Sample Category Title

Sell-Off in US Stocks Hit Short-Term Oversold Conditions, Relief Corrective Bounce Seen in Futures, Gold Extended Gains

US stocks slumped. All four major US stock indices ended Monday, 21 April session, deeply in the red. The S&P 500, Nasdaq 100, Dow Jones Industrial Average, and Russell 2000 lost 2% or more.

The 'US exceptionalism' narrative is under threat as US equities, the dollar, and Treasuries are being sold off simultaneously. Notably, over the past four weeks, the dollar and Treasuries have failed to act as traditional safe havens during periods of risk-off sentiment, instead behaving more like emerging market assets.

The current rout seen in the US dollar has wiped out all of last year’s gains seen in the US Dollar Index. The US dollar tanked to a 10-year low against the Swiss franc yesterday, and the euro climbed to an intraday high of 1.1573 against the US dollar, its highest level since November 2021.

The continuation of US President Trump’s threats to remove Fed Chair Powell and the growth uncertainties arising from US trade tariffs, coupled with retaliation measures, have benefited Gold.

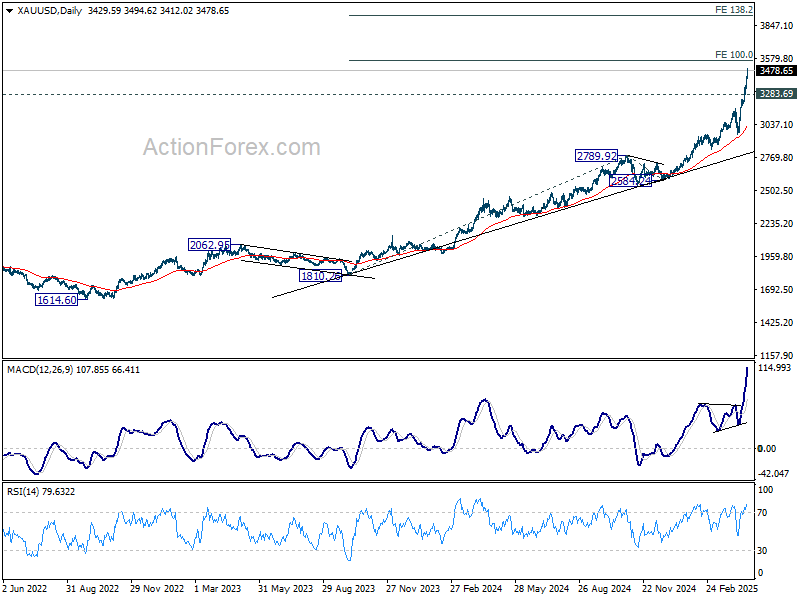

Gold (XAU/USD) surged to another fresh record yesterday with a gain of 2.9%. In today’s Asia opening session, it extended its rally by 0.7% and printed a new intraday all-time high of US$3,453 at this time of writing.

Reuters, according to a source, reported that the Bank of Japan (BoJ) is likely to keep its interest rate hike signal intact despite Trump tariff risks after the conclusion of its upcoming two-day monetary policy decision meeting, ending 1 May.

In addition, the source, as quoted by Reuters, stated that BOJ is likely to downgrade Japan's current fiscal 2025 economic growth forecast of 1.1% in its updated quarterly report release on 1 May.

After the conclusion of the first round of US-Japan trade talks last week, Japanese Prime Minister Ishiba told parliament yesterday, 21 April, that Japan will not concede to all US demands, citing the need to protect national interests, especially in the automobile and agricultural sectors.

Hence, the second round of trade negotiation talks between the US and Japan to be held before the end of April may not be smooth sailing.

After the sell-off seen in major US stock indices yesterday that led to short-term oversold conditions on several technical momentum indicators, the S&P 500 and Nasdaq 100 E-mini futures have managed to stage a relief corrective rebound of 0.7% each in today’s Asian opening session at this time of the writing.

The Hong Kong stock market reopened after a two-day Easter break, playing catch-up to global weakness. The Hang Seng Index is down 0.7% intraday.

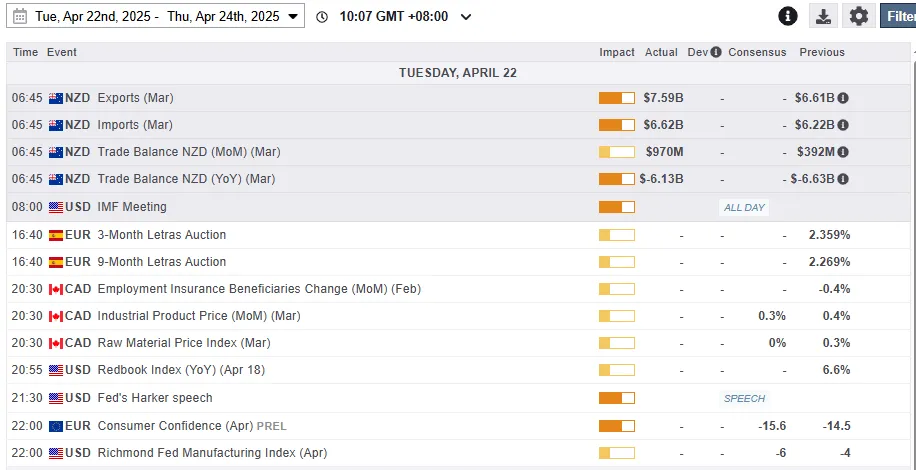

Economic data releases

Fig 1: Key data for today’s Asian mid-session (Source: MarketPulse)

Chart of the day – Hong Kong 33 at risk of further downside to retest 200-day MA

Fig 2: Hong Kong 33 CFD Index minor trend as of 22 Apr 2025 (Source: Trading View)

Since its recent minor swing high of 21,668 printed on 14 April, the short-term technical conditions of the Hong Kong 33 CFD Index (a proxy of the Hang Seng Index futures) have deteriorated.

The latest observations seen on its hourly RSI momentum indicator have just flashed out a bearish momentum condition at this time of writing below the 50 level.

All in all, the Hong Kong 33 CFD Index may see a multi-day decline to retest its 200-day moving average. Watch the 21,450 key short-term pivotal resistance, and a break below 20,840 near-term support may expose the next intermediate supports at 20,280 and 19,900 (200-day moving average).

On the other hand, a clearance above 21,450 invalidates the bearish tone to see a squeeze up for the next intermediate resistances to come in at 21,740 and 22,220/22,500 (also the area between the 20-day, and 50-day moving averages).

Trade Uncertainty Continues to Weigh on Markets

In focus today

Today will be light on the macro front, with markets continuing to closely watch trade uncertainty and any signals from Trump.

In the euro area, focus turns to the consumer confidence indicator for April. Consumer confidence has declined in the past months following a great rebound last year, and the trade war uncertainty in April has likely amplified the development.

In Sweden, the latest unemployment figures will be released today at 8:00 CET. The concerning trend observed in recent months may persist due to significant uncertainties faced by companies, which likely suppress their willingness to hire. Although we anticipate a decline in unemployment towards the end of the year, it may take a few more months to be certain that we have surpassed the peak levels.

For the remainder of the week, the most important data releases are the PMI reports for April, scheduled for release on Wednesday. As the surveys were conducted after Liberation Day, the figures are likely to provide a first glimpse of the impact from tariff uncertainty. Importantly, any progress in the tariff saga - particularly in US-China trade negotiations - and shifts in global investor sentiment will continue to influence markets this week.

Economic and market news

What happened during Easter

In the US, retail sales growth in March (ahead of Liberation Day) remained solid, printing close to expectations at 1.4% (cons: 1.3%, prior: 0.2%). Lower gasoline prices dragged on the headline, while car sales edged up. While tariff concerns likely impacted some categories, sales growth in bars and restaurants — often a good measure of discretionary spending and not affected by tariffs — gained some momentum from February. Overall, the release suggests that the very gloomy consumer sentiment readings have yet to translate into hard data as negatively as some had feared.

The Philly Fed's manufacturing index weakened markedly in April, with new orders slumping to -34.2 from 8.7 in March. Hence, there are signs that PMIs for April will deteriorate in the first reading after Liberation Day.

During Easter, several Fed speakers were on the wire. Fed Chair Powell (hawk and voting member) emphasized that the Fed remains in a wait-and-see mode. Similarly, NY Fed President Williams (hawk and voting member) said that he does not see an imminent need for a change in monetary policy. Chicago Fed President Goolsbee (neutral and voting member) stated that he hopes the US is not moving toward an environment where the Fed's monetary policy independence is questioned, following Trump's recent attacks on Powell. Considering the upcoming week for the Fed, focus will naturally be on Trump's outbursts toward Powell, but attention will also be on several Fed officials scheduled to speak before the blackout period begins on Saturday.

In the euro area, the ECB cut policy rates by 25bp, bringing the deposit rate to 2.25%, as widely anticipated. Overall, the meeting was in line with our expectations, with the ECB conveying a dovish tone - noting the downside risks to growth, while downplaying the topside risks to inflation. Markets reacted by sending European yields lower on the statement, with further declines during the press conference. EUR/USD moved initially lower, but the weak Philly Fed reading provided some support for the cross. Looking ahead, we continue to expect the ECB to deliver 25bp cuts at the upcoming meetings, bringing the deposit rate to 1.50% by September 2025. We currently see downside risks to growth, inflation and rates in the medium term. For more detail on our assessment of the ECB meeting, please see ECB review - Dovish bias in troubled waters, 17 April.

In China, the 1Y loan prime rate and the 5Y loan prime rate were held unchanged at 3.10% and 3.60%, respectively.

Turning to politics, China has accused the US of abusing tariffs and warned other countries against striking deals with the US at China's expense. The remarks come after a Bloomberg article, citing sources familiar with the matter, reported that the Trump administration is preparing to pressure nations seeking tariff reductions or exemptions from the US to curb trade with China - including through the imposition of monetary sanctions. For more detail on how we currently see China's footing in the trade war, please see Postcard from China - 10 key takeaways from trip to China, 16 April.

In the UK, March inflation was lower than expected across the board, with headline at 2.6% y/y (cons: 2.7%, prior: 2.8%), core at 3.4% (cons: 3.4%, prior: 3.5%) and services at 4.7% (cons: 4.8%, prior: 5.0%). The largest downward contribution came from recreation and culture and transport, while clothing provided the largest upward contribution. The monthly momentum eased in services and in core services, which is the key measure for the BoE. With UK inflation surprising to the downside over the past months we think the BoE is set to continue easing, delivering its next 25bp cut at the upcoming meeting in May.

In Denmark, Danmarks Nationalbank followed the ECB, cutting its key policy rate 25bp to 1.85%.

In Canada, the BoC held its policy rate at 2.75%, as expected by markets. The BoC emphasized that monetary policy cannot fix trade uncertainty and reaffirmed its 2% inflation target. The MPR included two scenarios: one with normal trade, showing modest growth and steady inflation, and another with a prolonged trade war, forecasting recession and inflation above 3% next year. The neutral rate estimate was kept unchanged at 2.25-3.25%. Markets now lean toward a June cut, suggesting the BoC is pausing, not ending, its easing cycle amid tariff-related uncertainty.

In Japan, the nationwide inflation report for March, saw core CPI rise 3.2% y/y from 3.0%, in line with expectations. Excluding fresh food and fuel costs, the index increased 2.9% y/y from 2.0%. Governor Ueda was on the wire, reiterating that the BoJ will continue to raise interest rates if underlying inflation pressures continue to accelerate toward 2%. That said, Ueda also signalled a naturally cautious and flexible approach amid the uncertainty stemming from Trump's potential tariffs. We continue to expect the BoJ to normalize policy further, delivering additional rate hikes this year.

In Turkey, the CBT surprised markets hiking its policy rate by 350bp to 46%.

In commodities space, easing supply concerns tied to potential progress in US-Iran nuclear talks pushed oil prices down over 2% during yesterday's session. As of this morning brent is trading around 67 USD/bbl.

Gold prices continued its record high rally this morning, hovering around USD3488 per troy, driven by investors seeking safe-haven assets.

Equities: Looking at equity markets over Easter - a period with more public holidays in Europe than in the US - the overall direction has been lower. Over the past five trading days, US equities have fallen by a little more than 4%, while European equities are marginally higher. That said, US futures are pointing higher this morning, whereas European futures are slightly in the red. In terms of cyclicals versus defensives, the risk-off sentiment has been most pronounced in the US, with cyclicals down more than 5%, while defensives are down around 2%. Europe shows a similar but more muted trend, with modest defensive outperformance. In the US yesterday, the Dow declined by 2.5%, the S&P 500 by 2.4%, the Nasdaq by 2.6%, and the Russell 2000 by 2.1%. With yesterday's moves, the VIX is now back at 33 - a clear reflection of the current environment, where uncertainty is weighing on equities more than hard macro data. Year-to-date, European equities have outperformed US equities by nearly 15% when measured in local currency. However, the recent EUR/USD appreciation adds another ~12% headwind for investors who have not hedged the dollar, making U.S. equity exposure particularly challenging this year. This morning, Asian equities are trading higher, while European futures are lower, and US futures are marginally up.

FI & FX: USD continues to weaken on the back of the economic and political uncertainty in US as well as recent comment from Trump regarding Fed Chairman Powell and the need for "pre-emptive rate cuts" from the Federal Reserve. Short-end rates in the US have fallen since last week, but the long-end continues to rise in a steepening move. Following a dovish ECB meeting with a widely anticipated 25bp rate cut, European rates have rallied, which helped the SEK perform against EUR last Thursday, however, the negative international turmoil has caught up with the SEK and will likely push EURSEK levels back towards our post ECB-decision near-term fair-value assessment of 11.

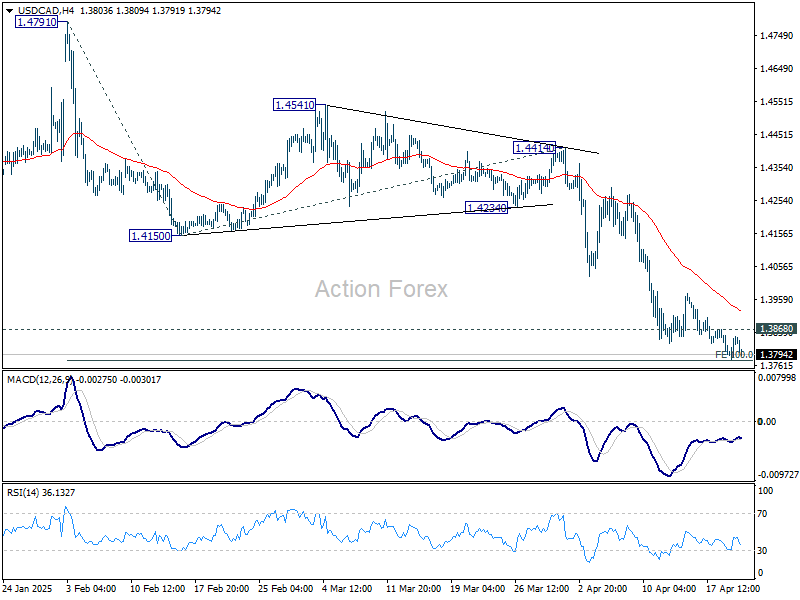

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3798; (P) 1.3825; (R1) 1.3868; More...

Intraday bias in USD/CAD remains on the downside. Firm break of 100% projection of 1.4791 to 1.4150 from 1.4414 at 1.3773 will extend the decline from 1.4791 to 138.2% projection at 1.3528. On the upside, above 1.3868 minor resistance will turn intraday bias neutral again first.

In the bigger picture, the break of 1.3976 resistance turned support (2022 high) and 55 W EMA (now at 1.3982) indicates that a medium term top is already in place at 1.4791. Fall from there would either be a correction to rise from 1.2005, or trend reversal. In either case, firm break of 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727 will pave the way back to 61.8% retracement at 1.3069.

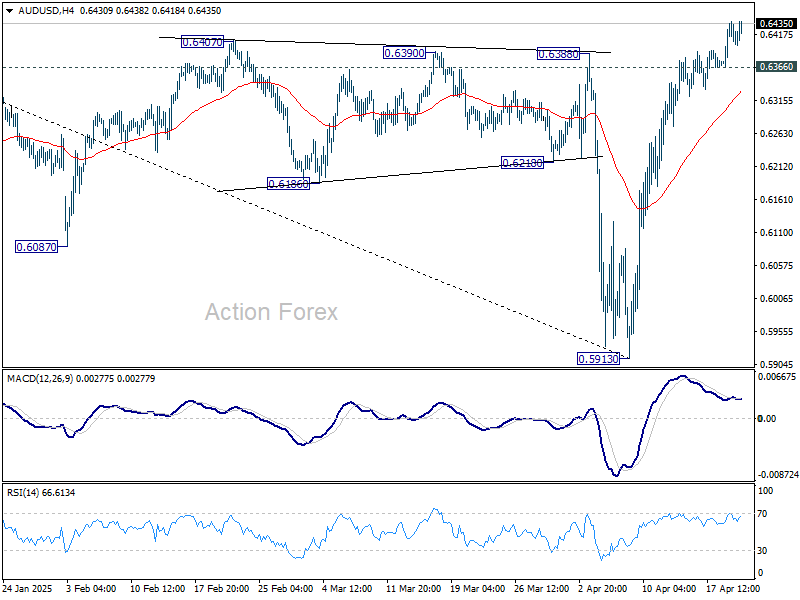

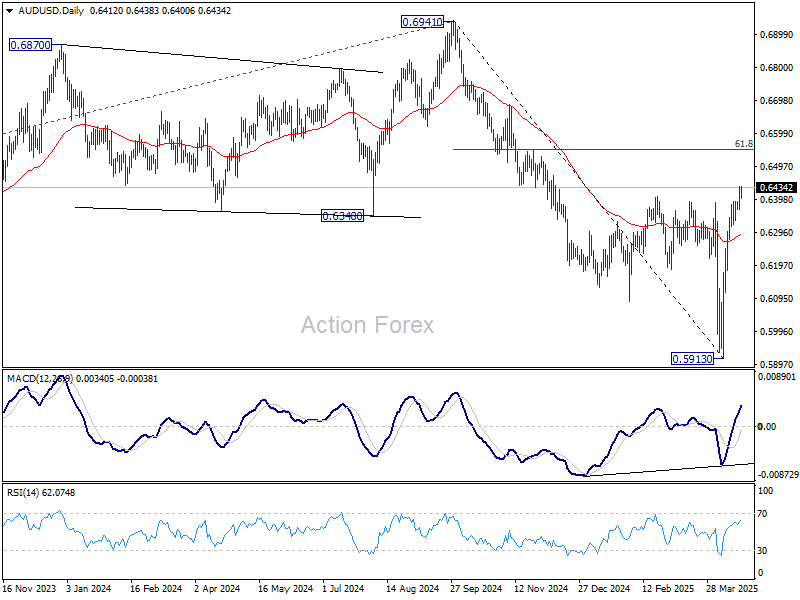

AUD/USD Daily Report

Daily Pivots: (S1) 0.6379; (P) 0.6408; (R1) 0.6447; More...

Intraday bias in AUD/USD remains on the upside for the moment. Current rise from 0.5913 should target 61.8% retracement of 0.6941 to 0.5913 at 0.6548, even still as a corrective move. On the downside, below 0.6356 minor support will turn intraday bias neutral again first.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. However, sustained trading above 55 W EMA (now at 0.6443) will argue that a medium term bottom was already formed, and set up further rebound to 0.6941 resistance instead.

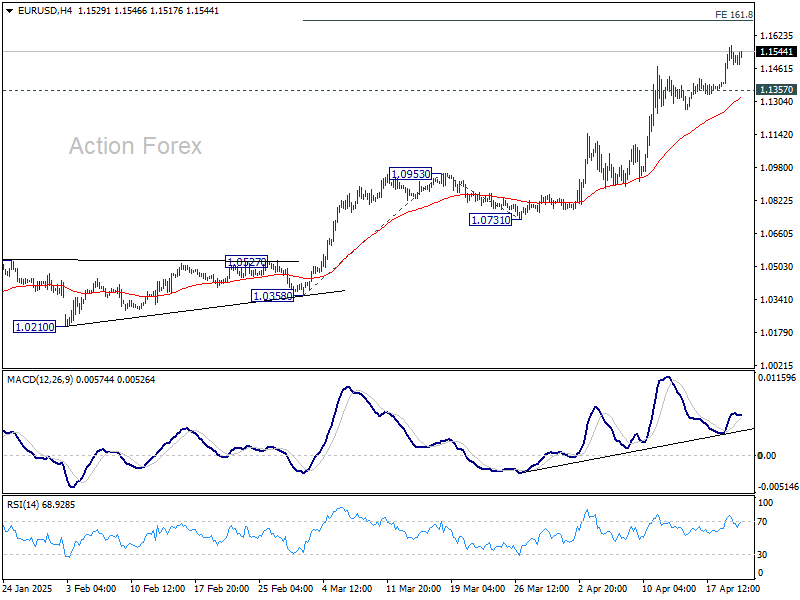

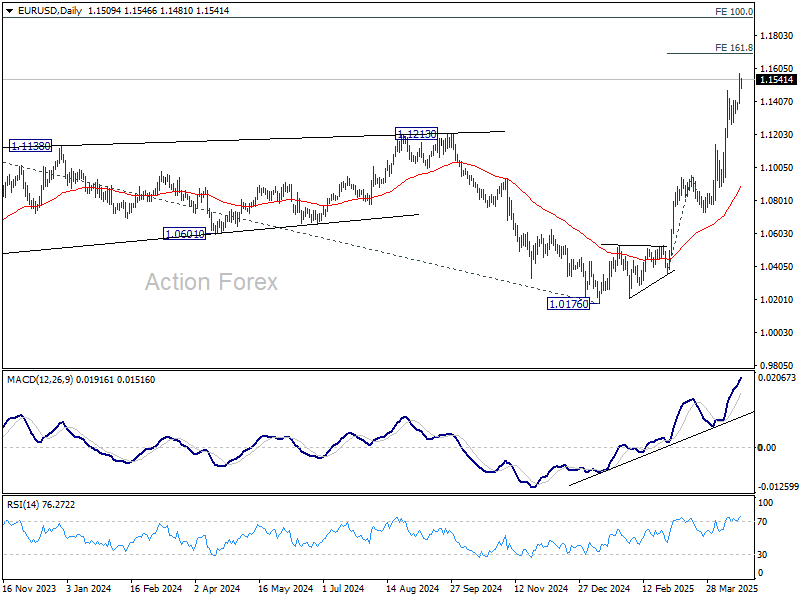

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1414; (P) 1.1494; (R1) 1.1592; More...

Intraday bias in EUR/USD remains on the upside for the moment. Current rise from 1.0176 should target 161.8% projection of 1.0358 to 1.0953 from 1.0731 at 1.1694 next. On the downside, below 1.1357 minor support will turn intraday bias neutral and bring consolidations again, before staging another rally.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0776) holds.

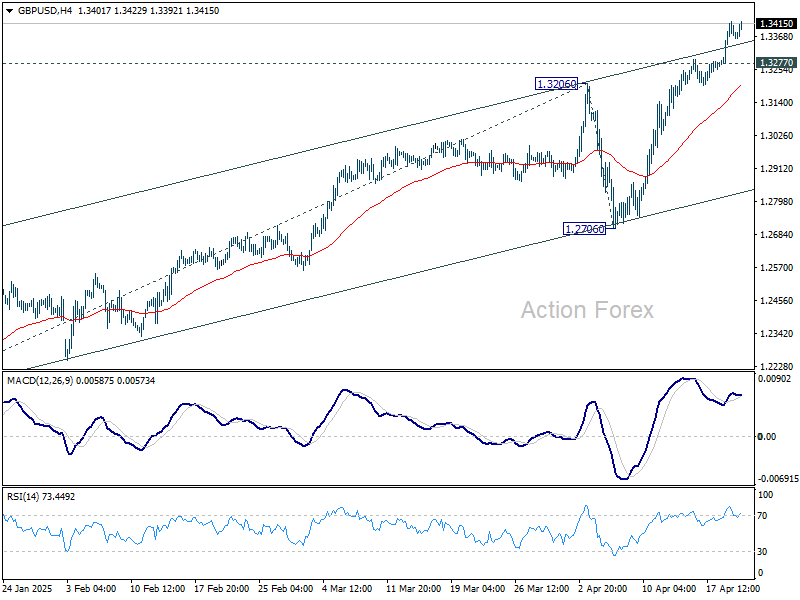

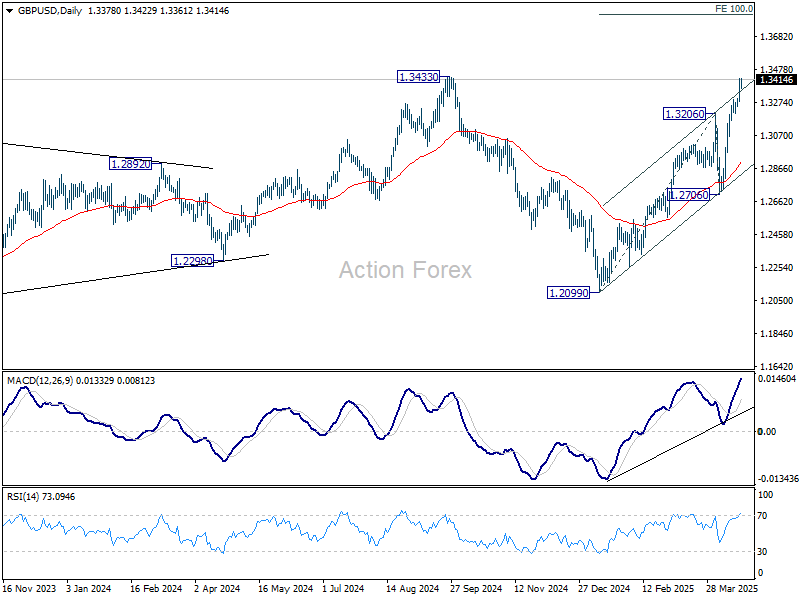

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3297; (P) 1.3359; (R1) 1.3444; More...

Intraday bias in GBP/USD remains on the upside for retesting 1.3433 high. Firm break there will confirm larger up trend resumption and target 100% projection of 1.2099 to 1.3206 from 1.2706 at 1.3813. On the downside, below 1.3277 minor support will turn intraday bias neutral again first.

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could be the second leg. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on break of 1.3433 at a later stage.

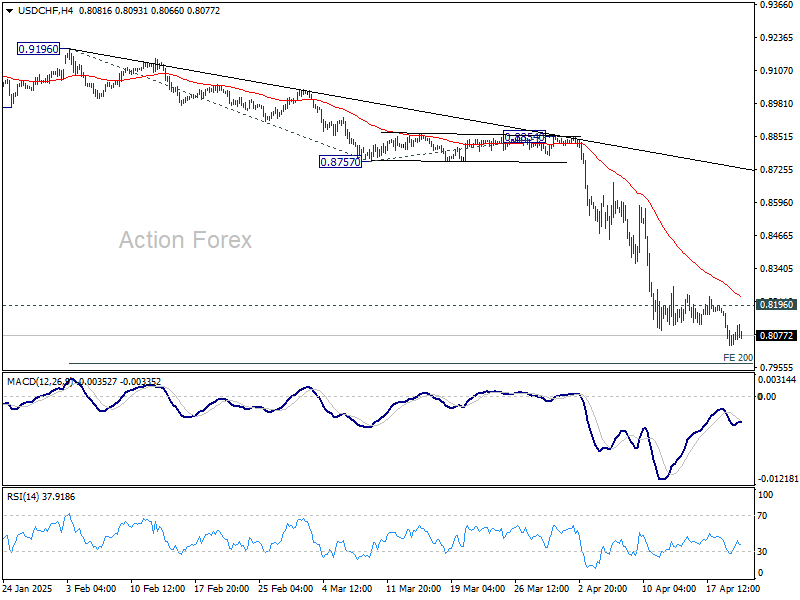

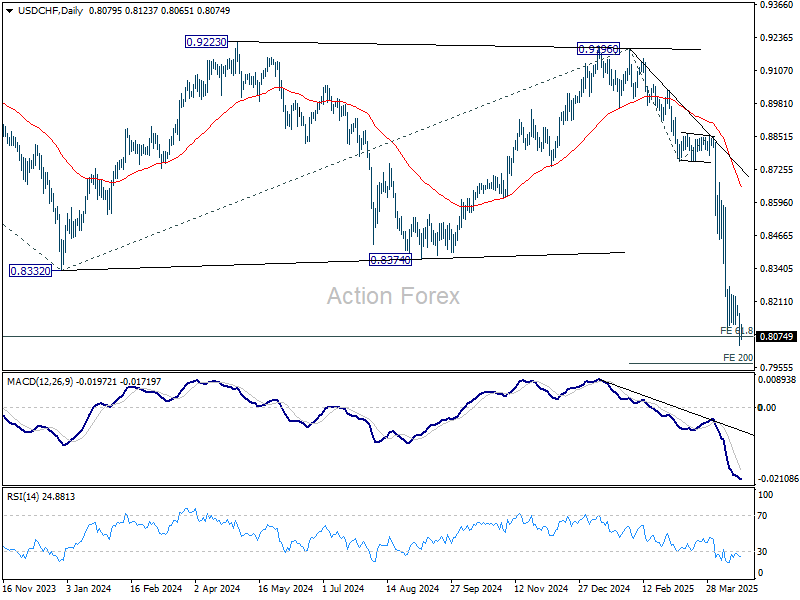

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8026; (P) 0.8104; (R1) 0.8169; More…

Intraday bias in USD/CHF remains on the downside for the moment. Current down trend should target 200% projection of 0.9196 to 0.8757 from 0.8854 at 0.7976 next. On the upside, above 0.8196 minor resistance will turn intraday bias neutral and bring consolidations again first.

In the bigger picture, the break of 0.8332 (2023 low) confirms resumption of long term down trend from 1.0342 (2017 high). Next target is 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9196 at 0.8075. Firm break there will target 100% projection at 0.7382. In any case, outlook will now stay bearish as long as 55 W EMA (now at 0.8794) holds.

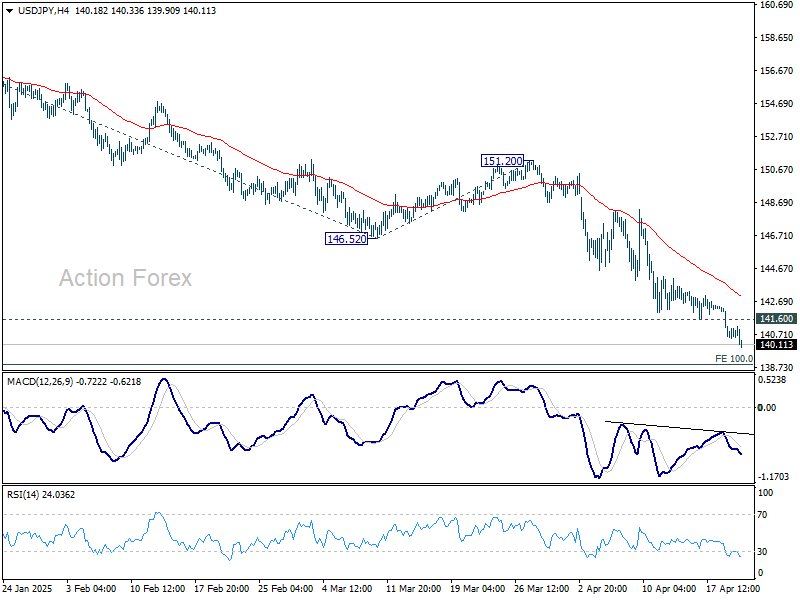

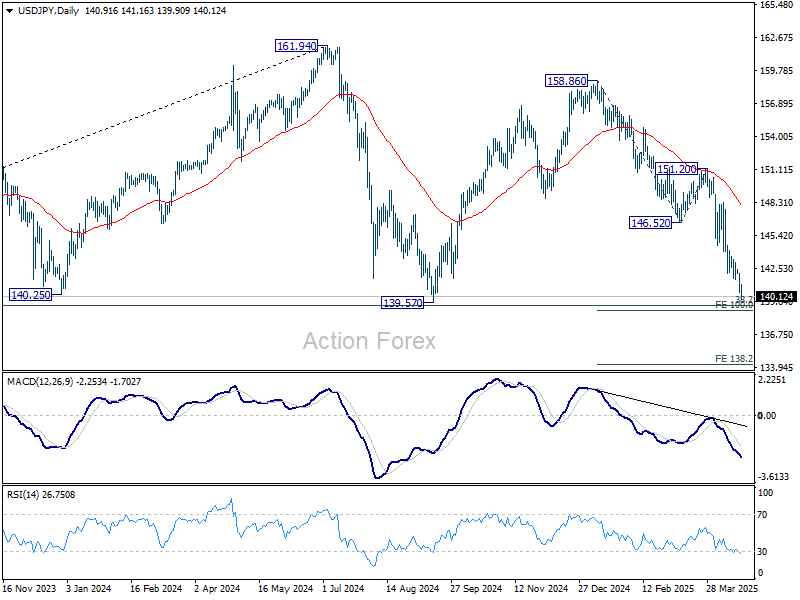

USD/JPY Daily Outlook

Daily Pivots: (S1) 140.18; (P) 141.16; (R1) 141.85; More...

Intraday bias in USD/JPY remains on the downside for the moment. Current fall from 158.86 is in progress for 139.57 support. Strong support could seen from 139.26 fibonacci level to bring rebound. On the upside, above 141.60 minor resistance will turn intraday bias neutral first. However, decisive break of 139.26 will carry larger bearish implications, and target 138.2% projection of 158.86 to 146.52 from 151.20 at 134.14.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Dollar Rout Deepens; Gold Charges Toward 3500, or Even 4000?

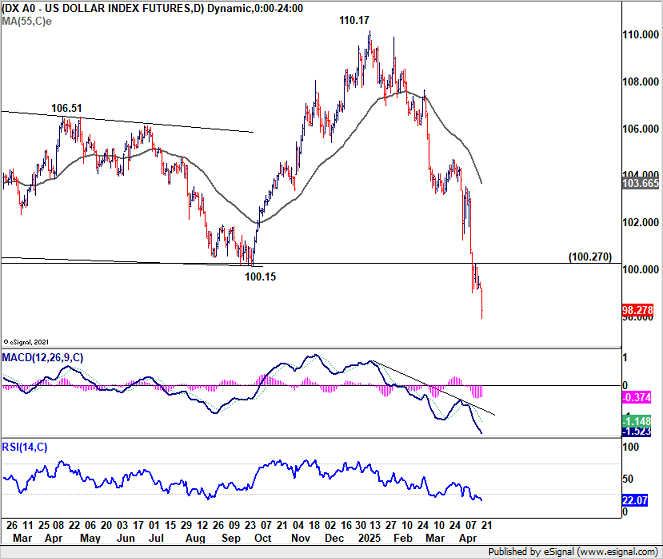

The broad selloff in US assets resumed overnight as market confidence took another blow from escalating political pressure on Fed. Major US stock indexes ended the session deep in the red, while 10-year Treasury yields surged back above 4.4%. The Dollar Index also plunged to a fresh three-year low, continuing its dramatic collapse.

The key catalyst: another public attack by US President Donald Trump, who took to Truth Social to call Fed Chair Jerome Powell a “major loser” and demanded that interest rates be cut “NOW” to avoid a economic slowdown. Trump’s renewed rhetoric has intensified concerns about Fed’s independence at a time of high uncertainty due to his own tariff policies.

The central bank has so far resisted political pressure, and more Fed officials are set to speak today. Markets expect them to defend the institution’s autonomy and reaffirm their data-dependent approach. Given the current policy fog, particularly surrounding Trump’s shifting trade stance, officials are likely to emphasize the need for further clarity before making any policy adjustments.

Meanwhile, the 90-day truce on Trump’s “reciprocal tariffs” continues with little meaningful progress in negotiations. Even talks with Japan, one of America's closest allies, remain stalled. Japanese Prime Minister Shigeru Ishiba stated on Monday that substance matters more than speed in any trade agreement. Additionally, Ishiba vowing not to concede on core issues such as car safety standards and agricultural access. Finance Minister Katsunobu Kato is expected to travel to Washington later this week for discussions with US Treasury Secretary Scott Bessent, with currency issues on the agenda.

Tensions with China continue to escalate. The Chinese Ministry of Commerce issued a sharp warning that Beijing will retaliate against any countries that cooperate with the US in ways that undermine China’s interests. China's message reinforces the view that global trade friction is far from resolved, despite temporary pauses.

Against this backdrop, Gold continues to surge as investors flee to safety. The precious metal’s record-breaking rally shows no signs of slowing, with momentum firmly in upside acceleration.

Technically, further rise is expected as long as 3283.69 support holds. Next target is 100% projection of 1810.26 to 2789.92 from 2584.24 at 3563.90. Firm break there will pave the way to 138.2% projection at 3938.13, which is close to 4000 psychological level.

Overall in the currency markets, Dollar is currently the worst performer by a mild, followed by Loonie and then Sterling. Yen is the strongest one, followed by Kiwi and then Euro. Swiss Franc and Aussie are positioning in the middle.

In Asia, at the time of writing, Nikkei is down -0.07%. Hong Kong HSI is up 0.20%. China Shanghai SSE is up 0.38%. Singapore Strait Times is up 0.90%. Japan 10-year JGB yield is up 0.023 at 1.312. Overnight, DOW fell -2.48%. S&P 500 fell -2.36%. NASDAQ fell -2.55%. 10-year yield rose 0.072 to 4.405.

Dollar Index crashes to 3-year low; 95 support holds long-term fate

Dollar Index broke through an important support overnight as recent decline accelerated, and hit the lowest level in three years. The selloff reflects a deepening flight out of US assets, as confidence continues to erode. A major driver of the decline has been US President Donald Trump’s ongoing public attacks on Fed, which have increasingly undermined perceptions of central bank independence and rattled investor trust in US policy credibility.

Technically, the break of 99.57 (2023 low) confirms resumption of the downtrend from 114.77 (2022 high). Near term outlook will now stay bearish as long as 100.27 resistance holds. Next target is 100% projection of 114.77 to 99.57 from 110.17 at 94.97.

This support zone around 95 psychological level is especially significant, as it aligns with the long term rising channel support that dates back to 2011.

Decisive break of 95 ahead could firstly trigger further medium term downside acceleration. More importantly, that could also mark the end of the broader uptrend that began from 2008 low at 70.69.

Such a structural breakdown would open the door for sustained weakness with medium-term downside targets around the 89.20–90.00 range, with risk of entering a new secular downtrend in the years ahead.

New Zealand posts surprise NZD 970m trade surplus as exports surge 19%

New Zealand recorded stronger-than-expected trade surplus of NZD 970m in March, far exceeding forecasts of NZD 80m. The surprise was driven by a robust 19% yoy increase in goods exports, which rose by NZD 1.2B to NZD 7.6B. Imports also grew, up 12% yoy to NZD 6.6B.

Export performance was particularly strong across key trading partners. Shipments to China rose by NZD 371m (23% yoy), while exports to the US and the EU grew by 22% yoy and 51% yoy respectively. Exports to Japan also increased 11% yoy, although shipments to Australia dipped slightly, down -0.47% yoy.

On the import side, the largest increases came from the US, with a 48% yoy jump worth NZD 243m. This was followed by China and the EU, which posted 14% yoy and 19% yoy gains respectively. Imports from South Korea bucked the trend, falling -12% yoy.

USD/JPY Daily Outlook

Daily Pivots: (S1) 140.18; (P) 141.16; (R1) 141.85; More...

Intraday bias in USD/JPY remains on the downside for the moment. Current fall from 158.86 is in progress for 139.57 support. Strong support could seen from 139.26 fibonacci level to bring rebound. On the upside, above 141.60 minor resistance will turn intraday bias neutral first. However, decisive break of 139.26 will carry larger bearish implications, and target 138.2% projection of 158.86 to 146.52 from 151.20 at 134.14.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Dollar Index crashes to 3-year low; 95 support holds long-term fate

Dollar Index broke through an important support overnight as recent decline accelerated, and hit the lowest level in three years. The selloff reflects a deepening flight out of US assets, as confidence continues to erode. A major driver of the decline has been US President Donald Trump’s ongoing public attacks on Fed, which have increasingly undermined perceptions of central bank independence and rattled investor trust in US policy credibility.

Technically, the break of 99.57 (2023 low) confirms resumption of the downtrend from 114.77 (2022 high). Near term outlook will now stay bearish as long as 100.27 resistance holds. Next target is 100% projection of 114.77 to 99.57 from 110.17 at 94.97.

This support zone around 95 psychological level is especially significant, as it aligns with the long term rising channel support that dates back to 2011.

Decisive break of 95 ahead could firstly trigger further medium term downside acceleration. More importantly, that could also mark the end of the broader uptrend that began from 2008 low at 70.69.

Such a structural breakdown would open the door for sustained weakness with medium-term downside targets around the 89.20–90.00 range, with risk of entering a new secular downtrend in the years ahead.