By loading the video, you agree to YouTube’s privacy policy.

Learn more

By loading the video, you agree to YouTube’s privacy policy.

Learn more

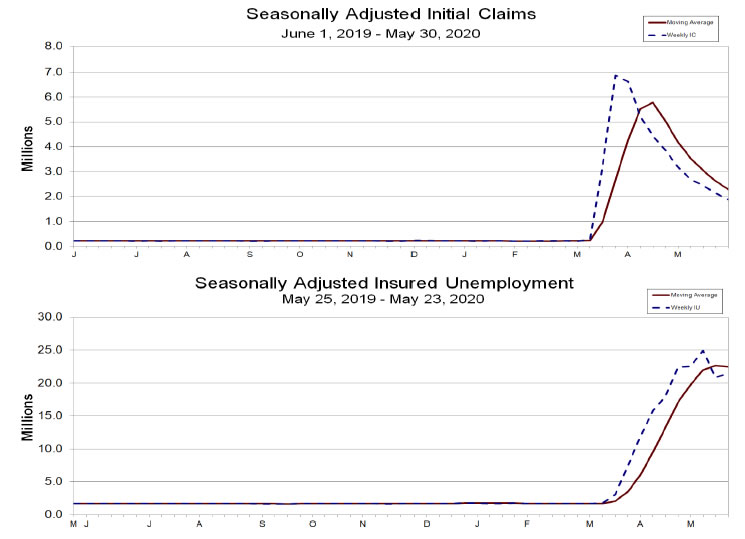

US initial jobless claims dropped another -249k to 1877k in the week ending May 30. Four-week moving average of initial claims dropped -324.8k to 2284k. Continuing claims rose 649k to 21487m in the week ending May 23. Four-week moving average dropped -222.5k to 22446k.

Also released, US trade deficit widened to USD -49.4B in April versus expectation of USD -41.5B. Non-farm productivity dropped -0.9% in Q1 while unit labor costs rose 5.1%. Canada trade deficit widened to CAD -3.3B in April versus expectation of CAD -2.7B.

Andrew Hauser, BoE Executive Director for Markets said even if negative interest rate is the right thing to do, “it’s not going to happen in the near term”. He added, “it’s on the retail side and banking side that we need to think more about it, and no decisions have been made about that either way.”

He also warned, “financial markets could come under strain again if there is another leg to the global infection cycle, or if economic data come out persistently worse than expected.”

ECB announced to increase the pandemic emergency purchase programme (PEPP) by EUR 600B to a total of EUR 1350B today. Purchases will continue to conducted in a “flexible manner over time, across asset classes and among jurisdictions”.

Also, the horizon of PEPP net purchases will be extended to “at least the end of June 2021”. Additionally, “the Governing Council will conduct net asset purchases under the PEPP until it judges that the coronavirus crisis phase is over.” Maturing principal payments will also be reinvested “until at least the end of 2022”.

Asset purchase programme net purchase will continue at monthly pace of EUR 20B and it’s expected to “run for as long as necessary”. Reinvestments of principal payments will also continue, “for an extended period of time”.

Interest rates are held unchanged, with main refinancing rate at 0.00%, marginal facility rate at 0.25% and deposit rate at -0.50%.

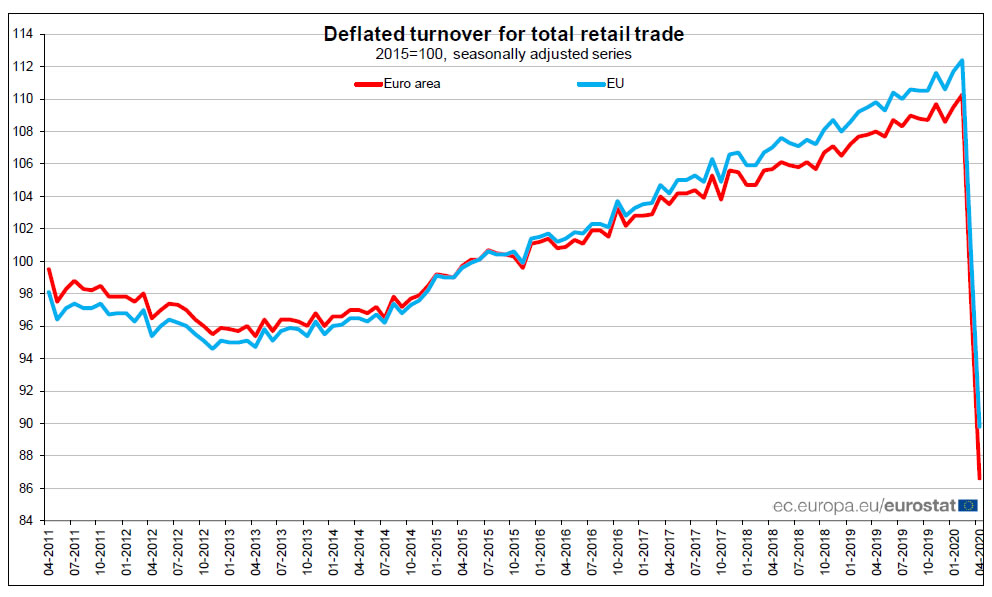

Eurozone retail sales dropped -11.7% mom in April, better than expectation of -15.0% mom. The volume of retail trade decreased by -27.7% mom for automotive fuels, by -17.0% mom for non-food products and by 5.5% for food, drinks and tobacco.

EU retail sales dropped -11.1% mom. Among Member States for which data are available, the largest decreases in the total retail trade volume were registered in Malta (-25.1%), Romania (-22.3%) and Ireland (-21.9%). The only increase was observed in Finland (+0.3%), while the volume in Sweden remained stable.

UK PMI construction rose notably to 28.9 in May, up from 8.2, but missed expectation of 30.0. Still, it was the second lowest level since February 2009 and stayed well below 50 handle. Markit said that severe weakness persists during May, despite gradual reopening of construction sites. There were rapid falls in new orders amid projection cancellations. Supply chain disruptions also remained widespread.

Tim Moore, Economics Director at IHS Markit: “A gradual restart of work on site helped to alleviate the downturn in total UK construction output during May, but the latest survey highlighted that ongoing business closures and disruptions across the supply chain held back the extent of recovery.”Survey respondents often commented on the cancellation of new projects and cited concerns that clients would scale back spending through the second half of 2020, especially in areas most exposed to a prolonged economic downturn.

“With construction firms anticipating a reduced pipeline of work and fewer tender opportunities, business expectations for the next 12 months remained negative in May. Since the start of the lockdown period in March, business sentiment has remained more downbeat than at any time since October 2008.”

ECB monetary policy decision is a major focus for today. After recent rhetorics from the central bank’s officials, markets are generally expecting an expansion of the Pandemic Emergency Asset Purchase (PEPP) to be announced today. Additional, ECB should release new macroeconomic projections that reflect the impact of the coronavirus pandemic.

President Christine Lagarde has already indicated that the “mild scenario” of coronavirus impact is already “out of data”. The development is “it’s very likely that we are somewhere between the medium and severe scenarios”. Thus, GDP projection might be revised down to -8% to -12% for 2020. Inflation forecasts should also be sharply downgraded.

Suggested reading: ECB Preview – Lagarde to Expand PEPP and Sharply Downgrade GDP and Inflation Forecasts.

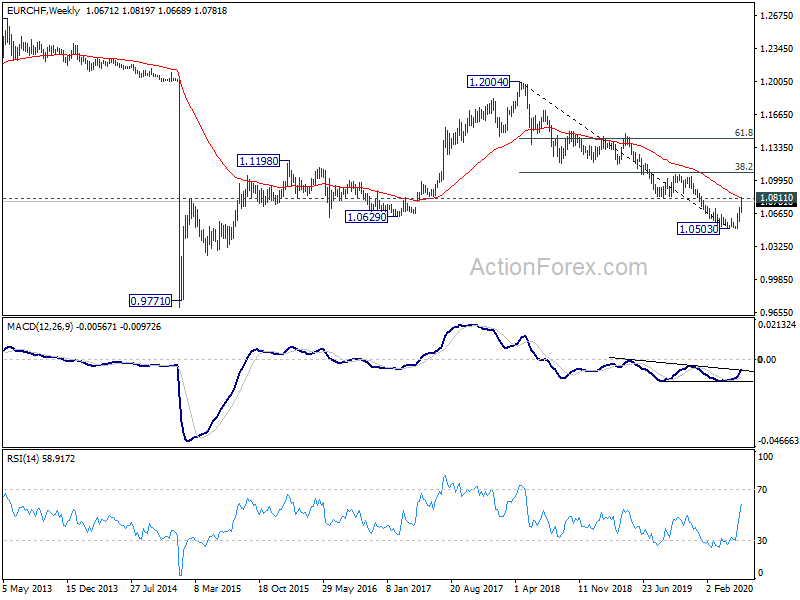

Euro is somewhat turning softer today as markets prepare for ECB decisions. The rebound in the recent weeks against Dollar, Yen, Swiss Franc, and ti a lesser extend Sterling, has been impressive. The case of a massive bullish reversal in Euro is building up. Yet, we’d prefer to see, at least some more decisive signals from EUR/CHF to confirm.

EUR/CHF is now pressing important resistance cluster between 1.0811 support turned resistance and 55 week EMA (now at 1.0826). Sustained break of this resistance zone should confirm medium term bottoming at 1.0503. Rise from there should at least be correcting the down trend form 1.2004 to 1.0503, with chance of trend reversal. In this case, further rally would be seen to 1.1059 cluster resistance (38.2% retracement of 1.2004 to 1.0503 at 1.1076). However, rejection by the current resistance zone will retain medium term bearishness for another low below 1.0503 down the road.

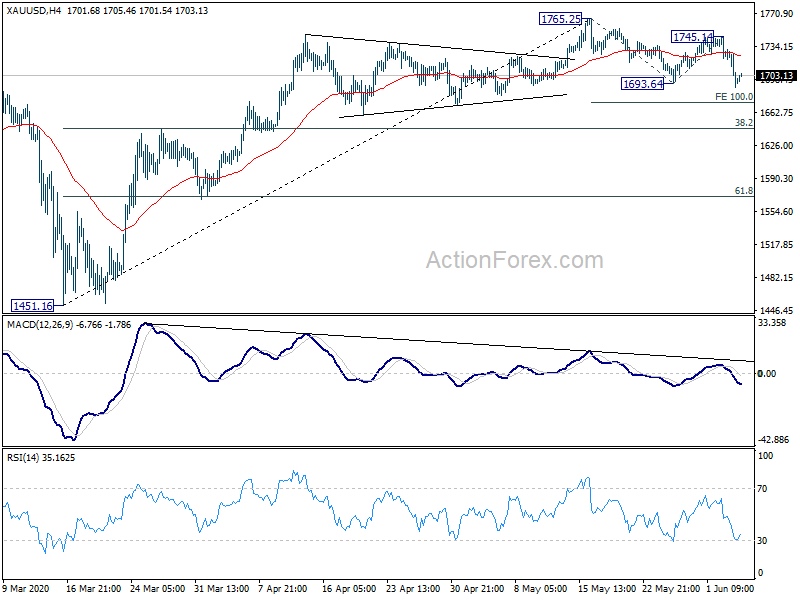

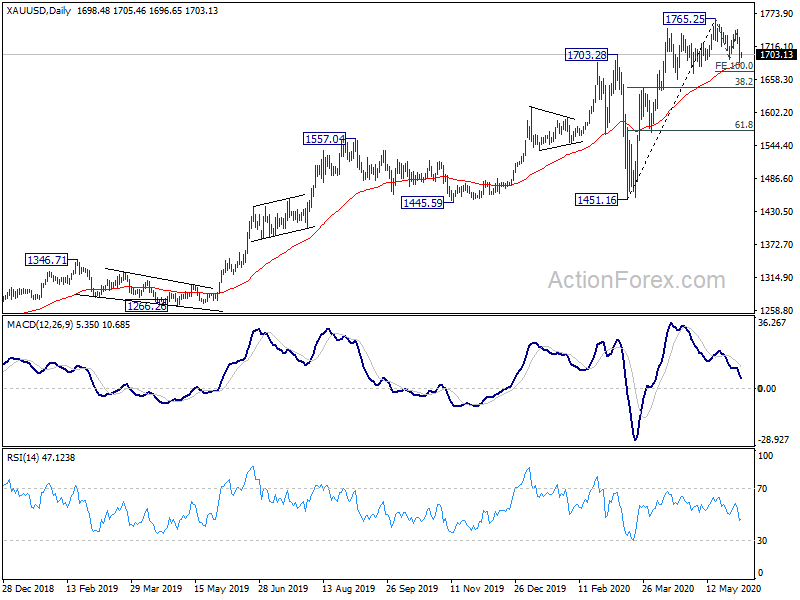

Gold dropped to as low as 1689.36 yesterday and the break of 1693.64 support confirmed resumption of corrective fall from 1765.25. Deeper decline is now expected to 100% projection of 1765.25 to 1693.54 from 1745.14 at 1673.53 next.

Also, we’re holding on to the view that such decline is correcting whole rise from 1451.16 to 1765.25. 55 day EMA (now at 1685.97) is now a focus. Sustained break there will affirm our view and target 38.2% retracement of 1451.16 to 1765.25 at 1645.26 next. In any case, risk will stay on the downside as long as 1746.14 resistance holds, in case of recovery.

Australia retail sales dropped -17.7% mom, more than double of March’s pre-lockdown surge of 8.5% mom. “COVID-19 continued to affect retail trade in April with many retail businesses closing their physical stores during April due to restrictions relating to social distancing” said Ben James, Director of Quarterly Economy Wide Surveys. “There were record falls in cafes, restaurants and takeaway food services (-35.4%), and clothing, footwear and personal accessory retailing (-53.6%), as well as a large fall in department stores (-14.9%).”

In April, in seasonally adjusted terms, exports of goods and services dropped -11% mom to AUD 37.5B. Imports of goods and services dropped -10% mom to AUD 28.7B. Trade surplus narrowed by -16% mom to AUD 8.8B.

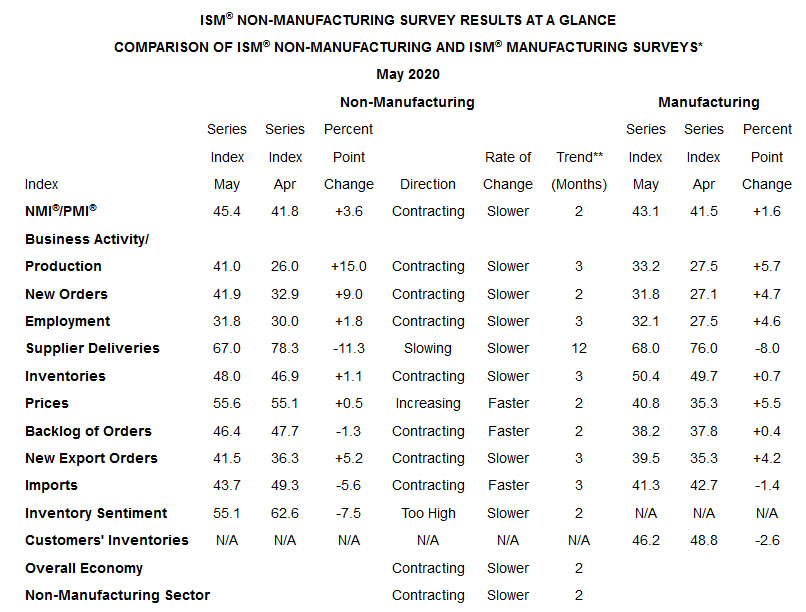

ISM non-manufacturing index rose to 45.4 in May, up from 41.8, slightly above expectation of 43.0. Production improved notably from 26.0 to 41.0, so was new orders, from 32.9 to 41.0. Employment edged up from 30.0 to 31.8. But these three components remained well below 50 handle.

ISM also noted: “The past relationship between the NMI® and the overall economy indicates that the NMI® for May (45.4 percent) corresponds to a 1.1-percent decrease in real gross domestic product (GDP) on an annualized basis.”

BoC kept overnight rate at “effective lower bound” of 0.25% as widely expected. Bank Rate and deposit rates are held correspondingly at 0.50% and 0.25% respectively. The surprise is that it decided to scale back some market operations as financial conditions improved. Though, BoC maintains its commitment to continue large-scale asset purchase until economic recovery is “well underway”.

BoC noted that globally, coronavirus impact “appears to have peaked” even though uncertainty “remains high”. Financial conditions “have improved” and commodity prices “have risen” in recent weeks. Canadian economy appears to have “avoided the most severe scenario” -2.1% Q1 GDP contraction was in the middle of he monitoring rate. Q2 GDP could further decline -10-20%. Recovery is expected to resume in Q3.

On market operations, BoC decided to reduce the frequency of the term repo operations to once per week, and its program to purchase bankers’ acceptances to bi-weekly operations.

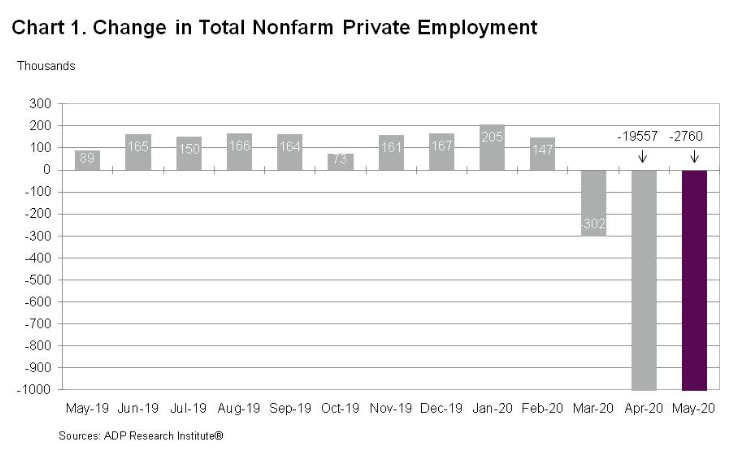

US ADP report showed only -2760k contraction in private sector jobs in May, well below prior months -19557k. By company size, small businesses lost -435k jobs, medium businesses lost -722k, large businesses lost -1604k. By sector, goods-producing companies lost -794k, service-providing companies lost -1967k.

“The impact of the COVID-19 crisis continues to weigh on businesses of all sizes,” said Ahu Yildirmaz, co-head of the ADP Research Institute. “While the labor market is still reeling from the effects of the pandemic, job loss likely peaked in April, as many states have begun a phased reopening of businesses.”

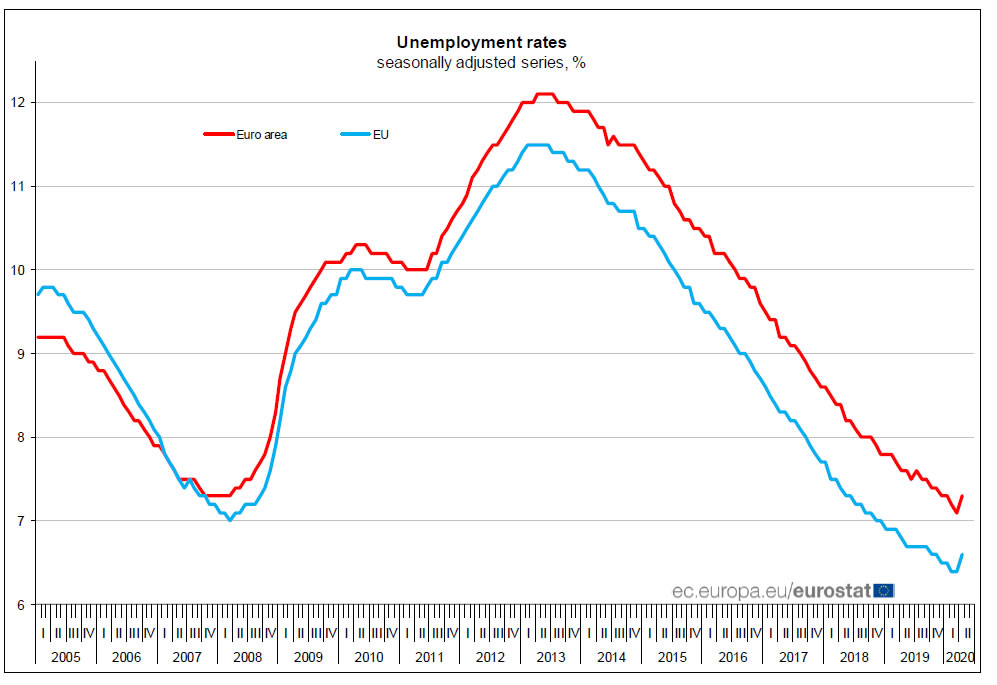

Eurozone unemployment rate rose to 7.3% in April, up from March’s 7.1%. EU unemployment rose to 6.6%, up from 6.4%. Eurostat estimates that 14.079 million men and women in the EU, of whom 11.919 million in the euro area, were unemployed in April 2020. Compared with March 2020, the number of persons unemployed increased by 397000 in the EU and by 211000 in the euro area.

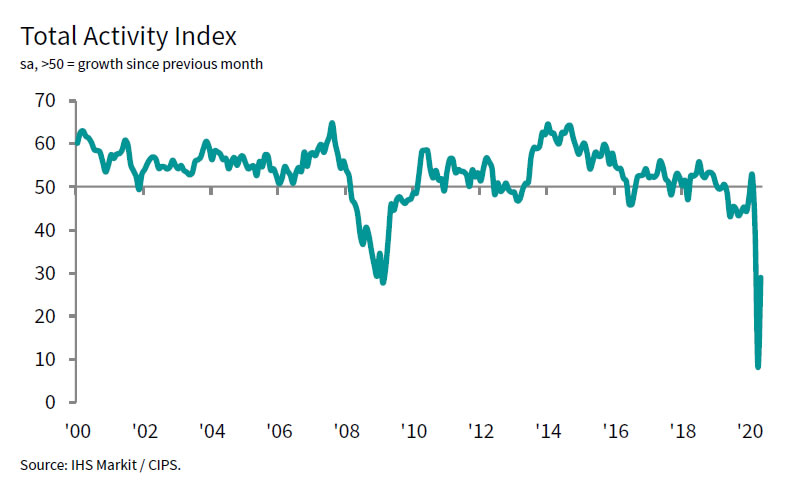

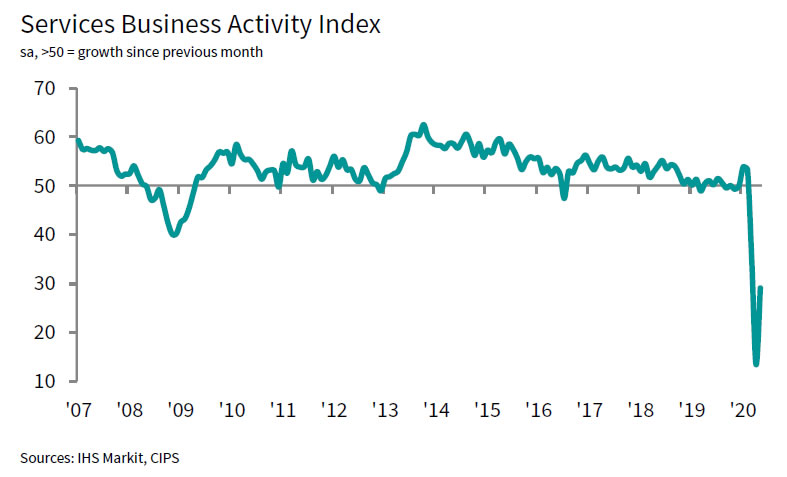

UK PMI Services was finalized at 29.0 in May, up from April’s 13.4. PMI Composite was finalized at 30.0, up from April’s record low of 13.8. Markit said new works slumped amid cutbacks to business and consumer spending. Employment remains on sharp downward trajectory. Business expectations, however, rise again from March’s record low.

Tim Moore, Economics Director at IHS Markit: “The COVID-19 pandemic continued to have a severe impact on UK service sector activity in May, despite a boost in some areas from the gradual easing of lockdown measures. Survey respondents noted that deep cuts to corporate spending had been a major factor dragging down business activity in May, leading to a lack of work to replace completed projects.

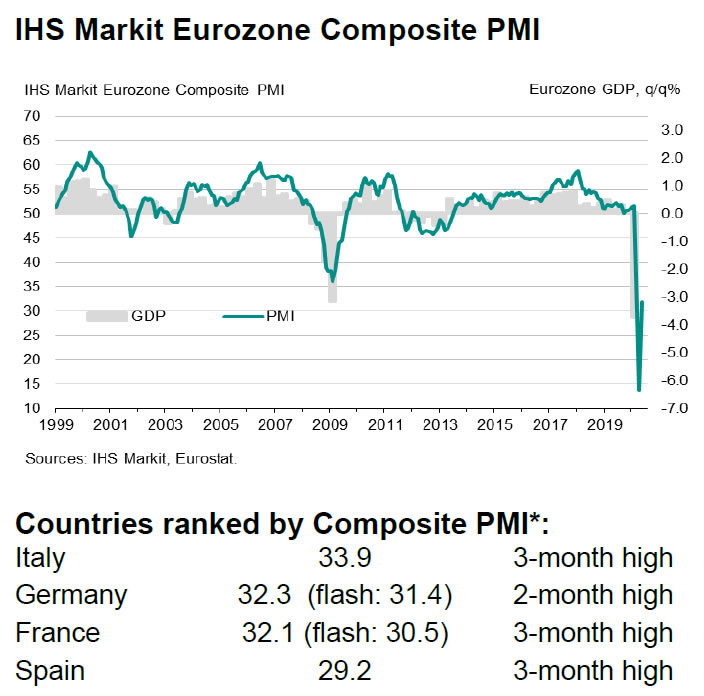

Eurozone PMI Services was finalized at 30.5 in May, up from April’s 12.0. PMI Composite was finalized at 31.9, up from 13.6. Among the member states where data are available, improvement were seen in Italy, Germany, France and Spain. But all PMI composite stayed well below 50, with Italy at 33.9, Germany at 32.3, France at 32.1, Spain at 29.2.

Chris Williamson, Chief Business Economist at IHS Markit said:

Eurozone GDP is consequently set to fall at an unprecedented rate in the second quarter, accompanied by the largest rise in unemployment seen in the history of the euro area.” But ” the downturn has already eased markedly in all countries surveyed.”

“Providing there is no resurgence of infection numbers, the planned lifting of lockdowns will inevitably help boost business activity and sentiment further in coming months. “However, the outlook is scarred by the prospect of demand remaining weak due to household spending being hit by high levels of unemployment and corporate spending being subdued as companies repair balance sheets.”

“We therefore remain cautious with respect to the recovery. Our forecasters expect GDP to slump by almost 9% in 2020 and for a recovery to prepandemic levels of output to take several years.”

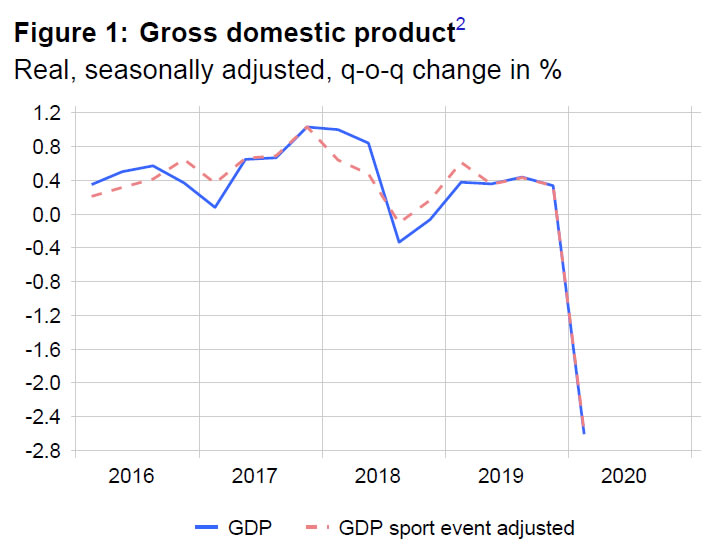

Swiss GDP contracted -2.6% qoq in Q1, worse than expectation of -2.2% qoq. “Due to the coronavirus pandemic and the measures to contain it, economic activity in March was severely restricted. The international economic slump also slowed down exports.”

By production approach, manufacturing dropped -1.3% qoq. Construction dropped -4.2% qoq. Trade dropped -4.4%. Accommodation and food dropped -23.4% qoq. Business services dropped -1.9% qoq. Health and social activities dropped -3.9% qoq. Arts, entertainment and recreation dropped -5.4% qoq. On the other hand, finance and insurance rose 1.5% qoq. Public administration rose 0.8% qoq.

By expenditure approach, private consumption dropped -3.5% qoq. Equipment and software investment dropped -4.0% qoq. Construction investment dropped -0.4% qoq. Export of services dropped -4.4% qoq. Import of goods dropped -1.1% qoq while imports of services dropped -1.2% qoq. On the other and, government consumption rose 0.7% qoq. Exports of goods rose 3.4% qoq.

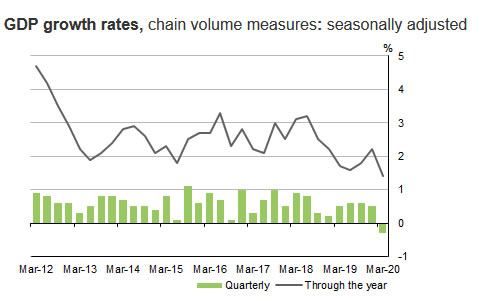

Australia GDP contracted -0.3% qoq in Q1, matched expectations. That’s the first contraction in 9 years. Also, the recession should have started in Q1, for the first time in 29 years. Annually, growth slowed to 1.4% yoy, lowest since September 2009 when Australia was in the midst of the global financial crisis.

Treasurer Josh Frydenberg confirmed that the economy is in recession and “that is on the basis of the advice that I have from the Treasury department about where the June quarter is expected to be.” “Based on what we know from Treasury, we’re going to see a contraction in the June quarter, which is going to be a lot more substantial than what we have seen in the March quarter,” he added.

Though, Frydenberg also said “in the face of a one-in-100-year global pandemic, the Australian economy has been remarkably resilient.” “This strength gave us the fiscal firepower to respond as we have done; Around $260 billion in economic support, or the equivalent of more than 13 per cent of GDP.”

Also from Australia, AiG Performance of Construction Index rose to 24.9 in May, up from 21.6. Building permits dropped -1.8% mom in April, better than expectation of -15.0% mom.

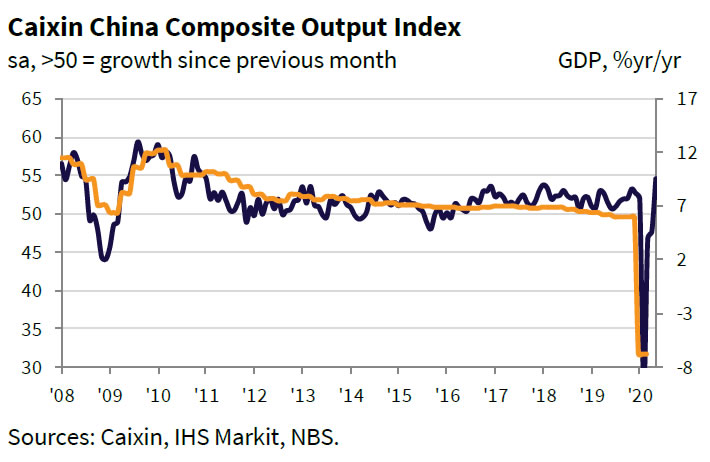

China Caixin PMI Services rose to 55.0 in May, up from April’s 44.4. PMI Composite rose to 54.5, up from 47.6, back in expansion territory. Markit said that business activity and new work rose at quickest pace since late 2010. Pandemic continued to weigh heavily on export orders. Employment fell slightly as firms look to raise efficiency.

Wang Zhe, Senior Economist at Caixin Insight Group said: “In general, the improvement in supply and demand was still not able to fully offset the fallout from the pandemic, and more time is needed for the economy to get back to normal. The composite employment gauge stayed in negative territory as companies were cautious about increasing headcounts. But they were relatively optimistic about the economy’s forward momentum, and look forward to implementation of the policies announced during the annual session of China’s top legislature.”

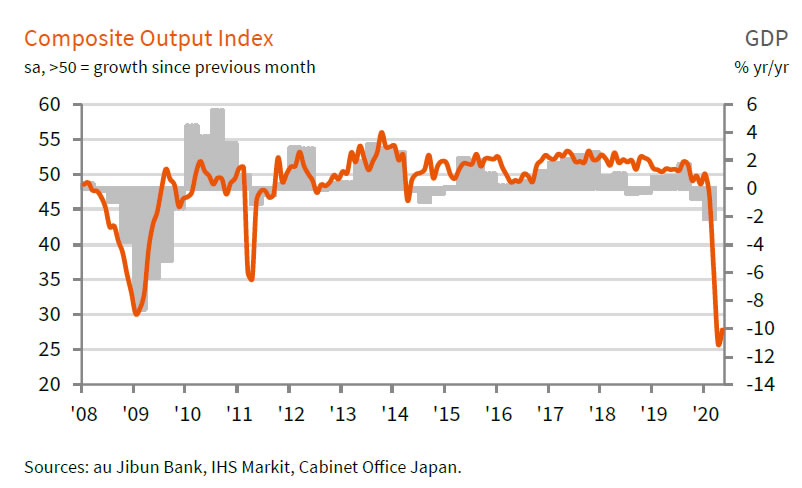

Japan PMI Services improved to 26.5 in May, up from April’s record low of 21.5. PMI Composite also rose slightly to 27.8, up from April’s record low of 25.8. The data signed “historically unparalleled” decline in output.

Joe Hayes, Economist at IHS Markit, said: “While the month of May has seen the Japanese government reduce the stringency of its lockdown, latest survey data indicated that economic activity continued to sink at a rate which had previously been unrivalled before the coronavirus crisis began… Looking at May’s survey data in isolation, the reading of the Composite PMI is indicative of GDP falling by around 10% on an annual basis. Taking into consideration the April reading, which was even worse, it is clear that the impact on second quarter GDP is going to be enormous.”

ActionForex.com was set up back in 2004 with the aim to provide insightful analysis to forex traders, serving the trading community for over a decade. Empowering the individual traders was, is, and will always be our motto going forward.

Contact us: contact@actionforex.com

© ActionForex.com © 2025 All rights reserved.

ECB Lagarde: Improvement in economic tepid comparing with the plummet

In the post meeting press conference, ECB President Christine Lagarde said economic data have shown some signs of a “bottoming-out” in the economy, alongside the gradual easing of coronavirus containment measures. But “the improvement has so far been tepid compared with the speed at which the indicators plummeted in the preceding two months.”

In the baseline scenario of new economic projections, GDP is expected to fall by -8.7% in 2020 (revised down by -9.5% from March projections), then rebound by 5.2% in 2021 (revised up by 3.9%) and 3.3% in 2022. Balance of risks are to the downside.

HICP inflation is projected to be at 0.3% in 2020 (revised down by -0.8%), 0.8% in 2021 (revised down by -0.6%) and 1.3% 2022 (revised down by -0.3%).

Full press conference statement here.