Sample Category Title

Fed’s Goolsbee dismisses stagflation risk, but warns on dual deterioration

Chicago Fed President Austan Goolsbee downplayed the risk of a 1970s-style stagflation scenario. He noted that with unemployment near 4% and inflation around 2.5% and falling, the current environment bears little resemblance to the high-inflation, high-unemployment era.

Speaking overnight, Goolsbee emphasized that today’s economic fundamentals are far stronger, with inflation far below double digits and labor markets still tight.

However, he cautioned that simultaneous deterioration in both inflation and employment remains possible. “There's definitely the possibility of both things getting worse at the same time,” he said. Goolsbee framed the outlook in terms of evaluating how large and lasting each side’s deviation might be—whether shocks are temporary or structural.

Final Countdown: Trade Peace or Market Panic on July 9?

Global markets are counting down to the July 8 and 9 deadlines set by the Trump administration. By these dates, countries must finalize trade deals with the U.S. — or face a sharp rise in tariffs. What happens could either bring relief to investors or reignite fears of a global trade war.

The trigger came on April 2, when President Trump announced sweeping new tariffs under his "America First" trade plan: a 10% base tariff on most imports, with the threat of much higher country-specific rates of up to 50%. At the same time, the administration paused enforcement for 90 days, giving countries until early July to negotiate individual exemptions.

Markets reacted swiftly:

- Stock prices tumbled as fears of a trade war grew

- Gold surged as investors sought safety

- The U.S. dollar weakened, reflecting doubts about long-term economic strength

- Volatility spiked, and investor confidence took a hit

Now, with the grace period ending on July 8 for most countries and July 9 for the European Union and others, global markets are once again on edge. Will new trade deals be reached? Or will tariffs snap back and disrupt global supply chains?

Let’s break down what’s happening, what to watch, and what the possible outcomes could mean for the markets.

Who Has Made a Deal (and Who’s Nearly There)?

Only a few countries have officially secured agreements so far:

- United Kingdom: Signed a partial trade deal covering cars, metals, beef, and ethanol. It’s not complete yet, but it’s the most advanced.

- China: Reached an agreement to ease tensions. China promised to speed up rare earth exports, and the U.S. scaled back some restrictions. But this is more of a truce than a full peace deal.

- Taiwan & Indonesia: Nearing deals.

- Vietnam & South Korea: Optimism is growing, but nothing signed yet.

Who Is Still at Risk?

Several key players are still negotiating and face the threat of higher tariffs if talks break down:

- European Union: Talks are tense. Some countries want a quick deal, others (like France) are pushing back. Car and steel tariffs are big sticking points.

- India: Progress has been made on energy and some agriculture, but India resists U.S. pressure on genetically modified crops and dairy.

- Japan: Wants a broad agreement but hasn’t agreed to U.S. demands on car tariffs.

- Canada: Talks have collapsed over a digital tax. Tariffs are expected if nothing changes.

- Others: Dozens of smaller nations — including Thailand, Mexico, and Algeria — are still in talks, and many face automatic tariff increases on July 9 if no deal is done.

President Trump has warned that countries without deals will be "sorted into proper buckets," but also said the U.S. "can do whatever we want" — leaving the door open for last-minute changes or extensions.

What the Market Is Expecting

Interestingly, despite all this tension, the stock market has not panicked. In fact, U.S. stocks have fully recovered all their losses from earlier this year and moved sharply higher in the past week. This tells us something important: Markets are expecting that most countries will eventually reach some kind of deal, or at least avoid the worst-case outcome of a full trade war. Here’s why:

- The China deal is done, and that was the biggest risk. With U.S.–China trade tension eased, the worst fears are off the table.

- Trump favors a strong stock market, especially ahead of the election. He’s made progress in improving the U.S. trade position already, and most signs suggest he doesn’t want to trigger a market crash now.

- A large sell-off seems unlikely, even though it’s still possible — Trump remains unpredictable, and markets know it.

- The market focus has started to shift toward U.S. interest rate cuts later this year. With inflation easing and the Fed signaling flexibility, traders are now watching rates more than tariffs.

- Volatility has been quiet for the past week, but that could change quickly as the deadline approaches and Trump begins pressuring countries to finalize deals.

The most likely outcome, based on current price action, is a continued relief rally, even if not every country reaches a full agreement. But traders should still be prepared for surprises.

What Could Happen? (And How Markets May React)

Here are four possible scenarios based on how the deadline plays out:

🟢 Scenario 1: Trade Peace (Deals or Extensions)

Most countries reach partial deals or get more time. The current 10% tariffs stay, but no big new penalties.

Potential Market Reaction:

- Stock markets rally

- Confidence improves

- Gold falls or stabilizes

- Bitcoin and crude oil rise

- USD strengthens

🟡 Scenario 2: Mixed Results (Some Deals, Some Tariffs)

The U.S. signs deals with a few countries but punishes others.

Potential Market Reaction:

- Winners and losers split across countries and industries

- Stocks move more erratically

- Volatility is high as traders try to understand the implications

🔴 Scenario 3: Market Panic (Tariffs on Many Countries)

The U.S. moves forward with high tariffs on multiple nations. No widespread deals.

Potential Market Reaction:

- Global stock sell-off

- Crude oil falls (on fears of weaker demand)

- USD continues to weaken

- Gold and JPY rise as safe havens

- High volatility returns

🔵 Scenario 4: Last-Minute Miracle (Full Breakthrough)

The U.S. unexpectedly reaches broad agreements with major partners.

Potential Market Reaction:

- Strong global rally

- Risk-on sentiment takes over

- Emerging market currencies jump

- Bitcoin rises, gold fall

- USD rises strongly

What to Watch Next

We’re heading into one of the most important trading weeks of 2025, with the July 8–9 tariff deadlines just ahead. Markets are on edge, and the next few days could bring major moves — either a continued rally or a sharp reversal.

Here are the key things to keep an eye on:

- Headlines and tweets from President Trump and U.S. trade officials — last-minute announcements or comments can shift sentiment instantly.

- Which countries finalize deals — and which are left out — will determine sector and regional winners and losers.

- Volatility indicators like the VIX — a spike could signal panic or uncertainty taking hold.

Only the UK and China have firm agreements in place. Most countries are still negotiating. If talks collapse, tariffs will hit and markets may drop. But if deals are made or deadlines are extended, a relief rally could continue. Stay flexible. Stay informed. Stay alert. Whether it’s trade peace or market panic — markets are ready to move.

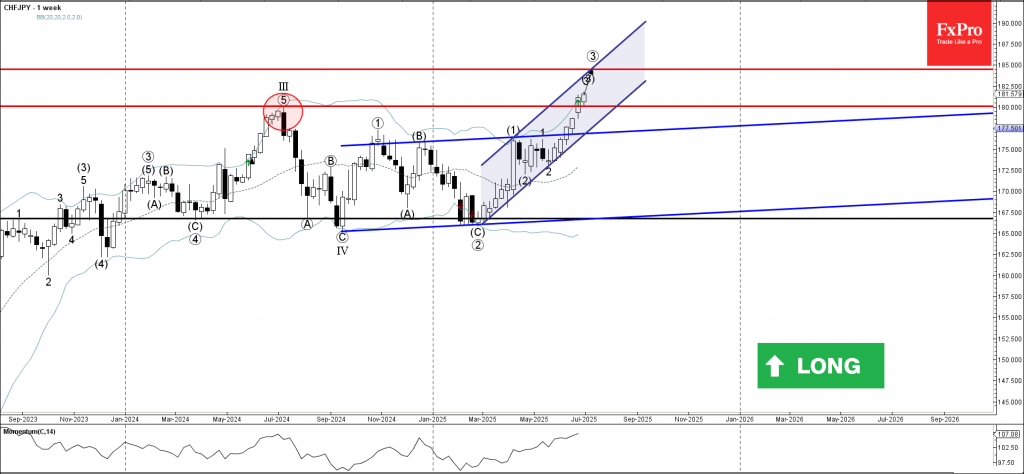

CHFJPY Wave Analysis

CHFJPY: ⬆️ Buy

- CHFJPY broke long-term resistance level 180.00

- Likely to rise to resistance level 185.00

CHFJPY currency pair continues to rise after the pair broke above the long-term resistance level 180.00 (former yearly high from the middle of last year).

The breakout of this resistance level should accelerate the active impulse wave (3) – which is moving inside the well-formed weekly up channel from March.

Given the clear weekly uptrend, CHFJPY currency pair can be expected to rise to the next resistance 185.00 (target price for the completion of the active impulse wave (3)).

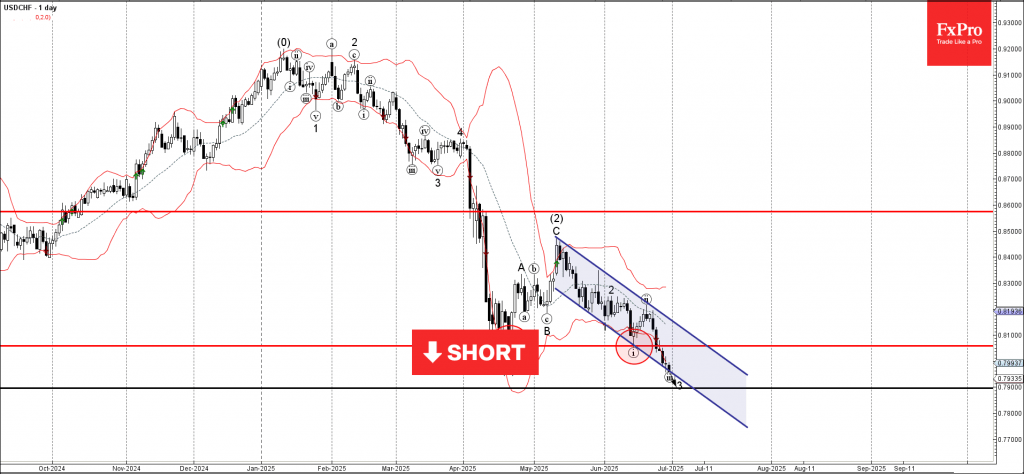

USDCHF Wave Analysis

USDCHF: ⬇️ Sell

- USDCHF falling inside a minor impulse wave

- Likely to fall to support level 0.7900

USDCHF currency pair is falling strongly inside the minor impulse wave 3, which recently broke the daily down channel from the start of May.

The breakout of this down channel follows the earlier breakout of the key support level 0.8055 (which stopped the previous impulse waves (1) and i).

Given the strong daily downtrend and the continuous outflows from US dollar or risk-on mood, USDCHF currency pair can be expected to fall to the next support level 0.7900, the target price for the completion of the active impulse wave 3.

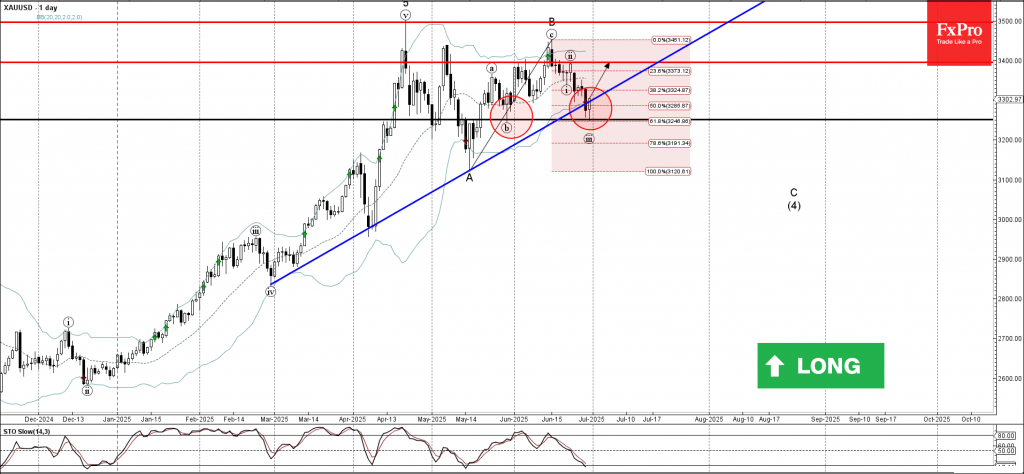

Gold Wave Analysis

Gold: ⬆️ Buy

- Gold reversed from support level 3250.00

- Likely to rise to resistance level 3400.00

Gold recently reversed up from the support level 3250.00 (which stopped wave (b) at the end of May, as can be seen from the daily Gold chart below) intersecting with the lower daily Bollinger Band and the 50% Fibonacci correction of the upward impulse from May.

The support level 3250.00 was further strengthened by the upward-sloping support trendline from February.

Given the clear daily uptrend, Gold can be expected to rise to the next resistance level 3400.00, which stopped the previous short-term correction ii.

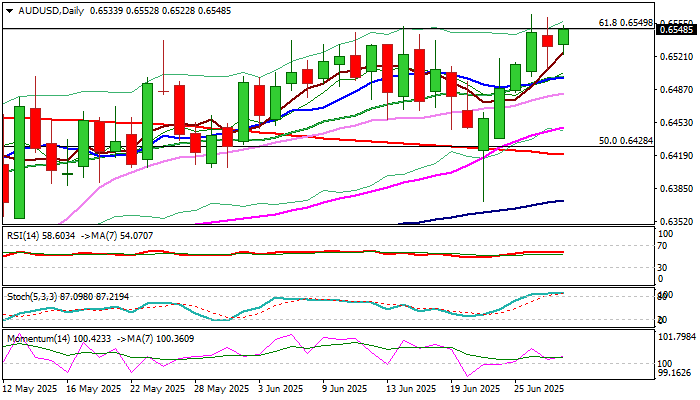

AUDUSD: Larger Bulls Take a Breather Under New 2025 Peak

AUDUSD trades within a narrow consolidation under new 2025 high (0.6563) for the second consecutive day and keeps firm bullish stance for now.

Technical picture remains firmly bullish on daily chart (the action is underpinned by thick ascending daily Ichimoku cloud), with additional positive signal from massive bullish engulfing on weekly chart and the pair being on track for the sixth consecutive monthly gain.

Bulls cracked important Fibo barrier at 0.6549 (61.8% of Sep 2024/Apr 2025, 0.6942/0.5914, downtrend) but were so far unable to register close above this level that would generate fresh bullish signal and expose targets at 0.6700 zone (Fibo 76.4% / 200WMA).

Overbought stochastic on daily chart probably keeps bulls on hold, with more quiet mode seen ahead of release of June report from US labor sector, which is likely to have significant contribution to Fed’s rate decisions in coming months.

Contained by converged 10/20DMA’s (0.6500) offer initial support which should ideally keep the downside protected, though deeper dips cannot be ruled out and should find firm ground above the top of daily cloud (0.6451) to keep bulls intact.

Caution on potential penetration of daily cloud which would expose next trigger at 0.6410 (Fibo 23.6% of 0.5914/0.6563 upleg / daily higher base).

Res: 0.6563; 0.6598; 0.6622; 0.6700

Sup: 0.6500; 0.6451; 0.6410; 0.6372

Market Wrap for the North American Session

Month-end flows notably influenced the session, leading to another instance of US Dollar underperformance. Equity markets, while ending the month on a positive note, experienced significant volatility into the close, as major participants leveraged the typically higher liquidity around monthly settlement prices for portfolio rebalancing.

Global indices are now closing above their early 2025 highs, completing what has been a volatile yet ultimately successful month of June.

Commodities observed a mixed performance today. Oil and other energy products saw declines, while Gold staged a notable rally throughout the session, closing just above the key $3,300 mark.

The broader macroeconomic landscape remained relatively calm. However, renewed tensions have emerged in Iran, and we will provide further analysis should the situation escalate.

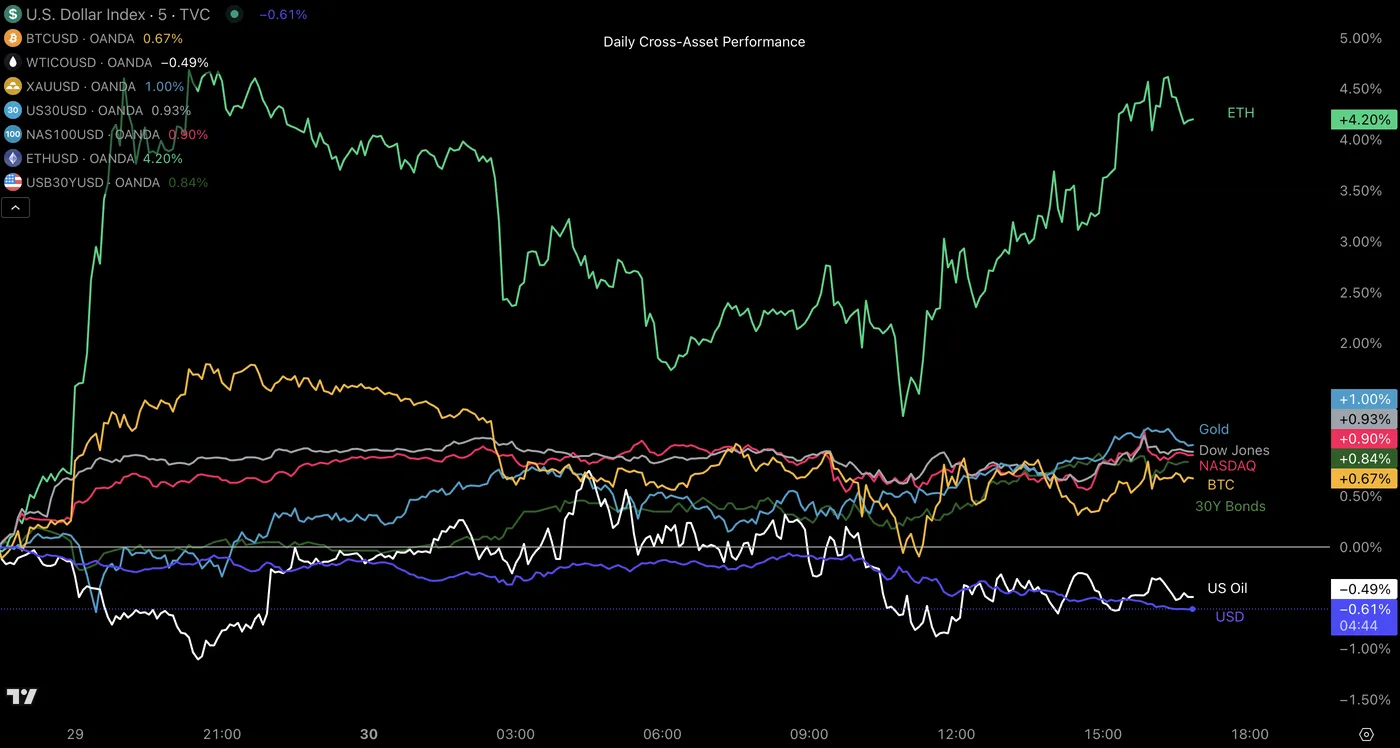

Daily Cross-Asset performance

Cross-Asset Daily Performance, June 30, 2025 – Source: TradingView

Ethereum is the standout performer on the session – Monitor the performance of the second biggest crypto in July as digital assets tend to perform well in the month starting tomorrow.

A picture of today's performance for major currencies

Currency Performance, June 30 – Source: OANDA Labs

The story repeats again in today's month-end flows – The US Dollar lagged again and Pacific currencies (NZD and AUD) are on top of majors.

Tomorrow's asset performance will be essential to monitor in order to see what markets are cooking for the upcoming month.

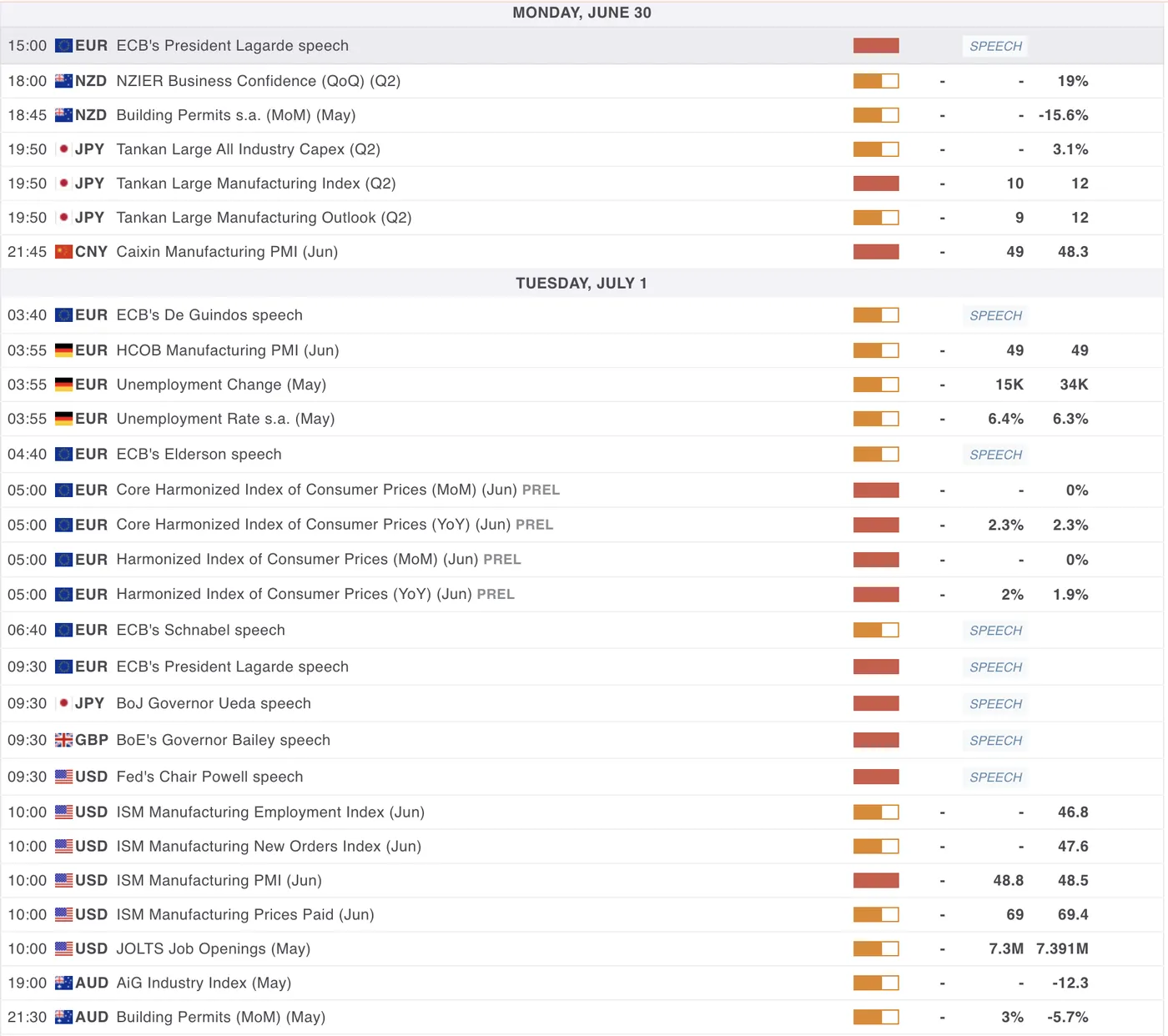

A look at Economic Data releasing in tonight and tomorrow's session

For all Market moving events, check the MarketPulse Economic Calendar

The overnight/tomorrow session will see more economic data releases, mostly with the US PMIs giving more clarity on the current economic picture for the US.

The ISM Manufacturing PMI is releasing tomorrow at 10:00 A.M. ET, expected at 48.8. The less market moving Chicago PMI came at a fairly big downward surprise with 40.3 vs 43 expected, markets may be preparing for some surprise in tomorrow's release.

Elsewhere, markets are awaiting for the Caixin PMI release from China tonight 21:45 (exp 49), which could be market moving particularly for APAC Currencies and Equity markets around the globe that have been performing quite dominantly in the past month.

For Euro traders, get ready for the Eurozone Inflation data release at 5:00 in the overnight session – We will have more clarity if the ECB has more work to do on their Monetary Policy or if the pause gets confirmed further.

Safe Trades!

Fed’s Bostic: Tariff effects may linger into 2026

Atlanta Fed President Raphael Bostic, speaking to CNBC, noted that “things are changing constantly,” complicating traditional forecasting methods. His comments come as markets monitor progress on President Trump’s new fiscal package, which passed a key Senate hurdle over the weekend.

From an inflation standpoint, Bostic said the Fed is watching how businesses and households adjust expectations and behaviors in response to current conditions. He saw “clear signs” that companies are planning to raise prices but cautioned that the scope and timing of those increases remain unclear.

Bostic also highlighted that many businesses now expect to delay tariff strategy decisions until 2026, suggesting the inflationary impact “could be a much more extended period than I think many expect."

Sunset Market Commentary

Markets

The European opening session of the week developed quiet and orderly. Trading settings which are unlikely to be repeated later this week given the avalanche of eco data and events approaching. The ECB published its first strategic review since 2021 (see news & views) as an appetizer in the build-up to the annual gathering in the Portuguese town of Sintra. It didn’t contain any groundbreaking views though. “Adapting to change: macroeconomic shifts and policy responses” is this year’s topic at the European Jackson Hole equivalent with ECB President Lagarde kicking off after European close with an introductory speech. A panel discussion with Lagarde, Fed Chair Powell, BoE Governor Bailey, BoJ governor Ueda (and BoK governor Rhee) is the forum’s headliner tomorrow afternoon. German harmonized inflation numbers showed price pressure unexpectedly slowing to 0.1% M/M and 2% Y/Y in June, making it a mixed national bag of numbers so far with upward surprises in Spain (0.6% M/M & 2.2% Y/Y) and France (0.4% M/M & 0.8% Y/Y) on Friday and in-line Italian data (0.2% M/M & 1.7% Y/Y) this morning. It makes for a likely dull, but welcome from a central bank point of view, outcome for tomorrow’s aggregate number (0.3% M/% & 2% Y/Y expected for headline; 2.3% Y/Y for core). Markets neglected the data with (EMU) inflation playing second fiddle as it hovers near the 2% price target will policy now well positioned to face an uncertain outlook. German yields trade up to 1.5 bps lower in a gentle steepening move. US Treasury yields slide 2 bps across the curve as focus turns to US Congress where Senators started a marathon of votes to finetune their version of President Trump’s Big Beautiful Bill after narrowly securing victory in a first procedural vote (51-49) on Saturday. A final Senate vote could come late today or early tomorrow. If it passes, the bill would then move back to the House. Despite today’s muted action in the Treasury market, we’d err on the side of new underperformance at the (very) long end of the curve later this week. The front end will be more interested in this week’s eco data (ISM’s and labour market update) and seems eager to exploit any sign of potential weakness. The combination of both won’t bode well for the dollar which remains stuck near multi-year lows (DXY 97.30; EUR/USD 1.1716; GBP/USD 1.3687).

News & Views

Polish inflation in June rose by 0.1% m/m to be up 4.1% on a yearly basis. The numbers printed broadly in line with expectations. Some details from Statistics Poland showed amongst others food and non-alcoholic beverage prices rising 0.1% m/m while energy prices (including electricity and gas) eased by 0.3% m/m. Transport fuels tumbled 1.3% in a monthly perspective. The June print means headline CPI is above the central bank’s upper bound of the 2.5% +/- 1 ppt tolerance range for a year now. Core inflation is due for release July 17 but has been trending lower in recent months to 3.3% in April, allowing the central bank (National Bank of Poland) to resume easing in May (-50 bps to 5.25%). The NBP made clear it would tread cautiously though. We expect one 25 bps move in Q3 followed by a cumulative 50 bps in cuts in the final quarter of this year (to 4.5%). Polish swap yields left the intraday lows after today’s release but remain up to 2.5 bps down for the day. The zloty trades stoic around EUR/PLN 4.24.

The ECB in its updated strategy reaffirmed its commitment to a symmetric 2% inflation target over the medium term. However, it now places greater emphasis on responding forcefully or persistently in case of sustained deviations in either direction. This is a departure of the 2020-2021 statement, which focused more on avoiding (too) low inflation. The ECB acknowledges that geopolitical and economic fragmentation, increasing use of AI, demographic change and the threat to environmental sustainability makes the inflation environment more uncertain and potentially more volatile. To account for this, the ECB will use scenario and sensitivity analyses in addition to the baseline. The central bank in pursuing its inflation goal keeps all monetary policy tools currently available in the toolkit, including negative rates, asset purchases and forward guidance. Their use, however, will be subject to a proportionality assessment to ensure flexibility and agility.