Sample Category Title

Europe’s Opening Bell: Futures Point to Weakness in Europe, Gold Eyes Further Gains, GBP/USD Hits October 2024 Highs

- European futures hint at a weak open, despite Asian stocks rising.

- President Trump's potential adjustments to auto tariffs are causing market instability and investor nervousness.

- Gold prices remain high, with potential for further gains.

- The US Dollar Index shows signs of potential rebound, but uncertainty remains due to tariffs.

Asian stocks rose on Tuesday, but futures hint at European and US market weakness as President Donald Trump hinted at possible exceptions to auto-related tariffs.

On Monday, Trump said he might adjust the 25% tariffs on imported cars and parts from countries like Mexico and Canada. These tariffs could make cars thousands of dollars more expensive, but Trump said car companies need some time to start manufacturing vehicles in the U.S.

Markets are stabilizing as the tech exemptions have given hope for possible negotiations after the president’s tariffs earlier this month caused global stocks to lose $10 trillion and triggered a sell-off in US Treasuries. However, the constant changes are making investors nervous, and business leaders, like JPMorgan’s Jamie Dimon, have warned that Trump’s attempt to change global trade rules could lead to a US recession.

U.S. Treasury bonds stabilized overnight after last week’s big sell-off, while the dollar continued losing popularity with investors.

Australia's central bank was cautious about cutting interest rates further, saying May would be a good time to review its policies. This was mentioned in the minutes of its April meeting released in the Asian session. The April meeting was held just before President Trump's tariffs disrupted global markets.

Gold prices continue to hold the high ground having seen a brief pullback yesterday met with renewed buying pressure. For a full breakdown on Gold, read: Gold (XAU/USD) price update: is price action pointing toward fresh highs? $3250 loading….?

Economic data releases

There is quite a bit of data to navigate during the European session today with French inflation, ECB lending survey and German ZEW sentiment data.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Chart of the day - US Dollar index

From a technical standpoint, the US Dollar Index selloff could be running out of steam.

Yesterday's failure by bears to print a fresh low and a daily candle close back above support may hint at the potential for a US Dollar rebound.

The 14-period RSI is eyeing a break back above the oversold 30 handle which could be seen as a sign of changing momentum.

A bullish move would be intriguing as the index will likely test the psychological 100 level, with acceptance needed if a sustained USD recovery is to take place.

The tariff shadow and uncertainty however, mean that such a recovery may struggle to gain traction just yet.

US Dollar Index (DXY) Chart, April 15, 2025

Source: TradingView.com (click to enlarge)

Support

- 99.56

- 99.00

- 97.70

Resistance

- 100.00

- 100.61

- 101.18

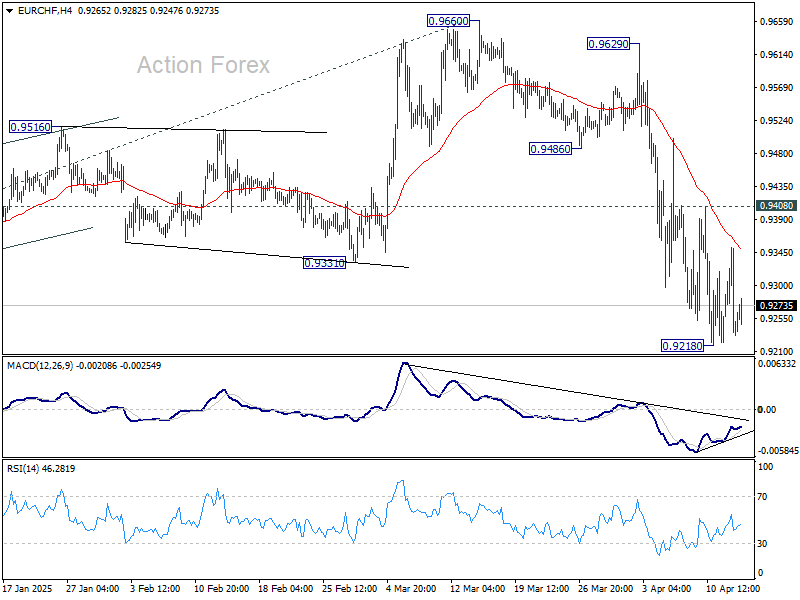

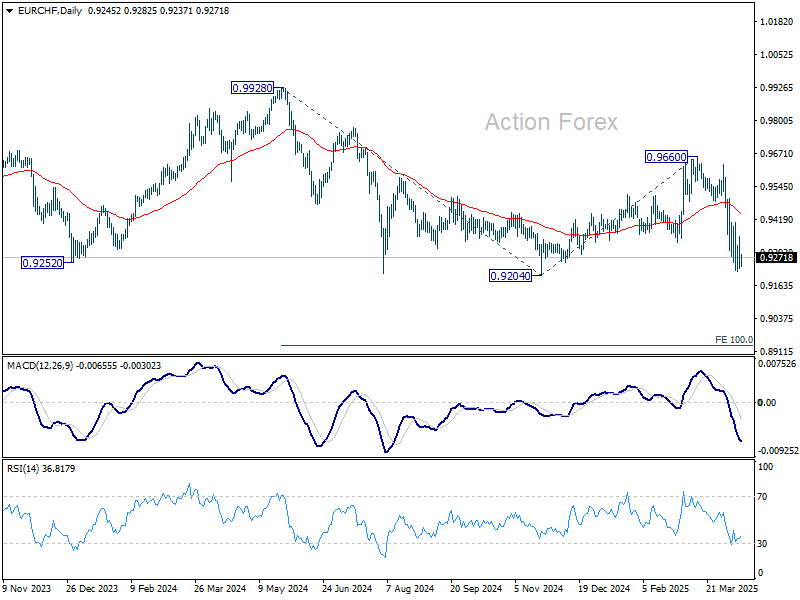

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9203; (P) 0.9279; (R1) 0.9324; More....

Intraday bias in EUR/CHF is turned neutral for consolidations above 0.9218. But outlook will remain bearish as long as 0.9408 resistance holds. On the downside, firm break of 0.9204 low will confirm larger down trend resumption.

In the bigger picture, rejection by long-term falling channel resistance (now at 0.9600) retains medium term bearishness. That is, down trend from 1.2004 (2018 high) is still in progress. Firm break of 0.9204 (2024 low) will confirm resumption. Next target is 100% projection of 0.9928 to 0.9204 from 0.9660 at 0.8936.

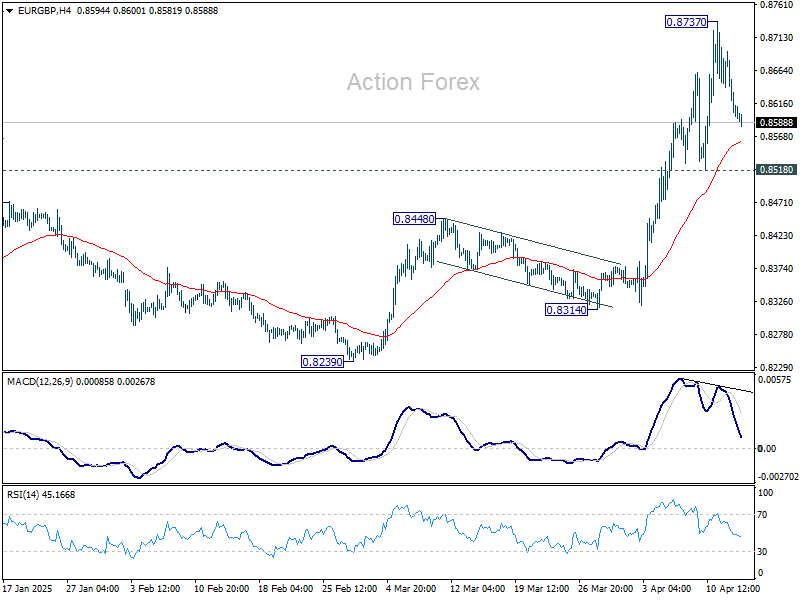

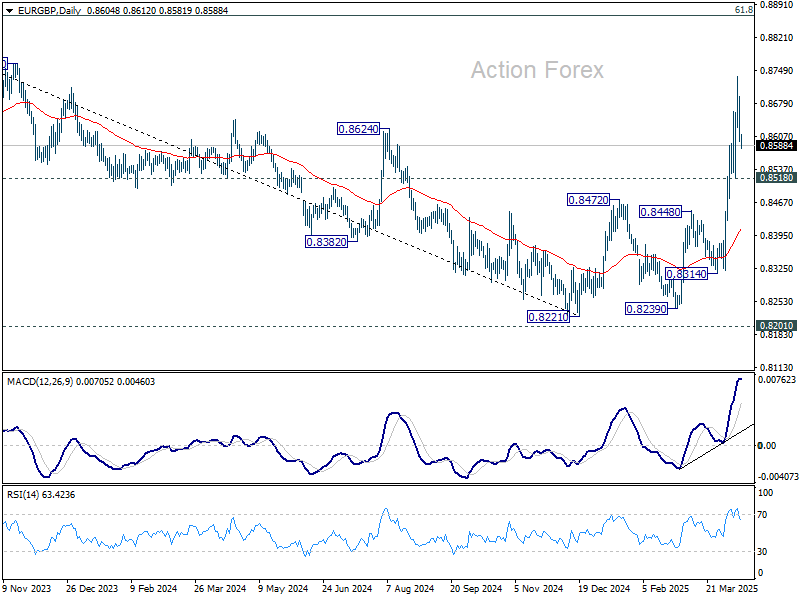

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8571; (P) 0.8633; (R1) 0.8666; More...

Intraday bias in EUR/GBP is turned neutral with current extended retreat. Some consolidations would be seen below 0.8737. But outlook will remain bullish as long as 0.8518 support holds. On the upside, break of 0.8737 will resume the larger rally from 0.8221.

In the bigger picture, down trend from 0.9267 (2022 high) should have completed at 0.8221, just ahead of 0.9201 key support (2024 low). Rise from 0.8221 is likely reversing the whole fall. Further rise should be seen to 61.8% retracement of 0.9267 to 0.8221 at 0.8867 next. This will now remain the favored case as long as 0.8472 resistance turned support holds.

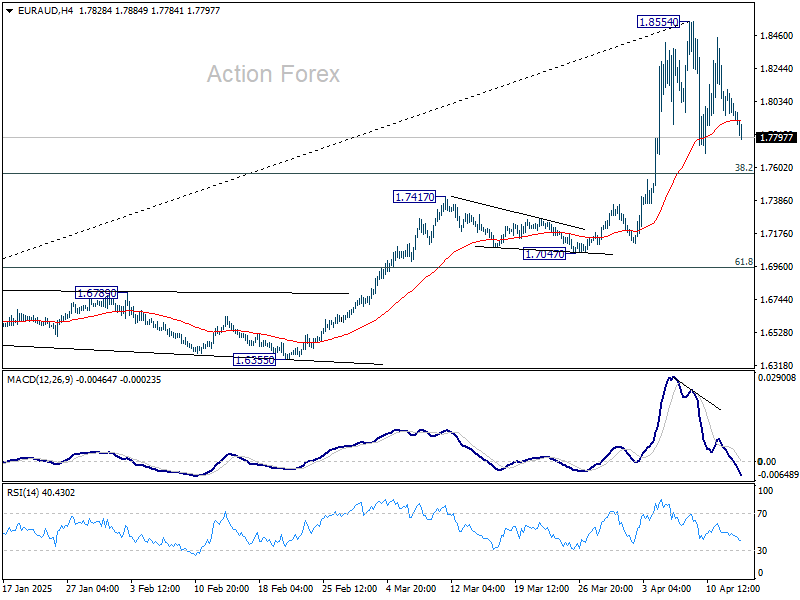

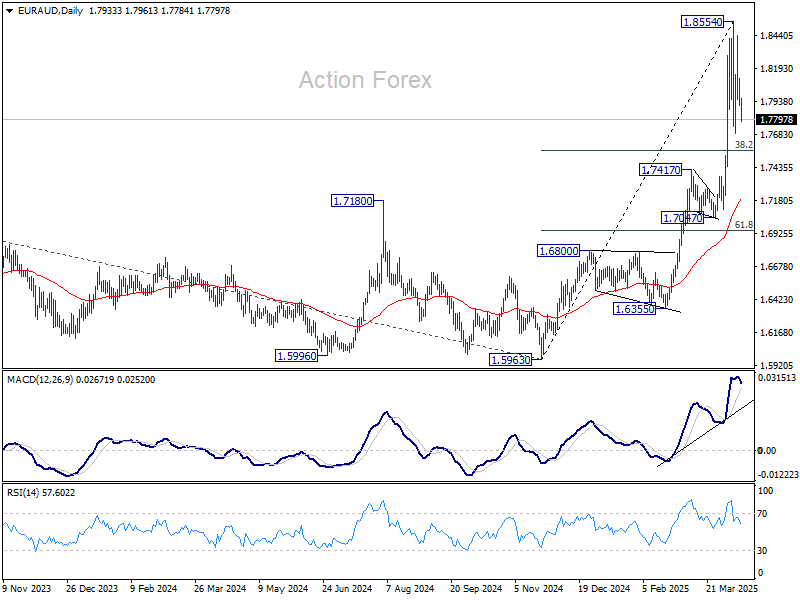

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7860; (P) 1.7987; (R1) 1.8066; More...

EUR/AUD's consolidation from 1.8554 short term to is still in progress and intraday bias stays neutral. In case of another dip, downside should be contained by 38.2% retracement of 1.5963 to 1.8854 at 1.7750. On the upside, firm break of 1.8554 will resume larger up trend.

In the bigger picture, up trend from 1.4281 (2022 low) is in progress, and in reacceleration phase as seen in W MACD. Next target is 100% projection of 1.4281 to 1.7062 from 1.5963 at 1.8744. Firm break there will pave the way to 138.2% projection at 1.9806, which is close to 1.9799 (2020 high). Outlook will remain bullish as long as 1.7417 resistance turned support holds even in case of deep pullback.

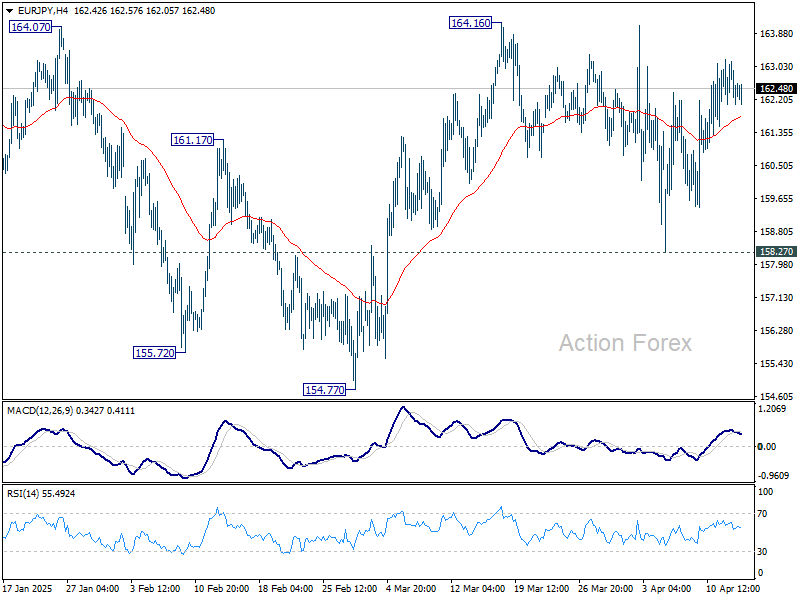

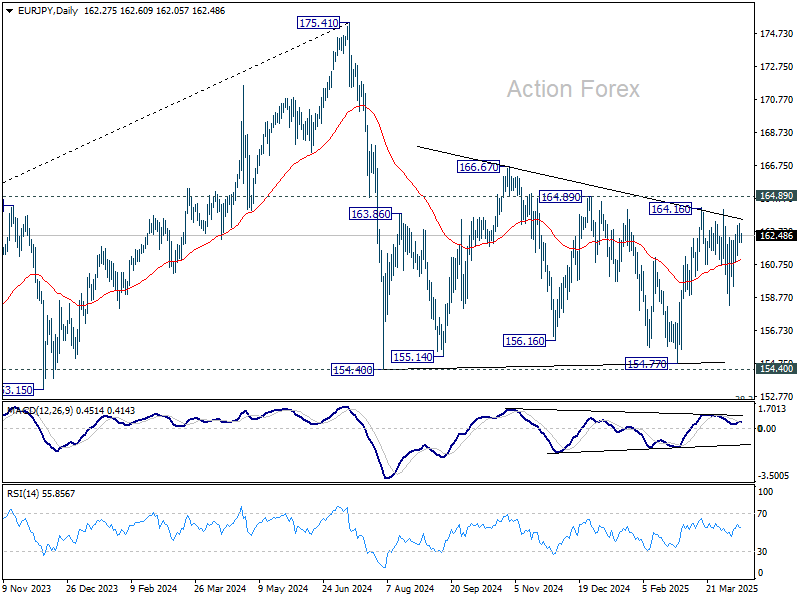

EUR/JPY Daily Outlook

Daily Pivots: (S1) 161.85; (P) 162.57; (R1) 163.06; More...

Intraday bias in EUR/JPY remains neutral as range trading continues. On the upside, above 164.16 will resume the rally from 154.77 to 164.89 resistance, and then 166.67. However, decisive break of 158.27 support will bring deeper decline back to 154.77 support. Overall, sideway consolidation pattern from 154.40 is still extending.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

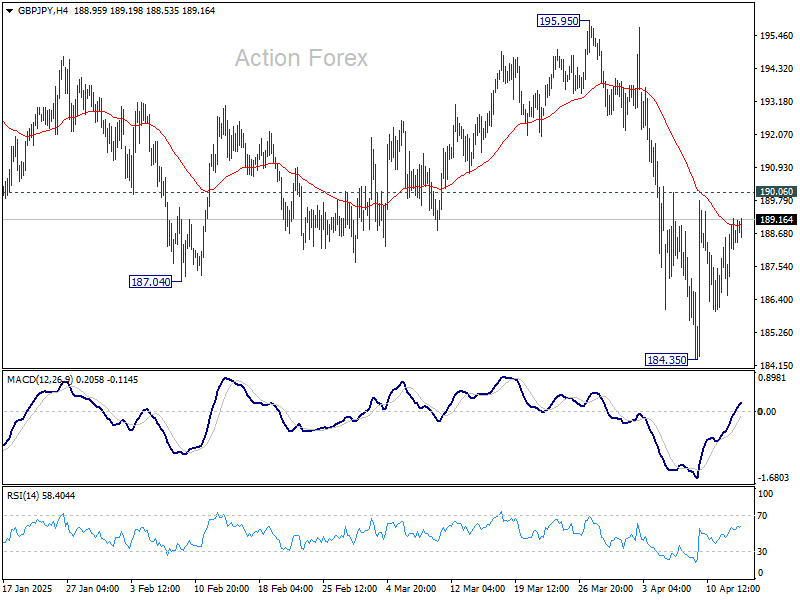

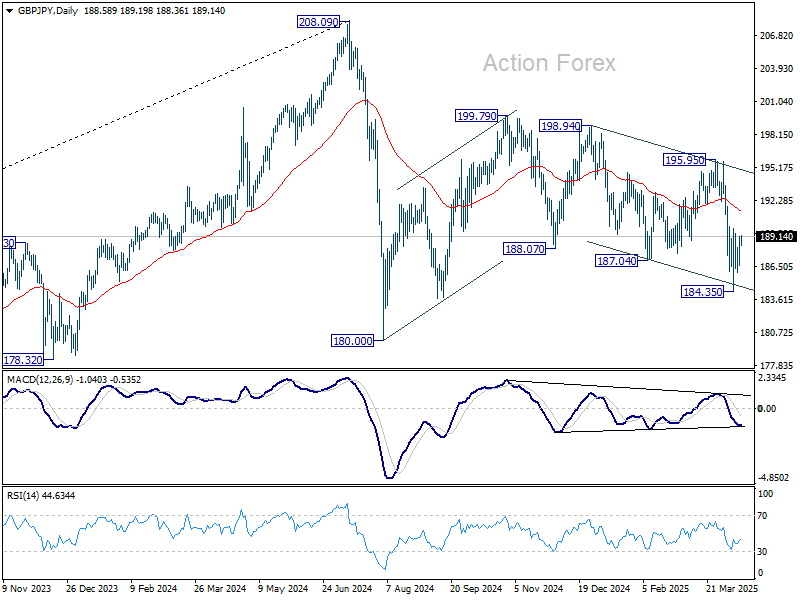

GBP/JPY Daily Outlook

Daily Pivots: (S1) 187.10; (P) 188.16; (R1) 189.72; More...

Intraday bias in GBP/JPY remains neutral as consolidation continues above 184.35. Risk will stay on the downside as long as 190.06 resistance holds. Below 184.35 will target 180.00 low. Nevertheless, break of 190.06 will turn bias back to the upside for stronger rebound.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 175.94 will bring deeper fall even still as a correction.

Brent Crude Price Consolidates

When analysing the Brent crude oil price chart six days ago, we:

→ identified a downward channel marked in red;

→ noted that the median line was acting as resistance;

→ suggested the price could find support at the lower boundary of the channel, reinforced by the psychological $60 per barrel level.

As shown on the XBR/USD chart, since then:

→ the price has indeed rebounded from the lower boundary (as indicated by the arrow), rising from its lowest level in nearly four years;

→ the median line has reaffirmed its role as resistance (highlighted by the marker).

Why Is Oil Consolidating?

From a technical perspective, several indicators suggest the market is consolidating. Notably, both the ADX and ATR indicators are trending downwards, which may be interpreted as a weakening of price momentum and volatility. Additionally, Brent’s price currently hovers around the channel’s median line — a level where supply and demand often reach equilibrium.

From a fundamental standpoint, it’s reasonable to assume that the current price has already factored in the latest developments surrounding the global trade war. However, another round of bold statements from the White House could still trigger a fresh move on the XBR/USD chart.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

German Economic Sentiment Set to Face a Sharp Decline Amid Tariff Turmoil

In focus today

The main data print is the German ZEW Economic Sentiment index for March which is set to release at 11:00 CEST. Consensus expectations are sharply to the downside at only 9.5, presumably due to the ongoing trade war turbulence. In February, the assessment of the current economic situation rose to 51.6 following the surprise in January at 26.0 which followed six months of declines. Current conditions are expected to improve marginally to -86.8 from -87.6 in February.

In Sweden at 8.00 CEST the government will present the spring budget amendment bill. However, most of it has already been revealed with total reforms of SEK11.5bn and where the largest announced proposal centres around an extended tax cut for home renovations. Last month the government announced a large, long-term, increase in defence spending but as the final target of defence spending will not be decided until the NATO summit in June, it will not be included in today's spring bill as we understand it. Hence, we do not expect the budget bill to be a market mover.

In the UK, we get the labour market report for February/March at 08:00 CEST.

Otherwise today is fairly quiet on the data front, with market participants eying the ongoing 'Tariff Turmoil'.

Economic and market news

What happened yesterday

In the US, Fed Governor Waller stated, "under large-tariff scenario with significant economic slowdown, I'd favour cutting policy rate sooner and more than previously thought." He (naturally) emphasized uncertainty but still sounded somewhat dovish in his remarks. Waller has often represented the consensus thinking within FOMC in the past. He highlighted that in a high-tariff scenario with average rates at 25% or above, as is just about the case today, the risk of recession would likely outweigh the risk of escalating inflation.

In Sweden, Money Market CPIF came in at 2.2% y/y (1Y) and 2.3% y/y (5Y). Inflation expectations increased slightly and expectations for GDP growth decreased significantly compared to March. This is also our expectations (or at least that the risk for lower growth has increased).

In Finland, the inflation data for March met expectations, with the CPI at 0.5% y/y and 0.0% m/m. This figure includes mortgage payments - which have decreased due to lower interest rates. Excluding these payments the preliminary HICP published earlier at 1.9%, indicated growing purchasing power in the Finnish economy.

In China, March Exports came in very strong at 12.4% y/y overshooting consensus estimates of 4.4% significantly. While the export figures are very strong by themselves, they are difficult to interpret due to the upcoming tariff changes. Exports are expected to decline sharply in April as trade with the US will cease at least in the short run. Importers could be viewing the tariffs as somewhat temporary and will thus postpone imports, while sectors like microchips and electronics may see increased activity. The situation is currently very muddy, making it challenging to decipher the underlying trends for the time being.

Equities: Global equities rose yesterday as further calmness, optimism, and risk appetite came to the investors. A key driver behind the rebound was growing belief that tariff levels may have peaked.

European equities outperformed those in the US, but more interestingly, it was the third consecutive day where defensive stocks outperformed cyclicals.

In the US, the worst-performing sector was consumer discretionary, a clear signal that investors are becoming more discerning - no longer selling indiscriminately but beginning to assess the longer-term implications of the trade war.

Hence, we are also seeing a growing realisation that earnings in certain sectors, mostly cyclicals, will be more impacted by what now looks increasingly like the endgame on tariffs.

In the US yesterday, the Dow rose 0.8%, the S&P 500 rose 0.8%, the Nasdaq rose 0.6%, and the Russell 2000 rose 1.1%.

Looking at Asia this morning, markets are also trading higher, with European futures in positive territory. US futures are marginally lower at the time of writing.

FI&FX: After bottoming near the 1.1300 level, EUR/USD has regained upward momentum, now hovering just below 1.14 as risk sentiment improved amid signs of greater flexibility from the US administration on tariffs. Similarly, NOK and GBP benefited from improving equity markets. European rates took a breather during yesterday's sessions with 2Y swap rates breaking below the 2% mark with calm market sentiment supporting equities across regions. Similarly, US Treasury yields declined amid dovish comments from FOMC's Waller highlighting his sensitivity to changes in employment. Today, keep an eye out for the US April Tax Day - the deadline for filing individual income taxes - which typically marks the largest daily inflows into the Treasury's cash balance of the year.

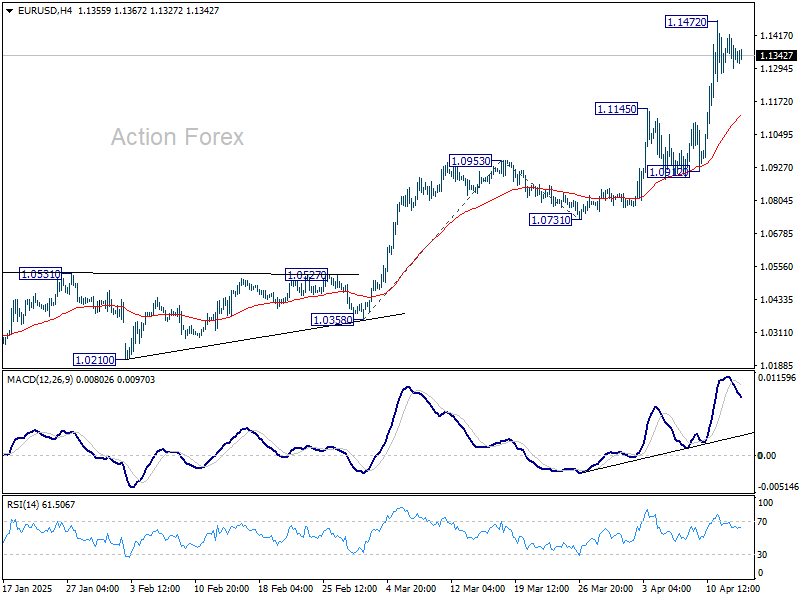

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1289; (P) 1.1357; (R1) 1.1418; More...

Intraday bias in EUR/USD remains neutral for consolidations below 1.1472 temporary top. Downside should be contained above 1.0912 support to bring another rise. On the upside, break of 1.1472 will target 161.8% projection of 1.0358 to 1.0953 from 1.0731 at 1.1694.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0745) holds.

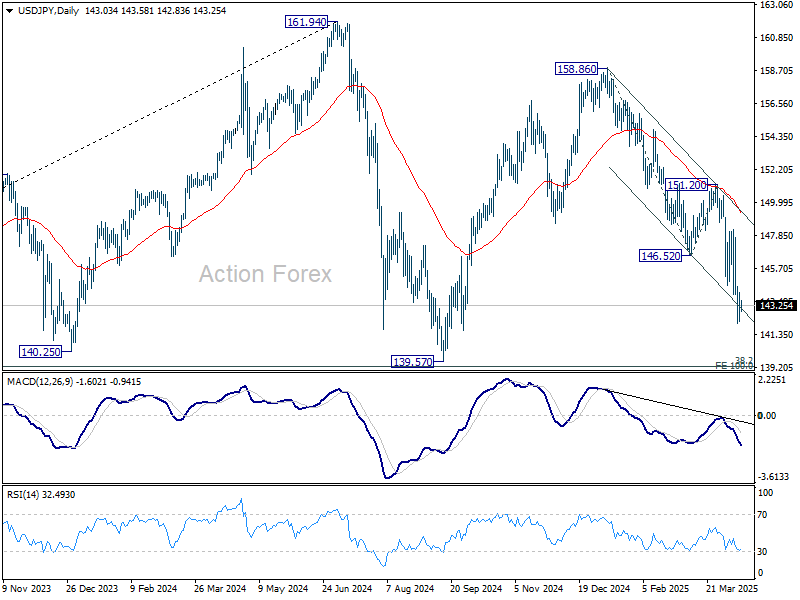

USD/JPY Daily Outlook

Daily Pivots: (S1) 142.14; (P) 143.11; (R1) 144.00; More...

Intraday bias in USD/JPY remains neutral for consolidations above 142.05 temporary low. Stronger recovery might be seen but outlook will stay bearish as long as 151.20 resistance holds. Below 142.05 will resume the fall from 158.86 to 139.57 support.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.