Sample Category Title

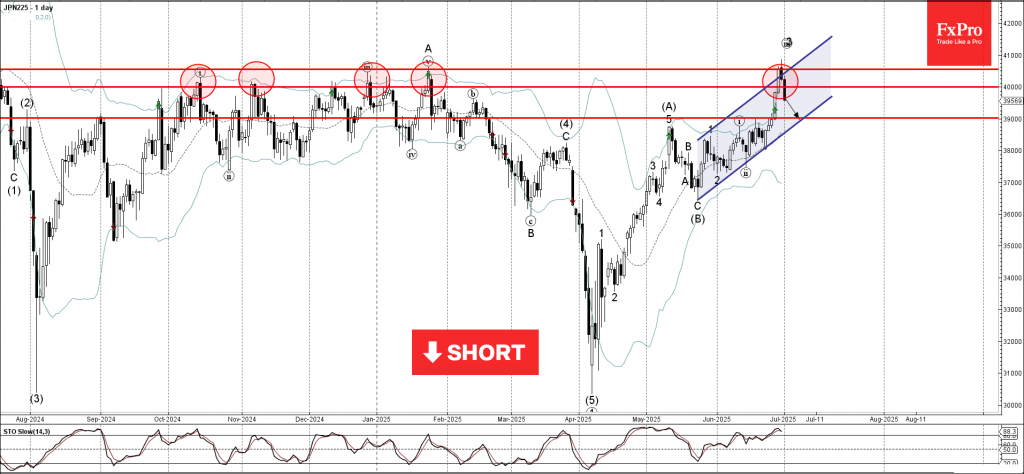

Nikkei 225 Wave Analysis

Nikkei 225: ⬇️ Sell

- Nikkei 225 reversed from resistance zone

- Likely to fall to support level 39000.00

Nikkei 225 index recently reversed down with the Evening Star from the resistance zone between the resistance levels 40000.00 and 40550.00 (former multi month high from January).

This resistance zone was strengthened by the upper daily Bollinger Band and by the resistance trendline of the daily up channel from May.

Given the strength of the aforementioned resistance zone and the overbought daily Stochastic, Nikkei 225 index can be expected to fall to the next support level 39000.00.

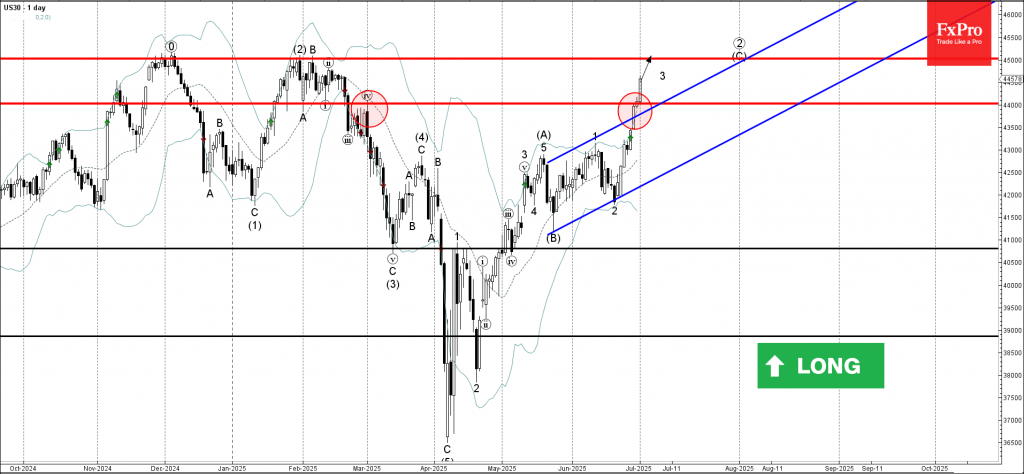

Dow Jones Wave Analysis

Dow Jones: ⬆️ Buy

- Dow Jones broke the resistance zone

- Likely to rise to resistance level 45000.00

Dow Jones index recently broke the resistance zone located at the intersection of the resistance level 44000.00 (former top of wave iv from March) and the resistance trendline of the daily up channel from May.

The breakout of this resistance zone accelerated the active impulse wave (3) – which is part of the multi-month upward ABC correction 2 from April.

Dow Jones index can be expected to rise to the next resistance level 45000.00 (target price for the completion of the active impulse wave (C)).

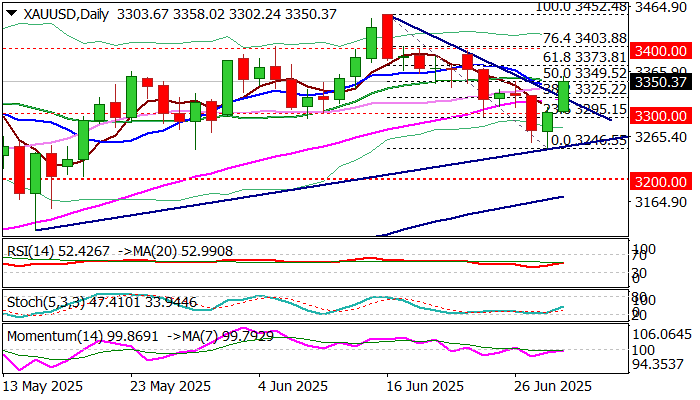

GOLD: Fresh Rally Provides Temporary Relief and Boosts Optimism

Recovery leg from $3246 (June 30 low) extends into second consecutive day and accelerated on Tuesday, recovering over 50% of the fall seen in past two weeks.

Weaker dollar on fresh tariff uncertainty as Trump’s July 9 deadline nears and his latest notification that there will be no further extension, lifted gold price.

Markets are also concerned about tax cut and spending bill, which President Trump want to be passed before July 4, add to gloomy outlook and contribute to fresh migration into safety.

Near term outlook has brightened after the recent downtrend was contained by top of daily Ichimoku cloud and subsequent bounce pushed the price away from dangerous zone below $3300, for now.

Daily close above broken Fibo level at $3325 (38.2% of $3452/$3246 bear-leg), also broken bear-trendline, is seen as minimum requirement to keep fresh bulls in play while close above cracked $3350 barrier (50% retracement / 20DMA)) would further strengthen near-term structure and shift focus towards $3373 (Fibo 61.8%).

Technical picture on daily chart is improving, although with warning signal from 14-d momentum which holds at the centreline, while overbought 4-h studies suggest that bulls may take a breather after strong acceleration today.

Consolidation or shallow correction should be contained above $3325 to keep near-term action biased higher.

Res: 3358; 3373; 3400; 3437

Sup: 3330; 3325; 3302; 3295

Preview of RBNZ: Time for a Cup of Tea

- We expect the RBNZ to leave the OCR unchanged at its July meeting.

- The RBNZ will likely retain an easing bias but stay noncommittal on when it might act on that bias.

- The RBNZ will likely note the uncomfortably high near-term inflation outlook and upweight this factor relative to more recent indicators of weaker economic momentum.

- This should point markets towards inflation and inflation expectations indicators when determining if a further cut will occur in August or sometime later.

RBNZ decision and communication.

The RBNZ will likely leave the OCR unchanged at its July meeting and take a wait-and-see attitude to the outlook for the OCR. While we expect the RBNZ to retain the easing bias it showed in its May Monetary Policy Statement communications, we don’t expect the RBNZ will give a strong guide on the timing on when it might cut the OCR further. Instead, we expect the RBNZ will give the market room to determine for itself, based on data released up until the August Monetary Policy Statement, whether a cut to 3% will happen in August, be delayed until later in the year, or be cancelled altogether.

The RBNZ will likely note that economic activity was stronger than expected in the first quarter of 2025, but that activity indicators since then have pointed to the slow down in economic momentum foreshadowed in their May forecasts. We doubt it will judge recent economic momentum as materially weaker than previously expected – but its likely they will point to some risk that such evidence might accumulate in coming months.

The RBNZ will also likely note that the near-term inflation outlook looks uncomfortably high. We think it will retain confidence that medium-term inflation will recede through 2026 – but will express uncertainty around that as well as the path of inflation expectations while headline inflation remains close to 3%.

The key in determining the timing of when (or if) the next 25bp rate cut occurs will be the relative weight the RBNZ places on the degree of concern about the near-term activity outlook versus the short-term inflation picture. We expect more weight will be placed on the inflation outlook given the single mandate the Monetary Policy Committee is working to.

A hawkish scenario would be one where the RBNZ said nothing about the potential for further easing. We don’t think the RBNZ will want to call time on the easing cycle just yet. But if the RBNZ were not to mention the potential for future easing at all, this would likely be interpreted as a hawkish signal by the market.

A dovish scenario would be one where the RBNZ plays down concern about the near-term inflation outlook and instead expresses comfort with the medium-term inflation outlook. In this scenario, the RBNZ would likely note the weaker short-term activity outlook and leave the impression that further policy easing is more likely than not at the August meeting provided that upcoming data meets expectations.

Recent data flow and impact

Key data that has accumulated since mid-May include:

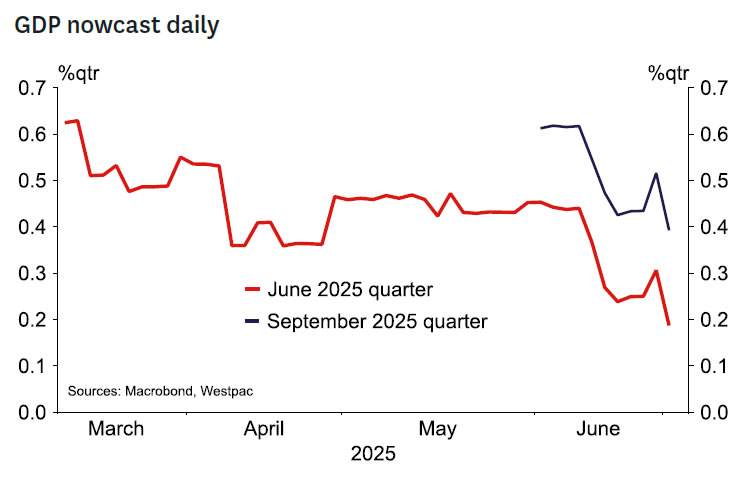

Stronger Q1 2025 GDP (0.8%q/q vs 0.4%q/q expected, albeit with a downward revision to growth in Q4) which implies stronger economic momentum and a slightly lower level of excess capacity than appreciated.

Weaker high frequency activity indicators for the May month (PMI’s, filled jobs, house prices and days to sell, consumer spending, business confidence). These look consistent with weaker activity in Q2 compared to Q1 and the RBNZ’s soft GDP growth expectations for Q2 and Q3 2025 (0.3% and 0.2% respectively). Nowcasts have accordingly been revised down in recent weeks.

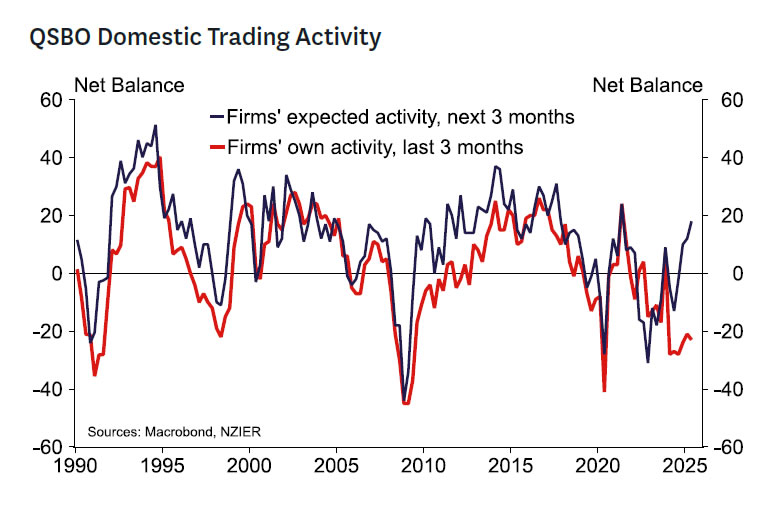

The still downbeat but also optimistic NZIER Quarterly Survey of Business Opinion. This survey showed firms perceive that they experienced weak activity in Q2 while optimism about the future improved from what was already relatively optimistic levels. It’s very much in the eye of the beholder which of these indicators best represents the underlying activity outlook – although recent experience suggests that the more positive forward-looking indicator has been closer to the mark.

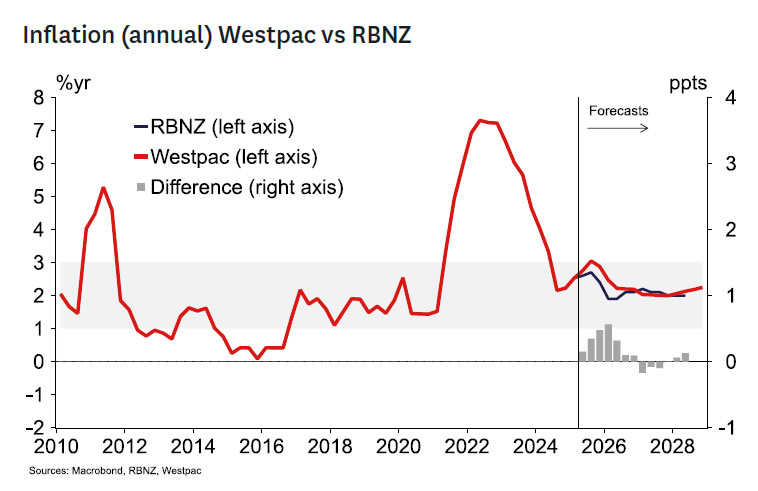

Stronger short-term inflation indicators. The monthly selected price indices suggest a more robust short-term inflation outlook than the RBNZ anticipated in May when they forecasted a 0.5%q/q and 2/6%y/y CPI outcome for the June quarter. Westpac has revised up its own CPI forecast from 0.4%q/q to 0.6%q/q since late May, especially reflecting strong food prices. It’s likely the RBNZ will have made a similar-sized adjustment. The outlook shows that headline inflation will rise to 3% in Q3 and be at 2.9% in Q4 2025. Inflation expectations continued to track higher in the June ANZ consumer survey.

Improved/less uncertain global growth and trade environment. High on the MPC’s mind in May was global uncertainty and the potential for weak global growth and a lower terms of trade. Since then, the outlook has improved somewhat. Progress has been made on trade deals such that the risks of very high and retaliatory tariffs look lower. Progress has been made in reducing risks to global security now Middle East tensions have reduced. Global equity markets are at record highs. Consensus forecasts for global growth have increased in the last 6 weeks – although these remain lower than forecasts seen before April.

Kelly’s take

A pause at this meeting is appropriate. There seems little risk of inflation moving very far into the bottom half of the target range in the next year or two. The global economic environment looks less threatening than might have been feared a month or two ago. And importantly, it’s not clear when inflation will peak and at what level.

There has been volatility in high frequency activity indicators, but also plenty of short-term news that might have driven sentiment in ways that may not prove to be long-lived.

Growth has been more solid than expected in the last couple of quarters and there are tangible signs of higher commodity prices and lower interest rates supporting the economy. Examples include strong agriculture sentiment and increased borrowing as well as rising demand for credit from investors in the housing market.

Strong commodity markets and the current level of interest rates will likely translate into trend to above-trend growth outcomes with time. This should be especially evident as global uncertainties continue to recede. The relatively high level of inflation limits the need to impart further stimulus at this time.

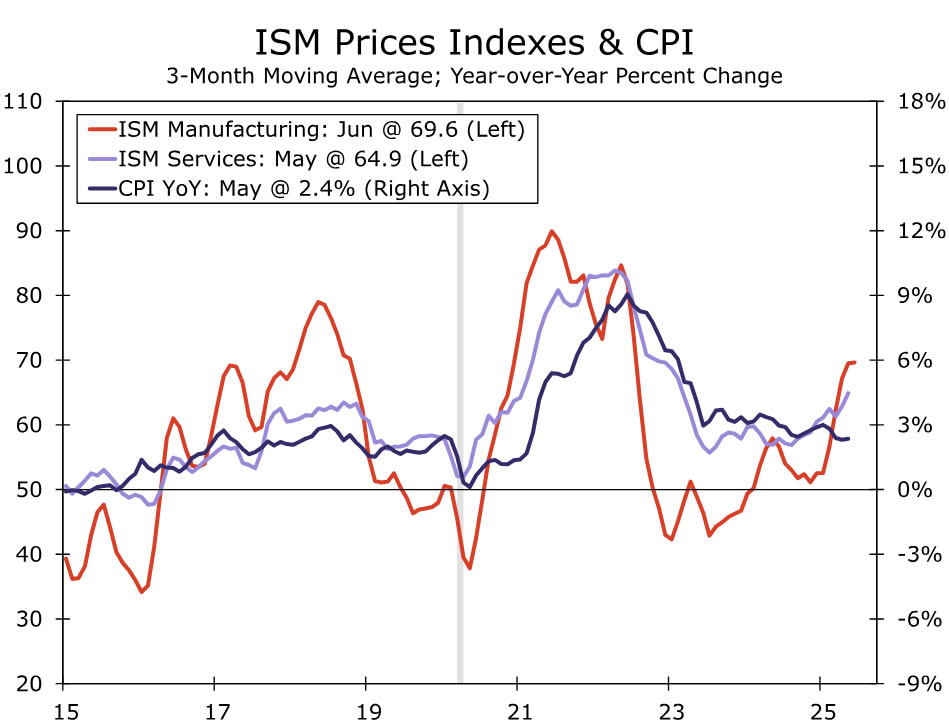

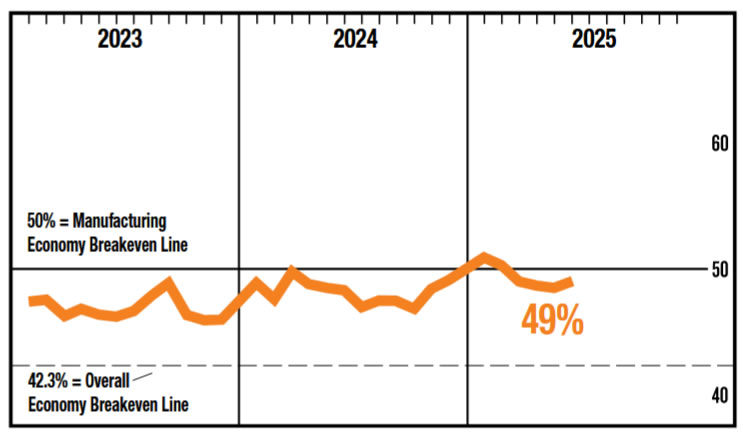

US: Widespread Tariff Concern Evident in June ISM Contraction

Summary

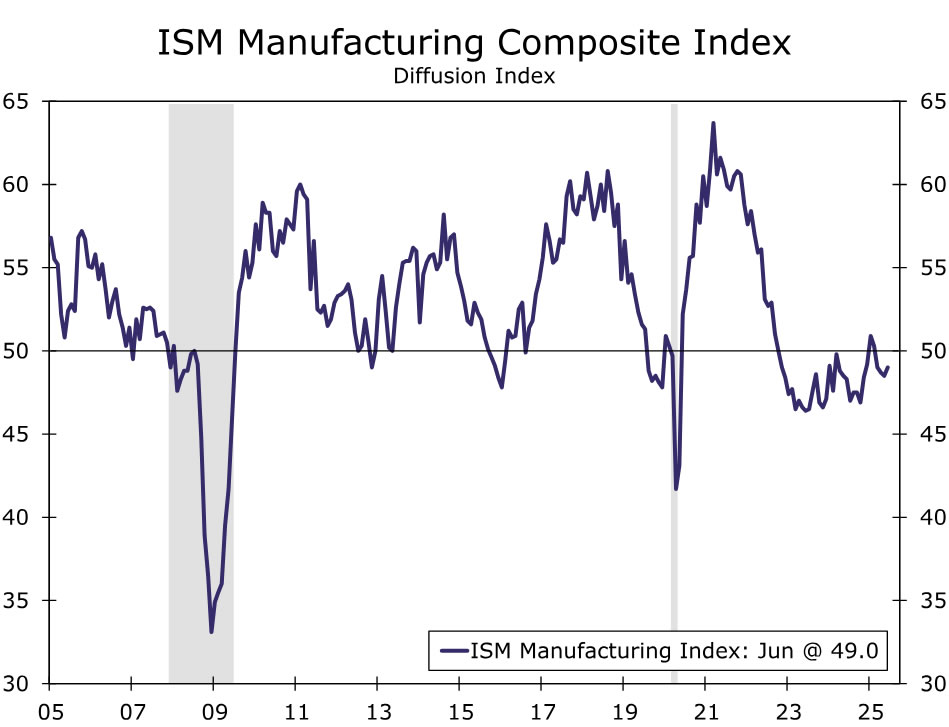

A rebound in production and a slower drawdown in inventories resulted in a more modest pace of contraction for ISM manufacturing in June. But worries about tariffs continue to crimp supply, leaving manufacturers fraught with trade-offs for holding inventory as pricing pressure builds.

Static in the Air

There is something in financial markets at the moment that is reminiscent of what you might experience just before a lightning strike. Equity markets testing record highs is analogous to the way the air becomes charged due to the accumulation of static electricity. Policymakers at the Fed say they are “well positioned to wait” before lowering rates, but that tingling sensation on your skin is the inevitable reaction to the relentless drumbeat of pressure from the White House to cut sooner. At issue of course is the degree to which tariffs will lead to higher inflation thereby justifying the Fed’s 'wait-and-see' approach or if the pass-through effect will continue to be as muted as it has been thus far, thereby clearing the path for lower rates.

Only hard inflation data confirming rising prices will be strong enough to ionize the air, but in this latest read on activity in the manufacturing sector, there is a case that supply chains remain disrupted, inventory management is fraught with trade-offs and pricing pressure is mounting.

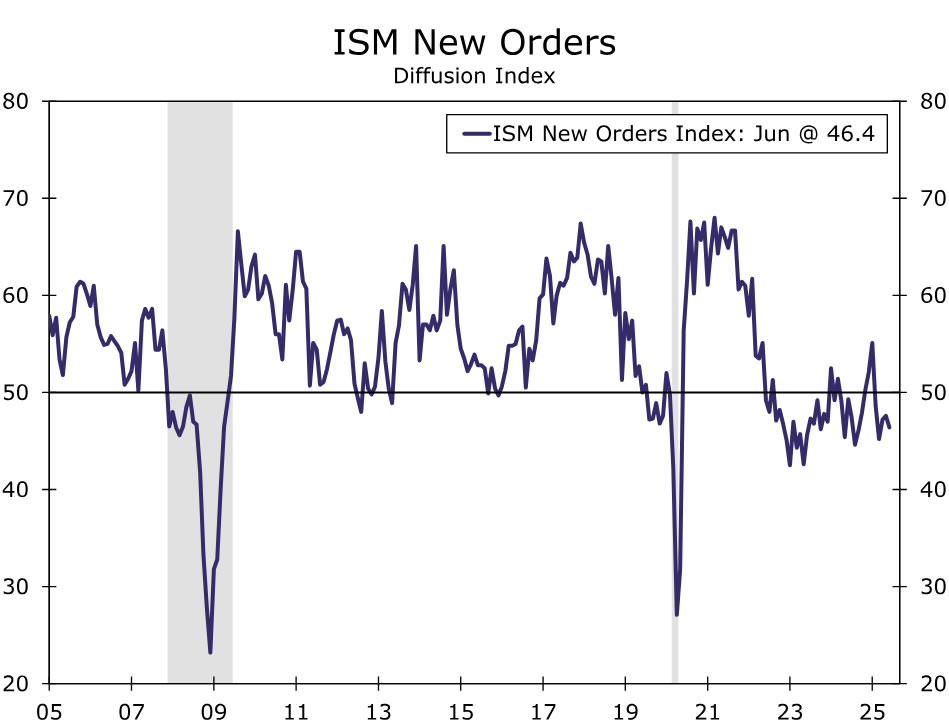

Tariffs are a top-of-mind worry across businesses with nine out of ten purchasing managers mentioning it in their responses. While tariffs are a universally held concern, it is clear that some industries are impacted more than others. In the machinery space, for example, one respondent said the "tariff mess has utterly stopped sales globally and domestically. Everyone is on pause. Orders have collapsed." The new orders component dropped to 46.4.

That drop in orders was offset last month with a near-five point pop in current production, which led the overall ISM manufacturing index up half a percent to 49.0 in June. The report still paints the picture of a manufacturing sector rife with challenges. We take the rise in production in June with a grain of salt as it came after a weaker trend the past few months and there was a near-even split between the number of industries reporting expansion versus contraction in current production. We expect the rise in production more so reflects a mere rebound after a couple of months of halted activity rather than the start of renewed growth. Ultimately, the only two things rising on trend in today's environment are wait times and prices; only supplier deliveries has an impact on the headline ISM.

Supplier deliveries, which measures the length of lead time for manufacturers to secure inputs, fell to 54.2 last month but remained in expansion and continued to be the largest counterweight to other components driving the composite index below 50. The measure is still consistent with longer wait times, a potential sign of building price pressure.

Inventories could be serving as a bulwark against the immediate pass-through of higher prices but those defenses are crumbling. The inventories index rose 2.5 points to 49.2; that means firms are still drawing down stockpiled inputs to sustain production, but the pace of that drawdown has slowed. When assessing their customer's inventories, firms suspect those stockpiles are also too low and being drawn upon more incrementally.

While the extent of tariff-induced inflation remains to be seen, the trend move higher in the ISM manufacturing prices paid index certainly suggests manufacturers are operating in a higher-cost environment. The prices paid index has now risen in nine of the past twelve months and remains the highest of any component above its prior six-month average. As the nearby chart shows, the overall consumer price index tends to track more closely with service-sector price pressure, but early price pressure tends to show up for manufacturers first.

Manufactures read on the labor market has been sour for some time. The employment component fell in June, keeping the index well-below the breakeven reading signaling a decrease in manufacturing jobs. We get the ISM services measure and the full nonfarm payroll report for June this Thursday, where we look for a slower pace of hiring. The stable moderation in the labor market has given the Fed cover to wait and assess the persistence of coming price pressure, but this 'stable' read on the labor market has begun to be called into question, increasing the importance around Thursday's data.

Fed’s Powell avoids rate commitment, highlights meeting-by-meeting approach

Fed Chair Jerome Powell refrained from signaling any clear path for rate policy during his appearance at the ECB’s Sintra forum, emphasizing that a July cut is neither guaranteed nor ruled out. “I really can’t say,” Powell responded when asked whether July is too soon for a move. “We are going meeting by meeting,” he added, avoiding any pre-commitments.

Powell’s remarks come as markets increasingly price in a September rate cut, with futures now assigning over 95% probability. However, the chair maintained that policy decisions will hinge on how key indicators — including inflation, labor market, and consumer behavior — evolve in the coming weeks. “I wouldn’t take any meeting off the table or put it directly on the table,” he said, reiterating that flexibility remains essential.

In broader comments, Powell emphasized the Fed’s core mandate, saying, “All I want — and all anybody at the Fed wants — is to deliver an economy that has price stability, maximum employment, financial stability.” He added that his focus remains on ensuring a healthy handoff to his eventual successor.

Sunset Market Commentary

Markets

It’s very unusual for ECB members to talk on the level of the single currency. It’s even more unusual that they do so in group. ECB vice governor de Guindos, Kazaks and Simkus used the sidelines of the ECB’s annual forum in Sintra to share their views. The vice governor started with the mandatory disclaimer that the ECB is monitoring it, but not targeting any concrete level. De Guindos nevertheless went as far as mentioning specific levels: “I think that EUR/USD 1.17, even 1.20 is not something. We can overlook it a little bit. Something beyond that would be much more complicated, but 1.20 is perfectly acceptable.” We’re not sure if it was the wisest move to point this out so specifically to markets/investors. Don’t poke the bear. Recall that higher EUR/USD forecasts together with a lower projected path for oil prices prompted significant (0.3 ppt) downward revisions to headline CPI this year (2%) and next (1.6%), enabling the final (our interpretation) policy rate cut to 2%. ECB Kazaks said that if the euro was to significantly appreciate further, it would weigh down on inflation and exports and could tilt the balance towards another cut. ECB Simkus wasn’t so worried about the actual level of the EUR/USD exchange rate, but did warn about the pace of recent appreciation. German Bundesbank Nagel offered some counterweight by downplaying the “historically average FX-level”. As we finish this report, the panel debate with ECB president Lagarde, Fed president Powell, BoE governor Bailey, BoJ Ueda and BoK governor Rhee is ongoing. Some (mostly non-market) moving excerpts: ECB Lagarde clearly indicated that she wouldn’t specifically comments on the level of the euro. BoE Governor Bailey repeated early signs of weakening of the UK economy and labour market though it didn’t filter through (in inflation) yet (GBP marginally underperforming); EUR/GBP 0.86). Fed chair Powell acknowledged that US policy rate would have been lower by now if it wasn’t for the tariff uncertainty. Of which he expects to see impact in Summer inflation readings. BoJ governor Ueda sees a slow increase in underlying inflation towards the 2% target (wage-consumption dynamics & tariff-combined) with food inflation (driven by administered prices) expected to subside by year-end. Today’s eco data included in line with consensus EMU June inflation numbers (0.3% M/M & 2% Y/Y; 2.3% for core) a near-consensus US manufacturing ISM (49 from 48.5 vs 48.8 expected) though with some worrying details (pace of job shedding and decline in new orders accelerating; sticky price pressure) and a stronger JOLTS report. US Treasuries were already under (selling) pressure in the run-up to the releases and currently lose more ground (up to 5 bps higher in bear flattening move). In the meantime, there’s still no white smoke coming from US Senate on their version of the One Big Beautigfil Bill Act.

News & Views

Consumer inflation expectations for the year ahead measured by the ECB’s monthly survey retreated from 3.1% to 2.8% in May. This compares to the perceived 3.1% for the past 12 months. The 3-year and 5-year ahead gauge slipped 0.1 ppt to 2.4% and remained unchanged at 2.1% respectively. Expectations for income growth in the coming year grew from 0.9% to 1% while those for spending growth eased to 3.5% from 3.7%. Consumers turned less negative on year ahead economic growth (-1.1% from -1.9%) as well as on the labour market (unemployment rate seen at 10.4% from 10.5%). Finally, respondents anticipate home prices to rise 3.2%, while seeing slightly lower mortgage rates for the 12 months ahead (4.4%). Households reporting a tightening (relative to those reporting an easing) in access to credit declined both over the previous and for the next 12 months.

The Czech manufacturing PMI in June improved from 48 to 50.2 in what is the first 50+ reading since May 2022. Growth, although modest, was supported by the sharpest increase in production since February 2022, an improvement in client demand (especially domestically) and a renewed rise in new orders. New export orders continued to decline amid competitive challenges and waning customer interest in key markets. Employment fell further as well amid cost-cutting efforts but at the slowest pace in the 33-month job shedding period. Work backlogs, however, rose again, moving into a three-month streak. Input costs continued to increase, though at a historically muted and slower pace than May. Output charges decreased marginally for the first time in four months with companies citing intense competitive pressures. Czech swap yields tumble between 3-8.3 bps, following core markets in a bull flattening move today. The Czech crown ignores the loss of interest rate support to hit another two-year high against the euro. EUR/CZK trades around 24.7.

US ISM manufacturing rises to 49.0, fourth month of contraction

US ISM Manufacturing PMI inched higher to 49.0 in June from 48.5, marking its fourth straight month in contraction territory but beating expectations of 48.8. While the slight improvement hints at stabilization, the broader picture remains soft. Notably, employment deteriorated further, falling to from 46.8 to 45.0, the fifth consecutive month of contraction. The prices paid index rose marginally from 69.4 to 69.7, indicating that cost pressures remain elevated, though the reading was still below market expectations of 70.2.

According to ISM, 46% of the manufacturing sector’s GDP contracted in June, a notable improvement from 57% in May. However, the share of GDP considered to be in “strong contraction” (PMI 45 or below) jumped to 25%, up sharply from 5% the prior month.

Despite the overall PMI suggesting 1.9% annualized GDP growth based on historical relationships, the underlying data show significant fragility in manufacturing employment and uneven recovery across subsectors.

Gold Surges Above $3,350 Again — Will Momentum Continue?

The question is a good one for the precious metal – It seems that markets are rebalancing flows towards Gold to start this session.

Canadian traders are off for Victoria Day and there is potential for overall less volume overall as this is typically a week that major market players decide to take off in North America, with also the 4th of July on Friday.

These lower volumes haven't translated to any sign of reversal for the US Dollar, and this has started to put its weight on Gold Bears – Prices rallied more than $100 in two sessions.

Positive sentiment and lackadaisical pushes to new highs led to more than 5% of correction from war highs, however yesterday's month-end rebalancing led to some decent buying in the metal – Buyers stepped in at the main daily upwards trendline that propelled the metal to new ATH several times, something to keep an eye on.

Maybe there is something that markets do not know yet, but one thing for sure is that the first day of July is not starting as Risk-On as the flows from last month, letting both Gold and Oil rally.

Before starting the Technical Analysis on Gold, quick reminder to not forget the US ISM PMIs at 10:00.

Gold Technical Analysis from Daily to 1H Charts

Gold Daily Chart

Gold Daily Chart, July 1, 2025 – Source: TradingView

Bulls really took advantage of the rising daily trendline identified in our last analysis of the precious metal – Also confirming further how important pyschological levels tend to be with prices showing sharp support at $3,250.

Prices just crosses above the 50-Day Moving average which had the potential to send the metal into a more corrective sequence – watch for headlines as markets may be preparing for a lower than expected NFP or more potentially, new tensions in the Middle East after a few attacks on Iranian soil were identified yesterday.

Gold 4H Chart

Gold 4H Chart, July 1, 2025 – Source: TradingView

Momentum is very strong, with the rebound on the immediate support zone around $3,250 leading to a Tight Bull Channel, where successive Bull Candles leave no space for sellers to have any control.

The pattern gets invalidated when a selling candle closes below the preceding bull candle – In the meantime, Gold bulls prevented a death cross between the 50 and 200 MA on the 4H Timeframe

Watch for reactions to overbought RSI, a consolidation near the highs is more bullish and a correction from here would entice a return of some more balance in flows.

Gold 1H Chart

Gold 1H Chart, July 1, 2025 – Source: TradingView

Prices broke out decently of the Hourly descending channel formed towards the end of last week, and the 1H Timeframe reconfirms how sellers haven't had a single chance in this two session rebound.

There is immediate resistance at $3,360, and way overbought momentum provides some chances for bears to step in.

As long as prices remain above the $3,300 Main Pivot, bulls remain in control

Any break below that pivot and further break below the Daily ascending trendline will give back the hand to the sellers.

Safe Trades!