Sample Category Title

Risk-Off Coupled With Renewed US Dollar Weakness as Trump Reasserts Threat to Remove Fed Chair Powell

In today’s Asian session, 21 April, the US dollar tumbled in line with intraday weakness seen in the US stock indices futures after the markets reopened from the Good Friday holiday break.

The US Federal Reserve’s independence has come under renewed threat from US President Trump again, when over the weekend it was reported that the US White House Administration has continued to evaluate the available options to seek a removal of Fed Chair Powell before his tenure ends in 2026.

The Japanese yen strengthened to a level last seen in September last year, where the USD/JPY shed -1% coupled with the EUR/USD rallying by 1.1% to hold at a 3-year high. In addition, the S&P 500 and Nasdaq 100 E-min futures declined by -0.9% each, respectively at this time of this writing.

Japan’s Nikkei 225 snapped its prior two sessions of gains with an intraday loss of 1.1% while the Hong Kong stock market remained shut for the Easter Monday holiday.

These observations suggest that market participants on the aggregate are questioning the US White House administration's current policies that may erode the confidence of holding US assets, and such a lack of confidence may amplify if the long-held independence of the Fed in terms of conducting monetary policy is removed.

Overall, the threat to the Fed’s independence had a greater market impact than the ECB’s dovish tone following its rate cut decision last Thursday, 17 April."

The yellow metal has continued to thrive in such uncertain times, where Gold (XAU/USD) added on to its gains with an intraday rally of 1.6% that saw another fresh all-time intraday high of $3,385 in today’s Asian session.

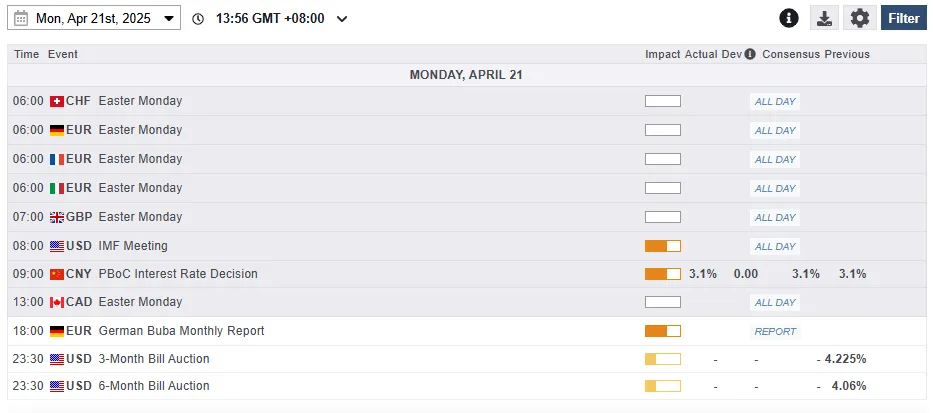

Economic data releases

Fig 1: Key data for today’s Asian mid-session (Source: MarketPulse)

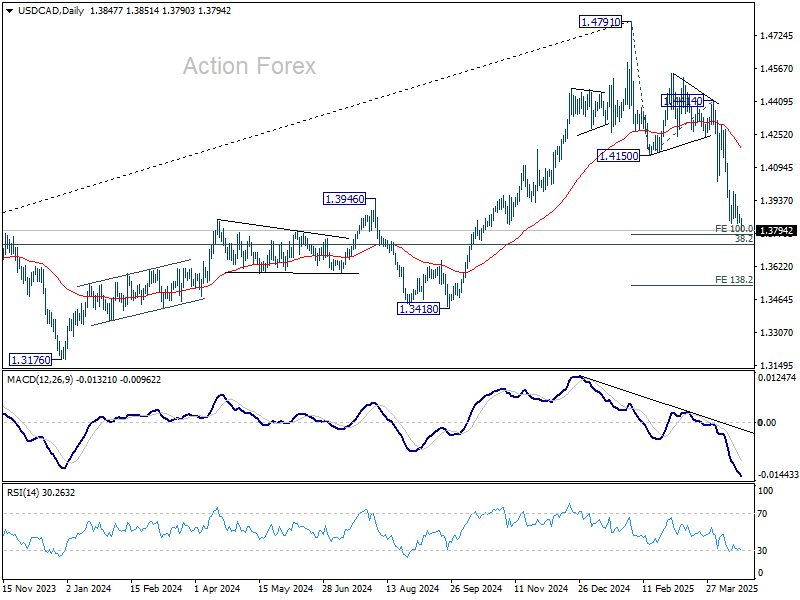

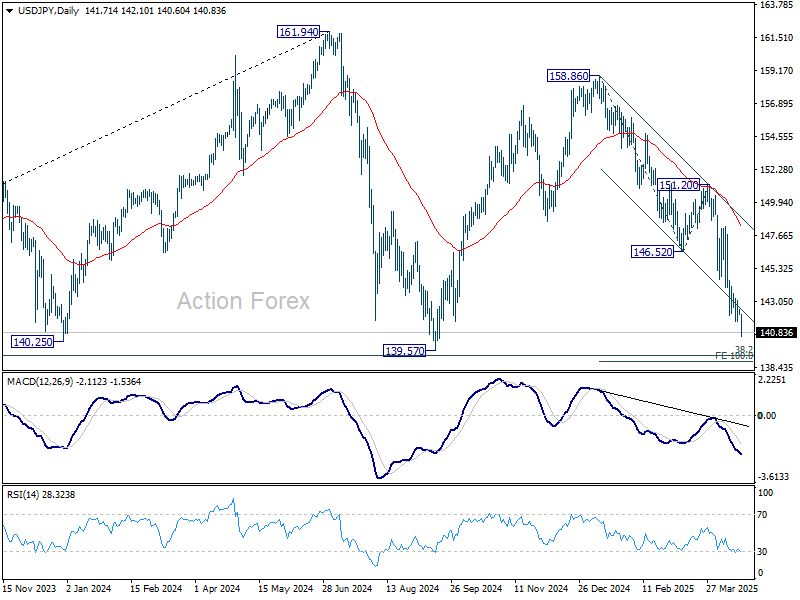

Chart of the day – Potential deceleration of USD/JPY after minor bounce

Fig 2: USD/JPY minor trend as of 21 Apr 2025 (Source: Trading View)

The USD/JPY has continued to plunge after its bearish breakdown from its “Pennant” configuration (considered as a minor consolidation within its ongoing medium-term downtrend phase) on last Wednesday, 16 April.

The hourly RSI momentum indicator has hit an extreme oversold reading of 8.2, its lowest level in the past four months, which suggests that USD/JPY may see an imminent minor corrective bounce before another leg of impulsive down move resurfaces.

Potential minor corrective bounce intermediate resistance to watch will be at 141.74 (former minor swing low of 17 April), and if the 142.70 short-term pivotal resistance is not surpassed to the upside, the USD/JPY may face renewed potential downside pressure to expose the next intermediate supports at 140.30/140.00 and 139.00/138.70.

On the flip side, a clearance above 142.70 invalidates the bearish tone to kickstart a potential mean reversion rebound sequence for the next intermediate resistances to come in at 144.10 and 145.10.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3832; (P) 1.3850; (R1) 1.3869; More...

USD/CAD's fall resumed by breaking through 1.3827 and intraday bias is back on the downside. Firm break of 100% projection of 1.4791 to 1.4150 from 1.4414 at 1.3773 will extend the decline from 1.4791 to 138.2% projection at 1.3528. On the upside, above 1.3868 minor resistance will turn intraday bias neutral again first.

In the bigger picture, the break of 1.3976 resistance turned support (2022 high) and 55 W EMA (now at 1.3982) indicates that a medium term top is already in place at 1.4791. Fall from there would either be a correction to rise from 1.2005, or trend reversal. In either case, firm break of 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727 will pave the way back to 61.8% retracement at 1.3069.

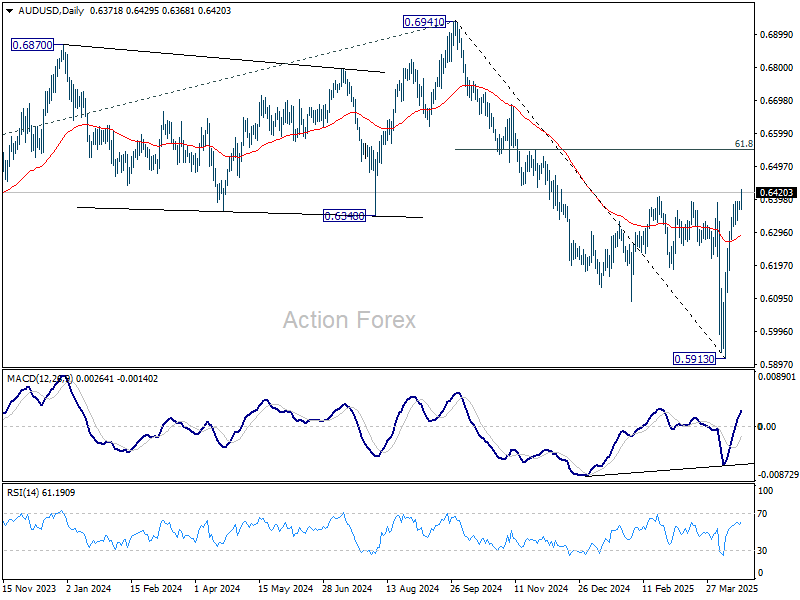

AUD/USD Daily Report

Daily Pivots: (S1) 0.6365; (P) 0.6379; (R1) 0.6391; More...

AUD/USD's rally resumed after brief consolidations and intraday bias is back on the upside. Current rise from 0.5913 should target 61.8% retracement of 0.6941 to 0.5913 at 0.6548, even still as a corrective move. On the downside, below 0.6356 minor support will turn intraday bias neutral again first.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. However, sustained trading above 55 W EMA (now at 0.6443) will argue that a medium term bottom was already formed, and set up further rebound to 0.6941 resistance instead.

USD/JPY Daily Outlook

Daily Pivots: (S1) 141.93; (P) 142.24; (R1) 142.47; More...

USD/JPY's decline continues today and intraday bias stays on the downside. Break of near term falling channel suggest downside acceleration. Current fall from 158.86 should extend to 139.57 support. On the upside, above 144.07 minor resistance will turn intraday bias neutral again. But overall outlook will stay bearish as long as 151.20 resistance holds.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

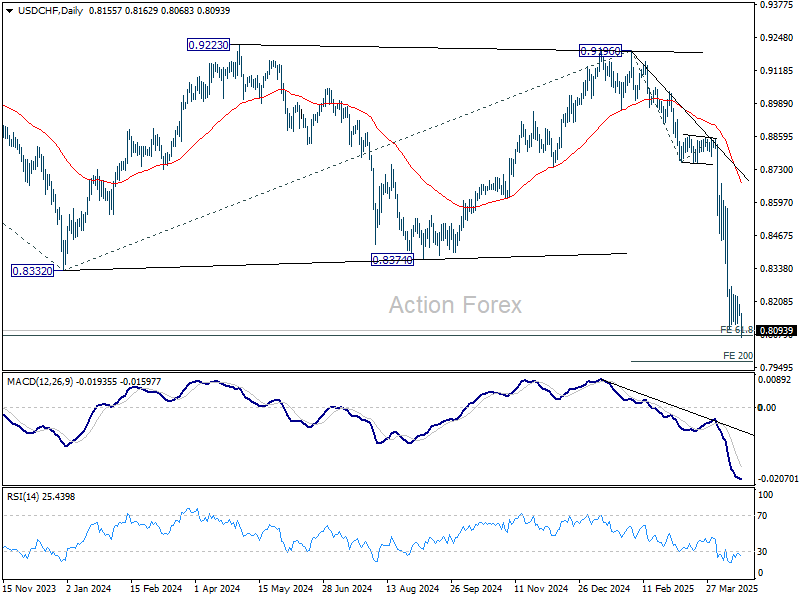

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8144; (P) 0.8176; (R1) 0.8195; More…

Intraday bias in USD/CHF is back on the downside with break of 0.8098. Current down trend should target 200% projection of 0.9196 to 0.8757 from 0.8854 at 0.7976 next. On the upside, above 0.8196 minor resistance will turn intraday bias neutral and bring consolidations again first.

In the bigger picture, the break of 0.8332 (2023 low) confirms resumption of long term down trend from 1.0342 (2017 high). Next target is 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9196 at 0.8075. Firm break there will target 100% projection at 0.7382. In any case, outlook will now stay bearish as long as 55 W EMA (now at 0.8794) holds.

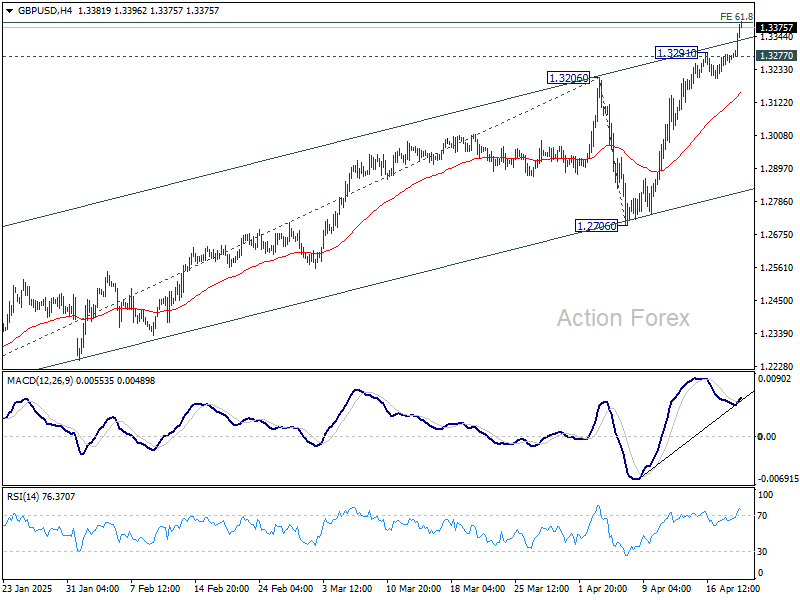

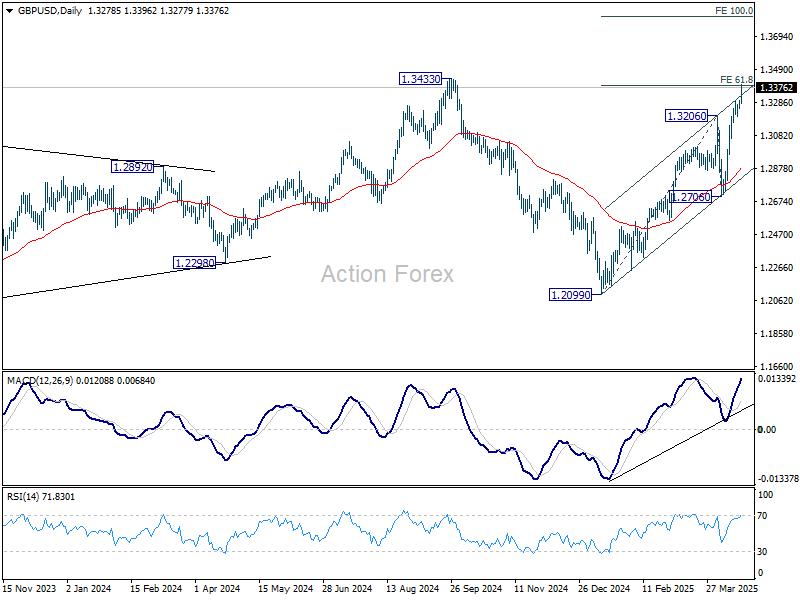

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3260; (P) 1.3280; (R1) 1.3316; More...

GBP/USD's really resumed by breaking through 1.3291 and intraday bias is back on the upside. Firm break of 1.3433 will confirm larger up trend resumption and target 100% projection of 1.2099 to 1.3206 from 1.2706 at 1.3813. On the downside, below 1.3277 minor support will turn intraday bias neutral again first.

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could be the second leg. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on break of 1.3433 at a later stage.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1314; (P) 1.1363; (R1) 1.1449; More...

EUR/USD's rally resumed by breaking through 1.1472 today and intraday bias is back on the upside. Current rise from 1.0176 should target 161.8% projection of 1.0358 to 1.0953 from 1.0731 at 1.1694 next. On the downside, below 1.1357 minor support will turn intraday bias neutral and bring consolidations again, before staging another rally.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0776) holds.

Dollar Slumps as Fed Independence in Question; Euro and Gold Surge on Haven Demand

Dollar weakened broadly in thin holiday trading today, dragged down by mounting concerns over the independence of the Federal Reserve. Investor anxiety escalated after White House economic adviser Kevin Hassett indicated that US President Donald Trump is continuing to explore whether he can remove Fed Chair Jerome Powell. While the legal basis for such a move is untested and unclear, the mere suggestion of political interference in the central bank’s policy process has significantly undermined market confidence.

This brewing conflict comes amid already heightened uncertainty surrounding US trade policy. Trump’s aggressive use of tariffs, most recently through sweeping reciprocal levies, has put the Fed in a difficult position. Officials including Powell have repeatedly warned that tariffs could simultaneously fuel inflation and suppress economic growth, increasing the risk of stagflation. A sudden crystallization of the threat to Fed independence would not only worsen market volatility but also raise tail risks, potentially triggering a broader loss of faith in US assets.

Powell, for his part, has firmly defended the Fed’s independence. In remarks last week, he asserted, “We’re never going to be influenced by any political pressure… Our independence is a matter of law.” He also reminded that Fed governors “are not removable except for cause,” and emphasized the long, fixed terms that protect against political meddling. While the "cause" does not typically include policy disagreements, the intensifying standoff with the White House has cast a long shadow over US institutions. Ad for now, the markets appear to be voting with their feet—out of the Dollar and into alternatives.

Euro has emerged as the biggest gainer in today’s subdued session, extending recent strength as investors seek refuge in the most liquid and viable alternative to Dollar. With its deep capital markets, relative political stability, and credible central bank, Euro is increasingly seen as a safer store of value amid the implosion of confidence in US governance. Other safe havens like the Japanese Yen and Swiss Franc are also holding firm, but it is Euro and Gold that are leading the charge.

Gold prices have surged to fresh record highs, fueled by a flight to safety and fears of policy instability. Technically, Gold is still in upside acceleration as suggested in D MACD. Despite overbought condition, there is no sign of topping yet. Decisive break of 161.8% projection of 2293.45 to 2789.92 from 2584.24 at 3387.52 will pave the way to 200% projection at 3577.18 next. Outlook will stay bullish as long as 3167.60 resistance turned support holds, in case of retreat.

China holds benchmark lending rates steady

China kept its benchmark lending rates unchanged for the sixth consecutive month today. One-year loan prime rate was held at 3.1% and the five-year LPR steady at 3.6%.

Subdued domestic inflation and growing global trade headwind, particularly the latest wave of tariff threats from the US, argue in favor of further policy easing However, PBoC appears reluctant to move ahead of Fed.

A premature rate cut could exacerbate downward pressure on the yuan, fueling capital outflows and financial instability.

April PMIs to gauge global business fallout from tariffs

The spotlight in the coming week will be on the flash PMI readings for April, covering major economies including Australia, Japan, the Eurozone, the UK, and the U.S. These surveys will serve as a timely barometer for assessing how global business conditions have responded to the surge in trade tensions following US President Donald Trump's "Liberation Day" tariff announcement earlier this month.

March PMIs had already reflected some of the early impact of trade policy uncertainty, particularly in North America. Notable takeaways included rising manufacturing input costs in the US and early signs of softening trade flows.

The upcoming data will be critical in identifying how deeply those measures are now affecting business conditions. Analysts will be watching for deterioration in new orders, delivery times, and price components—key indicators of disrupted supply chains and cost pass-through.

Beyond the PMIs, a series of supporting data will also shape market sentiment. US durable goods orders will be closely watched for signs of weakening beyond autos. Germany's Ifo business climate and expectations index will give a read on sentiment in Europe’s largest economy. Additionally, retail sales data from both the UK and Canada could reflect how consumers are responding to expected price shifts and economic uncertainty.

Here are some highlights for the week:

- Monday: China loan prime rate decision.

- Tuesday: Canada IPPI and RMPI; Eurozone consumer confidence.

- Wednesday: Australia PMIs; JapanPMIs, tertiary industry index; Eurozone PMIs, trade balance; UK PMIs; US PMIs, new home sales, Fed's Beige Book.

- Thursday: Japan corporate service prices; Germany Ifo; US jobless claims, durable goods, existing home sales.

- Friday: Japan Tokyo CPI; UK Gfk consumer sentiment, retail sales; Canada retail sales.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1314; (P) 1.1363; (R1) 1.1449; More...

EUR/USD's rally resumed by breaking through 1.1472 today and intraday bias is back on the upside. Current rise from 1.0176 should target 161.8% projection of 1.0358 to 1.0953 from 1.0731 at 1.1694 next. On the downside, below 1.1357 minor support will turn intraday bias neutral and bring consolidations again, before staging another rally.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0776) holds.

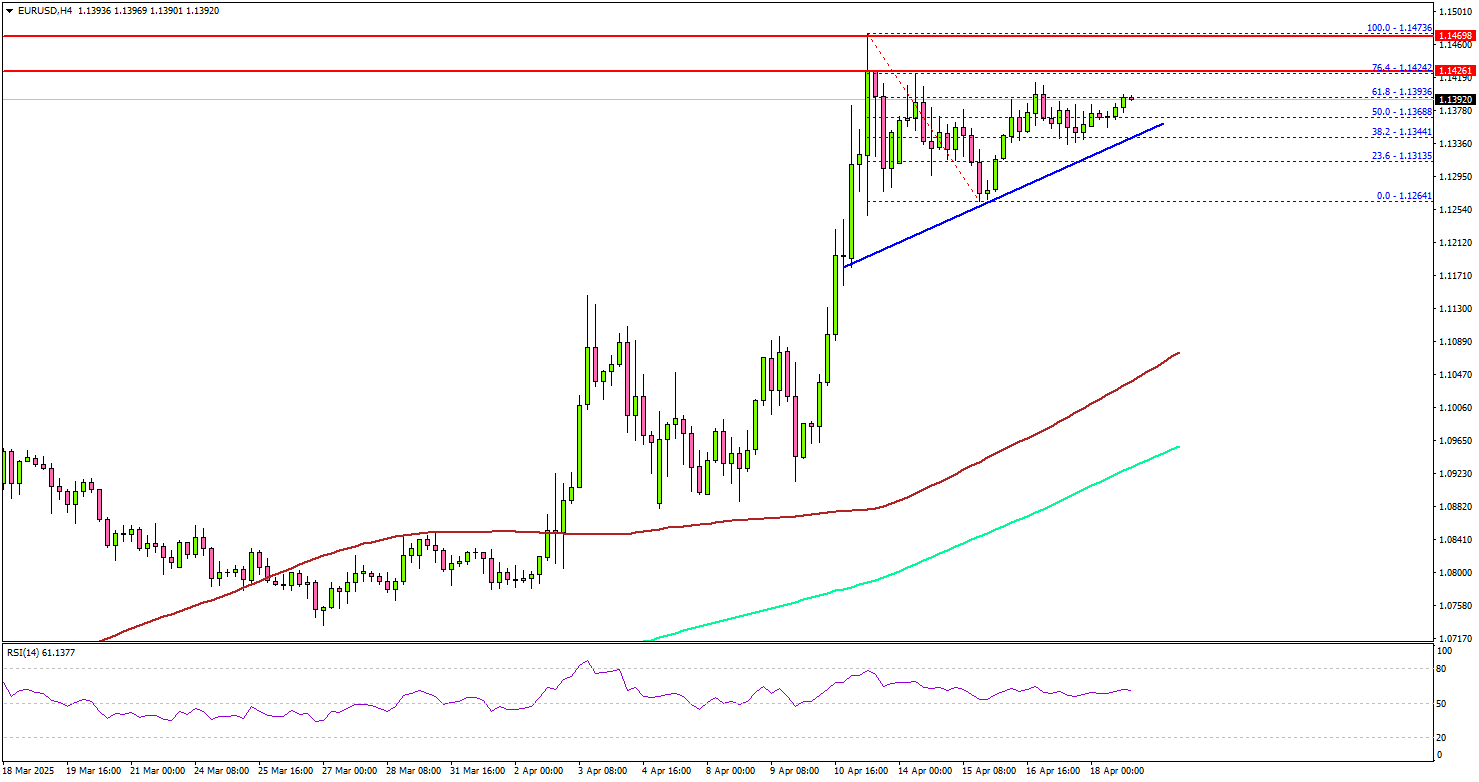

EUR/USD Poised for More Gains as Bulls Regroup

Key Highlights

- EUR/USD started a fresh increase above the 1.1250 resistance.

- A short-term bullish trend line is forming with support at 1.1345 on the 4-hour chart.

- GBP/USD gained pace and traded to a new multi-month high above 1.3300.

- Gold prices traded to a new record high and started a consolidation phase.

EUR/USD Technical Analysis

The Euro remained in a bullish zone above 1.1250 against the US Dollar. EUR/USD cleared the 1.1350 and 1.1380 levels before there was a consolidation phase.

Looking at the 4-hour chart, the pair settled well above the 1.1320 level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). There is also a short-term bullish trend line forming with support at 1.1345.

If there is a fresh increase, the pair could face resistance near the 1.1420 level. The next major resistance is near the 1.1450 level. The main resistance is now forming near the 1.1500 zone.

A close above the 1.1500 level could set the tone for another increase. In the stated case, the pair could even clear the 1.1550 resistance. On the downside, immediate support sits near the 1.1435 level and the trend line.

The next key support sits near the 1.1280 level. Any more losses could send the pair toward the 1.1220 level, where the bulls might take a stand.

Looking at GBP/USD, the bulls remained in action and were able to push the pair to a new multi-month high above the 1.3300 resistance.

Upcoming Economic Events:

- IMF Meeting.

China holds benchmark lending rates steady

China kept its benchmark lending rates unchanged for the sixth consecutive month today. One-year loan prime rate was held at 3.1% and the five-year LPR steady at 3.6%.

Subdued domestic inflation and growing global trade headwind, particularly the latest wave of tariff threats from the US, argue in favor of further policy easing However, PBoC appears reluctant to move ahead of Fed.

A premature rate cut could exacerbate downward pressure on the yuan, fueling capital outflows and financial instability.