Sample Category Title

(RBA) Minutes of the Monetary Policy Meeting of the Reserve Bank Board

Sydney – 31 March and 1 April 2025

Members present

Michele Bullock (Governor and Chair), Andrew Hauser (Deputy Governor and Deputy Chair), Marnie Baker, Renée Fry-McKibbin, Ian Harper AO, Carolyn Hewson AO, Steven Kennedy PSM, Iain Ross AO, Alison Watkins AM

Others present

Sarah Hunter (Assistant Governor, Economic), Brad Jones (Assistant Governor, Financial System), Christopher Kent (Assistant Governor, Financial Markets)

Anthony Dickman (Secretary), David Norman (Deputy Secretary)

Meredith Beechey Osterholm (Head, Monetary Policy Strategy), Andrea Brischetto (Head, Financial Stability Department), Sally Cray (Chief Communications Officer), David Jacobs (Head, Domestic Markets Department), Michael Plumb (Head, Economic Analysis Department), Penelope Smith (Head, International Department), Claudia Seibold (Senior Manager, Domestic Markets Department, for the discussion of ‘Assessing the RBA’s government bond holdings’)

First meeting

The Governor welcomed members to the inaugural meeting of the Monetary Policy Board.

Financial conditions

Members began their discussion of financial conditions by reviewing central bank policy rates in advanced economies. All central banks had acknowledged the heightened and ongoing uncertainty surrounding both the scope and potential impact of US trade policies. Members noted that expectations for policy rates in the United States and Canada had eased over prior months. Central banks in both countries had communicated downside risks to growth and upside risks to inflation from US tariffs, though the US Federal Reserve’s central expectation was for the effect on domestic inflation to be transitory. The lower expected path for US policy rates also reflected reduced market expectations of stimulatory fiscal policies and some softer-than-expected economic data.

In other major economies, financial market expectations for central bank policy rates had been more stable. In Europe, expectations of substantial fiscal stimulus – driven by an anticipated increase in defence spending and a relaxation of fiscal rules – had tempered expectations for further policy rate cuts. Expectations that the Bank of Japan’s policy rate would be increased had risen in response to stronger-than-expected wages data and broader expectations that inflationary pressures in Japan are likely to be sustained.

In Australia, market participants’ expectations for the path of the cash rate had shifted a little higher in the near term, in response to communication following the February monetary policy meeting, but expectations had declined further out in response to international developments. Members noted that market pricing at the time was for further cuts in the cash rate totalling 50-75 basis points by the end of 2025 – with little-to-no probability of a cut at the present meeting and around a 65 per cent probability of a cut in May. The cash rate path expected by market economists was a little higher than that reflected in market pricing. Members discussed possible explanations for this, including that market pricing incorporated some probability of very adverse outcomes associated with a marked escalation in trade tensions.

Longer term sovereign bond yields in advanced economies had drifted lower in the United States and Canada but had risen slightly in Europe and Japan, in part reflecting the different shifts in expectations for central bank policy in those economies. In the United States, market-implied measures of inflation expectations derived from bond yields had increased at the two-year horizon but remained largely unchanged at longer horizons, suggesting that market participants expected the announced tariffs would not have persistent effects on US inflation. Outside of North America, market measures of inflation expectations were little changed, including in Australia.

Turning to conditions in corporate funding markets, members noted that equity prices in the United States had fallen by almost 10 per cent from their peak as risk sentiment had deteriorated and the outlook for the US economy had weakened. By contrast, European equity prices had risen by more than 10 per cent since November, in response to expectations of greater defence and infrastructure spending and increased hopes of a ceasefire between Russia and Ukraine. Equity prices had declined in Australia by less than in the United States but by a similar amount to other small open economies that were particularly exposed to declines in global trade. Members noted that despite these recent movements, measures of compensation for risk in equity and corporate bond markets remained very low in all advanced economies. An important question was whether that optimism was justified on the basis of a relatively positive outlook for global activity, or whether it indicated the potential for financial conditions to tighten considerably if outcomes deteriorated, even modestly, relative to market expectations.

In China, total social financing had increased as a result of very strong growth in Chinese Government bond issuance. Household credit growth had also picked up but remained very low, with weakness in the property sector an ongoing constraint.

The Australian dollar had depreciated slightly on a trade-weighted basis since the previous monetary policy meeting. This had been driven by depreciation against the Chinese renminbi, the euro and the yen, and mainly reflected changing interest rate differentials. Commodity prices – another key determinant of the Australian dollar historically – had been little changed for several months. In trade-weighted terms, the Australian dollar was at the bottom of the range it had moved in over recent years and close to, or a little below, the various staff estimates of its long-run equilibrium value based on current information. Members noted that the Australian dollar had been an important automatic stabiliser for the economy in the face of sizeable global shocks and was expected to continue to play that role.

Members noted that Australian households’ debt servicing payments were still around their highest levels since 2012 as a share of household disposable income. Scheduled debt payments had stabilised relative to incomes over the second half of 2024, including because of growth in household incomes. However, households had increased their extra mortgage payments over the same period to pay down debt more quickly. Members noted that the reduction in the cash rate in February would reduce required household debt servicing payments somewhat and could provide indebted households with scope to finance higher consumption.

While overall financial conditions in Australia had eased a little with the cut in the cash rate target in February, members’ assessment was that they were still restrictive. Members nonetheless explored the extent to which competition among banks over preceding years and other factors had relaxed financial conditions. Aggregate credit growth had been somewhat stronger than in the years leading into the pandemic, which was unusual during a period of relatively high interest rates and in contrast to other advanced economies. Business credit growth had strengthened further in preceding months, though housing credit growth had moderated alongside weak housing price growth. Household credit had declined a little relative to income over preceding years, and business debt had risen only slightly as a share of GDP, from low levels.

International economic conditions

Members discussed the implications for the global economy of ongoing trade policy uncertainty. The US administration had imposed tariffs on Canada and Mexico, increased tariffs on China and set 25 per cent tariffs on aluminium and steel imports from all countries. Canada, China and the European Union had announced retaliatory tariffs. The United States had signalled that it would raise tariffs further, with an announcement of additional tariffs expected shortly after the meeting.

Members noted that a range of timely indicators of US economic sentiment had declined sharply, including consumer confidence, some business surveys and equity prices. This had increased the likelihood of lower growth in US household spending and business investment. Market economists’ forecasts for output growth in North America had been downgraded following announcements of higher tariffs, though forecasts for growth in Australia’s major trading partners had been less affected so far. The overall impact on global growth would depend on the policy responses in other economies. Members noted that recent data had suggested some pick-up in growth in China. Chinese authorities had also confirmed a 5 per cent GDP growth target in 2025, backed by more supportive fiscal policy to offset headwinds from tariffs and the still-weak property sector.

Members observed that the implications of tariffs for inflation could further complicate the global economic outlook. Inflation was still above central banks’ targets in some advanced economies and progress on disinflation had stalled or even reversed a little in some cases. Against this backdrop, countries imposing tariffs could experience higher import prices, supply chain disruptions and efficiency losses (resulting from tariff-induced distortions to trade patterns). These developments would raise the price level. If they also resulted in inflationary pressures that offset the disinflationary effects of lower output growth, policymakers in countries imposing tariffs could be faced with the challenging combination of slowing output growth and higher inflation. A range of market economists saw this as the most likely outcome for the United States in the period ahead.

The extent to which these international developments would affect the Australian economy was a further source of uncertainty and depended on a range of factors. Assuming the global tariffs announced so far and that the Australian Government did not impose retaliatory tariffs, a model-based scenario showed that the effects on GDP growth and inflation in Australia could be relatively modest. This reflected Australia’s limited direct trade exposure to the United States, additional policy support in China and Australia’s flexible exchange rate. There were clear downside risks for Australian growth relative to this scenario, if tariffs and policy uncertainty have a greater effect on global growth than expected, if the spillovers to Australia are larger or if there were further material increases in tariffs in other economies, including those that are important for Australia. However, the risks to Australian inflation were more two-sided and would depend on the timing and relative size of the effects on aggregate demand and supply: weaker global demand and the possibility of trade diversion away from the United States could reduce inflation in Australia, but a larger exchange rate depreciation or more substantial global supply disruptions could increase inflation.

Members observed that concerns about US trade policy were already having a material influence on planning activities of some globally oriented Australian firms, but did not yet appear to be a widespread consideration for domestically focused firms. Similarly, trade measures were yet to have a significant effect on measured activity or inflation in Australia. Members nevertheless emphasised the importance of being alert to any signs of this changing.

Domestic economic conditions

Turning to domestic conditions, members noted that recent domestic data had been generally consistent with the forecasts in the February Statement on Monetary Policy.

GDP growth had picked up in the December quarter 2024, broadly as expected and consistent with a continued recovery in domestic demand. In per capita terms, GDP had risen for the first time since late 2022, albeit only slightly. Private demand had increased modestly in the December quarter, led by household consumption, while public demand had continued to support growth. The limited information available about activity in early 2025 suggested that the pick-up in GDP growth had been sustained. Natural disasters in parts of Queensland and New South Wales, while having a significant impact on affected areas, were expected to have only a modest impact on aggregate GDP. The 2025/26 Australian Government Budget had not conveyed material changes to the outlook for overall public demand.

Household consumption growth had started to recover in the December quarter, underpinned by the ongoing pick-up in real household incomes. While some of this recovery in consumption appeared to reflect price-sensitive consumers concentrating spending in promotional periods during the December quarter, the pick-up in spending growth among components not affected by sales events suggested there had been a genuine improvement in underlying momentum. More recent indicators signalled that some of this pick-up had been sustained.

Members noted the staff’s overall assessment that labour market conditions remained tight. The unemployment rate had increased slightly in early 2025, as expected, and was little changed since mid-2024. Underemployment had declined further to its lowest level since early 2023. Other indicators had also contributed to the assessment that labour market conditions were tight, including job vacancies, job advertisements and the share of firms reporting labour availability as a significant constraint on output. However, the quits rate – which measures the share of employees voluntarily leaving jobs – had continued to decline, perhaps signalling that inter-firm competition for labour had eased. More broadly, the NAB measure of firms’ capacity utilisation had declined a little further in February, consistent with gradually easing capacity pressures outside the labour market.

Members discussed the surprising decline in employment and the participation rate in February. Given this was only one month’s data, it seemed possible that the declines were a result of volatility in the monthly labour force data rather than an indication of softening in labour market conditions. Other sources of information were not indicating a sharp deterioration in employment growth: employment intentions from liaison and business surveys had stabilised or picked up a little recently, and income tax withholding collections had not exhibited any unusual patterns. Members agreed on the importance of monitoring employment outcomes closely over coming months.

Data on wages and labour costs received since the previous monetary policy meeting had provided somewhat contradictory signals. Year-ended growth in the Wage Price Index (WPI) had eased in the December quarter 2024, to 3.2 per cent. This pace of wages growth was in line with expectations, but revisions to the quarterly data suggested there was slightly less momentum at the end of 2024 than had been expected. By contrast, average earnings from the national accounts and unit labour costs – which are more comprehensive but more volatile measures of labour compensation and labour costs than the WPI – had grown more strongly in late 2024 than expected. Unit labour costs had increased by around 5½ per cent over 2024, significantly higher than the average growth rate over the inflation targeting period, in part reflecting ongoing weakness in measured productivity. Members noted the staff’s assessment that, on balance, the information in the data on wages and unit labour costs received in preceding weeks was broadly offsetting in terms of implications for the inflation outlook. This judgement would, however, be reviewed as part of the updated forecasts in May.

The monthly CPI indicator suggested that trimmed mean inflation would be likely to fall below 3 per cent in the March quarter, even with some likely pick-up in the quarterly outcome because of anticipated strong growth in certain administered prices and the unwinding of some temporary factors. Recent outcomes in other inflation sub-components had been consistent with the staff’s expectations. New dwelling construction prices had declined slightly in recent months, though advertised rents had been stronger than expected. Some firms continued to report in liaison that weak demand had limited the extent to which they could pass input cost pressures through to consumer prices. Members noted that the energy rebate extension announced in the Australian Government Budget would affect the profile of headline inflation in 2025 and 2026.

Financial stability assessment

Members considered the staff’s semi-annual assessment of financial stability risks. The staff assessed that the Australian financial system had continued to display a high level of resilience, and that banks were well placed to continue supporting the economy even in the event of a significant economic downturn. Accordingly, members observed that there were no immediate implications for monetary policy arising from domestic financial stability considerations.

While financial pressures remained pervasive across the Australian community, they had generally eased a little. This reflected lower inflation, the Stage 3 income tax cuts and the reduction in the cash rate in February. The share of borrowers who had fallen behind on their mortgage payments had stabilised at around pre-pandemic levels, and most mortgagors had maintained large liquidity and equity buffers. While lower income borrowers had been more likely to fall behind on their mortgages, arrears rates for these borrowers were well contained and had been declining since mid-2024. Borrowers in aggregate had continued to add to prepayment buffers over recent months. The share of borrowers in severe financial stress was likely to decline further in the period ahead under the staff’s central projections for the economy, although uncertainty about the outlook remained pronounced.

Looking further ahead, members noted that the RBA and other regulators were attentive to vulnerabilities that might build in the financial system if households responded to an actual or anticipated easing in financial conditions by taking on excessive debt. While lending standards were currently sound, historical experience both in Australia and abroad suggested that periods of lower interest rates can coincide with riskier borrowing activity, a rapid increase in house prices and, at times, a relaxation of lending standards. Historically, borrowing by investors had been particularly sensitive to changes in conditions in the mortgage market. The potential for this activity to amplify the credit and housing market cycle would be monitored closely.

Business insolvencies had continued to rise but, on a cumulative basis, were still slightly below their pre-pandemic trend. Members observed that broader spillovers to the financial system had been limited because insolvent firms were generally small and did not have significant levels of bank debt. Most business borrowers had continued to manage the pressures on their finances, and leading indicators of financial stress in the corporate sector – such as overdue trade credit – had stabilised or improved.

Notwithstanding the resilience of the domestic financial system, members recognised the potential for heightened geopolitical tensions and global trade policy uncertainty to interact with existing vulnerabilities in the global financial system. In this context, members acknowledged the work being done by the RBA and other agencies of the Council of Financial Regulators to reinforce the resilience of the financial system to withstand geopolitical risks, including risks relating to cyber threats and potentially severe operational disruptions to financial and other national infrastructure.

Members discussed several vulnerabilities in key international financial markets that also had the potential to affect the Australian financial system. Term premia for long-term advanced economy government bonds had begun to increase, after several years during which they had been unusually low, partly in response to deteriorating fiscal outlooks. Members noted the potential for more significant adjustments in global bond term premia if geopolitical or fiscal risks were to worsen. Compressed risk premia in US equity and credit markets also increased the likelihood that adverse news could spark a disorderly correction in international asset prices. The increased use of leverage and large positions established by some international hedge funds in key overseas financial markets had the potential to amplify such shocks. In an extreme scenario, a rapid and disorderly repricing in global asset markets and disruptions to funding markets had the potential to spill over to the Australian financial system.

Domestically, members noted the importance of banks and superannuation funds ensuring their liquidity risk management frameworks were able to withstand severe-but-plausible liquidity shocks. In the past, the superannuation sector had generally displayed a high level of resilience to market shocks and funds’ investment activities had tended to support financial stability, but the growth in assets under management meant that strengthening superannuation funds’ governance and risk management practices remains a focus of regulators. Members also discussed the Australian Prudential Regulation Authority’s expectations that smaller banks should take steps to improve the diversification of their liquidity portfolios.

Considerations for monetary policy

Turning to considerations for the monetary policy decision, members noted that the flow of data since the previous monetary policy meeting had been largely in line with the expectations of the staff. Inflation had continued to decline gradually. The labour market was judged to be tighter than was consistent with full employment and, at this stage, the large fall in employment in February was considered more likely to be a statistical aberration than a turning point in labour demand. Members assessed domestic financial conditions to be still somewhat restrictive. The most significant development in the period leading up to the meeting had been the significant rise in uncertainty about global trade policy, although the effect of this on sentiment and economic developments in Australia was not yet clear.

In light of this assessment, members agreed that the outlook for inflation and the labour market set out in the February Statement on Monetary Policy remained an appropriate starting point for their policy deliberations. So far, the economy appeared to be tracking in line with the staff’s forecasts, which were for underlying inflation to return to the 2-3 per cent range from mid-2025 before settling a little above the midpoint.

Members turned their discussion to the risks that were most prominent in their thinking about the economic outlook, and the relative importance of these. They agreed that the risks to the outlook were two-sided, with some that could result in economic activity and inflation in Australia being weaker than expected and others that could result in economic activity and inflation strengthening more noticeably.

Regarding risks emanating from the domestic economy, members judged that the nature and importance of these had not changed materially since the previous monetary policy meeting. They noted that several of the domestic risks could result in a tighter labour market and higher inflation were they to materialise. These risks included the potential for the tight labour market and strong growth in unit labour costs to have a more pronounced effect on inflation than anticipated. Members noted that it was also possible that the emerging recovery in domestic private demand could prove stronger than expected. They observed that this could occur if financial conditions were less restrictive than they currently assumed. Members also observed that an important assumption underpinning the forecasts was that productivity growth picked up and that this was not assured. They emphasised that the prolonged period of above-target inflation over prior years made these risks more salient and discussed the importance of not jeopardising the progress that has already been achieved in bringing inflation sustainably back to the midpoint of the target by easing monetary policy prematurely, particularly considering the experience of some other countries where disinflation appeared to have stalled.

At the same time, members noted that several other domestically generated risks could see economic activity and inflation slow by more than expected. They observed that the degree of tightness in the labour market was still uncertain and that, if there turned out to be more capacity in the labour market than the staff had assessed, inflation could return to target sooner than currently forecast. The likelihood of that possibility would increase if the slowing in wages growth in late 2024 continued or if the recent weakness in employment persisted. It was also possible that the anticipated pick-up in consumption growth again proved to be overly optimistic.

Regarding risks to the outlook for the global economy, members noted that these had increased and were tilted to the downside. They agreed that a significant further increase in global tariffs or other trade restrictions could materially disrupt global trade. Uncertainty about global economic policy settings could also lead firms and households to reduce spending and investment. If either of those consequences were to transpire, global economic activity could fall significantly, though the implications for inflation would be more complicated.

Members agreed that the implications of global developments for the Board’s policy decisions would depend on their effects on Australian activity, inflation and employment. It was possible to envisage circumstances in which the impact was significant, and members acknowledged that it is important for monetary policy to be forward-looking. However, the information to hand did not imply a significant change in the outlook, despite the substantial level of uncertainty. Even with the recent adjustments in some markets, pricing in financial and commodity markets was cautiously optimistic. And heightened global uncertainty did not yet appear to be having a significant effect on domestic spending. Members noted that while concerns about global trade policy were receiving scrutiny by Australian companies that export to the United States, sentiment among domestically focused companies had not yet adjusted downwards. The implications for Australia of global tariff settings would also depend on how Chinese authorities respond, and members noted the Chinese authorities’ stated commitment to maintaining output growth around 5 per cent. Importantly, the Board would need to monitor closely the implications of global developments for Australian inflation. Some of those developments could exert disinflationary pressure, including weak demand and the potential for trade diversion, but others could be inflationary, such as potential impairments to global supply chains and exchange rate depreciation.

In light of these considerations, members agreed that it was appropriate to maintain the cash rate target at its current level at this meeting. There had not been sufficient information to alter the central outlook for the Australian economy significantly. In addition, members judged that it was not appropriate at this stage for monetary policy to react to the potential risks that could move outcomes in either direction. It was nevertheless important to remain alert to the evolving balance of risks. Members observed that the May meeting would be an opportune time to revisit the monetary policy setting with the benefit of additional data about inflation, wages, the labour market and trends in economic activity, along with a fresh set of economic forecasts and further information about the likely evolution of global trade policies. Collectively, this information would have a considerable bearing on their decision.

Looking forward, the Board discussed the monetary policy strategy, which was to bring inflation back to the midpoint of the target band while maintaining as much of the gains in employment as possible. While the available information suggested that the strategy was on track, members agreed that it was not yet possible to determine the timing of the next move in interest rates. They noted that future decisions would, in each instance, depend on new information and its implications for the economic outlook. Members noted risks to the outlook on both sides, and that monetary policy was well placed to respond to international developments were they to have material implications for Australian activity and inflation. Given this, members agreed that it would be helpful if the Board’s public communication following the meeting made it clear that the outcome of its next decision was not predetermined.

In finalising the policy statement, members emphasised the need to be cautious and alert to the evolving economic outlook, and the importance of future decisions being guided by the incoming information and the assessment of risks. They agreed that sustainably returning inflation to target is the Board’s highest priority and that it will do what is necessary to achieve that outcome.

The decision

The Board decided to leave the cash rate unchanged at 4.10 per cent, and the rate on Exchange Settlement balances unchanged at 4.00 per cent.

Assessing the RBA’s government bond holdings

Members discussed the staff’s latest assessment of the pace at which the RBA’s holdings of government bonds were running down. The current approach – which had been endorsed by the Reserve Bank Board in December 2023 – is to hold these bonds until maturity but review it periodically. As in previous assessments, the paper considered the options of continuing with the current approach or reducing the RBA’s holdings by gradually selling bonds. Members agreed that there were no clear reasons at present to vary the pace of rundown for monetary policy or financial stability purposes, but the scale and maturity structure of the holdings did have implications for the RBA’s risks and returns. Given that, members agreed to seek the views of the Governance Board on risk and return considerations. A decision could then be made in due course on the basis of those considerations and any potential implications for monetary policy and financial stability.

Fed’s Bostic cautions against bold policy moves as trade fog stalls US economy

Atlanta Fed President Raphael Bostic warned that the Trump administration's tariff measures and broader policy ambiguity have effectively pushed the economy into a "big pause," making it difficult for the Fed to chart a clear policy path.

Bostic emphasized that this uncertainty argues against any aggressive policy shifts in either direction. “Moving too boldly with our policy in any direction wouldn’t be prudent.” He likened the current climate to a “really, really thick” fog that hampers effective decision-making.

On the inflation front, Bostic acknowledged that tariffs are likely to exert upward pressure on prices. He now sees inflation returning to that level no sooner than 2027, well beyond previous expectations.

Bostic also anticipates that economic growth will decelerate sharply, with GDP expanding just above 1% this year—less than half the pace seen in recent years.

British Pound Breakout? GBP/USD Surges as Momentum Builds

Key Highlights

- GBP/USD started a fresh increase above the 1.3120 resistance.

- It cleared the 1.3150 zone and retested the 1.3200 resistance on the 4-hour chart.

- EUR/USD is consolidating gains above the 1.1280 support zone.

- Gold prices traded to a new record high above $3,240 and started a consolidation phase.

GBP/USD Technical Analysis

The British Pound remained supported above 1.2880 against the US Dollar. GBP/USD started a fresh surge above the 1.3000 and 1.3050 resistance levels.

Looking at the 4-hour chart, the pair cleared the 1.3150 zone and retested the 1.3200 resistance. There was a close above the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour).

A high was formed at 1.3201 and is currently consolidating gains. If there is a fresh increase, the pair could face resistance near the 1.3220 level.

The next major resistance is near the 1.3250 level. The main resistance is now forming near the 1.3320 zone. A close above the 1.3320 level could set the tone for another increase. In the stated case, the pair could even clear the 1.3450 resistance.

On the downside, immediate support sits near the 1.3140 level. The next key support sits near the 1.3080 level and the 23.6% Fib retracement level of the upward move from the 1.2708 swing low to the 1.3201 high. Any more losses could send the pair toward the 1.3015 level.

Looking at Gold, the price started a fresh increase, and the bulls might soon aim for a move toward the $3,300 level.

Upcoming Economic Events:

- UK Claimant Count Change for March 2025 – Forecast 30.3K, versus 44.2K previous.

- UK ILO Unemployment Rate for Feb 2025 (3M) – Forecast 4.4%, versus 4.4% previous.

Fed’s Waller weighs two tariff paths

In a speech overnight, Fed Governor Christopher Waller laid out two divergent scenarios for US tariff policy and their economic fallout.

The first scenario assumes high tariffs, near average 25% or more, and remain in place for an extended period. This reflects a structural shift toward domestic production and reduced trade dependence. The second scenario envisions a negotiated reduction in foreign trade barriers, which would lower the average tariff rate back to around 10%, closer to the levels anticipated earlier this year.

Waller warned that if the "high-tariff" regime holds, the US economy is likely to "slow to a crawl" with inflation rising to around 4% before retreating in 2026, assuming inflation expectations remain anchored. In this scenario, the unemployment rate could climb toward 5% next year as business investment weakens under higher costs and persistent uncertainty.

In contrast, if the current pause in reciprocal tariffs leads to meaningful progress in trade negotiations and the easing of barriers, Waller expects a milder economic impact. Under this "smaller tariff" path, the economy would continue to grow—albeit at a slower pace—while inflation would likely stay on a downward trend toward Fed’s 2% target. In such a case, he said, rate cuts could be warranted later this year as a “good news” policy move.

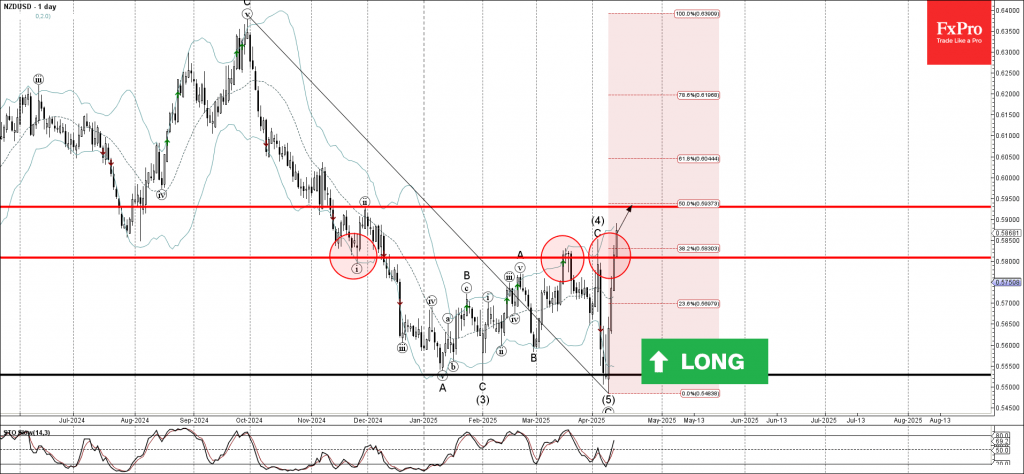

NZDUSD Wave Analysis

NZDUSD ⬆️ Buy

- NZDUSD broke resistance zone

- Likely to rise to resistance level 0.5930

NZDUSD currency pair recently broke the resistance zone between the key resistance level 0.5800 (which has been reversing the price from March) and the 38.2% Fibonacci correction of the downward impulse from September.

The breakout of this resistance zone accelerated the active intermediate impulse wave (1). Given the continuation of the strongly bearish US dollar sentiment, NZDUSD currency pair can be expected to rise to the next resistance level 0.5930, former top of wave ii from November.

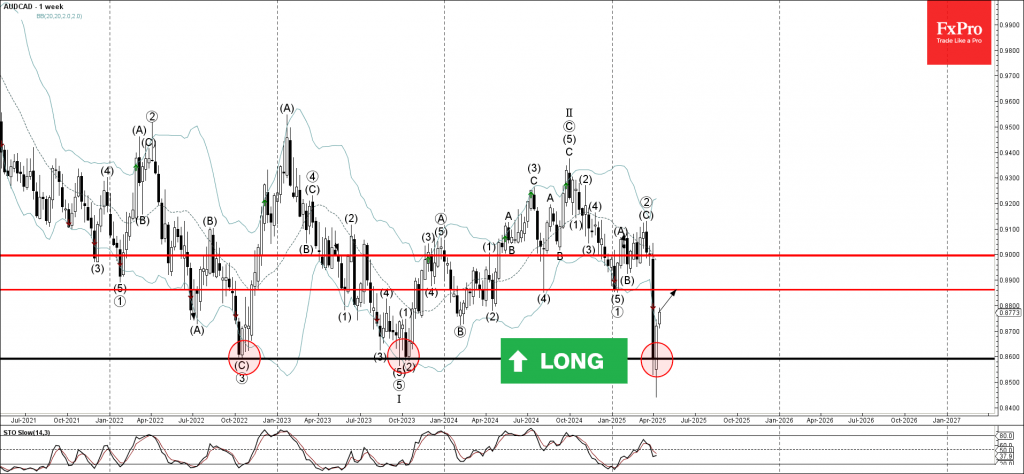

AUDCAD Wave Analysis

AUDCAD ⬆️ Buy

- AUDCAD reversed from the support zone

- Likely to rise to resistance level 0.8860

AUDCAD currency pair recently reversed up from the support zone located at the intersection of the long-term support level 0.8600 (which started two weekly uptrends from 2022) and the lower weekly Bollinger Band.

The upward reversal from this support area created the weekly Japanese candlesticks reversal pattern Piercing Line.

Given the strength of the aforementioned support zone, AUDCAD currency pair can be expected to rise to the next resistance level 0.8860, the former strong support from January.

Gold (XAU/USD) Price Update: Is Price Action Pointing Toward Fresh Highs? $3250 loading….?

- Gold prices saw a retreat from recent highs due to improved market sentiment and tariff exemptions, but Goldman Sachs has increased its gold price forecast for the end of 2025.

- Technical analysis indicates a potential for further price movement, with a focus on the 3250 handle and support at 3195 on the H1 timeframe.

- Period-14 RSI has left overbought territory. Has momentum shifted?

This is a follow-up analysis of our prior report “Gold (XAU/USD) price update: Bulls in charge as Trump hits tariff pause. $3150/oz up next?” published on 5 February 2025.

Gold prices have seen a retreat from the fresh highs printed in the Asian session dropping to a low of 3193 following the US open. Improved market sentiment across the board to start the week on the back of tariff exemptions on tech products from China.

Over the weekend there were also comments from Commerce Secretary Lutnick about how many countries are already ‘negotiating’ with the US. These were seen as positive developments helping overall sentiment and seeing a temporary pause in haven demand.

Goldman Sachs increased its forecast for gold prices by the end of 2025 to $3,700 per ounce, up from $3,300. They expect prices to range between $3,650 and $3,950, driven by higher demand from central banks and increased investments in gold-backed funds due to recession concerns. The bank also noted that if a recession happens, more money could flow into these funds, pushing gold prices to $3,880 per ounce by year-end.

Gold prices should remain supported however with any pullback likely to remain shallow in nature. The macro risks remain in play and until clarity on how much tariffs will be implemented, it looks like a bumpy road ahead. Volatility is likely to remain elevated and price swings are to become normality.

Technical Analysis - Gold (XAU/USD)

From a technical analysis standpoint, Gold prices have retreated from the fresh all-time highs printed in the Asian session.

Looking at the four-hour chart below and the parabolic move from the April 9 lows does leave room for a retracement.

The period-14 RSI has crossed back below the 70 overbought level, which is usually a sign that momentum may be shifting.

Gold (XAU/USD) Daily Chart, April 14, 2025

Source: TradingView (click to enlarge)

Dropping down to a one-hour H1 timeframe, and you can see that gold has formed higher low at 3195 support.

This would suggest a fresh high may be incoming with the 3250 handle now in focus.

However a H1 candle close below the support level at 3195 and a swift drop toward 3167 could come to fruition.

Gold (XAU/USD) Daily Chart, April 14, 2025

Source: TradingView (click to enlarge)

Support

- 3195

- 3167

- 3150

Resistance

- 3125

- 3145

- 3175

Strong Yen, Weak Dollar: How Low Can USDJPY Go?

Before trading any yen cross, always analyze the JPY separately as a haven and compare it with the index of the other currency involved. It’s essential to review each currency’s index to understand market sentiment and trade in line with the Primary Trend. For the yen, it’s useful to check the JPY Index versus the USD Index on TradingView.

The JPY Index reflects bullish sentiment, while the USD Index shows strong selling pressure. This suggests a bearish bias for the USDJPY pair. Any bullish movements for the USD will likely be short-lived unless a technical trend reversal is confirmed.

Fundamental Analysis

The Japanese yen (JPY) remains strong as a safe-haven asset amid escalating trade tensions between the U.S. and China. After Trump imposed new tariffs of 145%, China responded with 125% retaliatory tariffs. These geopolitical tensions are driving flows into the JPY, which is trading near its highest levels since September 2024. Additionally, optimism around a potential U.S.–Japan trade deal—fueled by encouraging comments from Trump and Treasury Secretary Scott Bessent—further supports the yen.

On the monetary policy front, divergence is putting downward pressure on USDJPY. The Bank of Japan (BoJ) maintains a hawkish stance following March’s 4.2% wholesale inflation data and wage pressure, while the Fed is expected to cut rates by 90 basis points in 2025 due to slowing inflation and the economic impact of tariffs. With the dollar at its lowest since April 2022, the pair continues in a multi-month downtrend, with risks skewed toward further USD weakness.

Key factors to monitor include the progress of U.S.–Japan trade talks, verbal interventions by Japanese officials regarding exchange rate volatility, and U.S. inflation and employment data to adjust Fed rate cut expectations.

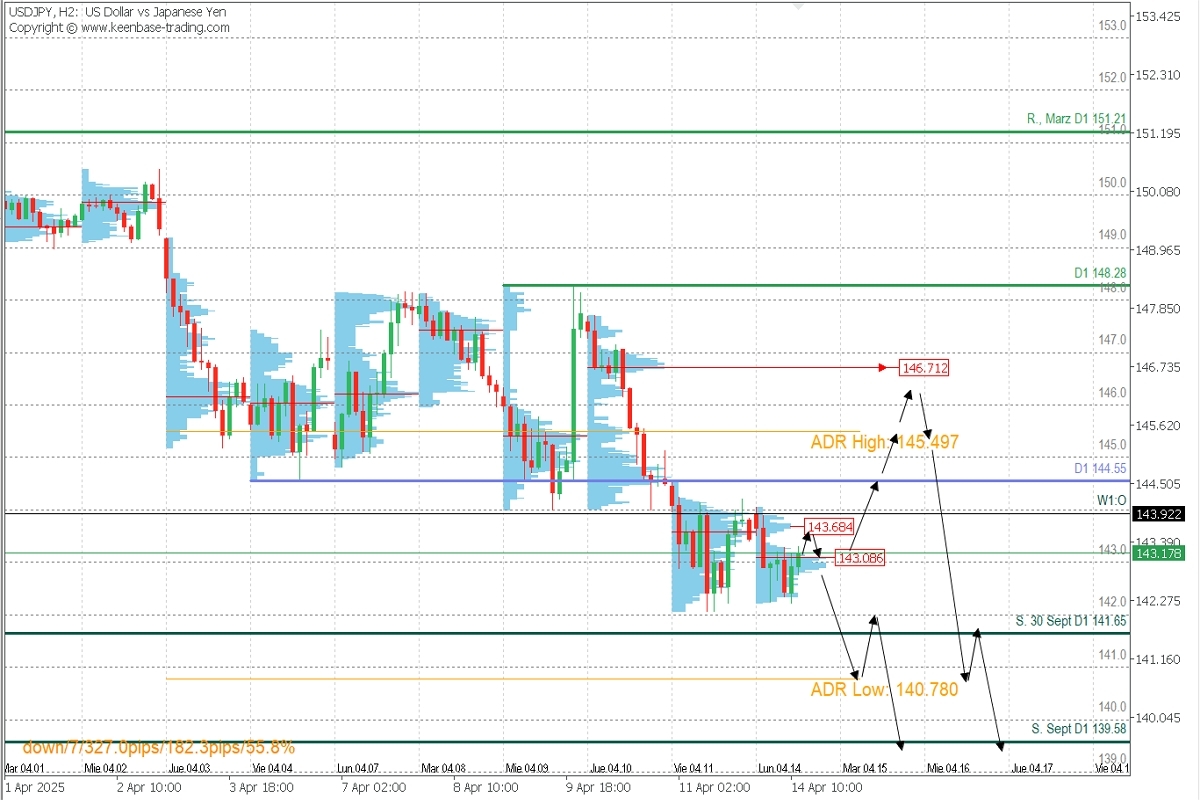

Technical Analysis | USDJPY, H2

- Supply Zones (Sell): 143.68, 144.55, 145.49, 146.71

- Demand Zones (Buy): 142.00, 141.00

The pair is showing intraday consolidation with a volume concentration zone at 143.08, a potential buying area. If respected as support, it could fuel a correction toward 144.00, 144.55, and extend toward the average daily bullish range at 145.49, where swing shorts may resume targeting the September support at 139.58.

The anticipated bearish scenario will be activated if price breaks decisively below 143.00 (with full-bodied candles), opening the path toward the September 30 support and the average daily bearish range at 140.78.

Technical Summary

- Corrective bullish scenario: Buy positions above 143.00 or 144.00 with TPs at 144.55, 145.00, and 145.49, from where swing selling can resume targeting 142.00 and 141.00.

- Anticipated bearish scenario: Sell positions below 143.00 with TPs at 142.00, 141.00, and 140.00.

Check out the EURJPY trading idea.

Exhaustion/Reversal Pattern (ERP): Before entering any trade in the key zones mentioned above, always wait for the formation and confirmation of an ERP on the M5 timeframe, like the ones taught here 👉 https://t.me/spanishfbs/2258

Uncovered POC: POC = Point of Control. This is the level or zone with the highest volume concentration. If a bearish move followed it, it is considered a sell zone and acts as resistance. Conversely, if a bullish impulse followed it, it is considered a buy zone, usually found at lows, and forms support zones.

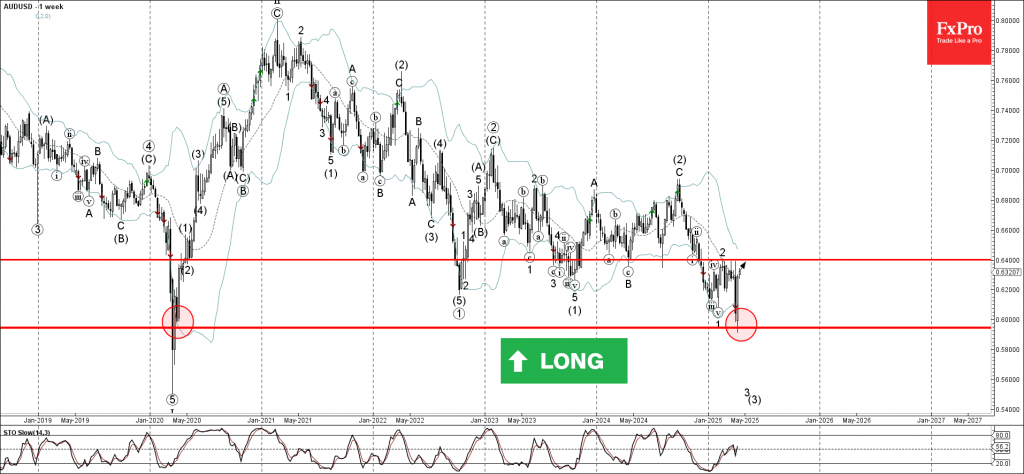

AUDUSD Wave Analysis

AUDUSD ⬆️ Buy

- AUDUSD reversed from the long-term support level 0.5945

- Likely to rise to resistance level 0.6400

AUDUSD currency pair recently reversed up from the support area between the major long-term support level 0.5945 (which started the sharp weekly uptrend in 2020) and the lower weekly Bollinger Band.

The upward reversal from this support area created the weekly Japanese candlesticks reversal pattern Bullish Engulfing – strong buy signal for AUDUSD .

Given the clear bullish divergence on the weekly Stochastic indicator and the strongly bearish US dollar sentiment, AUDUSD currency pair can be expected to rise to the next resistance level 0.6400.