move aims to “improve financial institutions’ ability to use foreign exchange funds.”

This RRR cut is set to release approximately USD 16.4B in foreign exchange, based on China’s FX deposits standing at USD 821.8B as of end-July. Market analysts also note that the FX RRR reduction could have the added effect of lowering dollar funding costs in the interbank market, thereby alleviating some of downward pressure on Yuan.

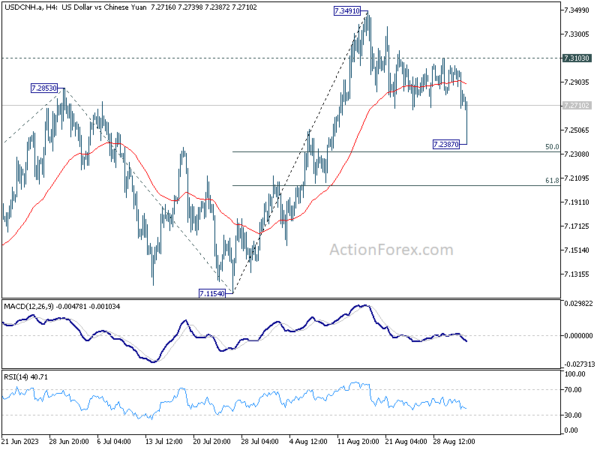

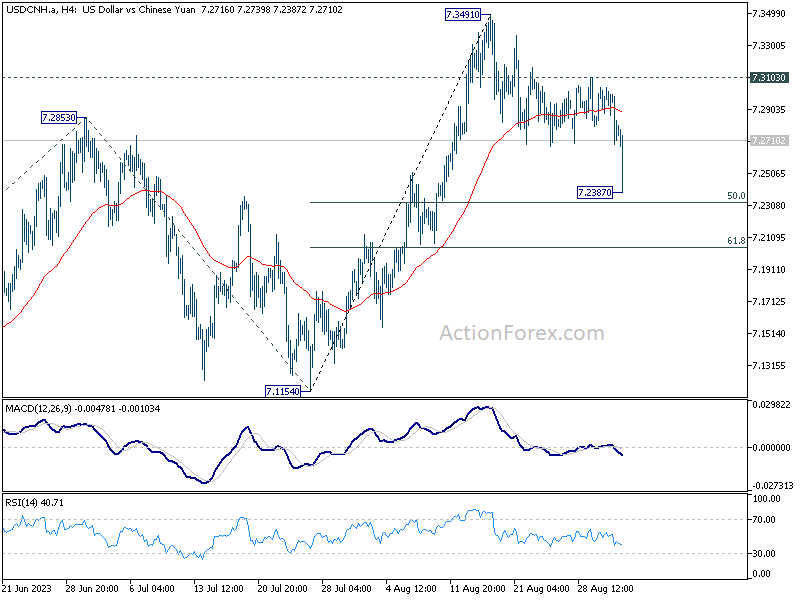

On the technical front, USD/CNH saw a drop to as low as 7.2387 following the announcement, but it has since recovered most ground. Despite the knee-jerk reaction, the broader uptrend from 6.6971 appears to remain intact. Should it break 7.3103 minor resistance, this would signal completion of the correction from 7.3491 and likely pave the way through 7.3491 for testing 7.3745 high.

However, considering bearish divergence condition in D MACD, strong resistance is likely at 61.8% projection of 6.8100 to 7.2853 from 7.1154 at 7.4091 to limit upside, to complete the five wave sequence from 6.6971.

While technical landscape seems to suggest further upside for USD/CNH, it is crucial to note that these views could be rendered academic at a moment’s notice. The Chinese authorities may implement various intervention measures any time, adding an extra layer of unpredictability to the equation.

BoJ stands pat, continue to closely monitor impacts of pandemic

BoJ kept monetary policy unchanged today as widely expected. Under the yield curve control framework, short-term policy interest rate is held at -0.1%. 10-year JGB yield target is kept at around 0%. The central bank will continue to purchase ETFs and J-REITS with upper limits of about JPY 12T and JPY 180B respectively. CP and Corporate bonds purchases will continue with upper limit of JPY 20Y until the end of September 2021.

BOJ also pledged to continue with QQE with Yield Curve Control “as long as it is necessary” and “continue expanding the monetary base” until core CPI exceeds 2% target in a “stable manner”. It will also “closely monitor” of the impact of COVID-19 and “will not hesitate to take additional easing measures if necessary”.

Full statement here.