Risk aversion ran wild as stock markets and other risk assets plummeted on global tariff escalation. The US dollar’s early gains during the end of May market rout is starting to reverse course on expectations the Fed may cut rates twice this year. Stocks are licking their wounds following a double dose of negative trade news. The first bullet came from China’s retaliatory measures that will deliver a crippling blow to multi-nationals and likely further downgrade earnings forecasts as the Sino-US relationship appears to going towards a path of irreparable damage. The second bullet came from the escalation in trade tensions between Mexico and US, which pretty much came out of nowhere. The trade spat with China has been brewing, but markets were taken back with the US actions towards Mexico. The US, Mexico and Canada were in the process of getting the USMCA approved with their respective governments, but that may have hit a road block now. President Trump’s attack to their southern neighbor saw a Mexican response that US exports of grains, pork, and apples may be hit with tariffs. Tariff escalation is detrimental to global growth and the bond market saw Bunds fall to a record low and the 10-year Treasury yield dropped to a fresh 20-month low and fell further below the Fed’s fund target range.

Markets will continue to care about every incremental trade update, but they should also closely pay attention to a couple important rate decisions and a wrath of Fed speak, which includes Chair Powell’s discussion on policy strategy. On Monday, President Trump will also make a state visit to the UK, where he will meet with Queen Elizabeth and PM May. Tuesday, the RBA is expected to cut rates and we hear from Fed Chairman Jerome Powell at a Fed Research Conference. Wednesday, the EIA releases their crude oil weekly report and the Fed releases the Beige book and members Clarida and Bostic speak. On Thursday, the ECB will keep policy steady and update their economic forecasts. Friday will see PM May step down as the leader of the conservative party and have the release of the US employment report, which expects to see hiring deliver 185,000 new jobs in May.

- RBA to cut rates and signal more are coming

- ECB to downgrade forecasts and give details on next round of TLTROs

- Fed’s Speakers to address recent trade war escalation and possible capitulation on cuts

RBA

On Tuesday, the Reserve Bank of Australia (RBA) is widely expected to cut the cash rate by 25 basis points to 1.25%, with investors focusing on how many more cuts will be queued up. Only 5% of economists, two specifically, see the RBA keep rates steady. At the last meeting, the RBA surprised many when they kept policy following disappointingly weak first-quarter inflation.

The RBA may decide on holding off on confirming any additional rate cuts, preferring to see how the global growth slowdown hits their domestic economy. The recent global bond rally took the Australian 10-year yield below the RBA’s cash rate of 1.5%, for the first time since 2015. Analysts are piling on the rate cut bets, JP Morgan sees rates falling to 0.50% by mid-2020 while Westpac and Capital Economics see cuts targeting 0.75%. With tame inflation, the RBA’s easing decision should be an easy one.

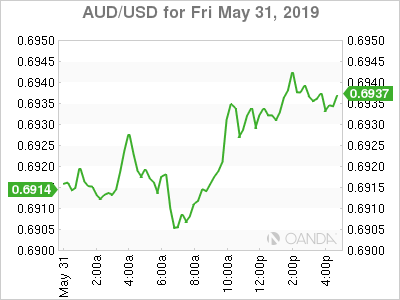

The Australian dollar remains near the lows of the year, as the recent escalation in trade wars dims global growth outlooks, and while data points in the Asia-Pacific continue to deteriorate. With China’s May manufacturing PMI falling back into contraction, expectations remain high the PBOC will come to the rescue. While the market begins pricing in further RBA rate cuts, we could limited Australian dollar downside as the greater driver could be the Fed’s capitulation with delivering their own rate cuts.

Fed

A wrath of Federal Reserve members will speak next week, with investors waiting to see further confirming signals that the Fed will provide further accommodation shortly. On Tuesday, Fed Chair Jerome Powell will discuss monetary policy strategy, tools, and communication practices at the Fed’s framework review conference in Chicago. Markets have not heard from Powell since the trade war went on steroids and he could use this as his stage to begin capitulate and signal accommodation is needed. The Fed’s preferred core price measure in April stayed steady at 1.6%, but still comfortably below the Fed’s 2% target. The US trade war escalations with China and Mexico will likely dominate the Fed’s concerns here and while the data-dependent script may suggest they need to see further data confirm weakness, they might agree that is not necessary.

ECB

The ECB rate decision is expected to see no change with rates and possibly minor downgrades with their economic forecasts. The central bank will also deliver more details on the expected launch of its third round of targeted long-term refinancing operations in September. Economists are expecting them to use TLTROs as a backstop, which could provide insurance in times of heightened uncertainty. With most of the other G7 central banks on the verge of providing stimulus, expectations are rising for the ECB to also provide fresh support to the ailing economy. Global trade wars are raising the risk for a euro zone recession, but that is still not the base case. The current implied interest rate probabilities see a 53% chance that the ECB cuts rates at the January 23rd 2020 meeting.

The upcoming meeting should see the ECB provide a slight adjustment to forward guidance becoming more accommodative. Economists however still are not abandoning a rate hike in the near future and that should provide some support for the euro. A Reuters poll showed 47% of the 60 contributors expect a rate hike at some point between now and the end of 2020, while 3% saw a cut and the rest expect no change in rates.

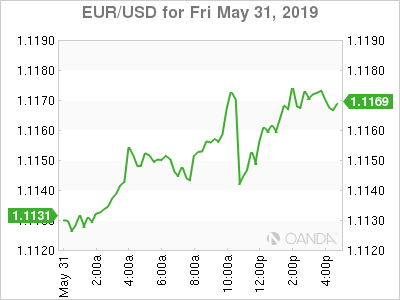

The euro remains stuck in very tight range and we should see 1.11 remain formidable support, while 1.1250 provides initial resistance.

Oil

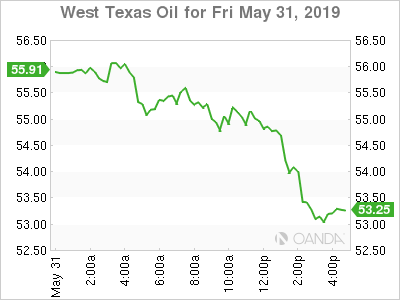

The month of May was a disaster for crude prices, the worst May performance in seven years, as unabrupt escalation with global trade war saw the global growth outlook crumble. Oil prices have now given up the lion share of the effects of the OPEC + production cuts. Geopolitical risks remain in place but right now demand growth is in freefall and oil remains vulnerable. The US – China trade war remains most critical to the global growth outlook, but the addition of trade tensions between the US and Mexico raised the slower demand picture for the Americas.

West Texas Intermediate crude’s selloff is now around 20% lower from the April 23rd high of $66.60. With rising expectations that OPEC will be less effective in signaling continued production cuts going forward, crude will need to rely on some positive outcomes on the trade front for prices to begin stabilizing.

Gold

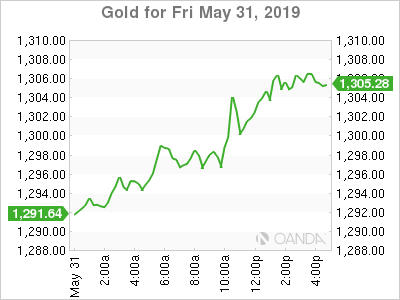

It took a while, but gold prices finally broke out higher after the trade war escalation led to a code red for global growth. A devastating month for equities, the worst one since December, and other risk assets saw a global bond rally lead the way for safe-haven assets. The yellow metal is once again becoming an attractive safe-haven as markets will remain skeptical on any trade progress after seeing how fast we could see Trump deliver a new tariff threat.

Sunday, June 2nd

9:45pm ET CNY Caixin Manufacturing PMI

Monday, June 3rd

2:30am ET CHF CPI m/m

3:15am ET EUR Spain Manufacturing PMI

3:45am ET EUR Italy Manufacturing PMI

3:50am ET EUR France Manufacturing PMI

3:55am ET EUR Germany Manufacturing PMI

4:00am ET EUR Eurozone Manufacturing PMI

4:30am ET GBP Manufacturing PMI

10:00am ET USD ISM Manufacturing PMI

10:00am ET USD Construction Spending m/m

9:30pm ET AUD Retail Sales m/m

Tuesday, June 4th

12:30am ET AUD RBA Interest Rate Decision

3:00am ET EUR Spain Unemployment m/m

4:30am ET GBP Construction PMI

5:00am ET EUR CPI Flash Estimate y/y

5:30am ET ZAR GDP Annualized q/q

9:00am ET MXN Consumer Confidence Index

10:00am ET USD Factory Orders m/m

10:00am ET USD Final Durable Goods Orders

9:30pm ET AUD GDP q/q

9:45pm ET CNY Caixin Services PMI

Wednesday, June 5th

4:30am ET GBP Services PMI

5:00am ET EUR Eurozone PPI m/m

5:00am ET EUR Eurozone retail sales m/m

8:15am ET USD ADP Employment Change

9:45am ET USD Final Markit Services PMI

10:00am ET USD ISM Non-Manufacturing Index

10:30am ET DOE US Crude Oil Inventories

1:00pm ET NZD QV House Prices y/y

9:30pm ET AUD Trade Balance

9:30pm ET AUD Building Approvals m/m

Thursday, June 6th

2:00am ET EUR Germany Factory Orders m/m

7:45am ET EUR ECB Interest Rate Decision

8:30am ET USD Trade Balance

8:30am ET USD Initial Jobless Claims

7:30pm ET JPY Household Spending y/y

Friday, June 7th

2:00am ET EUR Germany Industrial Production m/m

2:00am ET EUR Germany Trade Balance

2:00am ET NOK Norway Production data

2:45am ET EUR Industrial Production m/m

3:30am ET GBP Halifax House Prices m/m

8:30am ET USD Non-Farm Payroll Report, Unemployment Rate and Wage Data

8:30am ET CAD Employment Change and Unemployment Rate

9:00am ET MXN CPI y/y