Sample Category Title

Franc Appreciates Despite Risk-On Mood

Last week saw investors put more risk on the table as Middle East tensions de-escalated following a fragile but so far holding US-brokered peace between Israel and Iran. There was also progress on the trade front: the US and China announced they’ve reached a trade agreement that will help restore the flow of Chinese rare earth metals to the US in exchange for trade concessions. VanEck’s Rare Earth and Strategic Metals ETF jumped nearly 4% and is consolidating gains just below its 200-day moving average (DMA) this morning. Japan and India decided to extend their negotiators’ stays in Washington, raising hopes that the talks are progressing and could lead to more good news in the coming days. Canada rolled back a digital services tax on US companies—imposed just a week earlier—to open the door for softer negotiations. Taiwan said the country made ‘constructive progress’ in the second round of talks, and the EU’s Ursula von der Leyen sounded optimistic that the bloc will find a way to sign a deal to avoid 50% tariffs on European exports to the US.

As such, investors are optimistic and willing to take more risk on their shoulders. The S&P 500 advanced to a fresh record high on Friday, the Nasdaq 100 hit a new record of its own, and the Dow Jones Industrial Average reached its highest levels since March. The Russell 2000—which had plunged nearly 30% after its November peak—has now recovered more than 60% of those losses and is testing its 200-DMA to the upside. US mid-cap stocks have also broken above their 200-DMA, with momentum improving on the back of falling yields and rising dovish Federal Reserve (Fed) bets, despite the Fed’s persistently cautious tone. Chair Powell repeated last week that the Fed is not willing to rush into rate cuts before having a clearer picture of where inflation is headed amid tariff uncertainty. But that went mostly unheard.

In Europe, the Stoxx 600 closed the week on a positive note, ending above both its 50- and 100-DMA, while the FTSE 100 finished just below the 8800-point mark. The Nikkei 225 rallied past the 40,000 level last week on trade optimism and started this week positively as well. However, stocks in China and Hong Kong are still not reacting to the encouraging trade news: both the CSI 300 and the Hang Seng Index are seeing limited demand this Monday, despite the trade truce and better-than-expected PMI data—even though manufacturing activity remained in contraction for a third straight reading.

Overall, market sentiment is upbeat. Investors are pulling back their gold bets, but the Swiss franc remains surprisingly strong and in demand. The USDCHF slipped below the 0.80 mark last Friday and is consolidating under this level —a threshold breached only on rare occasions: once during the European debt crisis in 2011, which forced the Swiss National Bank (SNB) to impose a floor of 1.20 on the EURCHF, and again in January 2015, when the SNB abruptly removed that floor. The fact that the franc's strength persists despite zero rates and broadly positive global market sentiment is a growing concern for the SNB. The franc appears stuck in an appreciation spiral that hurts Swiss exporters. Yet currency intervention is off the table for now, as Switzerland must tread carefully during ongoing trade negotiations with the US—already sensitive after being listed by the US as a potential currency manipulator. So for the time being, Switzerland may have to live with a stronger franc—at least while trade talks continue—and enjoy their discounted summer vacations. But at some point, the franc's strength will need to be addressed to help Swiss economy cope with the loss of competitiveness. The SMI index has been weighed down by tariff uncertainty and franc strength since the beginning of the year, and zero rates have done little to revive investor appetite.

Elsewhere, the US dollar continues to weaken despite trade progress. News that Donald Trump’s so-called ‘beautiful tax bill’ is now headed to the Senate—and, if passed, would add an estimated $3.3 billion to the US debt pile—is undermining appetite for both the dollar and US Treasuries. The 10-year yield briefly rebounded before approaching 4.20% last week.

European investors have increased their incentive to repatriate funds, and the euro is benefiting from sustained appetite for European assets. The EURUSD surpassed the 1.17 mark last week and is consolidating gains above it, despite stronger-than-expected inflation readings from France and Spain on Friday. More inflation data is due today from Germany and Italy, but the eurozone’s aggregate inflation data for June—due tomorrow—is expected to show a 2% print. That would hit the ECB’s target exactly and keep the door open for further support, if needed. The latter remains supportive for the euro.

Other than the European inflation figures and Trump’s tax bill—aimed to pass before the July 4th holiday—the market's attention this week will also turn to the latest US jobs report and a series of final PMI prints. In energy markets, oil prices are worth watching as they give back the Middle East–led gains. WTI crude is sitting on a key Fibonacci support near $65 per barrel—the level that separates the year-to-date bearish trend from a potential medium-term bullish consolidation. Expectations that OPEC may announce a plan to bring more oil to market at its July 6 meeting could give bears the upper hand into the weekend.

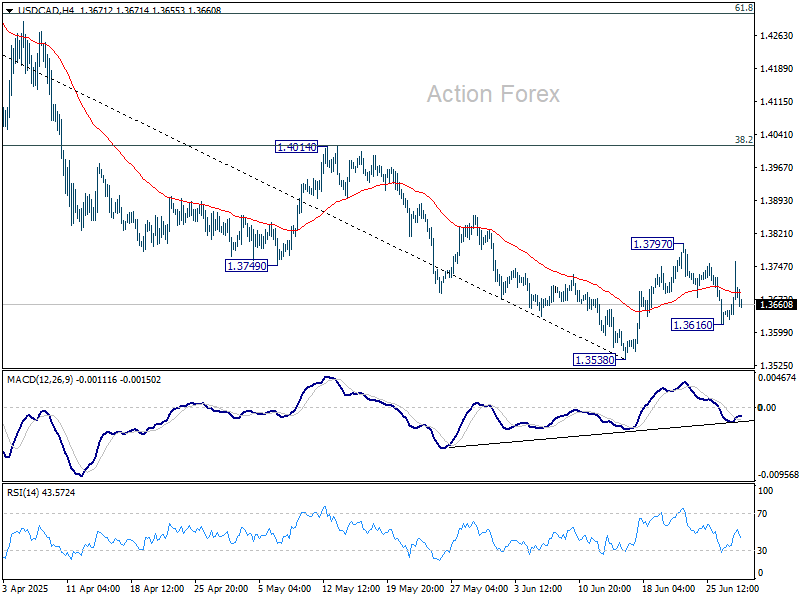

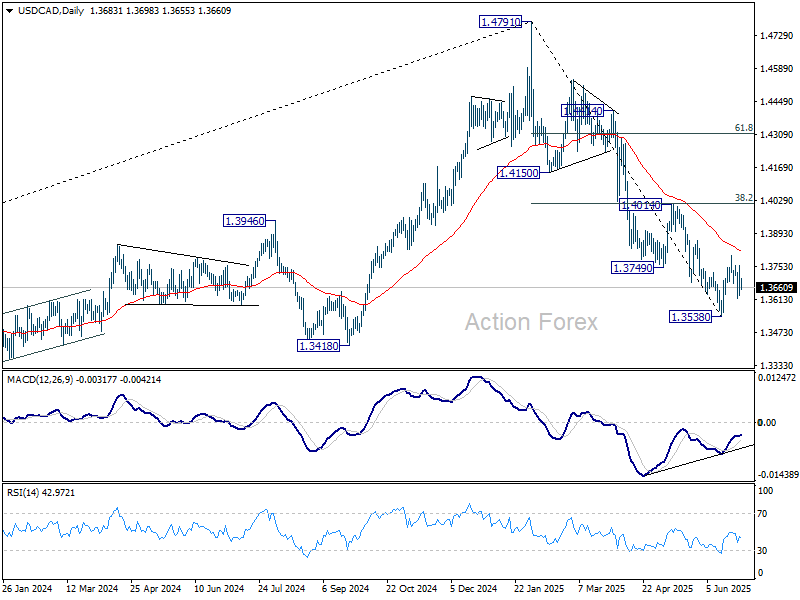

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3619; (P) 1.3689; (R1) 1.3750; More...

USD/CAD dips mildly today but stays in range of 1.3616/3797. Intraday bias remains neutral at this point. On the upside, break of 1.3797 will resume the rebound from 1.3538 short term bottom to 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 1.4017). Nevertheless, below 1.3616 will bring retest of 1.3538 low.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.

Canada Reverses Digital Tax to Save U.S. Trade Talks; Loonie Recovers Modestly

The forex market opened the week with low volatility and mixed Asian equities, but politically driven developments are keeping some G10 currencies in motion. Dollar is the weakest performer so far, with the Canadian Dollar also under pressure despite rebounding from weekend lows. Yen leads amid safe-haven inflows, while Kiwi and Aussie post modest gains.

Ottawa moved to de-escalate tensions with Washington by announcing a reversal of its digital services tax, originally set to take effect this week. The retroactive levy on American tech firms had prompted a sharp rebuke from US President Donald Trump, who vowed to halt all trade discussions with Canada. Reversing the tax was described by Canadian leadership as a strategic step to preserve the July 21 negotiation timeline and prevent retaliatory tariffs.

Canadian Prime Minister Mark Carney and Finance Minister Champagne framed the decision as a way to unlock progress on a new economic and security partnership. Markets welcomed the move, and the Loonie erased some of its losses, though sentiment remains fragile given the broader uncertainty heading into July’s tariff deadlines.

Meanwhile, the UK confirmed its partial trade agreement with the US has now come into force. British car exports will now face a reduced 10% tariff quota, and duties on aircraft parts have been removed. While the deal marks progress, the issue of steel and aluminum tariffs remains unresolved. UK officials reiterated their intent to push for 0% tariffs on core steel products under the agreed framework.

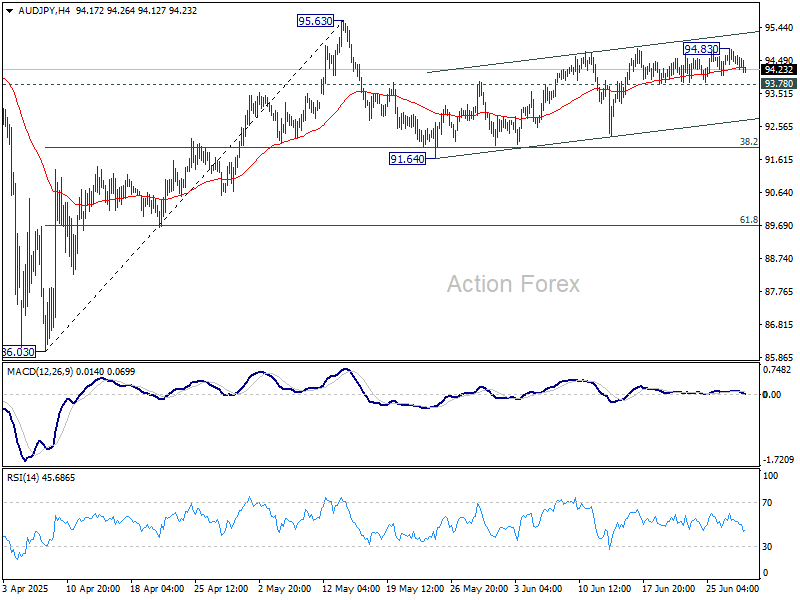

Technically, AUD/JPY's choppy recovery from 91.64 might be close to completion, with further lot of momentum as seen in 4H MACD. Firm break of 93.78 support will suggest that corrective pattern from 95.63 short term top has started. Deeper fall should the be seen back to 94.64 support next.

In Asia, at the time of writing, Nikkei is up 0.79%. Hong Kong HSI is down -0.38%. China Shanghai SSE is up 0.38%. Singapore Strait Times is up 0.03%. Japan 10-year JGB yield is flat at 1.437.

Japan’s industrial production rises 0.5% mom in May, far below expectation

Japan’s May industrial output came in far below expectations, rising just 0.5% mom versus the anticipated 3.4% mom growth. Though production improved in key sectors such as machinery and autos, five categories—led by non-auto transport equipment—recorded declines.

Shipments rose 2.2% mom, while inventories fell -1.9% mom, offering some positive signals, but not enough to shift the ministry’s cautious tone.

METI maintained its assessment that output “fluctuates indecisively”. A poll of manufacturers showed expectations for a muted 0.3% mom rise in June and a -0.7% mom drop in July.

China’s PMI manufacturing rises to 49.7, small firms lag

China’s official NBS PMI Manufacturing rose slightly to 49.7 in June, up from 49.5 and matching expectations. While still in contraction for a third straight month, the improvement in production (51.0) and new orders (50.2) suggests some stabilization in activity. Large manufacturers led the gains, with their PMI rising to 51.2, but conditions for small enterprises deteriorated sharply, with a 2-point drop to 47.3.

The Non-Manufacturing PMI also inched up to 50.5 from 50.3, supported by a rebound in construction activity. The construction business activity index rose to 52.8, while services slipped marginally to 50.1. Composite PMI rose to 50.7 from 50.4, reinforcing the picture of a subdued recovery.

NZ ANZ business confidence jumps to 46.3, but growth headwinds persist

Business confidence in New Zealand improved notably in June, with the ANZ headline index rising from 36.6 to 46.3 and firms’ Own Activity Outlook climbing from 34.8 to 40.9. Inflation expectations held steady at 2.71%.

ANZ warned that the underlying environment remains difficult, citing ongoing cost pressures, tight margins, and a global backdrop that continues to “impeding risk-taking”. The bank highlighted that while the 0.8% qoq Q1 growth was solid, the outlook for Q2 appears “not looking nearly so positive. Despite stronger sentiment, actual business conditions and demand may remain under pressure in the months ahead.

ANZ continues to forecast more rate cuts from the RBNZ than the central bank currently projects, arguing that the recovery will likely fall short of policymakers’ expectations. Still, it acknowledged that the RBNZ appears inclined to move slowly, balancing inflation risks with a softening economic backdrop.

US NFP and ISM, Eurozone CPI and ECB accounts watched this week

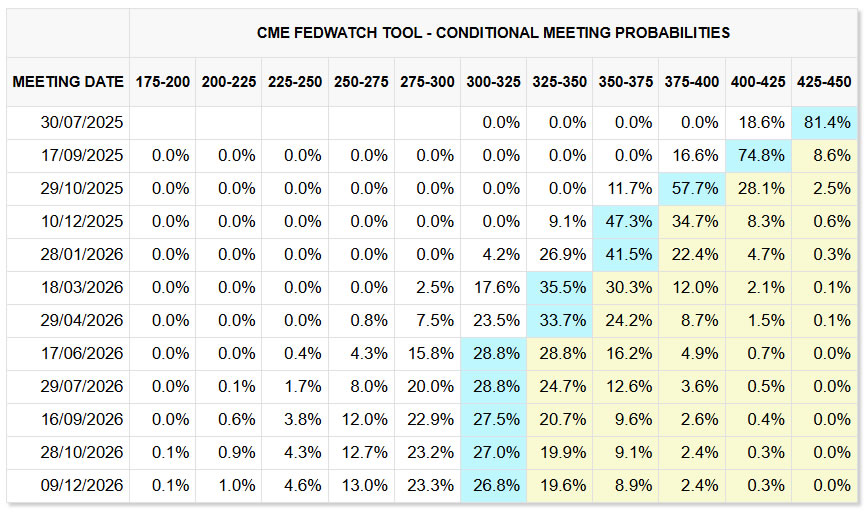

Markets will focus heavily on June’s US Non-Farm Payrolls report this week, which comes amid growing signs that Fed is willing to wait before resuming policy easing. Recent comments from Chair Jerome Powell and most other Fed officials suggest they still see the labor market as resilient, even as private-sector hiring has slowed. With tariffs set to lift inflation in the near term, policymakers appear content to wait while they assess how these effects filter into prices and activity.

Unless the NFP data is shockingly weak, it's unlikely to shift the consensus that July is too soon for another rate cut. September remains the earliest realistic window. That said, any meaningful downside surprise would firm up expectations for a September move and potentially encourage traders to lean more aggressively into bets for a third cut this year. For now, futures price in a 56% chance of a triple-easing path.

Beyond payrolls, traders will dissect the ISM Manufacturing and Services PMIs for guidance on activity, labor and inflation pressures. The prices and employment sub-indices carry particular weight in the current environment.

In the Eurozone, investors will focus on the June flash CPI and ECB meeting accounts. The central question is whether ECB has already concluded its current easing cycle or still sees the need for one final adjustment. While market pricing reflects a bias for one more cut by September, the lack of consensus is evident. A recent Reuters poll found only 53% of economists expecting another move.

Markets will look to the meeting accounts for any signs that influential members like Chief Economist Philip Lane see further cut as necessary. A dovish tone could revive rate cut bets and weigh on the Euro, while confirmation that ECB views policy as broadly appropriate now could prompt repricing toward a hold.

Here are some highlights for the week:

- Monday: Japan industrial production; China NBS PMIs; Germany import prices, retail sales, CPI flash; UK Q1 GDP final; Swiss KOF economic barometer; US Chicago PMI.

- Tuesday: Japan Tankan survey, PMI manufacturing final, consumer confidence; China Caixin PMI manufacturing; Swiss retail sales, PMI manuacturing; Eurozone PMI manufacturing final, CPI flash; Germany unemployment; UK PMI manufacturing final; US ISM manufacturing.

- Wednesday: Japan monetary base; Australia retail sales; Eurozone unemployment rate; US ADP employment; Canada PMI manufacturing.

- Thursday: Australia goods trade balance; China Caixin PMI services; Swiss CPI; Eurozone PMI Services final, ECB meeting accouints; UK PMI Services final; Canada trade balance; US non-farm payrolls, jobless claims, trade balance, ISM services.

- Friday: Japan household spendig; Germany factory orders; France industrial production; Swiss unemployment rate; UK PMI construction; Eurozone PPI.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3619; (P) 1.3689; (R1) 1.3750; More...

USD/CAD dips mildly today but stays in range of 1.3616/3797. Intraday bias remains neutral at this point. On the upside, break of 1.3797 will resume the rebound from 1.3538 short term bottom to 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 1.4017). Nevertheless, below 1.3616 will bring retest of 1.3538 low.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.

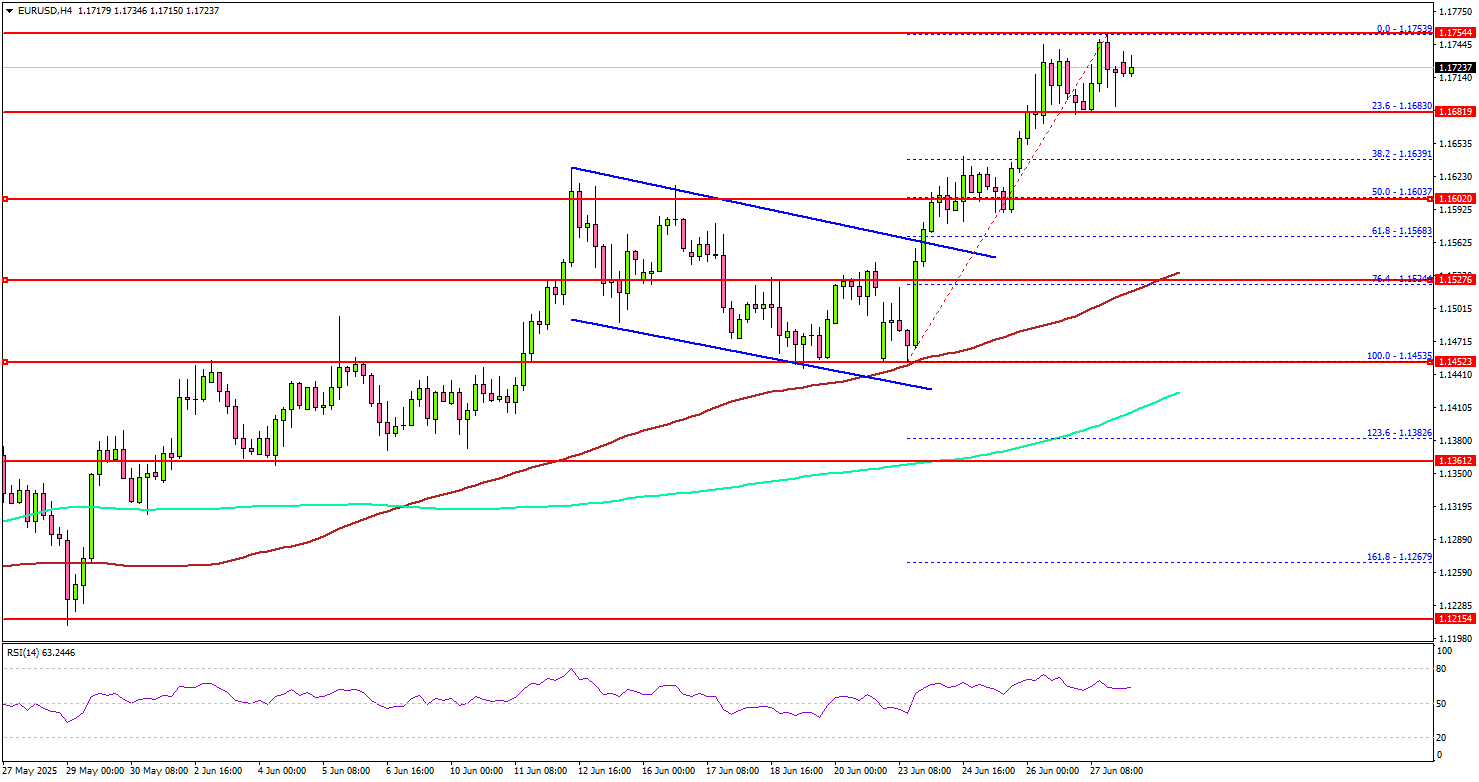

EUR/USD Pushes Upward — Bullish Momentum Supports Rally Extension

Key Highlights

- EUR/USD extended gains above the 1.1650 resistance.

- The pair is now consolidating below the 1.1750 resistance on the 4-hour chart.

- GBP/USD rallied above the 1.3650 and 1.3720 levels.

- USD/JPY might find bids near the 143.50 support zone.

EUR/USD Technical Analysis

The Euro started a steady increase above the 1.1650 level against the US Dollar. EUR/USD cleared many hurdles to enter a positive zone.

Looking at the 4-hour chart, the pair started an upward move by clearing a bullish flag pattern with resistance at 1.1565. It settled above the 1.1650 level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour).

The pair even cleared the 1.1720 level and tested the 1.1750 zone. It is now consolidating gains. On the downside, immediate support is near the 1.1680 level. The next key support sits near 1.1640.

Any more losses could send the pair toward the 1.1600 support zone. If the bulls remain active above the stated support levels, there could be a fresh increase. On the upside, the pair could face resistance near the 1.1750 level.

The next key resistance sits near the 1.1780 level. The first major resistance sits at 1.1800. A close above the 1.1800 level could set the pace for another increase. In the stated case, the pair could even clear the 1.1880 resistance. The next major stop for the bulls could be near the 1.1950 resistance.

Looking at GBP/USD, the pair gained pace for an upside break above the 1.3650 and 1.3720 resistance levels. The next key hurdle sits at 1.3800.

Upcoming Economic Events:

- German Consumer Price Index for June 2025 (YoY) (Prelim) – Forecast +2.1%, versus +2.1% previous.

- German Consumer Price Index for June 2025 (MoM) (Prelim) s– Forecast +0.2%, versus +0.1% previous.

- ECB's President Lagarde speech.

China’s PMI manufacturing rises to 49.7, small firms lag

China’s official NBS PMI Manufacturing rose slightly to 49.7 in June, up from 49.5 and matching expectations. While still in contraction for a third straight month, the improvement in production (51.0) and new orders (50.2) suggests some stabilization in activity. Large manufacturers led the gains, with their PMI rising to 51.2, but conditions for small enterprises deteriorated sharply, with a 2-point drop to 47.3.

The Non-Manufacturing PMI also inched up to 50.5 from 50.3, supported by a rebound in construction activity. The construction business activity index rose to 52.8, while services slipped marginally to 50.1. Composite PMI rose to 50.7 from 50.4, reinforcing the picture of a subdued recovery.

NZ ANZ business confidence jumps to 46.3, but growth headwinds persist

Business confidence in New Zealand improved notably in June, with the ANZ headline index rising from 36.6 to 46.3 and firms' Own Activity Outlook climbing from 34.8 to 40.9. Inflation expectations held steady at 2.71%.

ANZ warned that the underlying environment remains difficult, citing ongoing cost pressures, tight margins, and a global backdrop that continues to "impeding risk-taking". The bank highlighted that while the 0.8% qoq Q1 growth was solid, the outlook for Q2 appears "not looking nearly so positive. Despite stronger sentiment, actual business conditions and demand may remain under pressure in the months ahead.

ANZ continues to forecast more rate cuts from the RBNZ than the central bank currently projects, arguing that the recovery will likely fall short of policymakers’ expectations. Still, it acknowledged that the RBNZ appears inclined to move slowly, balancing inflation risks with a softening economic backdrop.

Japan’s industrial production rises 0.5% mom in May, far below expectation

Japan’s May industrial output came in far below expectations, rising just 0.5% mom versus the anticipated 3.4% mom growth. Though production improved in key sectors such as machinery and autos, five categories—led by non-auto transport equipment—recorded declines.

Shipments rose 2.2% mom, while inventories fell -1.9% mom, offering some positive signals, but not enough to shift the ministry’s cautious tone.

METI maintained its assessment that output “fluctuates indecisively”. A poll of manufacturers showed expectations for a muted 0.3% mom rise in June and a -0.7% mom drop in July.

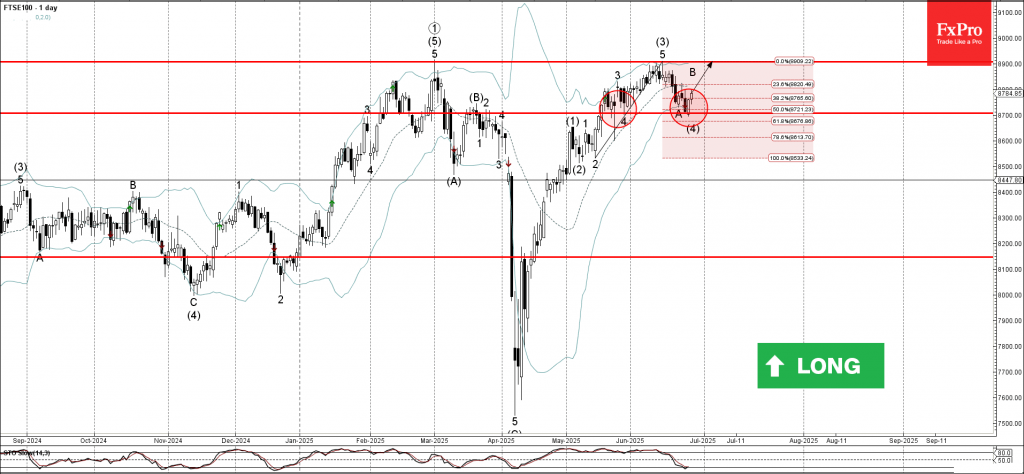

FTSE 100 Wave Analysis

FTSE 100: ⬆️ Buy

- FTSE 100 reversed from support level 8700.00

- Likely to rise to resistance level 8900.00

FTSE 100 index recently reversed up from the support level 8700.00 (which stopped wave 4 at the end of May, as can be seen from the daily FTSE 100 chart below) intersecting with the lower daily Bollinger Band and the 50% Fibonacci correction of the upward impulse from May.

The upward reversal from the support level 8700.00 stopped wave A of the active ABC correction (4) from the start of June.

Given the clear daily uptrend, FTSE 100 index can be expected to rise to the next resistance level 8900.00, which stopped the previous impulse wave (3).

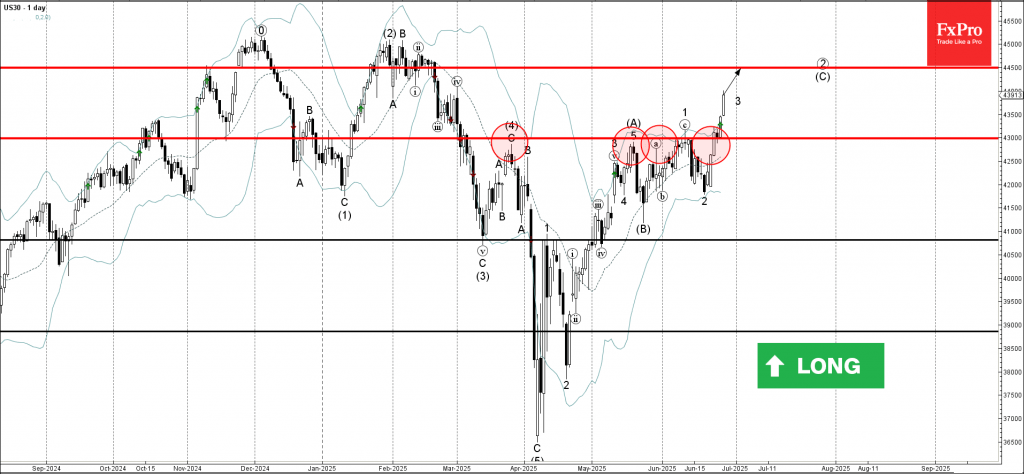

Dow Jones Wave Analysis

Dow Jones: ⬆️ Buy

- Dow Jones broke pivotal resistance level 43000.00

- Likely to rise to resistance level 44500.00

Dow Jones index recently broke above the pivotal resistance level 43000.00 (which has been reversing the price from the end of March, as can be seen from the daily Dow Jones chart below).

The breakout of the resistance level 43000.00 accelerated the active impulse wave 3 of the intermediate impulse wave (C) from the end of May.

Dow Jones index can be expected to rise to the next resistance level 44500.00, which is the target price for the completion of the active impulse wave (C).