Sample Category Title

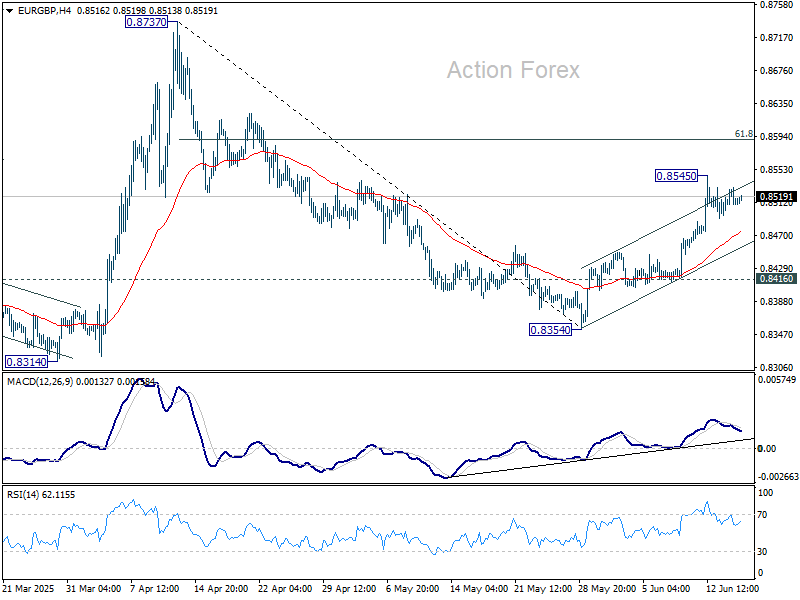

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8497; (P) 0.8515; (R1) 0.8531; More...

EUR/GBP is staying in consolidations below 0.6545 temporary top and intraday bias remains neutral. Further rally is expected as long as 0.8416 support holds. Above 0.8545 will target for 61.8% retracement of 0.8737 to 0.8354 at 0.8591. Firm break there will pave the way to 0.8373 resistance.

In the bigger picture, price actions from 0.8221 medium term bottom are merely forming a corrective pattern to the down trend from 0.9267 (2022 high). Nevertheless, there is no clear momentum to break through 0.8201 key support (2022 low) yet. Hence, range trading is expected between 0.8221/8737 for now.

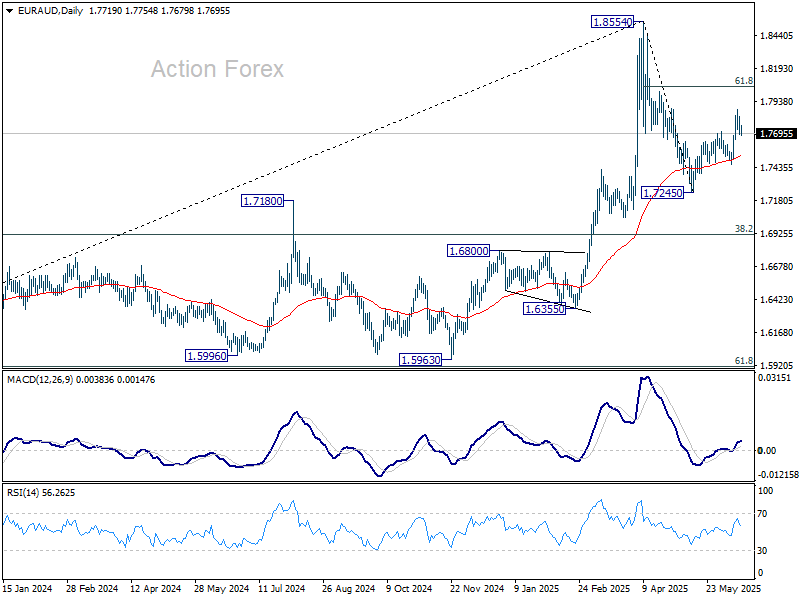

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7665; (P) 1.7744; (R1) 1.7800; More...

Intraday bias in EUR/AUD stays neutral as consolidations continue below 1.7880 temporary top. Overall development suggests that fall from 1.8554 has completed as a corrective move. Further rise is expected as long as 1.7459 support holds. Above 1.7880 will target 61.8% retracement of 1.8554 to 1.7245 at 1.8054. Firm break there will pave the way to 1.8554. However, break of 1.7459 will dampen this bullish view and bring deeper decline back to 1.7245 low.

In the bigger picture, with 55 W MACD staying well below signal line, 1.8554 is likely a medium term top already. Price actions from there are seen as a corrective pattern only. While deeper pullback might be seen, downside should be contained by 38.2% retracement of 1.4281 (2022 low) to 1.8554 at 1.6922 to bring rebound. Up trend from 1.4281 is still expected to resume at a later stage.

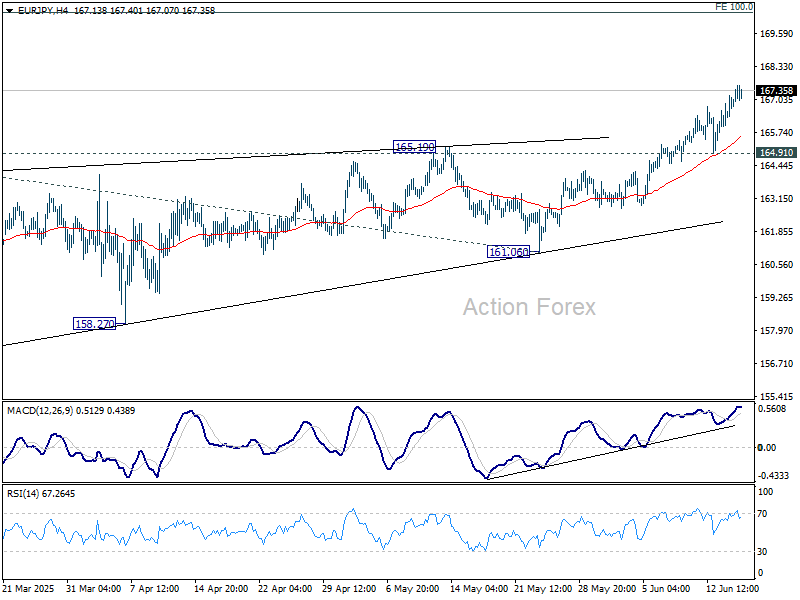

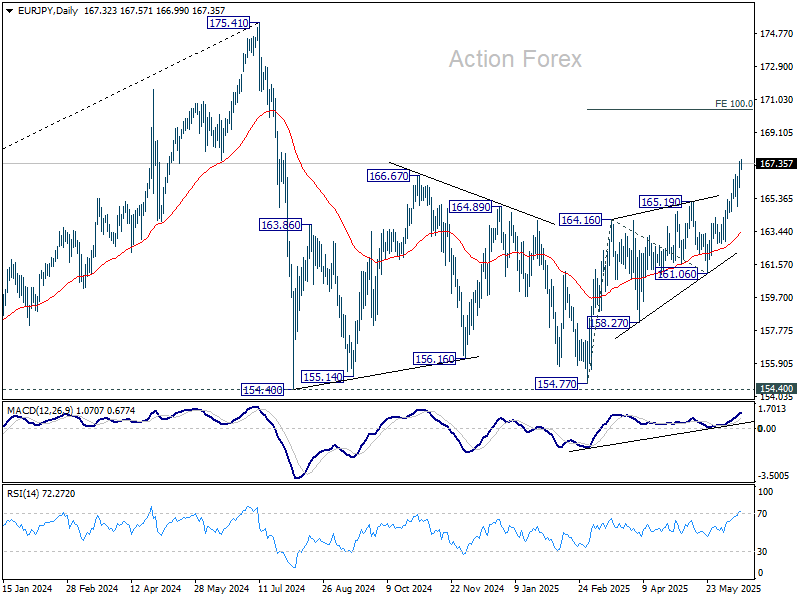

EUR/JPY Daily Outlook

Daily Pivots: (S1) 166.42; (P) 166.95; (R1) 167.91; More...

Intraday bias in EUR/JPY remains on the upside for the moment. Current rise from 154.77 is in progress. Next target is 100% projection of 154.77 to 165.19 from 161.06 at 170.45. For now, further rally is expected as long as 164.91 support holds, in case of retreat.

In the bigger picture, price actions from 175.41 are seen as correction to up trend from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

Any Sort of Negative USD-News Could Deliver Another Blow to the Greenback.

Markets

The situation in the Middle East continues dominating headlines. Israel’s rapid dominance over western Iranian skies lowered chances of an escalation with Iran rumored to be willing to restart nuclear talks. The 1%-rebound of stock markets adds to our hypothesis that – apart from oil prices – those regional conflicts often have a rather brief shelf life as dominant market theme. US President Trump abruptly leaving the G7-meeting one day early and calling for Tehran evacuation sends risk sentiment the other way again this morning as the waiting game for stronger market forces continues. Tomorrow’s FOMC meeting, the approaching deadline of 90-day tariff pauses (July 8), Senate progress of Trump’s beautiful bill (Senate version expected as soon as Monday; July 4 deadline is still on) or the German cabinet meeting to decide/unveil initial infrastructure spending plans (June 24) are all loose ends with (significant) market moving potential.

Core bonds threaded water for most of the day, though the very long end of the US curve underperformed somewhat after an average 20-yr Bond auction. At the margin, it contrasted somewhat with better sales of 10-yr and 30-yr Notes/Bonds last week. The US 30-yr yield added 6.1 bps on a daily basis and is rapidly closing in on the psychological 5% mark (4.95% close). Breaching that level caused some more general market stress last month. The German yield curve ended almost at Friday’s levels. On FX markets, the dollar failed to profit from recent market volatility and higher oil prices. At EUR/USD 1.1558, it suggests that any sort of negative USD-news could deliver another blow to the greenback. Short term (today), we eye US retail sales. Consensus expects a 0.6% M/M drop in the headline number with sales excluding auto and gas forecast to be 0.3% higher on the month. We see asymmetric risks with any signs of (tariff-related) weakening in US consumer demand being used to ignite some Fed rate cut bets later this year and able to hurt the dollar. EUR/GBP holds steady this morning around 0.8515 with news of the signed trade deal between US President Trump and UK PM Starmer being discounted already. Tomorrow’s UK inflation numbers and Thursday’s BoE meeting are more important GBP-drivers. Especially if they provide leeway to extending the quarterly cutting cycle.

News & Views

The Japanese central bank left the base rate unchanged at 0.5% this morning but adjusted its tapering plans. It had been reducing the amount of bond buying since August of last year with the aim of halving the JPY 5.7tn monthly pace to JPY 2.9tn through March 2026. This represented a decrease by JPY 400bn each quarter. The BoJ sticks to that plan but will slow down the tapering pace to JPY 200bn in the next fiscal year from March 2026 through March 2027. Monthly buying in this case will then have been trimmed to JPY 2.1tn. This will be subject to an interim assessment at the June 2026 meeting first and suggests the BoJ wants to keep all flexibility. It was in any case an expected move based on a survey by the central bank among market participants, asking about the optimal size of purchase reductions. Markets are not expecting much for the remainder of the year in terms of rate hikes. The BoJ noted moderating growth and sluggish underlying CPI but said that both would rise in the medium term. It mentioned trade in particular as a risk to the outlook. The Japanese yen rises slightly against peers this morning. Yields in the country add about 4 bps in longer tenors.

US president Trump and UK PM Starmer at the G7 summit have signed a document, agreeing to move ahead with the trade agreement/framework struck last month. Among the provisions are reduced US tariffs on UK auto exports from 27.5% to 10% on an annual quota of 100k vehicles. And after signing an executive order, Trump exempted UK’s civil aerospace aircraft sector from the baseline 10% tariff. A key UK demand also included an exemption on steel from the 25% levy but the US would only do so up until a certain quota that still needs to be set. UK in return a.o. committed to “working to meet American requirements on the security of the supply chains of steel and aluminum” including on the “nature of ownership”. This was done in particular to address US concerns on foreign ownership of British Steel, a major steel company acquired by China in 2020. The US also won UK concessions on agriculture.

Not a Classical De-Escalation Story

Stocks in Europe and the US rallied as oil and gold retreated yesterday on news that Iran is willing to resume talks on its nuclear program. The market interpreted this as a sign that Iran either has no intention — or possibly no means — to escalate the war, easing concerns about potential disruption to the Strait of Hormuz, a critical chokepoint through which around 20% of global oil and gas flows transit.

However, this is not a classic de-escalation story. While Iran appears to be signalling restraint, former President Donald Trump urged the evacuation of Tehran, and Israel has vowed to continue its strikes. This makes it a one-sided de-escalation at best, and keeps risks across energy markets and haven assets tilted to the upside. If Iran fails to find room to manoeuvre diplomatically, it could easily make a U-turn.

Meanwhile, tensions between Russia and Ukraine remain high

As such, natural gas surged nearly 5% yesterday and continues to climb this morning, while oil prices are also rebounding. US crude is bid into the $70 per barrel, while Brent sees demand below its 200-DMA near $71.40. Upside appears limited for now, as the market remains well-supplied — the US is pumping at record levels, and OPEC+ is adding hundreds of thousands of barrels back into a market with weak demand and soft Chinese data. Yet global energy supply remains fragile, and it wouldn’t take much to shake the physical flow of oil and reverse market sentiment in a heartbeat.

History offers two valuable templates

In the early 1970s, oil seemed abundant. Supply was strong, demand was healthy, and few foresaw disruption. Then came the 1973 Arab Oil Embargo. Practically overnight, the world flipped from oversupply to panic. Oil prices quadrupled, strategic reserves were born, and energy security became a global priority. The market had underestimated just how quickly a geopolitical shock could upend the balance.

Then, in the 1980s, we saw the opposite kind of shock. Demand growth slowed dramatically — thanks to fuel efficiency, conservation efforts, and structural economic shifts — while supply surged from new sources like the North Sea and Alaska. OPEC attempted to support prices by cutting output, but non-OPEC countries kept pumping. In 1986, Saudi Arabia gave up defending prices and opened the taps, triggering a price collapse from $30 to under $10 a barrel, and ushering in a decade of cheap oil.

Today, we see a blend of both historical dynamics. Supply is rising, OPEC is relaxing its restrictions, demand remains sluggish, and geopolitical tensions are mounting. This leaves the market at a crossroads:

- One path resembles the 1970s, where a geopolitical shock chokes supply and sends prices soaring.

- The other mirrors the 1980s, where weakening cartel discipline sparks a price war and the market crashes under its own abundance.

Which way will it break? That’s unclear. But history tells us this: when oil markets feel safest, they’re often sitting on the edge of a major turn. The latter wouldn’t mean sustainably high oil prices, but a spike is a risk that remains on the table. And higher oil prices is bad for global inflation, it rises price pressures and forces the central banks to hike interest rates. Higher borrowing costs weigh on growth prospects and equity valuations. So the level of uncertainty in the market and actual risk appetite barely match.

In FX markets, the US dollar remains under pressure, suggesting that investors are still not fully pricing in Middle East risk. But this sense of calm may be misplaced. Markets seem far too relaxed in the face of serious geopolitical risks. Any escalation could trigger renewed appetite for the dollar, gold, and oil. Despite recent weakness driven by global trade tensions, the dollar tends to hold up well when geopolitical uncertainty rises.

The EURUSD continues to consolidate gains above the 1.15 mark, while the yen showed only a muted reaction to the Bank of Japan's (BoJ) decision to leave rates unchanged and slow the pace of bond tapering — as expected. The USDJPY is down this morning due to broad-based dollar softness, but Japanese 10-year yields have risen for a third consecutive day, adding to risks for global markets: rising Japanese yields threaten to reverse carry trades, posing another headwind for global risk assets.

Note also that rising Japanese yields could be pressuring US yields higher. The US 10-year is trending up, despite the fraught geopolitical backdrop. As a result, equity indices are in the red this morning, and we may see the S&P 500 give back its Monday gains.

Looking ahead, the Federal Reserve (Fed) kicks off its two-day policy meeting today. While no change in rates is expected, geopolitical uncertainty and trade tensions make the outlook more complex. Recent inflation data has been reassuring — suggesting price pressures are not accelerating — but tariffs and the risk of an oil price spike due to Middle East tensions will likely keep the Fed in a cautious stance.

That said, markets could still react strongly to even a hint of dovishness from the Fed this week. Investor positioning and sentiment suggest a clear appetite to push the S&P 500 to fresh all-time highs. But with little fundamental support behind the current risk rally, much of it appears to be driven by FOMO — the fear of missing out.

Ongoing Conflict Between Isreal and Iran

In focus today

Strikes in Iran and Isreal are continuing to escalate with Isreal claiming control of Teheran airspace yesterday. Israel has expanded its bombardment of Iran and is now also targeting critical energy infrastructure. Iran is responding with its largest ever missile assault but has so far abstained from actions that would disrupt or devastate global energy markets. Join us in a 30-minutes briefing What's next in the Middle East where our experts walk you through the current situation and what to expect going forward today at 10:30-11:00 CET.

In the afternoon, US retail sales and industrial production data are due for release for May. Consumer sentiment has improved after the US-China trade deal in mid-May according to the latest surveys, but retail sales data will provide more tangible evidence if that has truly been the case. The latest hard data point from April showed households' savings rate ticking higher as a sign of rising caution.

On the data front from Germany, we will receive the ZEW index for June. Expectations rebounded in May following the April 'liberation day' plunge. We expect a further improvement in June as the trade war risk has eased. Amid rising expectations, we expect the assessment of the economic situation to remain low.

In the morning for Sweden, we will receive the official labour market data (LFS) for May. We expect a modest decline in employment (m/m) and a similarly small increase in the unemployment rate, to 8.6%, which would be in line with weaker labour demand indicators such as new vacancies. Additionally, the National Institute of Economic Research (NIER) will release their new macroeconomic forecasts today, which are highly valued by the forecasting community.

Economic and market news

What happened overnight

In Japan, the Bank of Japan left rates unchanged this morning by a unanimous vote, as widely expected. With an 8-1 vote, they decided to keep the current tapering pace in place until March 2026 but reduce it from then on, also as expected. This means, the current bond purchase of about JPY4 trillion per month will be reduced to JPY3 trillion by March 2026 and JPY2 trillion by March 2027. The market reaction has been very muted on the decision.

We continue to see scope for a rate hike in October, even if recent market pricing has pushed the next rate hike into early next year. Upcoming wage data confirming the solid negotiated pay hikes in the spring and perhaps a trade deal with the US might give room for a clearer picture going forward. Around 07.30 CET, we will listen in to the press conference, when Governor Ueda balances continued high inflation driven by food and the risk from the trade war.

What happened yesterday

In energy markets, oil prices declined to USD 73 per barrel - up only 3 dollars compared to before the initial attack. The decline was due to news that Iran could be looking to de-escalate the conflict with Israel. If the situation starts to calm, we expect oil prices to fall back further, as focus would shift from the oil market and return to the trade war and the potential for further OPEC+ output increases. Yet, tensions remain high as Trump left a G-7 meeting to return to Washington, D.C. to focus on the conflict, while calling for an evacuation of Tehran.

In China, the batch of data for May showed a solid revival in retail sales, however also a weakening housing market. Stimulus continues to keep the Chinese economy afloat amid the US-China trade war, likely keeping growth close to the 5% target level this year.

Equities: Equity markets rallied broadly across regions yesterday in what looked like a rebound - or perhaps more precisely - a reversal of Friday's moves. Cyclicals outperformed defensives rather clearly, and energy stocks were notably weaker, following a decline in oil prices. One point worth noting is that the pharma sector underperformed on both sides of the Atlantic. In the US yesterday, Dow +0.75%, S&P 500 +0.94%, Nasdaq +1.52%, Russell 2000 +1.12%. This morning, the picture in Asia is mixed, with Japan leading the way despite the Bank of Japan telling it will cut its bond buying program in half starting 2026. As expected, the BoJ kept rates unchanged. Futures in both the US and Europe point lower ahead of the open.

FI and FX: Risk sentiment improved through yesterday's session as Iran was reported to seek and end to hostilities. Oil prices dropped following the announcement, though attacks from both sides have continued. Euro rates fell, with short-end tenors prompting a bullish steepening of the 2s10s swap curve. Meanwhile, US Treasury yields continued their upward trajectory, driven by rising inflation breakeven levels. The DXY index edged down as EUR/USD briefly surpassed the 1.16 threshold. EUR/SEK and EUR/NOK remained largely stable throughout the session, while USD/JPY climbed. The Bank of Japan maintained its policy rate at 0.5%, signalling a deceleration in JGB purchases from April 2026. The yen experienced minimal impact, with USD/JPY trading at 144.5 this morning. However, overnight risk sentiment has deteriorated following President Trump's call for an evacuation of Tehran.

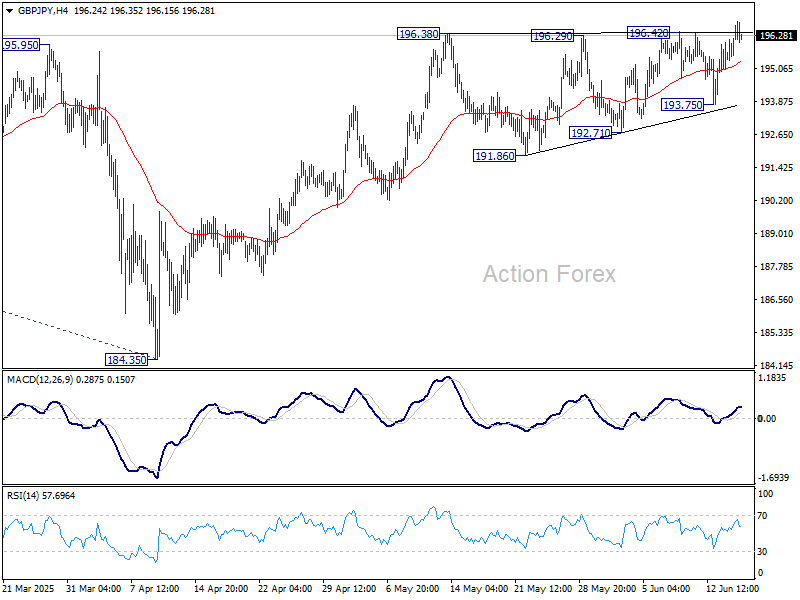

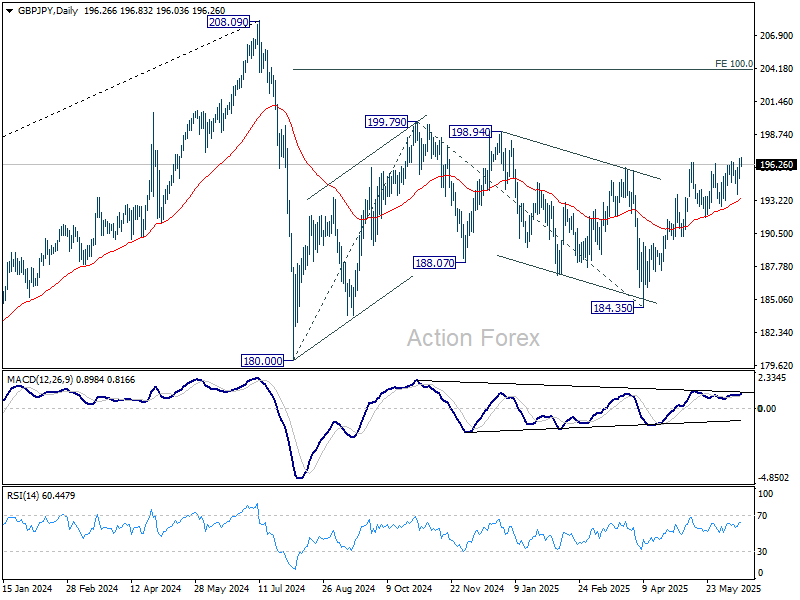

GBP/JPY Daily Outlook

Daily Pivots: (S1) 195.58; (P) 196.13; (R1) 197.14; More...

GBP/JPY retreated mildly after edging higher to 196.83. Yet, the breach of 196.42 resistance argues that rise recent rally is resuming. Intraday bias is mildly on the upside for 199.79 resistance first. Firm break there will target 100% projection of 180.00 to 199.79 from 184.35 at 204.14. For now, outlook will stay cautiously bullish as long as 193.75 support holds, in case of retreat.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 175.94 will bring deeper fall even still as a correction.

Yen Recovers Slightly After BoJ Hold; Trade Diplomacy Mixed Across G7

Yen recovered modestly after BoJ held interest rates steady at 0.50%, in line with expectations. The decision came with no change to the existing bond taper plan, but with a new framework to gradually reduce bond purchases starting in fiscal 2026. Markets interpreted the move as largely symbolic for now, since implementation begins next year. Overall, reaction was subdued, with most major currencies trading within last week’s ranges.

BoJ’s decision to phase in bond tapering follows a spike in yields on super-long Japanese government bonds last month, which has increased fiscal strain. Finance Minister Katsunobu Kato warned that sustained high rates could worsen Japan’s fiscal health. BoJ Governor Ueda acknowledged waning demand for long-dated bonds and noted that yield volatility in those maturities risks bleeding into shorter-term rates with broader economic consequences.

Still, Yen's rebound was limited as the market continues to price in a long period of policy inertia. Underlying inflation remains sluggish and economic growth is projected to moderate in the near term. With medium-term inflation expected to rise only gradually, the BoJ is sticking to a cautious path while monitoring global developments—especially on the trade front.

Trade diplomacy produced mixed results at the G7. The US and UK reached a new deal that preserves favorable tariff treatment for British autos and eliminates duties on aerospace exports, but left the steel and aluminum issue unresolved. The deal averts higher tariffs scheduled for next month, but Britain must meet new security conditions to keep its metals industry exempt. Prime Minister Starmer secured some concessions, but the agreement remains partial.

By contrast, Japan came away empty-handed from its bilateral session with the US Prime Minister Ishiba admitted to reporters that significant gaps remain, particularly on auto tariffs. The 25% levy on Japanese vehicles, along with other reciprocal tariffs, remains paused until July 9—but time is running out. Without a deal, Japan faces renewed headwinds just as its economy shows signs of softening.

Meanwhile, Canada and the US have committed to finalizing a comprehensive economic and security agreement within 30 days. While no details were released, both sides characterized the talks as constructive. These incremental steps highlight the fragmented state of global trade realignment as countries seek partial wins amid broader tensions.

In the forex market, Aussie and Kiwi outperform, while Euro follow with mild gains. Dollar, Swiss Franc, Yen and remain softer, with most pairs and crosses trapped inside last week's ranges.

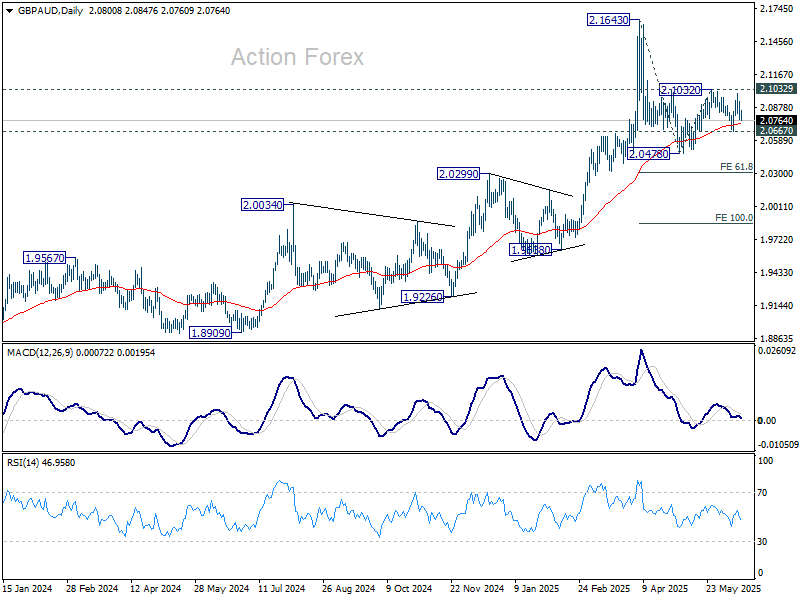

Technically, GBP/AUD was rejected by 2.1032 resistance again and focus is back on 2.0667 support. Firm break there will argue that the correction from 2.1643 is resuming with another down leg through 2.0478 support to 61.8% projection of 2.1643 to 2.0478 from 2.1032 at 2.0312. Nevertheless, break of 2.1032 will extend the rebound from 2.0478 to retest 2.1643 high.

In Asia, at the time of writing, Nikkei is up 0.46%. Hong Kong HSI is down -0.32%. China Shanghai SSE is down -0.08%. Singapore Strait Times is up 0.36%. Japan 10-year JGB yield is up 0.026 at 1.48. Overnight, DOW rose 0.75%. S&P 500 rose 0.94%. NASDAQ rose 1.52%. 10-year yield rose 0.028 to 4.452.

Looking ahead, Germany ZEW economic sentiment is the main feature in European session. Later in the day, US retail sales will take center stage. Import prices, industrial production and capactity utilization, business inventories, and NAHB housing index will also be released.

BoJ maintains policy, expects gradual rebound in inflation after near term weakness

BoJ kept its short-term interest rate unchanged at 0.5% in a unanimous decision today, while sticking with its current bond tapering program through March 2026. Looking further out, the central bank introduced a new bond purchase schedule for fiscal 2026, planning to reduce monthly purchases by JPY 200B each quarter, bringing the total to JPY 2T per month by March 2027.

In its statement, the BoJ downgraded its growth outlook, noting that Japan’s economy is “likely to moderate” in the near term as overseas economies slow and domestic corporate profits weaken. While accommodative financial conditions should provide some support, the central bank only expects a modest recovery later as global growth returns.

On inflation, the impact from food and import price increases is "expected to wane", while underlying CPI is likely to remain “sluggish” due to a slowing economy. However, the bank anticipates that inflation will gradually pick up over time, supported by rising medium- to long-term inflation expectations and a growing “sense of labor shortage” as the economy recovers.

BoJ also acknowledged “extremely uncertain" outlook around the global trade and policy environment, warning of spillovers to Japan’s financial markets and inflation outlook. The statement emphasized the need to closely monitor foreign exchange developments and their broader implications.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 195.58; (P) 196.13; (R1) 197.14; More...

GBP/JPY retreated mildly after edging higher to 196.83. Yet, the breach of 196.42 resistance argues that rise recent rally is resuming. Intraday bias is mildly on the upside for 199.79 resistance first. Firm break there will target 100% projection of 180.00 to 199.79 from 184.35 at 204.14. For now, outlook will stay cautiously bullish as long as 193.75 support holds, in case of retreat.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 175.94 will bring deeper fall even still as a correction.

BoJ maintains policy, expects gradual rebound in inflation after near term weakness

BoJ kept its short-term interest rate unchanged at 0.5% in a unanimous decision today, while sticking with its current bond tapering program through March 2026. Looking further out, the central bank introduced a new bond purchase schedule for fiscal 2026, planning to reduce monthly purchases by JPY 200B each quarter, bringing the total to JPY 2T per month by March 2027.

In its statement, the BoJ downgraded its growth outlook, noting that Japan’s economy is “likely to moderate” in the near term as overseas economies slow and domestic corporate profits weaken. While accommodative financial conditions should provide some support, the central bank only expects a modest recovery later as global growth returns.

On inflation, the impact from food and import price increases is "expected to wane", while underlying CPI is likely to remain “sluggish” due to a slowing economy. However, the bank anticipates that inflation will gradually pick up over time, supported by rising medium- to long-term inflation expectations and a growing “sense of labor shortage” as the economy recovers.

BoJ also acknowledged “extremely uncertain" outlook around the global trade and policy environment, warning of spillovers to Japan’s financial markets and inflation outlook. The statement emphasized the need to closely monitor foreign exchange developments and their broader implications.

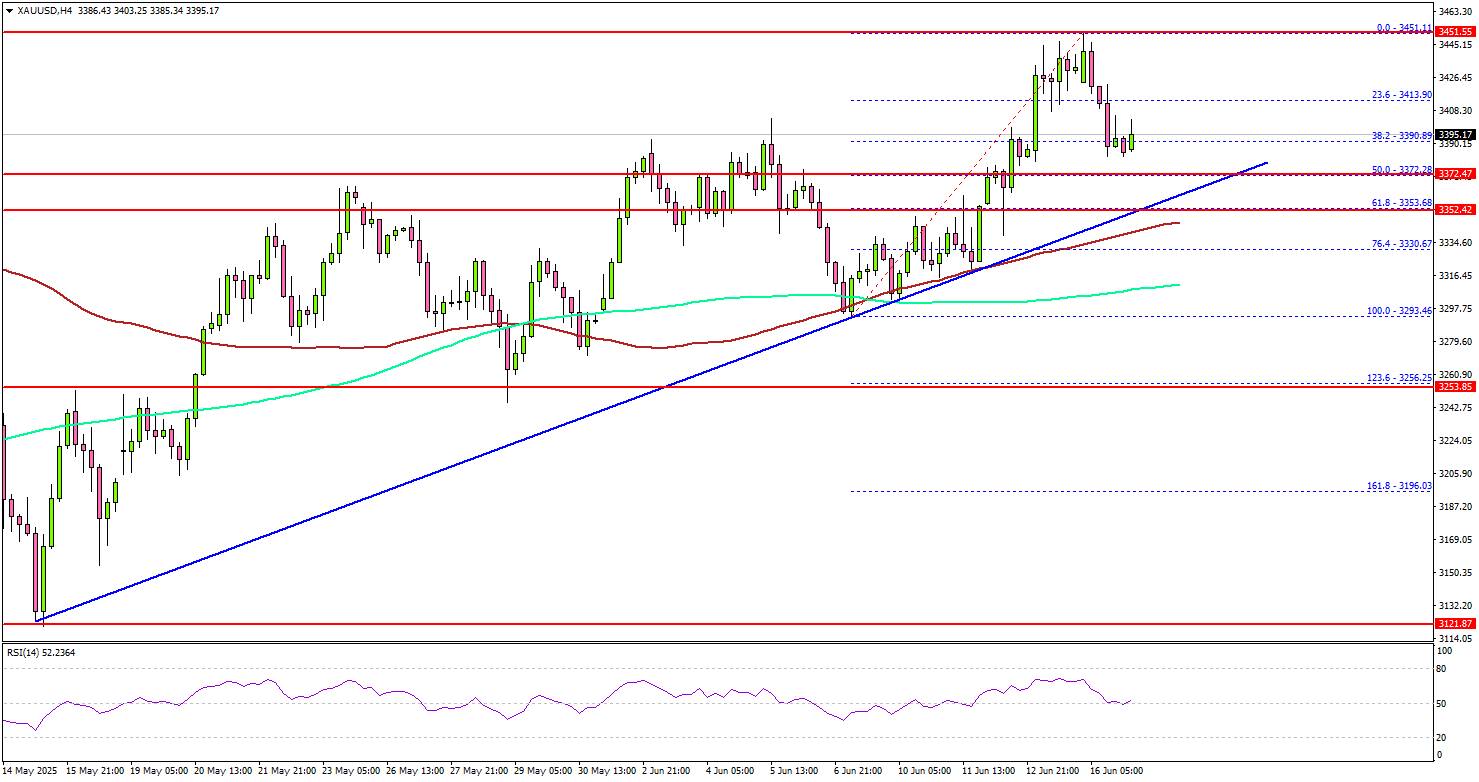

Gold Dips, But Sentiment Turns Bullish on Long-Term Potential

Key Highlights

- Gold found support near $3,250 and started a fresh increase.

- A key bullish trend line is forming with support at $3,355 on the 4-hour chart.

- EUR/USD is moving higher above the 1.1550 resistance zone.

- WTI Crude Oil prices dipped sharply after facing rejection near $77.50.

Gold Price Technical Analysis

Gold prices remained supported above $3,250. The price formed a base and started a fresh increase above the $3,280 and $3,320 resistance levels.

The 4-hour chart of XAU/USD indicates that the price settled above the $3,375 level, the 200 Simple Moving Average (green, 4 hours), and the 100 Simple Moving Average (red, 4 hours). It even cleared the $3,440 level before the bears appeared.

A high was formed near $3,451 and the price saw a downside correction. There was a move below $3,440. On the downside, initial support is near the $3,372 level.

The first key support is $3,355. There is also a key bullish trend line forming with support at $3,355 on the same chart. The next major support is near the $3,335 level. The main support is now $3,320. A downside break below the $3,320 support might call for more downsides. The next major support is near the $3,250 level.

On the upside, immediate resistance is near the $3,440 level. The next major resistance sits near the $3,450 level. A clear move above the $3,450 resistance could open the doors for more upsides. The next major resistance could be $3,480, above which the price could rally toward the milestone level of $3,500.

Looking at EUR/USD, the pair started a decent upward move and might soon aim for a fresh increase if it clears the 1.1650 resistance.

Economic Releases to Watch Today

- US Industrial Production for May 2025 (MoM) – Forecast +0.1%, versus 0% previous.

- US Retail Sales for May 2025 (MoM) – Forecast -0.7%, versus +0.1% previous.