Sample Category Title

Canada: Housing Starts Remained Elevated in May

Canadian housing starts came in at a healthy rate of 279.5k annualized units in May, essentially holding on to April's large gain. Meanwhile, the six-month moving average of starts inched higher by 0.8% m/m to 243.4k units.

In urban markets, May's performance was evenly split across the multi-family and single-detached sectors, with the former rising by 2k to 217.3k units, while the latter declined by the same amount to 42.5k units.

Urban starts were up in 5 of 10 provinces:

- Starts rose strongly in Quebec (+10k to 61k units) while inching higher in Ontario (+1.8k to 66k units). They also increased in the Prairies (+6.2k to 81k units), lifted by Manitoba and Alberta.

- Starts dropped in the Atlantic (-2.3k to 16k units), weighed down by Newfoundland and Labrador, PEI and Nova Scotia. They also pulled back significantly in B.C. (-15.4k to 36k units).

Key Implications

With May's solid level, housing starts are on track to increase in the second quarter. This bodes well for residential investment and should help offset some softness on this component coming through from home sales.

Elevated building permits suggest that homebuilding can maintain a healthy pace in the near-term, but we don't expect this to last. Homebuilding should cool moving forward as slower population growth, falling rents in key markets, high construction costs, and past declines in home sales weigh on activity.

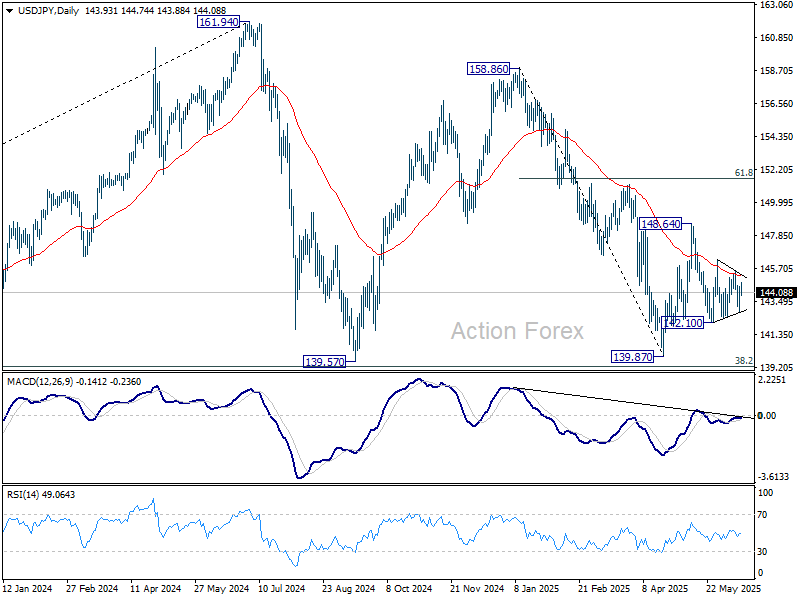

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 143.10; (P) 143.79; (R1) 144.78; More...

USD/JPY is staying in sideway trading and intraday bias remains neutral. Sideway trading continues in USD/JPY and intraday bias remains neutral. On the downside, break of 142.10 support will resume the fall from 148.64 to retest 139.87 low. On the upside, above 145.46 will turn bias to the upside for 146.27 first. Firm break there will target 148.64 resistance.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

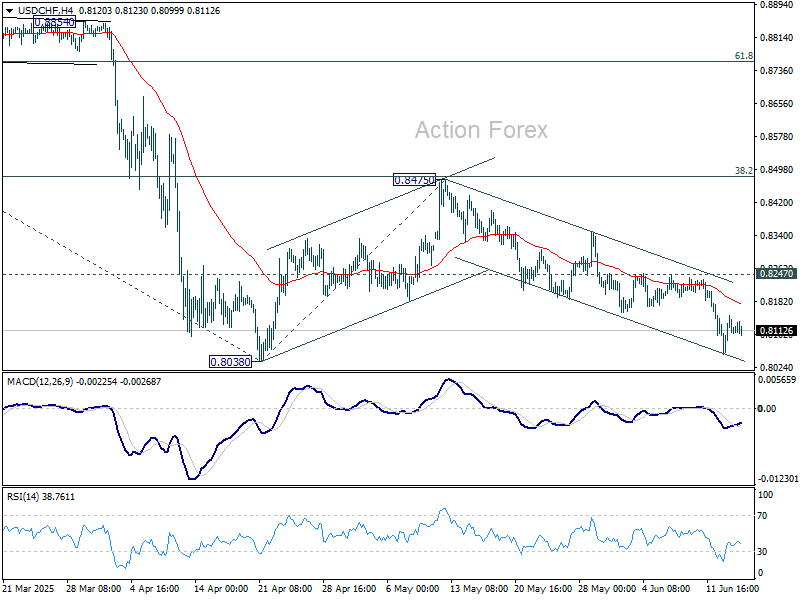

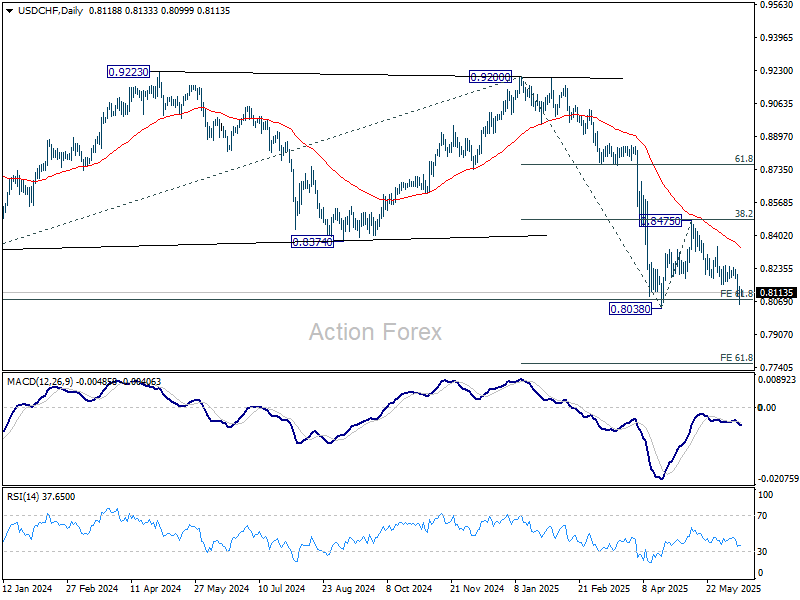

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8062; (P) 0.8106; (R1) 0.8155; More….

Intraday bias in USD/CHF stays neutral and outlook is unchanged. On the upside, break of 0.8247 resistance will argue that corrective pattern from 0.8038 is starting the third leg. Bias will be turned back to the upside for 0.8475 resistance again. However, firm break of 0.8038 will resume larger down trend. Next target will be 61.8% projection of 0.9200 to 0.8038 from 0.8475 at 0.7757.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8656) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

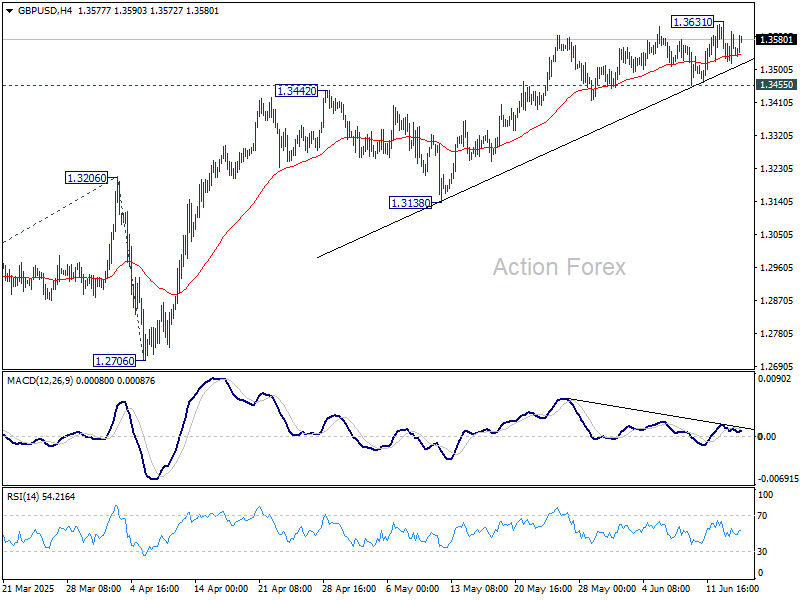

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3517; (P) 1.3574; (R1) 1.3632; More...

GBP/USD is staying in consolidations below 1.3631 temporary top and intraday bias remains neutral. Further rally is expected as long as 1.3455 support holds. Break of 1.3631 will resume the rise from 1.2099 and target 100% projection of 1.2099 to 1.3206 from 1.3138 at 1.3813. On the downside, break of 1.3455 support should confirm short term topping, and bring deeper correction to 55 D EMA (now at 1.3320) instead.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2937) holds, even in case of deep pullback.

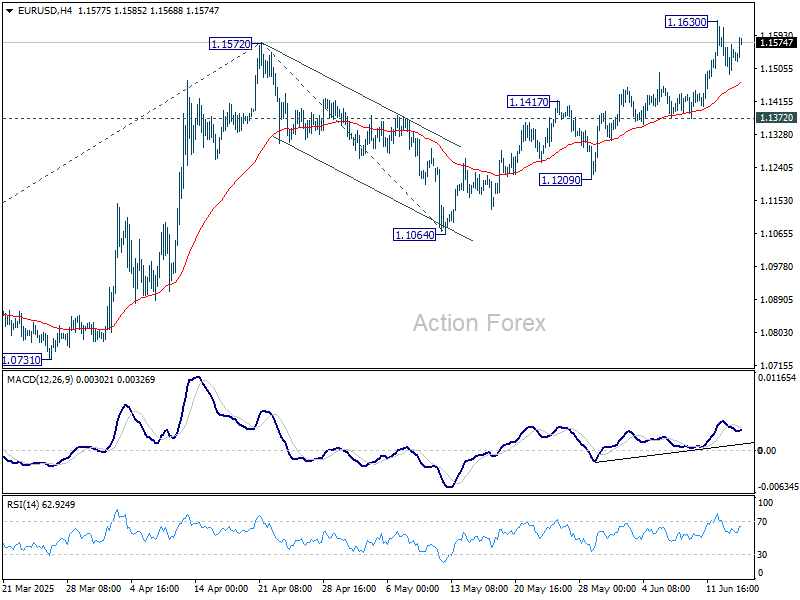

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1491; (P) 1.1552; (R1) 1.1616; More...

Intraday bias in EUR/USD remains neutral and more consolidations could be seen below 1.1630 temporary top. Further rise is expected as long as 1.1372 support holds. Break of 1.1572 will extend the rally from 1.0176. Next target is 61.8% projection of 1.0176 to 1.1572 from 1.1064 at 1.1927. However, break of 1.1372 support will indicate short term topping, and turn bias to the downside for deeper pullback.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 1.1604 support holds.

Geopolitics on Backburner as Investors Eye Trade Negotiations and BoJ Hold

Global financial markets showed remarkable resilience on Monday despite a continuous escalation in Middle East tensions. Iranian missiles struck Israel’s Tel Aviv and Haifa overnight, prompting an immediate warning from Israel’s defence minister that Tehran would soon “pay the price.” Iran has reportedly rejected ceasefire negotiations while under Israeli attack, communicating its position through mediators in Qatar and Oman. Yet, despite the geopolitical flare-up, European bourses edged higher, following gains in Asia, and US futures suggest a positive open.

Investor focus appears to be shifting from conflict zones back to trade negotiations. A report in Handelsblatt suggests EU negotiators are considering offering the US 10% tariff on all EU exports to prevent harsher measures targeting key sectors like autos, pharmaceuticals, and electronics. The proposal is not permanent and would come with strings attached. In return, Brussels is reportedly open to reducing tariffs on US vehicles and easing legal or technical barriers that have historically limited American car exports to Europe.

Meanwhile, Japanese Prime Minister Shigeru Ishiba is set to meet US President Donald Trump on the sidelines of the G7 summit. Tokyo has been seeking a breakthrough on tariff issues after several inconclusive rounds of negotiations. Monday's high-level meeting is seen as a potential turning point, although expectations remain cautious.

Currency markets are calm, with most major pairs trading within Friday’s range. Dollar is underperforming, followed by Yen and Canadian Dollar. In contrast, Aussie and Kiwi are leading the pack, benefiting from the mild risk-on mood. Euro is also moderately firmer, while the Swiss franc and Aussie are positioned in the middle of the board.

BoJ’s rate decision is the key focus in the upcoming Asian session. The central bank is widely expected to leave its policy rate unchanged at 0.50%. Amid lingering trade uncertainty and weak external demand, expectations for further tightening have diminished. A Reuters poll shows 52% of economists now see no additional rate hikes in 2025, with most expecting just one 25-basis-point hike by March 2026. Unless trade dynamics improve meaningfully, BoJ is likely to maintain its cautious stance.

Technically, CHF/JPY's rally from 165.83 continues today and edged higher to 178.17. Current development suggests that medium term consolidation from 180.05 has already completed with three waves to 165.83, and larger up trend is ready to resume. Still, the main hurdle for this bullish case lies is resistance zone between 61.8% projection of 165.83 to 176.45 from 173.06 at 179.62 and 180.05. Or in short, 180 psychological level is the key.

In Europe, at the time of writing, FTSE is up 0.47%. DAX is up 0.36%. CAC is up 0.74%. UK 10-year yield is up 0.007 at 4.564. Germany 10-year yield is up 0.02 at 2.558. Earlier in Asia, Nikkei rose 1.26%. Hong Kong HSI rose 0.70%. China Shanghai SSE rose 0.35%. Singapore Straight Times fell -0.08%. Japan 10-year JGB yield rose 0.051 to 1.454.

Swiss government cuts GDP forecast, warns of below-average growth in 2025–26

Switzerland’s Federal Government Expert Group has lowered its economic growth forecasts, citing persistent global trade uncertainty and weaker investment momentum. GDP, adjusted for sporting events, is now projected to grow just 1.3% in 2025 and 1.2% in 2026, down from March’s forecasts of 1.4% and 1.6%, respectively.

These figures imply a period of significantly below-average growth for the Swiss economy, even under the assumption that the recent US import tariffs remain capped at current levels and that the trade conflict does not escalate further.

The inflation forecast for 2025 has been revised down to just 0.1%. In 2026, inflation is projected to pick up to 0.5%.

ECB's Nagel warns against premature policy commitment

German ECB Governing Council member Joachim Nagel struck a cautious tone at a conference today, warning against locking in any specific policy path amid persistent global uncertainty.

Markets currently price in only one more rate cut by year-end. But Nagel resisted endorsing that outlook, stressing that rapidly evolving conditions make it unwise to pre-commit.

“We must keep our eyes and ears open for the risks to price stability,” he said, pointing specifically to current developments in the Middle East as a source of heightened uncertainty.

Nagel also offered a downbeat assessment of Germany’s near-term prospects, forecasting stagnation in Q2 and flagging the global trade war as a significant drag. He estimated that escalating trade tensions could shave as much as 0.75 percentage points off German growth over the medium term.

ECB’s de Guindos sees inflation risks balanced, Euro strength not a concern

In a Reuters interview, ECB Vice President Luis de Guindos downplayed concerns over a return to the ultra-low inflation era of the 2010s, despite the recent strengthening of Euro. De Guindos acknowledged that these developments could weigh on headline inflation but emphasized that “the risk of undershooting is very limited.” He maintained that inflation risks are now "balanced". Euro’s recent appreciation was neither rapid nor volatile, and therefore "not going to be a big obstacle" at 1.15 level.

De Guindos expressed confidence that inflation will rebound after dipping to 1.4% in Q1 2026, citing a still-tight labor market and sustained wage pressures. Compensation growth, supported by union demands, is expected to remain near 3%. This aligns with ECB’s medium-term outlook of returning inflation to its 2% target.

While stopping short of explicitly endorsing a pause, de Guindos indicated that market pricing for just one more rate cut, potentially later this year, was consistent with ECB President Christine Lagarde’s latest messaging.

“Markets have understood perfectly well what the President said about being in a good position,” he noted, adding that investors now correctly anticipate that the ECB is nearing the end of its easing cycle.

NZ BNZ services slumps to 44.0, economy returning to recession

New Zealand's services sector took a steep turn downward in May, with the BusinessNZ Performance of Services Index plunging from 48.1 to 44.0, the lowest reading since June 2024. Activity and new orders led the decline, falling from 46.7 and 50.2 to 40.1 and 43.2 respectively, as businesses reported broad-based weakness in demand. Employment also edged down from 47.9 to 47.2.

Sentiment on the ground paints an equally grim picture. Negative commentary from survey respondents rose to 65.6%, up from 61.8% in April. Businesses cited reduced consumer spending, revenue declines, and heightened uncertainty over inflation, interest rates, and the economic outlook. Many reported that customers are delaying decisions and becoming more cautious in their spending—mirroring trends typically seen during periods of economic stress.

BNZ Senior Economist Doug Steel noted that the PSI collapse closely follows the earlier fall in the Performance of Manufacturing Index, reinforcing signs of widespread economic fragility. With both key sectors now contracting, concerns are rising that New Zealand may be "returning to recession".

China's retail sales shine with 6.4% yoy growth, but production and investment drag continues

China’s latest economic data for May paints a mixed picture. Industrial production rose 5.8% yoy, falling short of the expected 6.0% and reflecting lingering weakness in external demand. This comes on the heels of a sharp -34.5% yoy drop in exports to the US, despite the mid-May rollback of some tariffs. The full impact of reduced tariffs is expected to emerge more clearly in June though.

In contrast, retail sales provided a bright spot, jumping 6.4% yoy and beating forecasts of 5.0% yoy. The rebound was supported by the government’s aggressive push to boost consumer spending through its appliance and vehicle trade-in program. The Ministry of Commerce reported that the campaign has already generated over CNY 1.1m in sales this year.

However, fixed asset investment remains a drag, growing only 3.7% ytd yoy versus expectations of 3.9%. The persistent weakness in property investment, down 10.7% in the first five months of the year, highlights ongoing strain in the real estate sector.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1491; (P) 1.1552; (R1) 1.1616; More...

Intraday bias in EUR/USD remains neutral and more consolidations could be seen below 1.1630 temporary top. Further rise is expected as long as 1.1372 support holds. Break of 1.1572 will extend the rally from 1.0176. Next target is 61.8% projection of 1.0176 to 1.1572 from 1.1064 at 1.1927. However, break of 1.1372 support will indicate short term topping, and turn bias to the downside for deeper pullback.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 1.1604 support holds.

Crypto Market Quickly Recovered from the Shock

Market Picture

The Crypto Market cap stood at $3.34 trillion on Monday morning, up 2% over the past 24 hours, confirming a rebound from the support line of recent weeks near $3.2 trillion. The crypto market is being actively bought up against the backdrop of positive dynamics in key global stock indices. It cannot be said that the world has awakened an appetite for risk, but there is no reason to talk about a sustained drive for safety yet.

Bitcoin is up 1.7%, lagging major altcoins such as Solana (+7.8%) and Ethereum (+4.1%) in terms of growth. After finding support on the decline in the $104K area, near which the 50-day moving average also passes, BTC confirmed its commitment to the upward trend. However, resistance at $110K proved too difficult for the bulls in May and early June. Will they manage to consolidate above the current momentum? We will find out this week.

Ethereum has gained 5% since the start of the day on Monday to $2,630, having been trying to break through the 200-day average for over a month. The best attempt during this time was last week, with an update of 4-month highs on 11 June. Over the weekend, we again saw active support on declines below $2,500. Paradoxically, the positive market sentiment is working in favour of bulls in cryptocurrencies.

News Background

Inflows into spot Bitcoin ETFs in the US resumed after two weeks of small outflows. According to SoSoValue, net inflows into spot BTC ETFs last week amounted to $1.37 billion, reaching $45.61 billion since Bitcoin ETFs were approved in January 2024.

Net inflows into spot Ethereum ETFs in the US rose to $528.1 million last week. Total net inflows since the ETF’s launch in July have risen to $3.85 billion.

The growing popularity of corporate reserves in Bitcoin poses a systemic risk to the crypto market, Coinbase notes. Already, 234 firms hold a total of 820,542 BTC. During periods of market stress, they may face the need for forced sales to cover liabilities and further depress the price.

Bitcoin mining difficulty has paused its growth, retreating slightly from its historic high of 129.98 T reached two weeks ago.

The e-commerce platform Shopify, in partnership with Coinbase and Stripe, has added the ability to accept payments in Circle’s USDC stablecoin.

Cardano founder Charles Hoskinson proposed allocating $100 million in ADA tokens from the project’s reserves to purchase Bitcoin and stablecoins to boost the DeFi segment of the network.

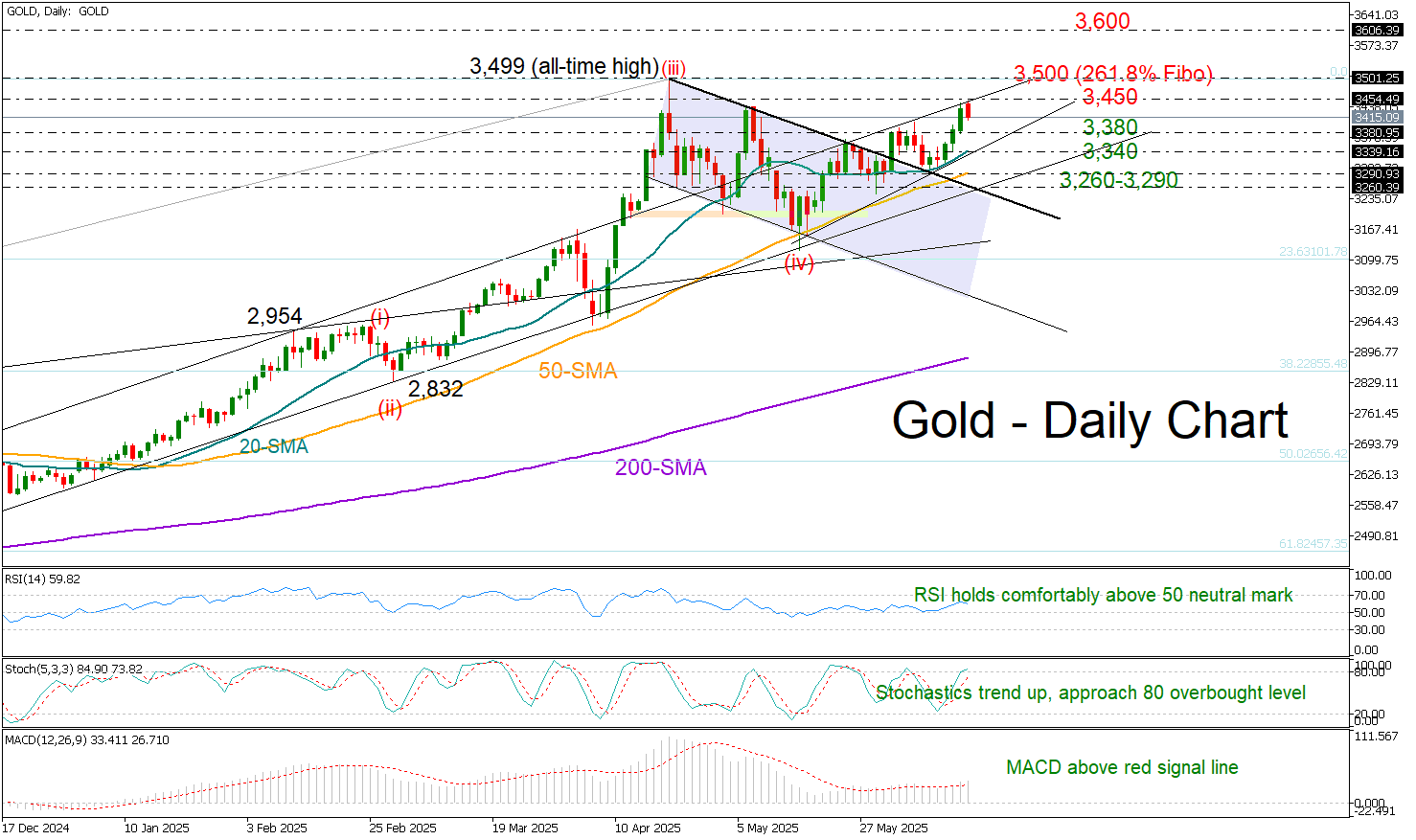

Will Gold Break into Uncharted Territory?

- Gold begins a new bullish cycle, tests May’s ceiling near 3,450.

- Technical signals favor the bulls, focus shifts to all-time highs.

Gold is once again flirting with its spring record-high area of 3,440–3,500, as the escalating Middle East conflict between Israel and Iran shifted funds towards the safe-haven precious metal.

From a technical perspective, the 20-day simple moving average (SMA) has halted selling pressure for the third consecutive week near 3,300, helping the price rally to as high as 3,450 today. With technical indicators trending positively, traders may anticipate further gains in the coming sessions. However, some caution is warranted, as the stochastic oscillator is approaching its 80 overbought threshold.

The 3,450 zone is currently serving as a key resistance level. A decisive breakout above it could lead to a test of the psychological 3,500 level, which almost capped April’s record rally. Beyond that, attention could turn to the 3,600 area, while a more aggressive rally might target the 161.8% Fibonacci extension of the April–May decline, near 3,735.

On the downside, failure to close above 3,450 may trigger a pullback toward 3,380, or even lower, to the 20-day SMA at 3,340. Further declines could encounter a stronger support region between 3,260 and 3,290; a break below this zone would jeopardize the current upward trend and potentially open the door for a deeper drop toward 3,200.

In summary, gold is attracting fresh buyers near the 3,450 resistance area. A strong close above this level is needed to open the path toward uncharted territory.

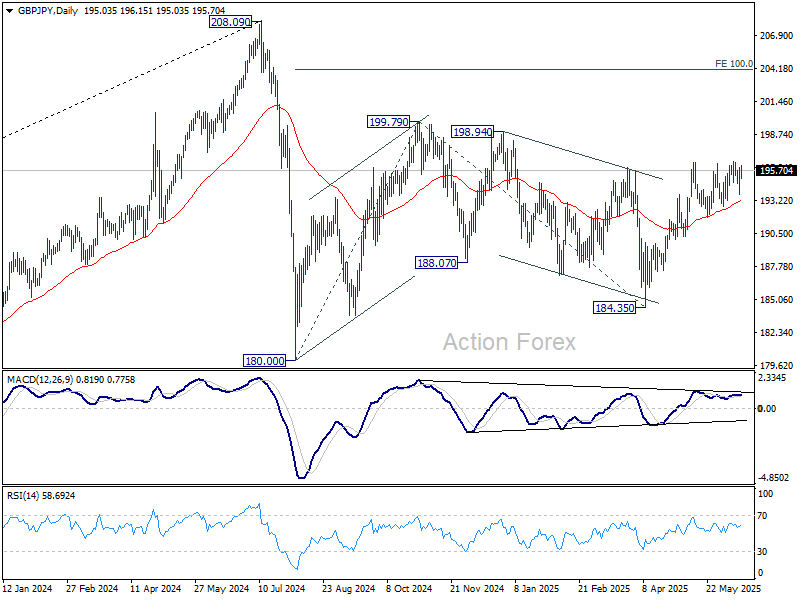

GBP/JPY Daily Outlook

Daily Pivots: (S1) 194.26; (P) 195.12; (R1) 196.47; More...

GBP/JPY is still extending consolidation from 196.38 and intraday bias remains neutral. Further rise is expected with 191.86 support intact. Firm break of 196.38 will resume whole rally from 184.35 to 199.79 resistance, and possibly further to 100% projection of 180.00 to 199.79 from 184.35 at 204.14.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 175.94 will bring deeper fall even still as a correction.

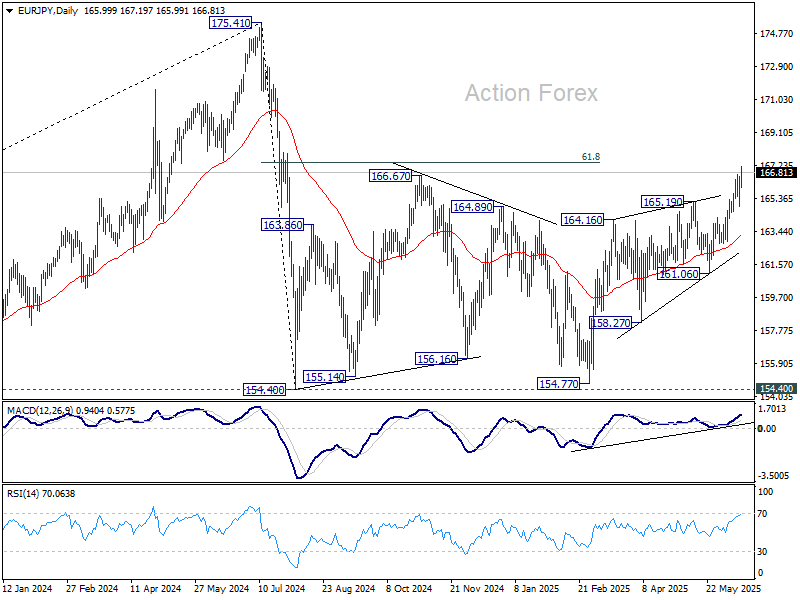

EUR/JPY Daily Outlook

Daily Pivots: (S1) 165.35; (P) 165.97; (R1) 167.02; More...

EUR/JPY's rally resumed by breaking through 166.73 temporary top and intraday bias is back on the upside. Current is part of the rally from 154.77, and should target 61.8% retracement of 175.41 to 154.77 at 167.38. For now, further rally is expected as long as 164.91 support holds, in case of retreat.

In the bigger picture, price actions from 175.41 are seen as correction to up trend from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.