More central bank meetings will follow in the coming week, this time with the Reserve Bank of Australia, while things will heat up a little on the data front as September PMIs are on the agenda, as well as the all-important US jobs report. Although investors have recently pared some of their bleakest outlook for global growth and recession risks have receded somewhat, the incoming data will nevertheless be watched closely as trade tensions could flare up at any moment. Meanwhile, as temperatures reach boiling point at Westminster expect no letup in the unfolding Brexit drama.

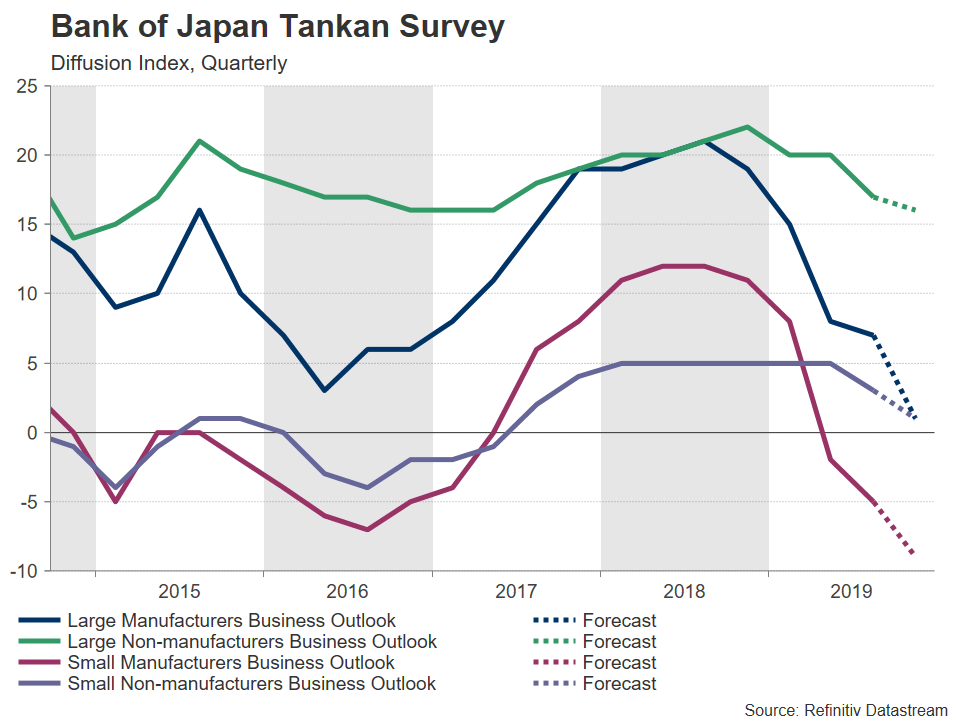

BoJ Summary and Tankan survey could hint at October stimulus

It will be a busy start to the week in Japan as apart from major data releases, the Bank of Japan will publish the Summary of Opinions of its September policy meeting. The Bank had signalled possible easing in October at the last meeting, saying it will “reexamine economic and price developments at the next MPM”. The Summary is likely to reveal the extent to which policymakers debated fresh stimulus to boost flagging growth and inflation, and if they’re leaning towards approving further monetary easing at the next meeting on October 30-31.

The Bank’s own Tankan business survey for the third quarter, due on Tuesday, will also be key in determining whether policy adjustment is on the cards. The Tankan report is an important indicator of business confidence and outlook for various sectors of the economy as well as a barometer for corporate spending. A sharp deterioration in business sentiment and investment plans would strengthen the case for the BoJ to act at its next meeting.

Other data to watch out of Japan are retail sales and preliminary industrial output readings on Monday and jobs numbers on Tuesday, all for August.

Any hints of policy easing would impose downside pressure on the yen. But with the BoJ’s arsenal almost depleted, a big sell-off seems improbable and can be easily offset by safety buying should risk aversion set in.

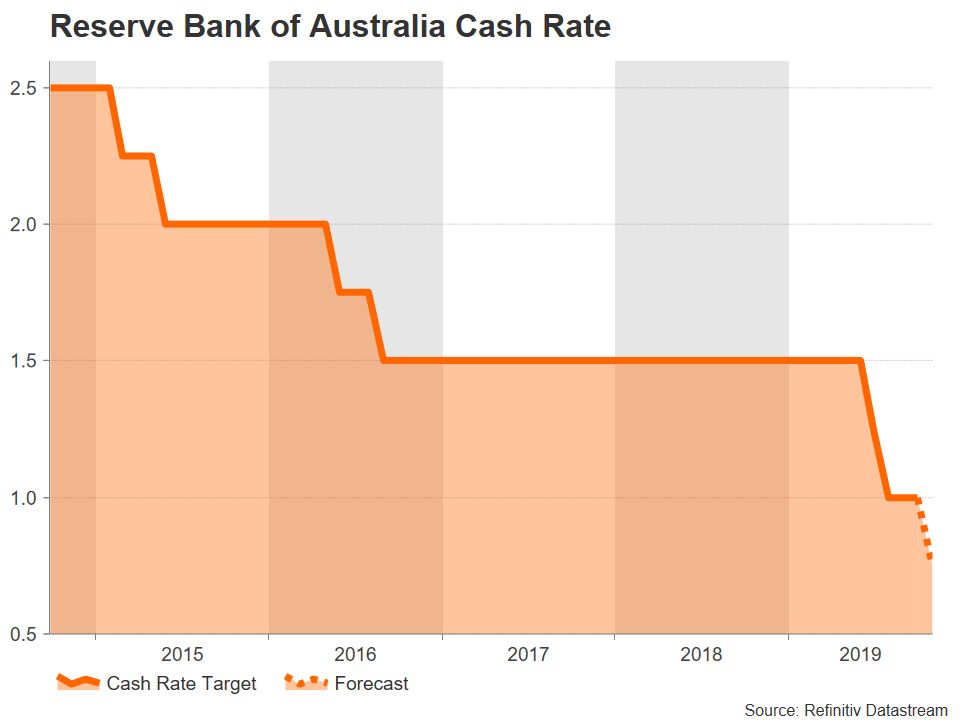

RBA to make third cut

The Reserve Bank of Australia’s governor, Philip Lowe, gave confusing messages about the policy direction in remarks made earlier this week. Lowe took markets by surprise when he said the Australian economy is at a “gentle turning point”. His unexpected optimism suggested a rate cut at the next meeting on Tuesday may not be a done deal. However, he also indicated it was a priority to prevent the exchange rate from appreciating. Hence, investors still think that the RBA will lower rates in October for the third time this year and are pricing around a 77% probability of a 25-basis points cut.

The Australian dollar is likely to come under pressure from a rate cut, though the bigger focus will be on whether the RBA will signal further reductions in the cash rate. A hawkish cut could see the aussie spiking higher.

Traders should also keep an eye on a raft of data for August expected out of Australia next week. Private sector credit numbers are due on Monday, followed by the AIG manufacturing index and building approvals on Tuesday, trade figures on Thursday and retail sales on Friday.

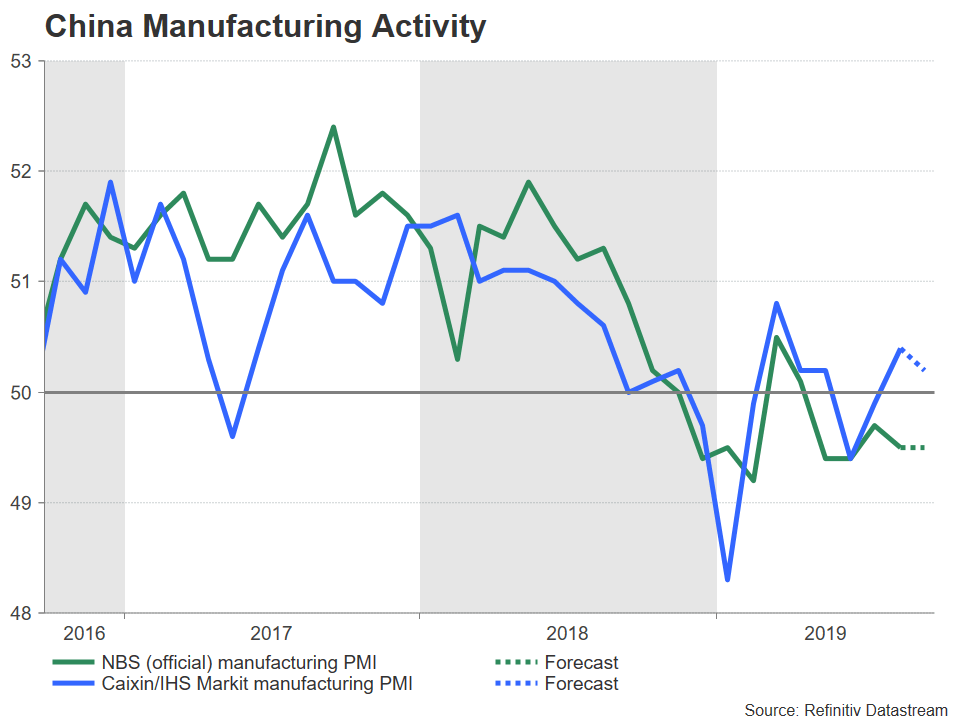

Chinese PMIs eyed before week-long holiday

Asian trading volumes are expected to be thin next week as Chinese markets will be closed from Tuesday onwards for National Day. But before local traders desert their desks, the latest manufacturing gauges will come under the spotlight on Monday.

Those hoping for a turnaround in China’s gargantuan manufacturing sector will probably be disappointed as the official manufacturing PMI is forecast to have stayed unchanged at 49.5 in September, pointing to continued mild contraction. In contrast, the IHS Markit/Caixin PMI is expected to have held above the 50 level that separates expansion from contraction, but to have eased slightly to 50.2.

Any worrying readings from the Chinese PMIs are bound to hurt the risk-sensitive Australian and New Zealand dollars. The kiwi will also be susceptible to surveys out of New Zealand. The ANZ business outlook report for September is due on Monday and the NZIER quarterly business opinion is out on Tuesday. Investors will be watching for signs that the Reserve Bank of New Zealand’s rate cuts are starting to lift business morale as any improvement could further temper expectations of a rate cut in November, following somewhat less dovish remarks from the RBNZ Governor this past week.

Few drivers for sagging euro and pound

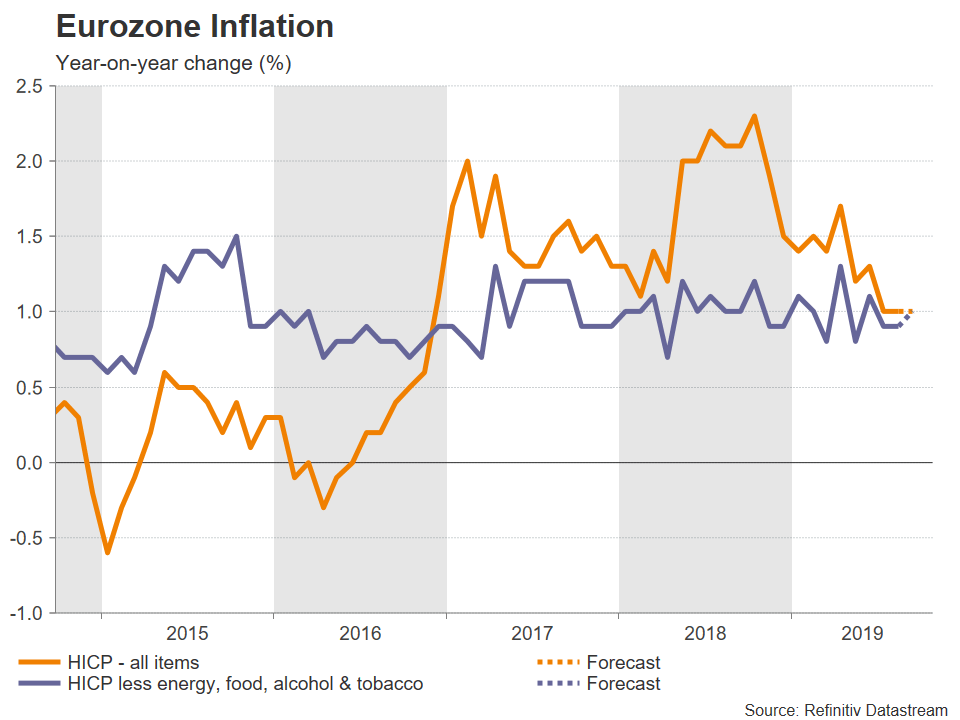

It hasn’t been a good week for the euro and pound as growth and Brexit jitters have dragged the currencies to fresh lows. There’s little in next week’s European and UK calendars that could lift either currency out of the doldrums.

For the Eurozone, the highlight will be the flash inflation prints for September on Tuesday. The headline rate of inflation is expected to have held steady at 1.0% year-on-year in September. The data is unlikely to have a major impact on the euro as the European Central Bank is anticipated to stay on hold for the time being given the splits within the Governing Council on the need for further monetary easing. Instead, traders will be more interested in news of possible fiscal stimulus in the bloc, particularly Germany.

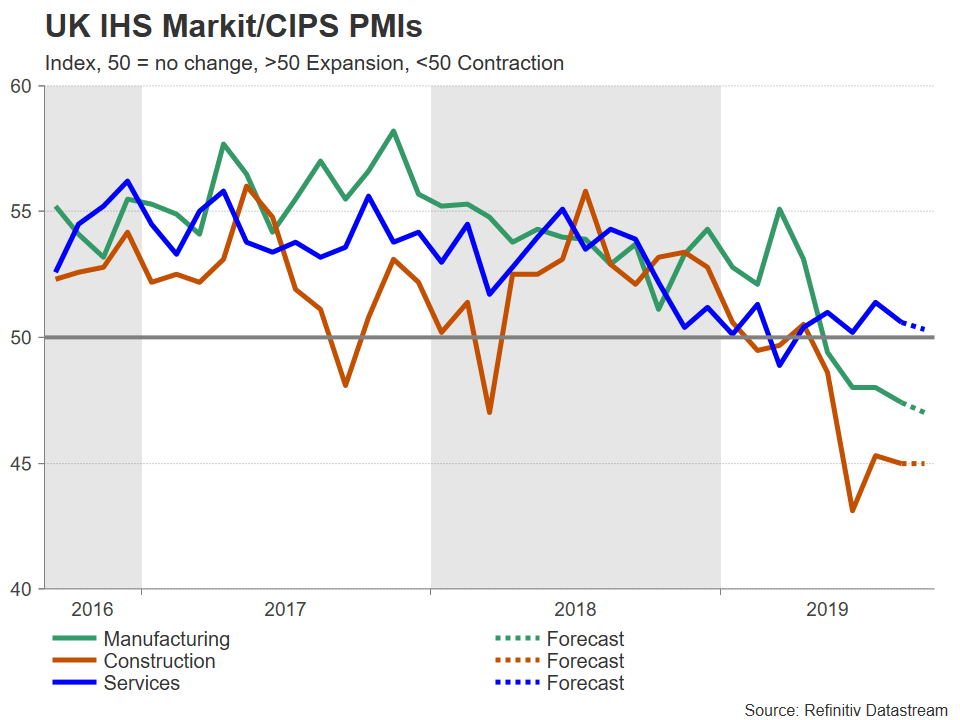

Over in the UK, revised GDP estimates and the Markit/CIPS PMIs should attract attention for pound traders, though sterling will continue to be steered mostly by Brexit developments. A snap general election is looking increasingly off the table before October 31 and so the big question now is if Prime Minister Johnson can agree a revised deal with the EU. With some sign of movement in the Brexit talks, the pound stands to gain from any positive headlines.

There’s likely to be a more muted reaction, however, to Monday’s second estimate of GDP growth in Q2 where no revision is expected to the initial reading of -0.2% quarter-on-quarter, and the manufacturing, construction and services PMI prints on Tuesday, Wednesday and Thursday, respectively.

Dollar to take its cues from ISM PMIs and nonfarm payrolls report

With the US Federal Reserve pushing back on excessive rate cut expectations, investors have only marginally adjusted their bets of aggressive easing. This suggests there’s plenty of scope for additional gains for the US dollar should the incoming data further allay recession concerns.

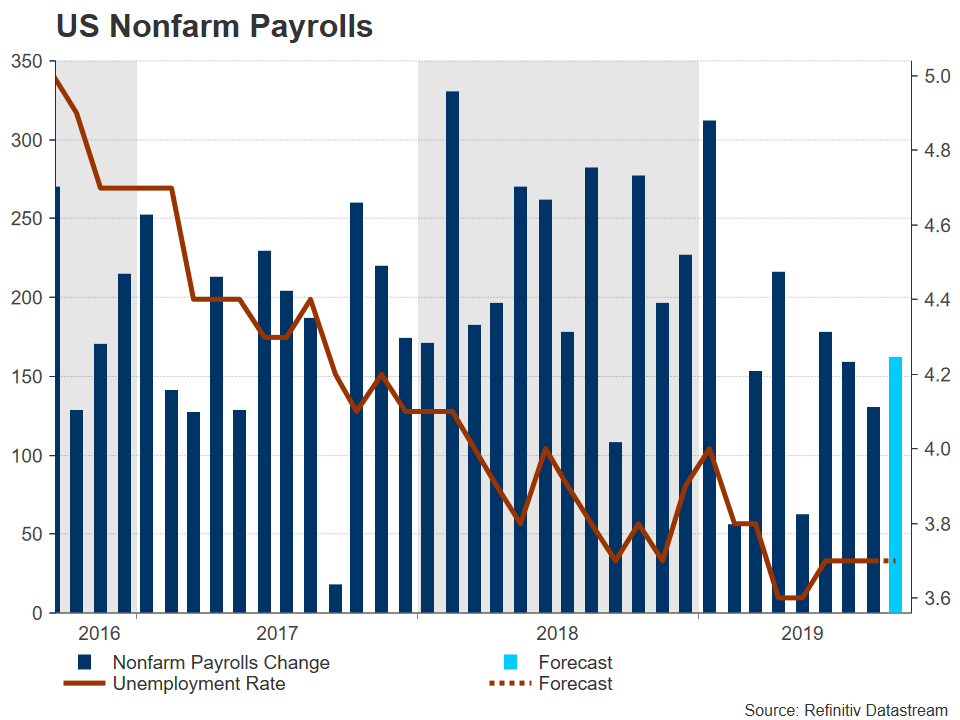

Kicking off the week in the United States will be the Chicago PMI for September on Monday. On Tuesday, all eyes will be on the ISM manufacturing PMI after the index fell below 50 in August for the first time in three years, briefly heightening fears of a downturn. There might be some relief, however, if the PMI recovers to 50.4 in September as forecast. The ISM’s non-manufacturing PMI will follow on Thursday, though forecasts are for the composite index to fall slightly to 55.8 in September. Factory orders are also due on Thursday, before attention turns to the nonfarm payrolls report on Friday.

After moderating to 130k in August, nonfarm payrolls are anticipated to have picked up to 162k in September. The unemployment rate is forecast to remain unchanged at 3.7%, while average hourly earnings are projected to have increased by 0.3% month-on-month.

An overall stronger-than-expected payrolls report could push the dollar index beyond this week’s 3-week top. But with the greenback’s advances not supported by a similar move in Treasury yields, weak jobs numbers could lead to a sharp retreat in the currency.

Finally, across the border in Canada, monthly GDP figures will be looked at on Tuesday for clues on whether Canada’s economy continues to defy the global economic gloom. However, even if another solid GDP growth is recorded in July, the boost to the Canadian dollar is likely to be short-lived as the currency’s broader trend appears to be driven by the trade war risks.

{kind=link}