Sample Category Title

ECB officials at Sintra keep slight dovish bias as easing cycle nears end

At the ECB’s annual forum in Sintra, policymakers reinforced that it's is nearing the end of its easing cycle, even though further rate cut cannot be ruled out.

Chief Economist Philip Lane emphasized that the “last cycle” of battling post-pandemic inflation is over, having brought price growth down from 10% to near the 2% target. Still, he clarified that being “done” with the previous cycle does not rule out additional moves if circumstances change, particularly as the eurozone faces lingering uncertainty from global trade tensions and weak growth.

Belgian central bank chief Pierre Wunsch echoed the sentiment, saying the “job is mostly done” on inflation but that risks are now tilted to the downside. Wunsch added that "“if we have to move more it probably will be to the downside, a further cut."

Latvian central banker Martins Kazaks added that any future moves would likely be small and designed as fine-tuning or “insurance cuts.” He cited Euro’s recent appreciation as a potential drag on inflation and exports, reinforcing the case for a cautious bias toward easing.

Vice President Luis de Guindos said that while the current EUR/USD exchange rate—hovering near 1.17—is not concerning, a rapid move beyond 1.20 would begin to pose challenges for inflation and competitiveness. "But 1.20 is perfectly acceptable."

Lithuania’s Gediminas Šimkus also leaned dovish, stating that any next move would “be down,” though he remained cautious about timing. He said September might be too early to decide. Simkus added: "I believe a move, if any, is more likely towards the end of the year."

Eurozone PMI manufacturing finalized at 49.5, divergences persist

Eurozone Manufacturing PMI was finalized at 49.5 in June, up slightly from 49.4 in May and marking the highest level in nearly three years. The data reflects gradual stabilization across the bloc’s industrial base, with output expanding for the fourth straight month and new orders showing signs of bottoming out. However, the headline figure remains below the 50-mark, signaling the sector is still technically in contraction.

Among individual economies, Ireland (53.7), Greece (53.1), Spain (51.4), and the Netherlands (51.2) led the pack with readings in expansion territory. In contrast, France (48.1), Italy (48.4), and Austria (47.0) continued to weigh on the region, posting multi-month lows. Germany, the bloc’s industrial engine, came in at 49.0—its best level in 34 months, but still shy of expansion.

Hamburg Commercial Bank’s Cyrus de la Rubia noted that longer delivery times and a stabilization in order books are early signs of a pickup in demand, despite ongoing macro risks from tariffs, the Middle East, and Ukraine. He added that if Germany returns to growth—helped by fiscal support from the new coalition—France, Italy, and Austria could follow, given their strong trade ties.

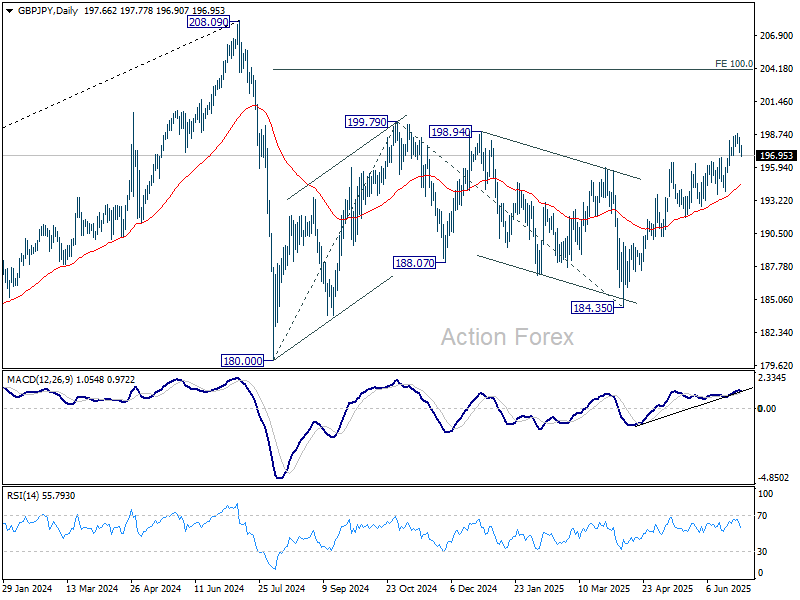

GBP/JPY Daily Outlook

Daily Pivots: (S1) 197.20; (P) 197.84; (R1) 198.46; More...

Intraday bias in GBP/JPY remains neutral, and some more consolidations would be seen first. Near term outlook will stay bullish as long as 193.99 support holds. Above 198.78 will resume the rise from 184.35 to 199.79 resistance. Break there will target 100% projection of 180.00 to 199.79 from 184.35 at 204.14.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 175.94 will bring deeper fall even still as a correction.

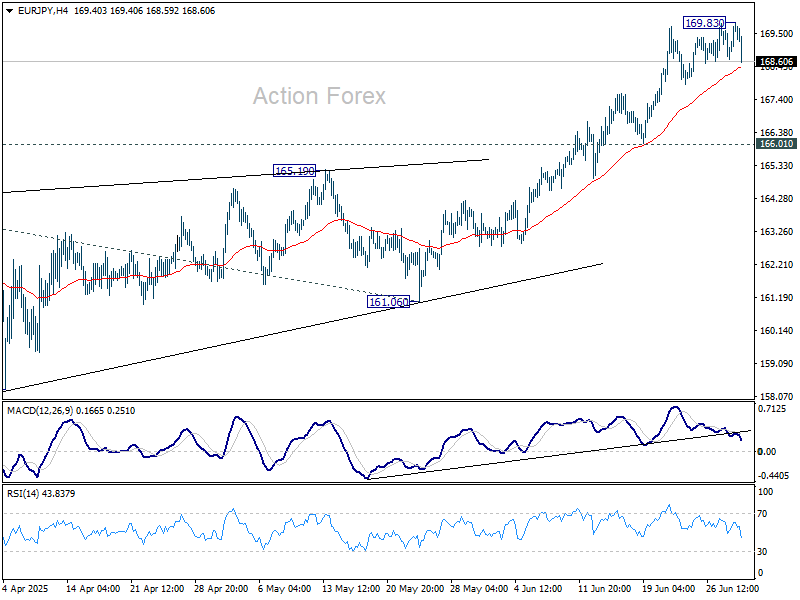

EUR/JPY Daily Outlook

Daily Pivots: (S1) 169.02; (P) 169.44; (R1) 170.19; More...

Intraday bias in EUR/JPY remains neutral first, and more consolidations could be seen. Downside should be contained well above 166.01 support to bring another rally. Above 169.83 will resume the rise from 154.77 to 100% projection of 154.77 to 164.16 from 161.06 at 170.45. Break there will target 138.2% projection at 174.03.

In the bigger picture, price actions from 175.41 are seen as correction to up trend from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

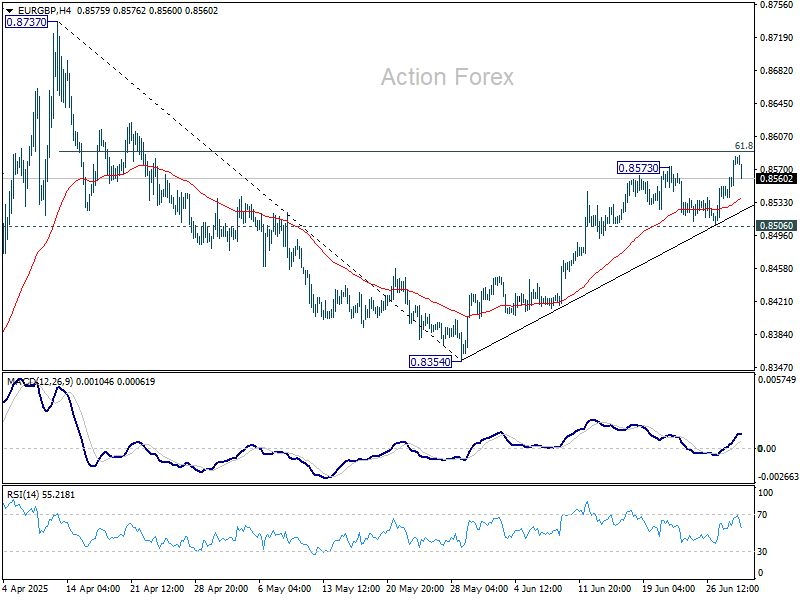

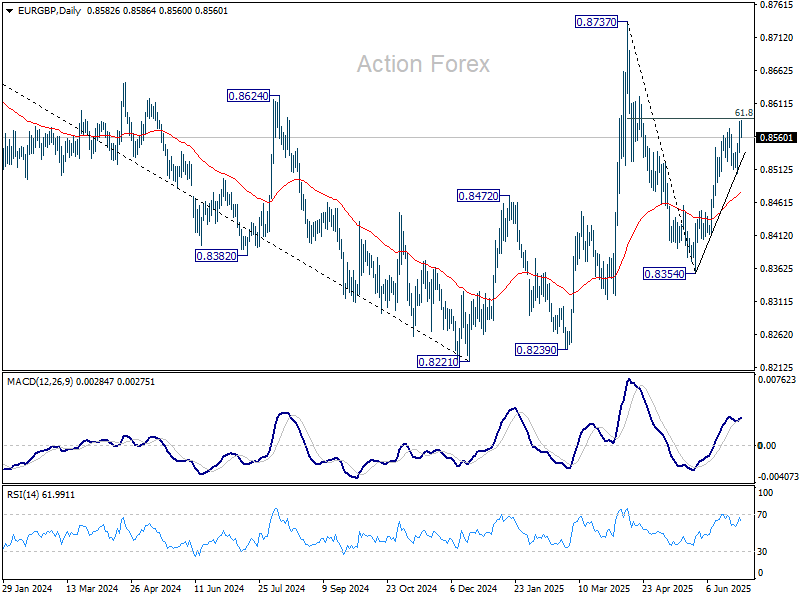

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8553; (P) 0.8570; (R1) 0.8600; More...

Intraday bias in EUR/GBP is back on the upside with breach of 0.8573 temporary top. Sustained trading above 61.8% retracement of 0.8737 to 0.8354 at 0.8591 will extend the rally from 0.8354 to 0.8737 high. However, firm break of 0.8506 support will suggest rejection by 0.8591, and turn bias back to the downside instead.

In the bigger picture, price actions from 0.8221 medium term bottom are seen as forming a corrective pattern to the down trend from 0.9267 (2022 high). Nevertheless, there is no clear momentum to break through 0.8201 key support (2022 low) yet. Hence, range trading is expected between 0.8221/8737 for now.

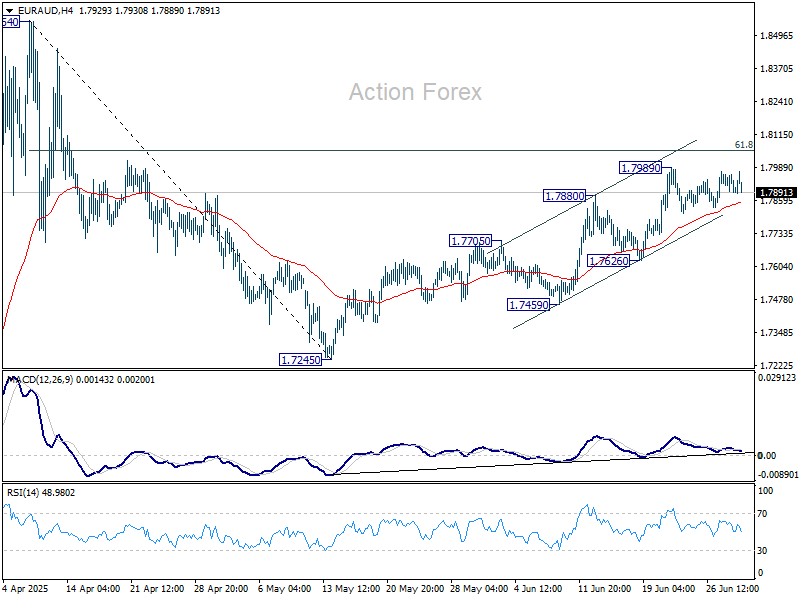

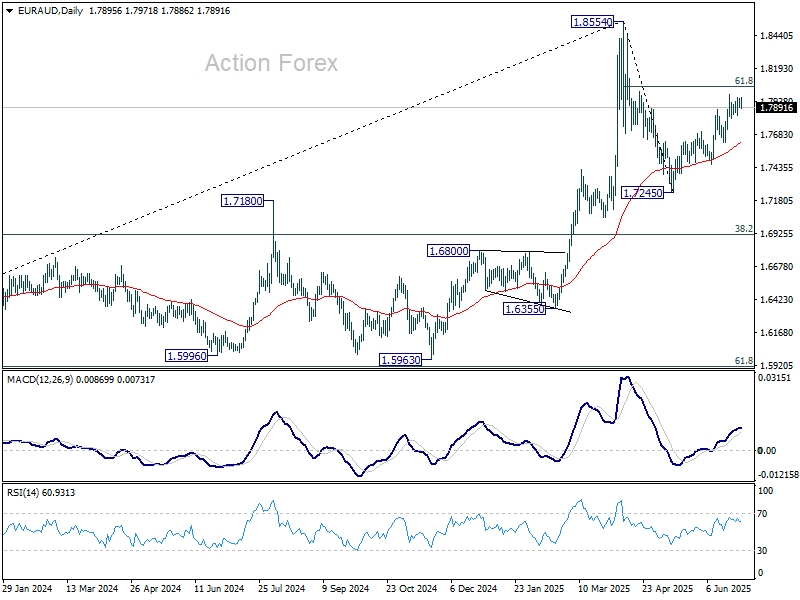

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7881; (P) 1.7923; (R1) 1.7952; More...

EUR/AUD is staying in consolidation below 1.7989 and intraday bias stays neutral. Further rally is expected as long as 1.7626 support holds. Above 1.7989 will target 61.8% retracement of 1.8554 to 1.7245 at 1.8054. Sustained break there will pave the way to 1.8554.

In the bigger picture, price actions from 1.8554 medium term are seen as a corrective pattern. While deeper pullback might be seen, downside should be contained by 38.2% retracement of 1.4281 (2022 low) to 1.8554 at 1.6922 to bring rebound. Up trend from 1.4281 is expected to resume at a later stage.

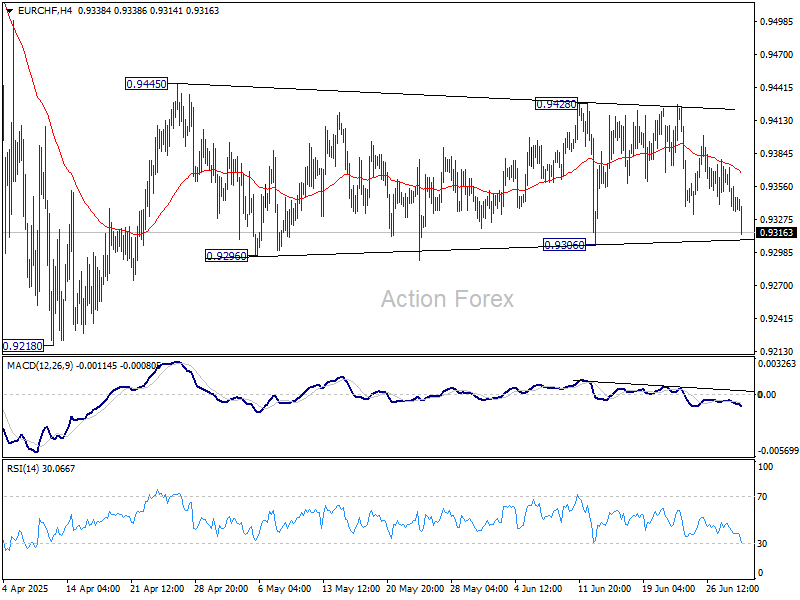

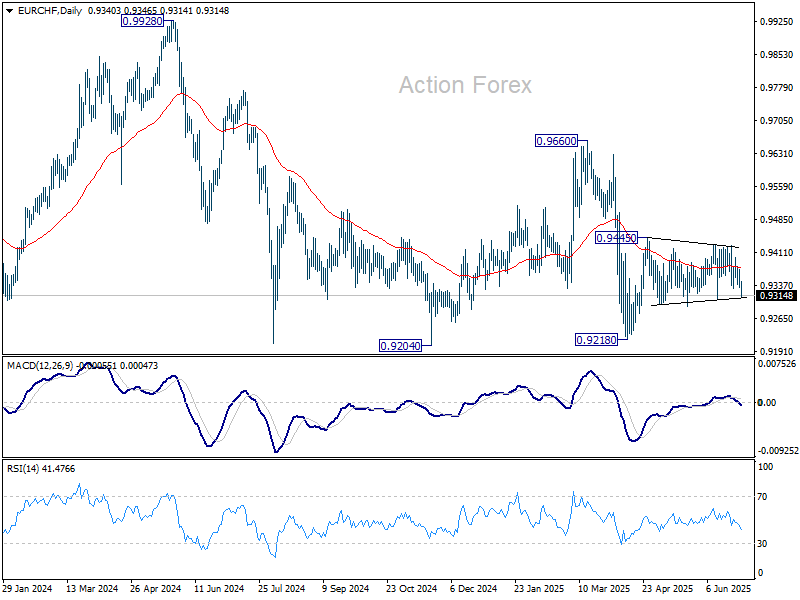

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9330; (P) 0.9353; (R1) 0.9371; More....

EUR/CHF is still staying in range of 0.9306/9428 and intraday bias stays neutral. Further rally is mildly in favor as long as 0.9306 support holds. On the upside, break of 0.9428/45 resistance zone will resume the rebound from 0.9218. On the downside, break of 0.9306 will bring retest of 0.9218 low instead.

In the bigger picture, while downside momentum has been diminishing as seen in W MACD, there is no sign of bottoming yet. EUR/CHF is still staying below 55 W EMA and well inside long term falling channel. Outlook will stay bearish as long as 0.9660 resistance holds. Break of 0.9204 (2024 low) will confirm resumption of down trend from 1.2004 (2018 high).

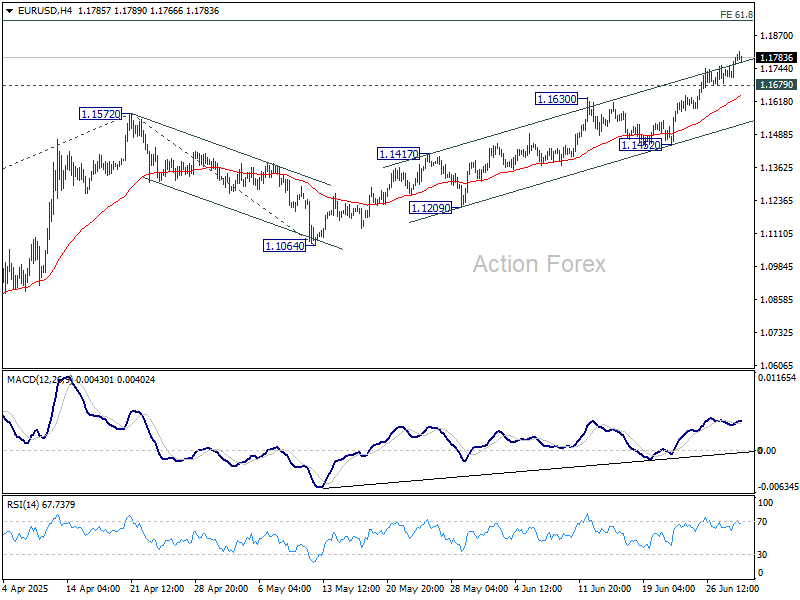

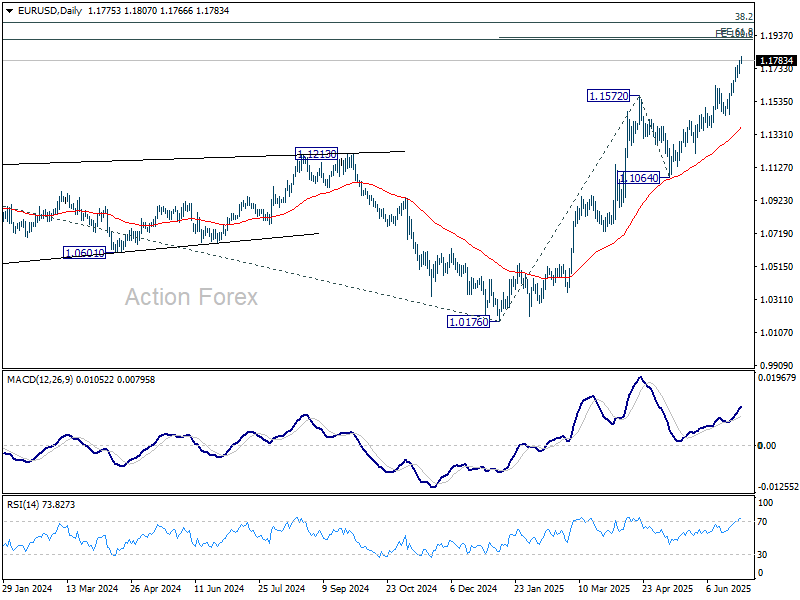

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1735; (P) 1.1761; (R1) 1.1815; More...

EUR/USD's rally continues today and intraday bias stays on the upside. Current rise should target 61.8% projection of 1.0176 to 1.1572 from 1.1064 at 1.1927. On the downside, below 1.1679 minor support will turn intraday bias neutral and bring consolidations. But downside should be contained above 1.1452 support to bring another rally.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 1.1604 support holds.

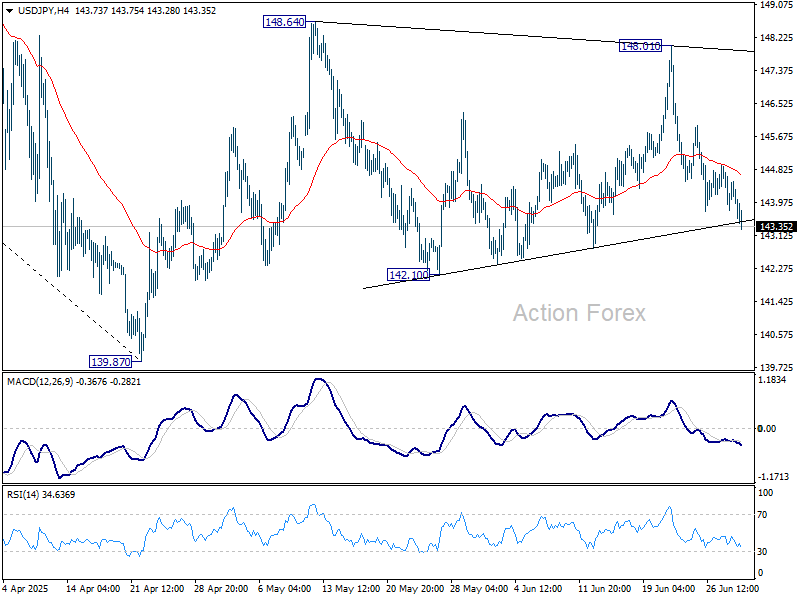

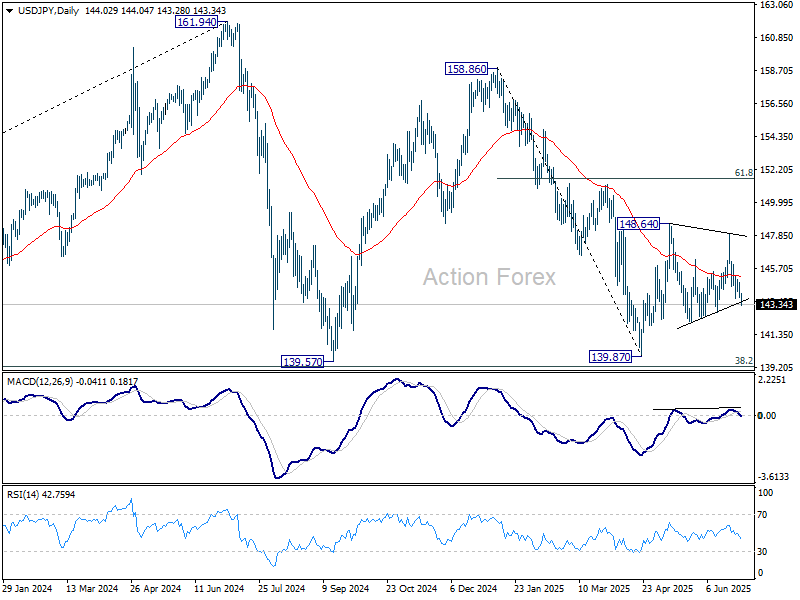

USD/JPY Daily Outlook

Daily Pivots: (S1) 143.62; (P) 144.19; (R1) 144.61; More...

No change in USD/JPY's outlook as range trading continues. Intraday bias remains neutral. On the upside, firm break of 148.01 resistance will resume the rise from 139.87 to 61.8% retracement of 158.86 to 139.87 at 151.22. However, break of 142.10 will bring deeper fall back to retest 139.87 low.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3693; (P) 1.3717; (R1) 1.3760; More...

Intraday bias in GBP/USD remains neutral and more consolidations could be seen below 1.3770 temporary top. Downside of retreat should be contained above 1.3369 support to bring another rally. Above 1.3770 will target 100% projection of 1.2099 to 1.3206 from 1.3138 at 1.3813.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2960) holds, even in case of deep pullback.