Sample Category Title

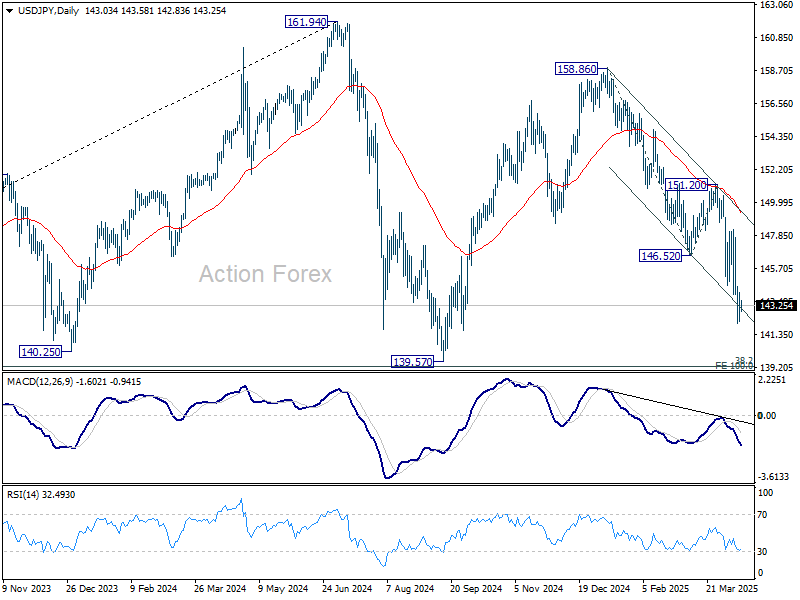

USD/JPY Daily Outlook

Daily Pivots: (S1) 142.14; (P) 143.11; (R1) 144.00; More...

Intraday bias in USD/JPY remains neutral for consolidations above 142.05 temporary low. Stronger recovery might be seen but outlook will stay bearish as long as 151.20 resistance holds. Below 142.05 will resume the fall from 158.86 to 139.57 support.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

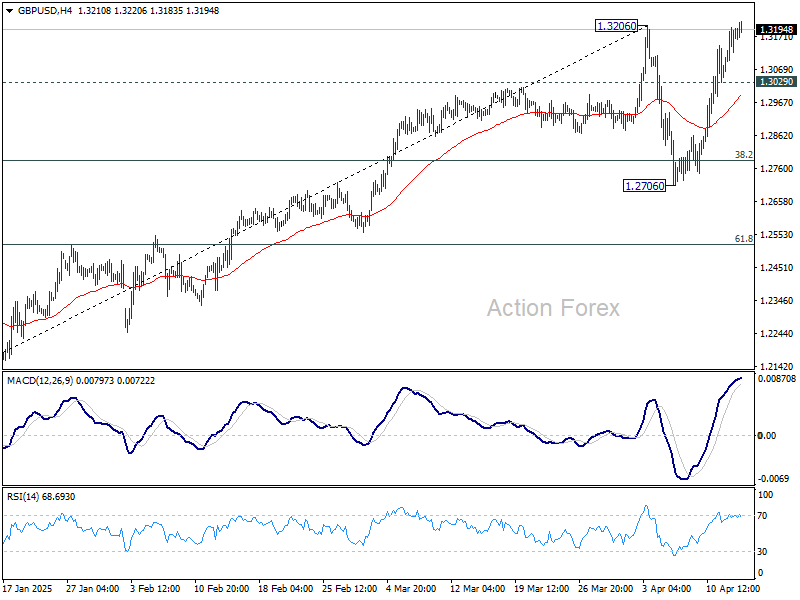

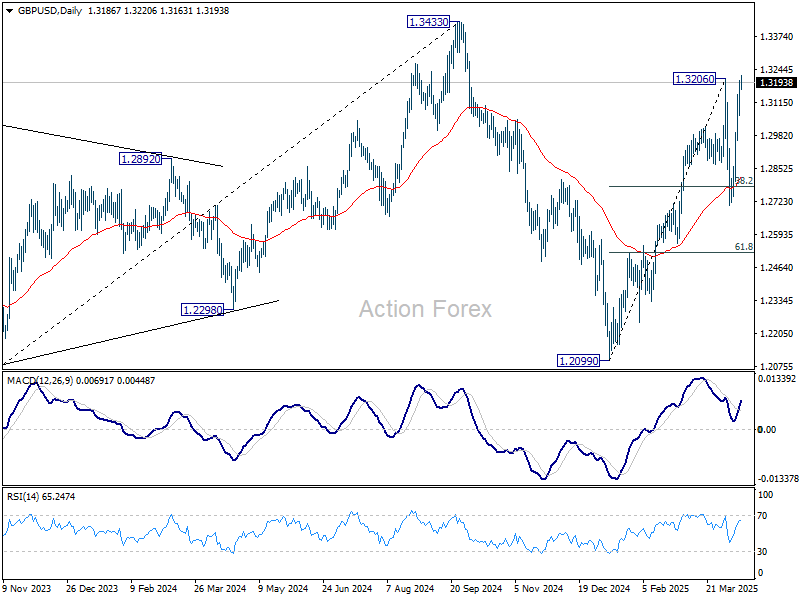

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3102; (P) 1.3151; (R1) 1.3241; More...

Intraday bias in GBP/USD remains on the upside for the moment. Firm break of 1.3206 resistance will will resume the rally from 1.2099 to retest 1.3433 high. On the downside, below 1.3029 minor support will turn intraday bias neutral again first. But overall near term outlook will stay bullish as long as 1.2706 support holds.

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could be the second leg. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on break of 1.3433 at a later stage.

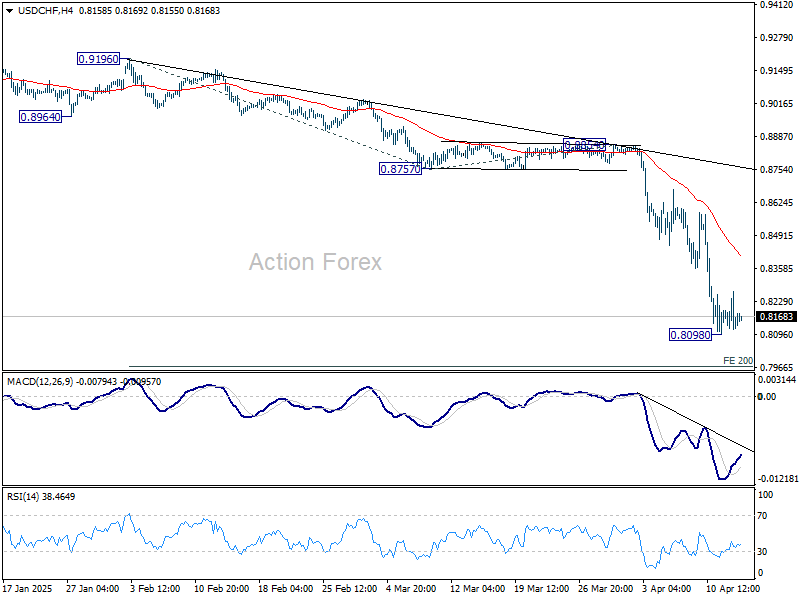

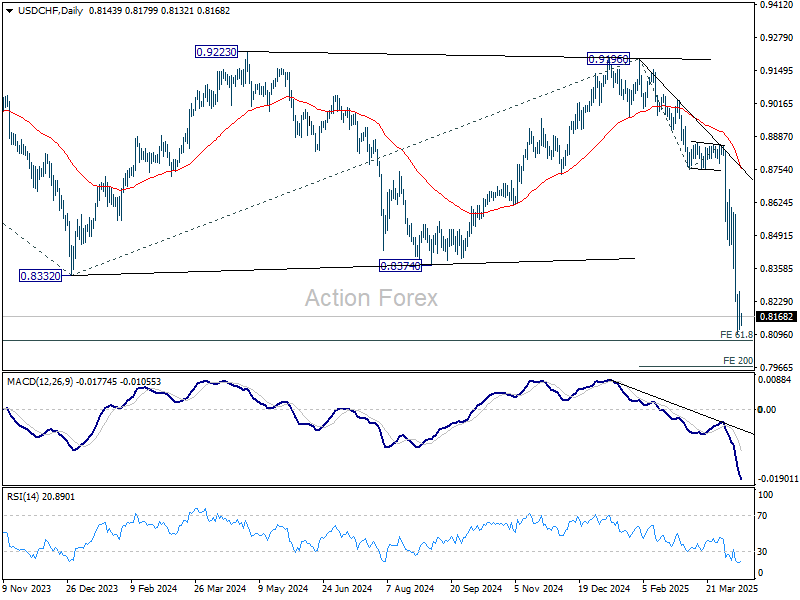

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8089; (P) 0.8179; (R1) 0.8238; More…

Intraday bias in USD/CHF remains neutral for consolidations above 0.8098 temporary low. While stronger rise might be seen, upside should be limited by 55 4H EMA (now at 0.8408) to bring another fall. On the downside, break of 0.8098 will resume recent down trend to 200% projection of 0.9196 to 0.8757 from 0.8854 at 0.7976 next.

In the bigger picture, the break of 0.8332 (2023 low) confirms resumption of long term down trend from 1.0342 (2017 high). Next target is 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9196 at 0.8075. Firm break there will target 100% projection at 0.7382.

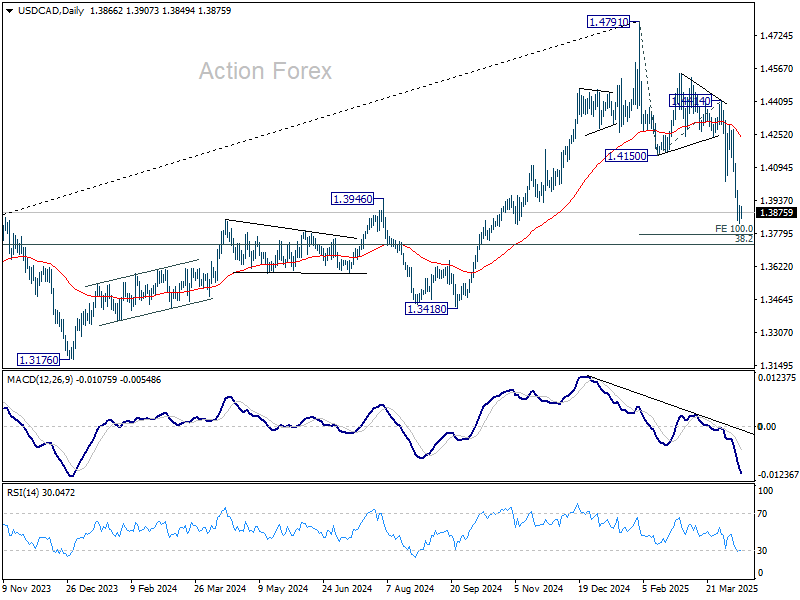

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3831; (P) 1.3871; (R1) 1.3913; More...

Intraday bias in USD/CAD is turned neutral first with current recovery. Some consolidations would be seen above 1.3827 temporary low. But outlook will stay bearish as long as 1.4150 support turned resistance holds. Below 1.3827 will resume the fall from 1.4791 to 100% projection of 1.4791 to 1.4150 from 1.4414 at 1.3773.

In the bigger picture, the break of 1.3976 resistance turned support (2022 high) and 55 W EMA (now at 1.3983) indicates that a medium term top is already in place at 1.4791. Fall from there would either be a correction to rise from 1.2005, or trend reversal. In either case, firm break of 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727 will pave the way back to 61.8% retracement at 1.3069.

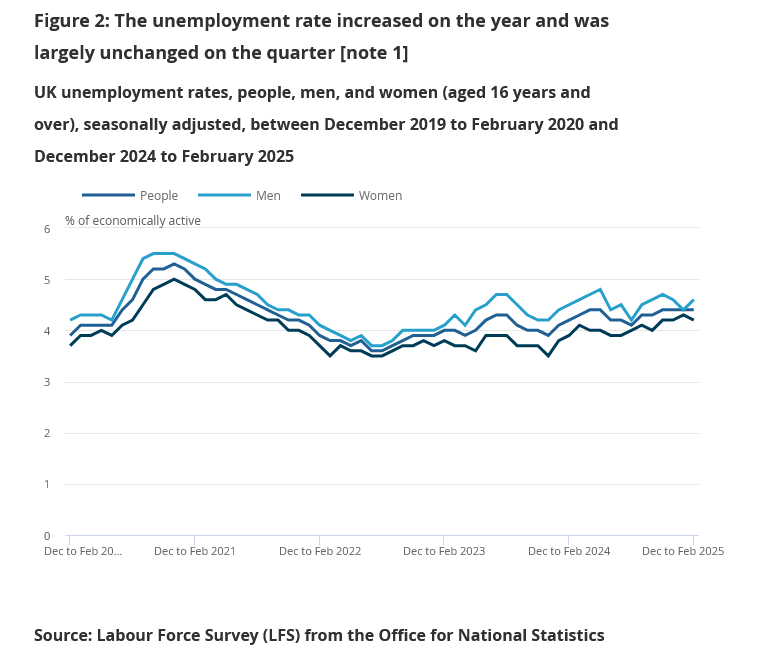

UK payolled employment falls -78k, wage growth slows

UK payrolled employment falling -by 78k in March, down 0.3% mom. Median monthly pay growth also moderated to 4.8% yoy from 5.5% yoy, pointing to easing wage pressures. Meanwhile, claimant count rose by 18.7k, less than the expected 30.3k increase.

In the three months to February, unemployment rate held steady at 4.4%, in line with expectations. Wage growth came in slightly below forecasts across the board. Average earnings including bonuses rising 5.6% yoy (unchanged from the previous month) and those excluding bonuses up 5.9%, a touch softer than the anticipated 6.0% yoy.

Risk Sentiment Remains More Constructive This Morning

Markets

The first session of the Easter trading week evolved relatively quietly especially when compared to last week’s turbulence. US assets got some reprieve. Daily changes on the US yield curve ranged between -6.2 bps (30-yr) and -14.9 bps (5-yr). US Treasuries found some support in comments by Fed governor Waller who returned to the 2021-2022 playbook by calling the resulting inflation spike from Trump’s tariff policy as likely to be transitory. He outlined two potential scenarios, one with an average US tariff rate of 25% through 2027 and one where the average rate is negotiated down to 10%. In the latter, his base case, he expect inflation to peak close to 3% with the US economy able to withstand the growth hit. The Fed should stay put with rate cuts later this year on the table (“good news” cut scenario). In the adverse scenario, inflation is likely to peak near 5% with a significant slowdown in the economy prompting a spike in the unemployment rate. In that case, Waller argues that the Fed should start cutting rates sooner and to a greater extent in response to the deteriorating economy (“bad news” cut scenario). Waller’s comments contrast with weekend views by Minneapolis Fed Kashkari who ruled out interest rate cuts as an insurance policy against an economic slowdown instead focusing on keeping inflation expectations anchored. Atlanta Fed Bostic thinks that the uncertain outlook puts the Fed and the economy in a “big pause position”, targeting just one policy rate cut this year. US Treasury Secretary Bessent after market close also tried to sooth (Treasury) market stress by pointing out increased foreign demand at recent auctions (vs rumoured sovereign selling) and by showing readiness to act if necessary to improve liquidity (eg by expanding the buyback program for older, off the run, securities). US stock markets recovered between 0.5%-1% yesterday, helped by president Trump’s suggestion to temporarily exempt tariffs on imported vehicles and parts to buy manufacturers time in relocating production. Over the weekend, a similar exemption was given to some electronics. On the one hand, short-lived product exclusions are becoming part of the improvised tariff policy. On the other hand, probes into semiconductor and pharmaceutical imports are a prelude for more sectoral tariffs. EUR/USD traded volatile to close in the middle of the 1.13-1.14 day range. The eco calendar was thin and had no intraday impact. The NY Fed survey was the sole datapoint. It nevertheless showed short-term (1-yr) inflation expectations rising from 3.13% to 3.58%, the highest level since September 2023.

Risk sentiment remains more constructive this morning in Asian dealings. The ECB’s lending survey, German ZEW investor confidence, the US empire manufacturing survey and US import/export prices are on tap. We expect them to play second fiddle and look at the equity market for guidance. We continue to err on the side of caution and don’t think we’re already set for a sustained risk rebound. UK labour market data were close to consensus this morning and don’t effect sterling. EUR/GBP finds a bid near 0.86.

News & Views

UK’s British Retail Consortium said that retail sales in the period between March 2 and April 5 rose by 1.1% y/y and 0.9% when the same stores are polled. BRC noted this March figure is artificially lower due to the timing of Easter in 2024 (March) and this year (April) and its chief executive said that the numbers therefore mask signs of underlying strength of demand. Food sales rose 1.6% and will probably get a boost in the next update. The non-food category registered a 0.6% increase with the improving weather having made for a particularly strong final week (gardening, DIY equipment). BRC did warn for the government’s tax increase to be passed on to consumers later this year, triggering an inflation uptick and potentially capping consumer spending again.

South Korea upped a support package created last year by around 25% to KRW 33tn for its critical semiconductor industry. The government decided to do so in the face of growing uncertainty originating from US policy and rising competition from China. For the same reasons it also hiked a financial assistance programme for the sector to KRW 20tn. The news comes after the US late yesterday initiated probes into semiconductor as well as pharmaceutical imports for national security reasons. They are seen as the precursor to actual import tariffs.

Uncertainties Persist, But Treasury Pressure Remains Manageable

Markets kicked off the week on a positive note on relief regarding the consumer electronics tariffs – that will not be exempt but will be part of a different ‘tariff bucket’ (20% instead of 145% for those made in China). Then, there was some relief for auto and part makers, as well. As such, the European stocks rallied 2.70% on partial rollback of the tariffs, the US stocks kicked off the week higher,but euphoria weakened into the session end on news that the US Commerce Department launched a probe into chips and pharmaceutical imports on national security reasons. The S&P500 closed the session 0.80% higher, while the tech-heavy Nasdaq couldn’t keep more than 0.57% of this advance. Apple jumped nearly 7% at the open but ended the session 2.20% up, while Nvidia was up by almost 3% at the open but closed -0.20% lower despite announcing half a trillion worth of infrastructure investment with its bodies including TSM. TSM – on the other hand – that’s preparing to announce its Q1 results this week - closed 0.80% lower.

This morning, the futures are flat with Nasdaq futures under pressure. Sentiment is fragile on bipolar announcements from the US that’s taking a toll on companies’ and investors’ ability to make decisions...

... except for China! China this week makes the decision of not reacting anymore (which I think is the best option because I myself deal with a 4 and a6-year old everyday) Instead of responding to the US, China’s Xi visits Asian counterparts to convince them that whatever they will negotiate to avoid US tariffs – it won’t be stable enough than sealing a deal with China. Appetite for Chinese stocks remain limited with the CSI 300 near flat today and the Hang Seng index giving back early gains.

One man’s misery is another’s fortune. Volatility helps trading desks post shiny revenues. Goldman Sachs yesterday announced its best revenue for equities trading in history. Traders there made $4.2bn as clients adjusted portfolios in response to tariff-induced market swings.

We’ve seen worse

Uncertainties persist but the good news is that the pressure on the Treasuries front remains bearable – and that is one place to watch carefully to judge how dangerous volatility gets. The US 2-year yield eased to 3.85% on expectation that the Federal Reserve (Fed) would better intervene than not to keep the US economy afloat through the storm, while the 10-year yield eased to 4.35%. We are substantially above the 3.80-3.90% range of a week ago, but the easing tensions hint that the selloff across the stock markets could stabilize, as well. All that – of course – under the assumption that Trump doesn’t say anything extravagant.

If you want ultimate protection, gold is there for you at around $3230 per ounce level. Is it too high to buy? Yes, it’s relatively high. If we look at the mint ratio - the ratio between gold and silver – it spiked above 100 during last week’s risk selloff. This ratio normally trends between 60 and 80, and rises when growth expectations are cooling because silver is more tied to industrial demand, so it's riskier and more cyclical. Therefore, yes gold is valued at around 100 times the same amount of silver, and Goldman expects the price of an ounce to hit $4000 by the middle of next year. It’s high, but what’s high if China (and others) were to replace their treasury holdings by gold?

Speaking of waning growth expectations

OPEC joined others in announcing further cuts to its global demand forecast this year and the next on tariff uncertainty. They lowered their projections by 100K barrels a day for this year and the next and predict that demand will grow by 1.3mbpd (or about 1%) over the next two years. That’s still significantly higher than other agencies. EIA for example dampened its own growth forecast by 30% to 900K bpd, while GS sees demand rising by only half a mbpd. US crude is better bid after last week’s short crash to the $55pb level but risks remain tilted to the downside with the next natural target for the bears standing at the $50pb.

In the FX

The more the US shakes the world with tariffs to get richer, the more the rest of the world dumps the dollar. The greenback remains under a decent pressure on waning growth expectations. Growth expectations are pulled lower everywhere – even in Germany that will benefit from massive defense and infrastructure spending – but the pace of deterioration of the US expectations are faster. As such, the dollar index consolidates below the 100 level this morning – the lowest levels in three years. The EURUSD remains bid above 1.13, Cable extends gains above 1.32, probably also fuelled by better than expected growth data of last Friday, the USDCAD sank below the 1.40 level and its 200-DMA last week despite the falling oil prices while the USDJPY consolidates near 142-143. The price rallies are interesting opportunities to strengthen short USDJPY positions on expectation that the Bank of Japan (BoJ) will remain supportive of the economy in the changing geopolitical spectrum.

Today, Canada and France will release their latest CPI updates, while German sentiment index and Eurozone industrial production are expected to come in soft enough to cement expectations that the European Central Bank (ECB) will cut the rates by 25bp this week and a few more times in the coming meetings if inflation remains under control. If that’s the case, the softness of the data could be good news for the euro and the European stocks.

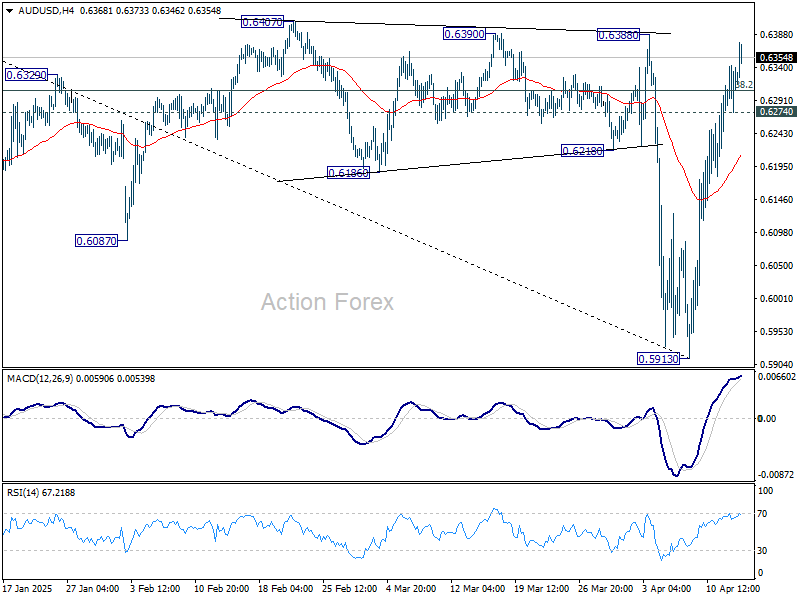

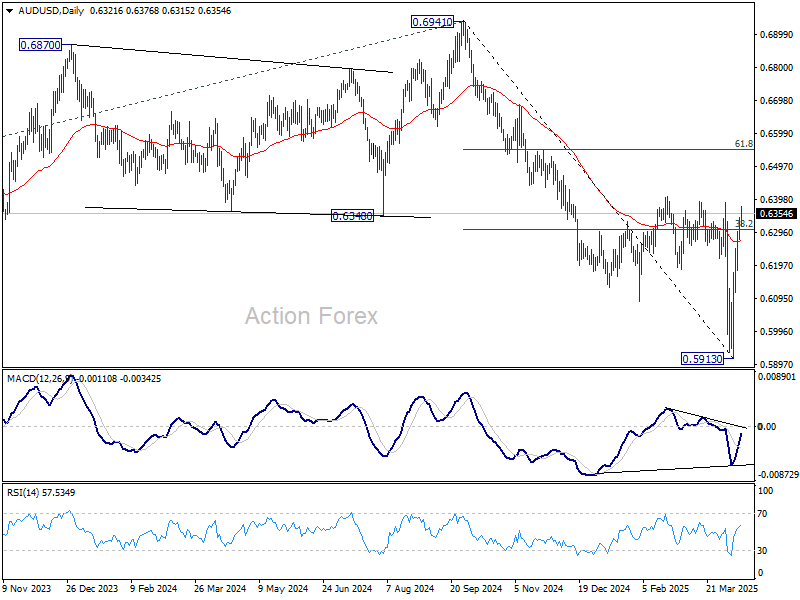

AUD/USD Daily Report

Daily Pivots: (S1) 0.6287; (P) 0.6315; (R1) 0.6355; More...

AUD/USD's rally from 0.5913 is still in progress and intraday bias stays on the upside. Firm break of 0.6407 resistance will pave the way to 61.8% retracement of 0.6941 to 0.5913 at 0.6548, even still as a corrective move. On the downside, below 0.6180 minor support will turn intraday bias neutral first.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. However, sustained trading above 55 W EMA (now at 0.6441) will argue that a medium term bottom was already formed, and set up further rebound to 0.6941 resistance instead.

Aussie Rises on Risk Rebound; RBA Keeps May Decision Open-Ended

Commodity currencies, including Australian, New Zealand, and Canadian Dollars, are trading broadly higher in today’s Asian session, buoyed by continued recovery in global stock markets. Sterling is also advancing alongside, supported by improving risk sentiment. Meanwhile, traditional safe havens like the Swiss Franc, Japanese Yen, are on the back, along with the greenback foot. Swiss Franc is particularly soft, pulling back after recent strong gains. Euro remains directionless in the middle of the pack, showing little inclination to break out against Dollar yet.

In RBA's minutes policymakers explicitly citing China’s response as a pivotal factor shaping Australia’s economic outlook and, by extension, future rate decisions. Given that China remains the only major economy actively retaliating against US tariffs, the fallout from a protracted trade war could be particularly impactful for Australia. While some analysts read the RBA’s language as a signal that a rate cut may come as soon as May, the actual odds remain more evenly balanced than market consensus might suggest. Tomorrow’s Australian employment report could help clarify the picture, at least a little bit.

Fed Governor Christopher Waller’s speech is worth a read. It offered a structured view of the unfolding US tariff regime. Waller outlined two potential paths: one focused on reshoring manufacturing and reducing trade dependency—implying a prolonged period of elevated tariffs. The other, a route aimed at leveraging tariffs to negotiate lower trade barriers from other countries. The ultimate outcome hinges on the political objectives of the Trump administration. But in reality, the likely result may lie somewhere between those extremes.

Technically, Bitcoin is showing signs of stabilizing after its recent pullback. It remains well supported by 73812 cluster support (38.2% retracement of 15452 to 109571 at 73617) for now. Bullish convergence condition in D MACD is raising chance of a near term reversal. Firm break of 88769 resistance will argue that correction from 109571 has completed already, and the larger up trend remains intact. Retest of 109571 high should then be seen next.

In Asia, at the time of writing, Nikkei is up 0.96%. Hong Kong HSI is down -0.11%. China Shanghai SSE is down -0.17%. Singapore Strait Times is up 1.75%. Japan 10-year JGB yield is up 0.032 at 1.372. Overnight, DOW rose 0.78%. S&P 500 rose 0.79%. NASDAQ rose 0.64%. 10-year yield fell -0.129 to 4.364.

Fed’s Waller weighs two tariff paths

In a speech overnight, Fed Governor Christopher Waller laid out two divergent scenarios for US tariff policy and their economic fallout.

The first scenario assumes high tariffs, near average 25% or more, and remain in place for an extended period. This reflects a structural shift toward domestic production and reduced trade dependence. The second scenario envisions a negotiated reduction in foreign trade barriers, which would lower the average tariff rate back to around 10%, closer to the levels anticipated earlier this year.

Waller warned that if the "high-tariff" regime holds, the US economy is likely to "slow to a crawl" with inflation rising to around 4% before retreating in 2026, assuming inflation expectations remain anchored. In this scenario, the unemployment rate could climb toward 5% next year as business investment weakens under higher costs and persistent uncertainty.

In contrast, if the current pause in reciprocal tariffs leads to meaningful progress in trade negotiations and the easing of barriers, Waller expects a milder economic impact. Under this "smaller tariff" path, the economy would continue to grow—albeit at a slower pace—while inflation would likely stay on a downward trend toward Fed’s 2% target. In such a case, he said, rate cuts could be warranted later this year as a “good news” policy move.

Fed's Bostic cautions against bold policy moves as trade fog stalls US economy

Atlanta Fed President Raphael Bostic warned that the Trump administration's tariff measures and broader policy ambiguity have effectively pushed the economy into a "big pause," making it difficult for the Fed to chart a clear policy path.

Bostic emphasized that this uncertainty argues against any aggressive policy shifts in either direction. “Moving too boldly with our policy in any direction wouldn’t be prudent.” He likened the current climate to a “really, really thick” fog that hampers effective decision-making.

On the inflation front, Bostic acknowledged that tariffs are likely to exert upward pressure on prices. He now sees inflation returning to that level no sooner than 2027, well beyond previous expectations.

Bostic also anticipates that economic growth will decelerate sharply, with GDP expanding just above 1% this year—less than half the pace seen in recent years.

RBA Minutes: Next rate move not predetermined, China’s tariff response a key variable

The minutes from RBA’s March 31–April 1 meeting revealed emphasized that it was "not yet possible to determine the timing of the next move in interest rates." The Board emphasized the importance that the "next decision was not predetermined".

Members agreed that the May meeting would offer a more "opportune time" for reassessment, as it would coincide with updated data on inflation, wages, employment, and global tariff developments, as well as a revised set of economic forecasts.

RBA highlighted that the economic outlook could be significantly shaped by how Chinese authorities respond to global tariff developments. Meanwhile, RBA acknowledged that risks to the outlook exist on both sides.

On one hand, global trade uncertainties and softening demand may pose disinflationary pressures, while on the other, risks such as supply chain disruptions and currency depreciation could fuel inflation.

RBA opted to keep the cash rate unchanged at 4.10% at the meeting.

Looking ahead

Germany ZEW economic sentiment, and Eurozone industrial production will be featured in European session. Later in the day, main focus is on Canada CPI. US will release Empire state manufacturing and import prices.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6287; (P) 0.6315; (R1) 0.6355; More...

AUD/USD's rally from 0.5913 is still in progress and intraday bias stays on the upside. Firm break of 0.6407 resistance will pave the way to 61.8% retracement of 0.6941 to 0.5913 at 0.6548, even still as a corrective move. On the downside, below 0.6180 minor support will turn intraday bias neutral first.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. However, sustained trading above 55 W EMA (now at 0.6441) will argue that a medium term bottom was already formed, and set up further rebound to 0.6941 resistance instead.

RBA Minutes: Next rate move not predetermined, China’s tariff response a key variable

The minutes from RBA’s March 31–April 1 meeting revealed emphasized that it was "not yet possible to determine the timing of the next move in interest rates." The Board emphasized the importance that the "next decision was not predetermined".

Members agreed that the May meeting would offer a more "opportune time" for reassessment, as it would coincide with updated data on inflation, wages, employment, and global tariff developments, as well as a revised set of economic forecasts.

RBA highlighted that the economic outlook could be significantly shaped by how Chinese authorities respond to global tariff developments. Meanwhile, RBA acknowledged that risks to the outlook exist on both sides.

On one hand, global trade uncertainties and softening demand may pose disinflationary pressures, while on the other, risks such as supply chain disruptions and currency depreciation could fuel inflation.

RBA opted to keep the cash rate unchanged at 4.10% at the meeting.