In China, industrial production grew 6.9% yoy in October, matched expectations. The figure was unchanged from September’s growth. Fixed asset investment grew 1.8% ytd yoy, above expectation of 1.6%. But retail sales rose only 4.3% yoy, below expectation of 5.0% yoy. That’s nevertheless still the strongest rise this year, as led by 12.5% growth in auto sales.

Overall, the set of data suggested that China’s economy maintained broad-based acceleration in October, which could likely continue through the rest of Q4. Policy stimulus continued to had a positive impact on both investment and industrial output. The consumer sectors were also returning to normal.

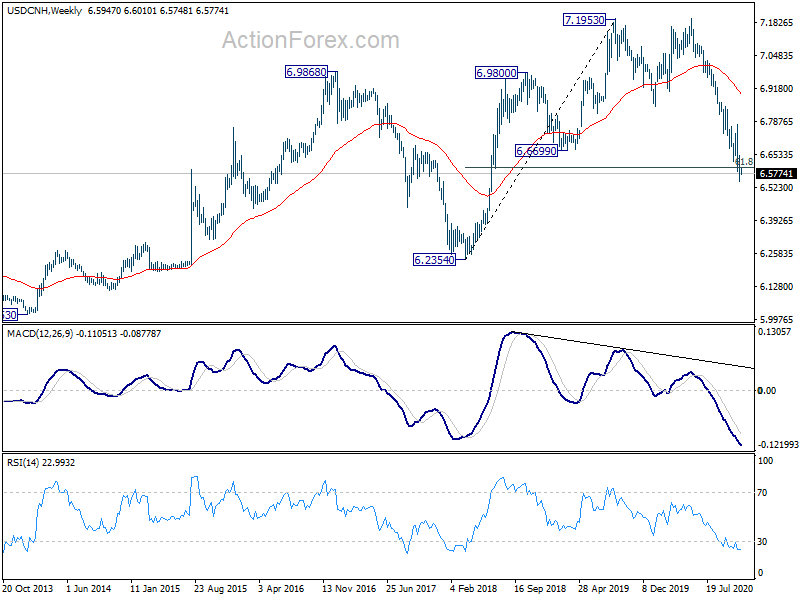

The Chinese Yuan is also maintaining its strong medium term up trend. USD/CNH has taken out 6.6699 key support level last month. 61.8% retracement of 6.2354 to 7.1953 at 6.6020 was also lost. Further decline could be seen back to 6.2354 low next.

RBA Lowe outlined four changes on monetary policy front this year

RBA Governor Philip Lowe outlined four changes on the monetary policy front during 2020. Firstly, the nature of RBA” forward guidance has moved to place much more weight on actual outcomes, rather than forecast outcomes”. An example is seen in the statement, where RBA said “the Board will not increase the cash rate until actual inflation is sustainably within the 2 to 3 per cent target range.” For this to occur wages growth will have to be “materially higher than it is currently”, which requires “significant gains in employment and a return to a tight labour market.” A second and related change has been a shift in the relative weight given to jobs and inflation.

The third change is a “strengthening in the gravitational pull of low global interest rates. Ignoring this would have “obvious implications for our exchange rate and our economy.” “Over the medium term, I do expect to see a time when Australia’s strong economic conditions once again justify higher interest rates. But today, during a global pandemic when a lot of people have lost their jobs and many businesses are struggling, is not the time for that.”

The fourth change was “the return to a world in which quantities, not just prices, matter.”

Full speech here.