Sample Category Title

ECB SAFE survey: Firms see slower inflation, trade shocks reorder priorities

The ECB’s latest SAFE (Survey on the Access to Finance of Enterprises) report showed that Eurozone firms have revised down their short-term inflation expectations while maintaining a cautious view on long-term price pressures. The median forecast for inflation one year ahead dropped to 2.5% from 2.9%. Expectations for three- and five-year horizons remained steady at 3.0%.

When asked about risks to five-year inflation, 52% of firms still viewed them as skewed to the upside, though that figure declined slightly from 55%. The share of firms seeing balanced risks increased to 33%, while those perceiving downside risks remained unchanged at 14%.

This round also included ad hoc questions about the impact of rising trade tensions, particularly recent US tariff announcements. The survey revealed uneven exposure across firms, with exporters to the US and manufacturing companies facing the greatest challenges. About 30% of respondents reported concerns over supply chain disruptions, including delays and shortages.

In response, many businesses are already pivoting. Firms cited plans to reorient sales toward domestic and EU markets and restructure supply chains to reduce dependency on vulnerable links.

Full ECB Survey on the Access to Finance of Enterprise here.

Japan’s Coalition Loses Majority, Yen Higher

The Japanese yen has started the week with strong gains. In the European session, USD/JPY is trading at 147.71, down 0.73% on the day.

Japanese PM on shaky ground after election drubbing

Japanese Prime Minister Ishiba's ruling coalition failed to win a majority in the election for the upper house of parliament on Sunday. The result is a humiliating blow to Ishiba, as the government lost its majority in the lower house in October.

The stinging defeat could be the end of the road for Ishiba. The Prime Minister has declared he will remain in office, but there is bound to be pressure from within the coalition for Ishiba to resign.

The election result was not a surprise, as voters were expected to punish the government at the ballot box due to the high cost of food and falling incomes. The price of rice, a staple food, has soared 100% in a year, causing a full-blown crisis for the government, which has resorted to selling stockpiled rice from national reserves to the public.

The election has greatly weakened Ishiba's standing, which is bad news as Japan is locked in intense trade talks with the US. President Trump has warned that he will impose 25% tariffs on Japanese goods if a deal isn't reached by August 1. Japan is particularly concerned about its automobile industry, the driver of its export-reliant economy.

Bank of Japan expected to stay pat

The Bank of Japan meets on July 31 and is widely expected to continue its wait-and-see stance on rate policy. The BoJ has been an outlier among major central banks as it looks to normalize policy and raise interest rates. However, with the economic turbulence and uncertainty due to President Trump's erratic tariff policy, the Bank has stayed on the sidelines and hasn't raised rates since January. Japan releases Tokyo Core CPI on Friday, the last tier-1 event before the rate meeting.

USD/JPY Technical

- There is resistance at 148.39 and 149.08

- 147.95 and 147.70 are the next support levels

USDJPY 1-Day Chart, July 21, 2025

ETH/USD Rate Surges Over 50% Since Early July

Back in May, we reported that the Ethereum network had successfully undergone a major upgrade named Pectra, which triggered a surge in demand for Ethereum and a confident upward movement in the ETH/USD rate (indicated by the arrow on the chart).

At the time, we also suggested that the $1,800 to $2,300 range could be considered a broad bullish Fair Value Gap, meaning it could act as a support zone for ETH/USD in the event of a pullback.

Indeed, the price did retreat into the $1,800–$2,300 zone, with the B→C correction forming a textbook 50% retracement of the A→B impulse. After a brief consolidation, the upward trend resumed. Bullish sentiment was further supported by regulatory improvements in the US, particularly the passing of legislation on stablecoins, which fostered a more favourable environment for the development of new projects on the Ethereum blockchain.

These and other fundamental drivers contributed to a more than 50% increase in ETH/USD throughout July.

Technical Analysis of the ETH/USD Chart

Since April, ETH/USD price movements have been forming an ascending channel (highlighted in blue), with the price entering the upper half of the channel by mid-July. This move was accompanied by the formation of new highs without significant pullbacks—an indication of strong demand.

Given the inherent inertia of financial markets, it is difficult to imagine a sharp reversal from a bullish to a bearish trend. However, there are reasons to believe that the steep upward movement in ETH’s price may slow in the near term:

→ the price is approaching the upper boundary of the channel, which typically acts as resistance;

→ the RSI indicator has remained in overbought territory for several days;

→ the psychologically significant $4,000 level may also act as resistance, as it has on previous occasions (e.g., in December 2024).

FXOpen offers the world's most popular cryptocurrency CFDs*, including Bitcoin and Ethereum. Floating spreads, 1:2 leverage — at your service. Open your trading account now or learn more about crypto CFD trading with FXOpen.

*Important: At FXOpen UK, Cryptocurrency trading via CFDs is only available to our Professional clients. They are not available for trading by Retail clients. To find out more information about how this may affect you, please get in touch with our team.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

GBP/USD Dips Further While USD/CAD Consolidates Gains

GBP/USD started a downside correction from the 1.3620 zone. USD/CAD declined and now consolidates below the 1.3750 level.

Important Takeaways for GBP/USD and USD/CAD Analysis Today

- The British Pound started a fresh decline and settled below the 1.3500 zone.

- There is a connecting bullish trend line forming with support at 1.3415 on the hourly chart of GBP/USD at FXOpen.

- USD/CAD started a fresh decline after it failed to clear the 1.3775 resistance.

- There is a key bullish trend line forming with support at 1.3715 on the hourly chart at FXOpen.

GBP/USD Technical Analysis

On the hourly chart of GBP/USD at FXOpen, the pair struggled above the 1.3600 zone. The British Pound started a fresh decline below the 1.3550 pivot level against the US Dollar, as discussed in the previous analysis.

The pair dipped below the 1.3500 and 1.3450 levels. A low was formed at 1.3364 and the pair is now consolidating losses. On the upside, it is facing resistance near the 1.3475 level. The next key resistance is near 1.3490 and the 50% Fib retracement level of the downward move from the 1.3619 swing high to the 1.3364 low.

An upside break above the 1.3490 zone could send the pair toward 1.3520 and the 61.8% Fib retracement level.

More gains might open the doors for a test of 1.3620. If there is another decline, the pair could find support near the 1.3415 level and a connecting bullish trend line. The first major support sits near the 1.3365 zone.

The next major support is 1.3350. If there is a break below 1.3350, the pair could extend the decline. The next key support is near the 1.3320 level. Any more losses might call for a test of 1.3250.

USD/CAD Technical Analysis

On the hourly chart of USD/CAD at FXOpen, the pair climbed toward the 1.3775 resistance zone before the bears appeared. The US Dollar formed a swing high near 1.3774 and recently declined below the 1.3750 support against the Canadian Dollar.

There was also a close below the 50-hour simple moving average and 1.3735. The pair is now consolidating losses below the 50% Fib retracement level of the downward move from the 1.3774 swing high to the 1.3695 low. But the bulls are active near the 1.3700 level.

If there is a fresh increase, the pair could face resistance near the 1.3735 level. The next key resistance on the USD/CAD chart is near the 1.3755 level or the 61.8% Fib retracement level.

If there is an upside break above 1.3755, the pair could rise toward 1.3775. The next major resistance is near the 1.3800 zone, above which it could rise steadily toward 1.3880.

Immediate support is near the 1.3715 level and a key bullish trend line. The first major support is near 1.3675. A close below the 1.3675 level might trigger a strong decline. In the stated case, USD/CAD might test 1.3650. Any more losses may possibly open the doors for a drop toward the 1.3620 support.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Singapore Stocks Hit Record High, Gold (Chart of the Day) Bullish Momentum Building Up

Asia Pacific stock markets opened the week on a mixed note. Singapore’s Straits Times Index (STI) led the pack, surging 0.5% intraday to a new all-time high of 4,225, breaking above the psychological 4,200 mark and continuing its bullish run.

Singapore leads Asia as STI hits record high, Hang Seng extends gains, ASX 200 lags

Hong Kong’s Hang Seng Index added 0.3%, building on last Friday’s breakout above the 19 March 2025 high. In contrast, Australia’s ASX 200 underperformed with a sharp 1.2% decline, reflecting divergent regional market sentiment.

Japan markets react calmly to the election outcome

Sunday’s Upper House election in Japan resulted in the ruling LDP-Komeito coalition losing its majority. However, the market response was relatively muted as the outcome had already been priced in. The Japanese yen recovered 0.4% intraday after falling to a three-month low last week. Nikkei 225 futures gained 0.3% on Globex trading, although the Tokyo market remained shut for a public holiday.

Dovish Fed comments weigh on US Dollar

The US dollar stayed soft in Asia following dovish remarks from Fed Governor Waller on Friday. Waller signalled openness to a rate cut, diverging from his colleagues’ cautious stance. This shifted market expectations: while the July FOMC is still seen as a hold (95% odds), the probability of a 25-bps cut in September rose to 61%, up from 55% a week ago, per CME FedWatch data.

Yen, Aussie, Sterling gain; Gold extends rebound

In the FX space, the Japanese yen led gains (0.4%) during the Asian session, followed by the Australian dollar and British pound (both up 0.2%). The softer US dollar supported Gold (XAU/USD), which posted a 0.6% intraday gain, marking its second consecutive daily advance, as it eyes the US$3,374 resistance level set on 14 July.

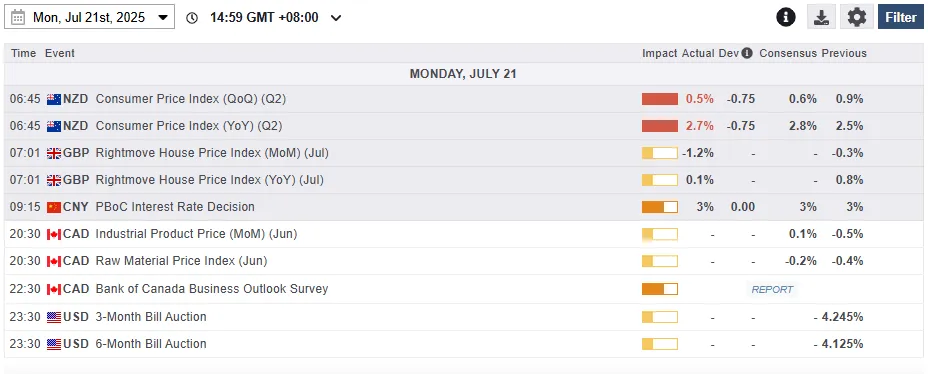

Economic data releases

Fig 1: Key data for today’s Asia mid-session (Source: MarketPulse)

Chart of the day – Gold (XAU/USD) looks poised for a potential minor bullish breakout

Fig 2: Gold (XAU/USD) minor trend as of 21 July 2025 (Source: TradingView)

The recent minor sideways range compression of Gold (XAU/USD) in place since 3 July has reached a potential tipping point for at least a minor breakout scenario.

Two key elements have increased the odds of a bullish breakout scenario. Firstly, Gold (XAU/USD) has retested the medium-term ascending trendline support in place since 31 December 2024 low for the third time on last Thursday, 21 July.

Secondly, in conjunction with the third retest on the medium-term ascending trendline support of Gold (XAU/USD), the hourly MACD trend indicator has traced a bullish divergence condition on 17 July, inched higher, and staged a MACD-Signal line bullish crossover in today’s Asia session at this time of writing.

Watch the US$3,328 short-term pivotal support, and a clearance above US$3,374 upside trigger level may see a minor bullish breakout unfolding for the next intermediate resistances to come in at US$3,400 and US$3,450 in the first step.

On the flip side, failure to hold at US$3,328 invalidates the bullish scenario for another round of minor choppy corrective decline sequence to expose the next intermediate supports at US$3,309, and US$3,293/3,282.

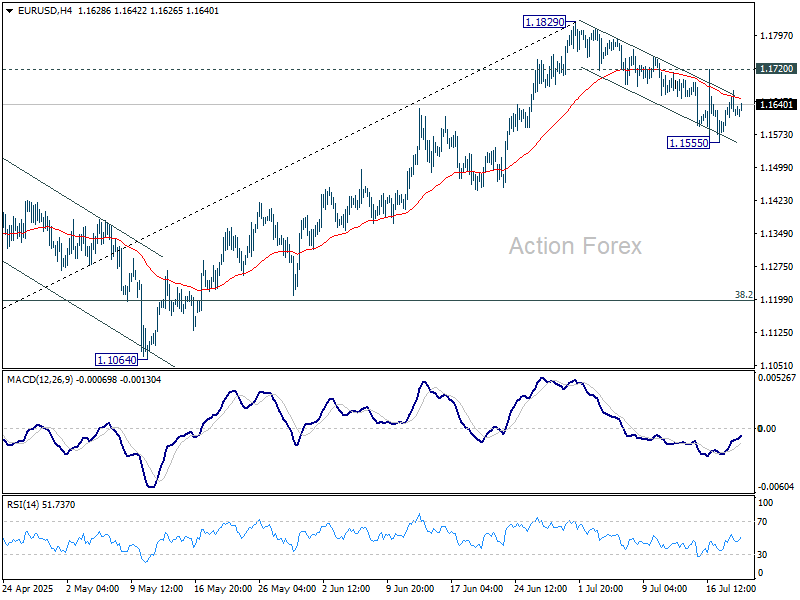

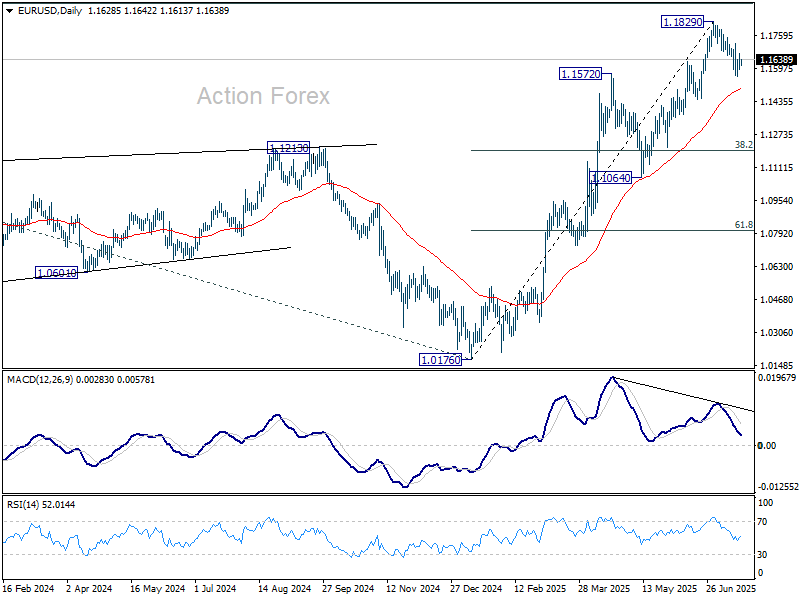

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1587; (P) 1.1630; (R1) 1.1667; More...

Intraday bias in EUR/USD remains neutral. Fall from 1.1829 might extend lower, and sustained trading below 55 D EMA (now at 1.1498) will argue that it's already correcting the rally from 1.0176, and target 38.2% retracement of 1.0176 to 1.1829 at 1.1198. On the upside, though, break of 1.1720 will bring retest of 1.1829 high.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.

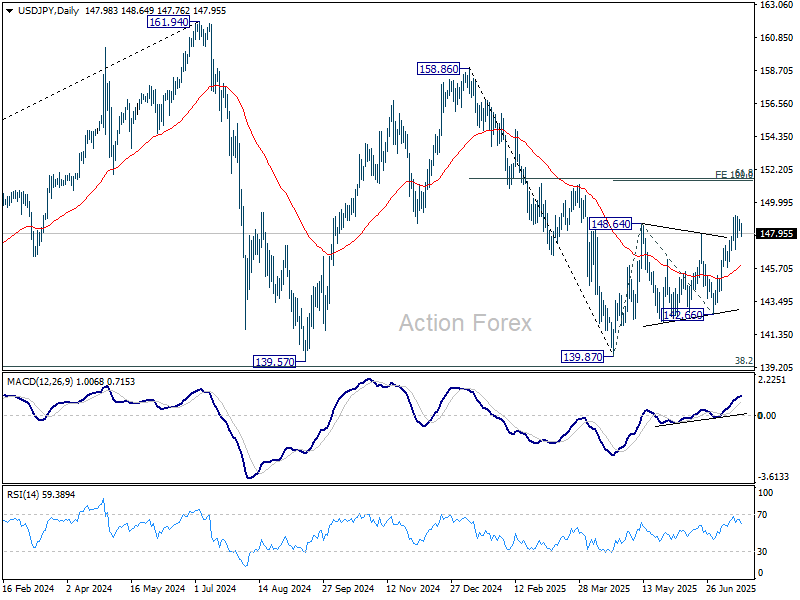

USD/JPY Daily Outlook

Daily Pivots: (S1) 148.39; (P) 148.64; (R1) 149.08; More...

Intraday bias in USD/JPY remains neutral for the moment, and more consolidations could be seen below 149.17. Further rally is expected as long as 55 D EMA (now at 145.86) holds. On the upside, break of 149.17 will target 100% projection of 139.87 to 148.64 from 142.66 at 151.43. That is close to 61.8% retracement of 158.86 to 139.87 at 151.22.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). There is no clear sign that the pattern has completed yet. But still, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

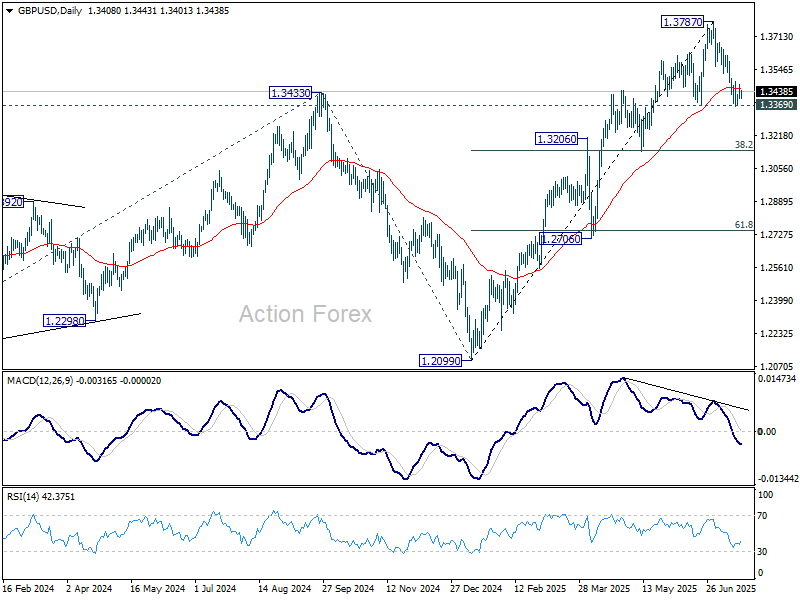

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3383; (P) 1.3429; (R1) 1.3455; More...

Intraday bias in GBP/USD stays neutral at this point. On the downside, firm break of 1.3363/9 will suggest that fall from 1.3787 short term top is already correcting the rise from 1.2099. Deeper decline should then be seen to 1.3138 cluster support (38.2% retracement of 1.2099 to 1.3787 at 1.3142). However, strong rebound from current level will retain near term bullishness. Break of 1.3561 support turned resistance will bring retest of 1.3787 high.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3017) holds, even in case of deep pullback.

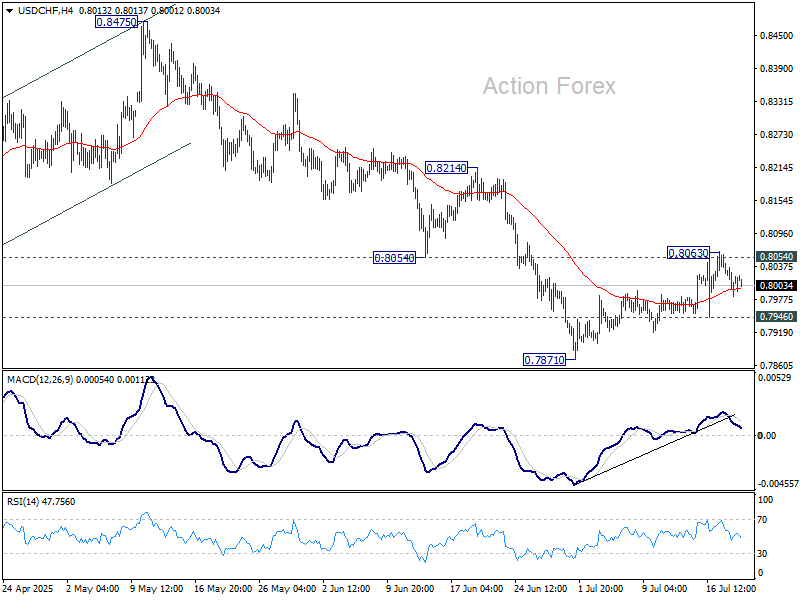

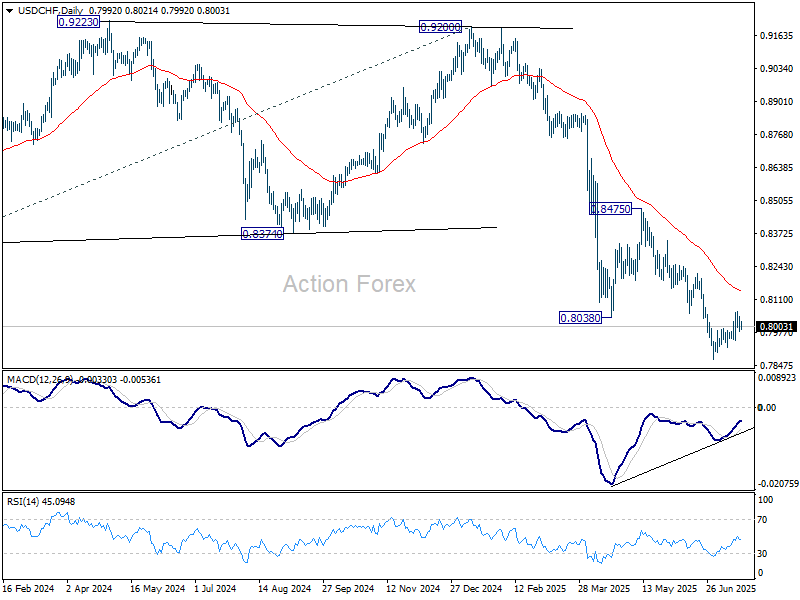

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7982; (P) 0.8020; (R1) 0.8054; More….

Intraday bias in USD/CHF remains neutral for the moment. On the downside, break of 0.7946 support will argue that correction from 0.7871 has completed, and bring retest of this low. Nevertheless, firm break of 0.8054/63 will bring stronger rebound to 55 D EMA (now at 0.8140).

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.

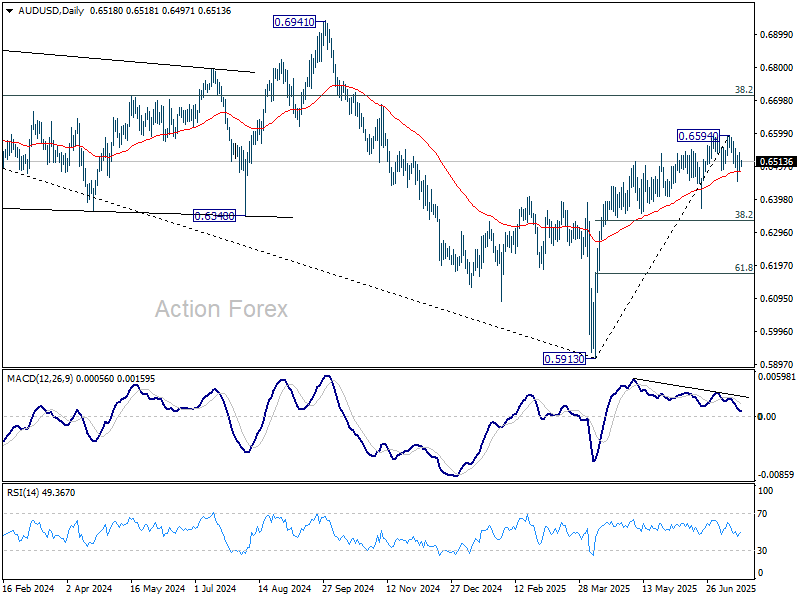

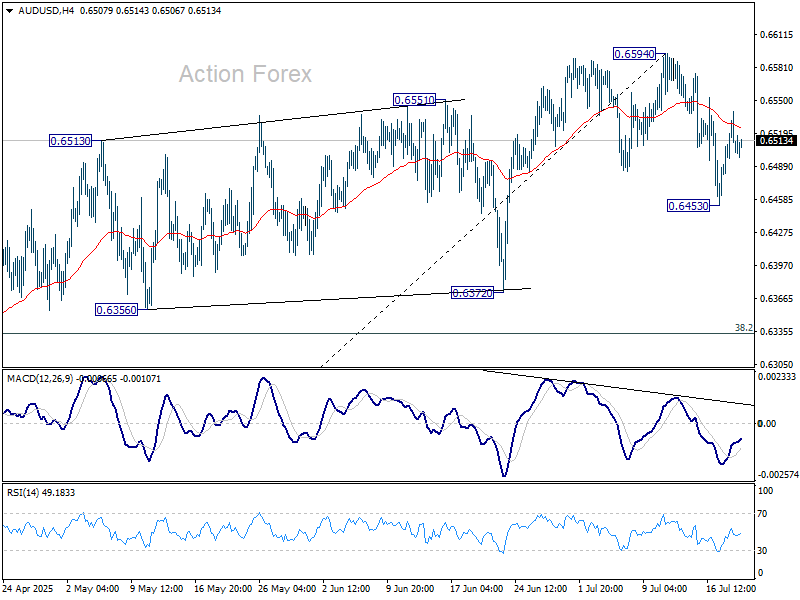

AUD/USD Daily Report

Daily Pivots: (S1) 0.6478; (P) 0.6509; (R1) 0.6539; More...

Intraday bias in AUD/USD remains neutral for the moment. Decline from 0.6594 could extends lower. Break of 0.6453 will target 38.2% retracement of 0.5913 to 0.6594 at 0.6334, as a correction to the whole rally from 0.5913. Risk will stay mildly on the downside for now as long as 0.6594 resistance holds, in case of stronger recovery.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. While stronger rally cannot be ruled out, outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, even in case of another fall through 0.5913, downside should be contained above 0.5506 (2020 low).