Fed delivered the 25bps rate hike and lifted the federal funds rate to 1.50-1.75% as widely expected. But Dollar bulls are clearly dissatisfied with the updated economic projections. The accompanying statement is nearly a carbon copy of the prior one with balanced changes. It added that “recent data suggest that growth rates of household spending and business fixed investment have moderated from their strong fourth-quarter readings.” But at the same time, “economic outlook has strengthened in recent months.” The interest rate decision was made with unanimous 8-0 vote.

Going into the projections:

Real GDP forecast for 2018 is raised to 2.7% (up from 2.5%), for 2019 raised to 2.4% (up from 2.1%), for 2020 unchanged at 2.0%.

- Implication is that Fed is expecting slight boost from tax cuts in 2018 and 2019. But the impact won’t be long lasting and would fade into 2020.

Unemployment rate forecast for 2018 is lowered to 3.8% (down from 3.9%), for 2019 lowered to 3.6% (down from 3.9%), for 2020 lowered to 3.6% (down from 4.0%).

- The employment market is expected to improve further, with the help of tax cuts and expansive fiscal policy. And the impact would sustain.

PCE inflation forecast for 2018 unchanged at 1.9%, for 2019 unchanged at 2.0%, for 2020 raised to 2.1% (up from 2.0%)

Core PCE inflation forecast for 2018 unchanged at 1.9%, for 2019 raised to 2.1% (up fro 2.0%), for 2020 raised to 2.1% (up from 2.0%).

- While unemployment rate would continue to drop, GDP growth to stay solid, inflation will pressure will remain contained. Fed is seeing the current pattern to continue.

Federal funds rate projection for 2018 unchanged at 2.1%, 2019 raised to 2.9% (up from 2.7%), 2020 raised to 3.4% (up from 3.1%).

- This is possibly what disappointed dollar bulls most. It implies Fed will stick with the course of only three rate hike this year. There might be one more hike in 2019 to three in total, thanks to the GDP growth in both 2018 and 2019, as well as the steep improvement in labour market. And, Fed is more confident that there will be another two rate hikes in 2020.

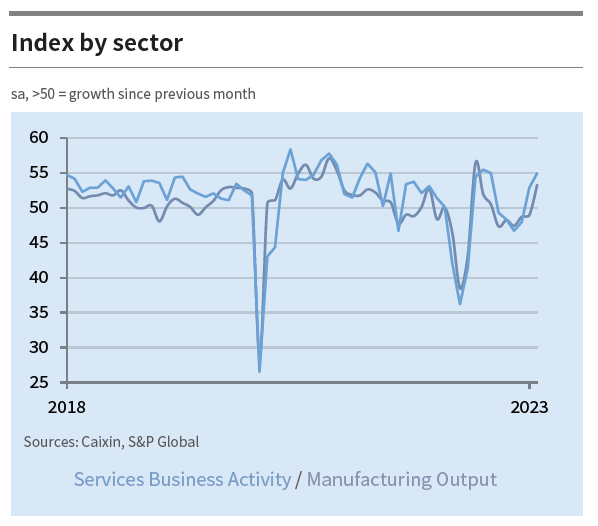

UK PMI manufacturing finalized at 60.9, marked growth spurt beset by supply chain issues

UK PMI Manufacturing was finalized t 60.9 in April, up from 58.9. That’s also the highest reading since July 1994’s record high at 61.0. Markit said production and new order growth strengthened. Output prices rose at record pace.

Rob Dobson, Director at IHS Markit, said: “Further loosening of COVID-19 restrictions at home and abroad led to another marked growth spurt at UK factories. The headline PMI rose to a near 27-year high, as output and new orders expanded at increased rates. The outlook for the sector is also increasingly positive, with two-thirds of manufacturers expecting output to be higher in one year’s time. Export growth remains relatively subdued, however, as small manufacturers struggle to export.

“The sector also remains beset by supply-chain issues and rising inflationary pressures. Disruption following Brexit and COVID-19, especially at ports, caused a further near-record lengthening of supplier delivery times. The resulting input shortages kept producer price inflation among the highest over the past four years. Manufacturers have generally passed on these costs to customers, as highlighted by a survey-record rise in selling prices, but it is hoped that this inflationary backdrop will subside once supply and demand come back into line as covid-related logistic delays ease.”

Full release here.