Sample Category Title

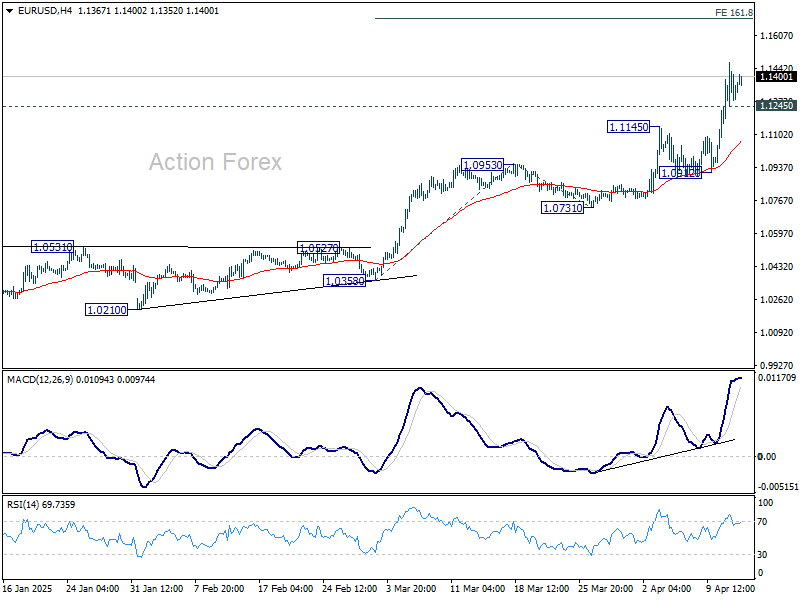

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1207; (P) 1.1340; (R1) 1.1494; More...

Intraday bias in EUR/USD remains on the upside at this point. Current rally should target 161.8% projection of 1.0358 to 1.0953 from 1.0731 at 1.1694. On the downside, below 1.1245 minor support will turn intraday bias neutral and bring consolidations. But downside should be contained above 1.0912 support to bring another rise.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0725) holds.

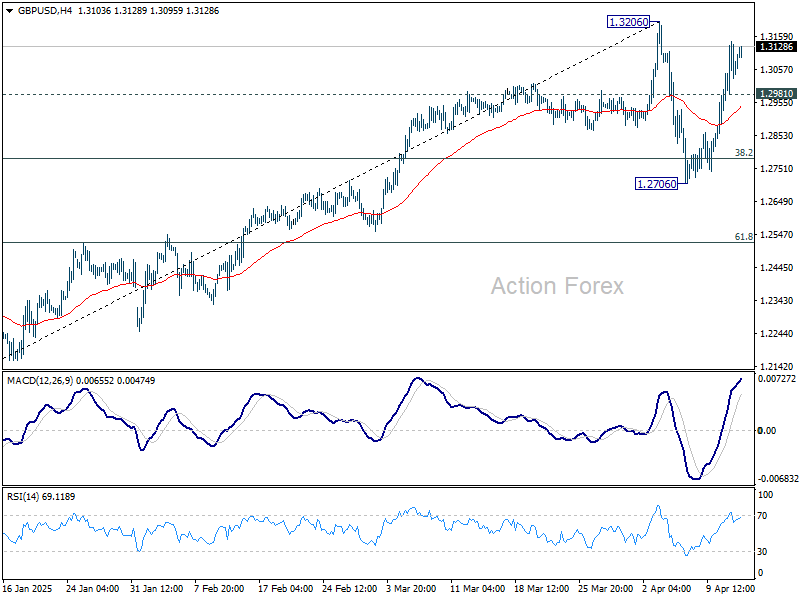

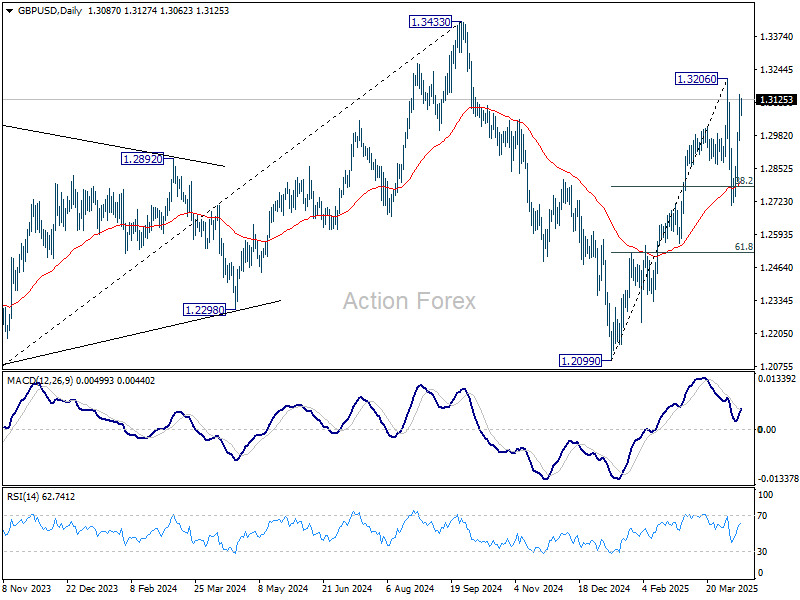

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2987; (P) 1.3067; (R1) 1.3168; More...

Intraday bias in GBP/USD remains on the upside for 1.3206 resistance. Firm break there will resume the rally from 1.2099 to retest 1.3433 high. On the downside, below 1.2981 minor support will turn intraday bias neutral again first. But overall near term outlook will stay bullish as long as 1.2706 support holds.

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could be the second leg. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on break of 1.3433 at a later stage.

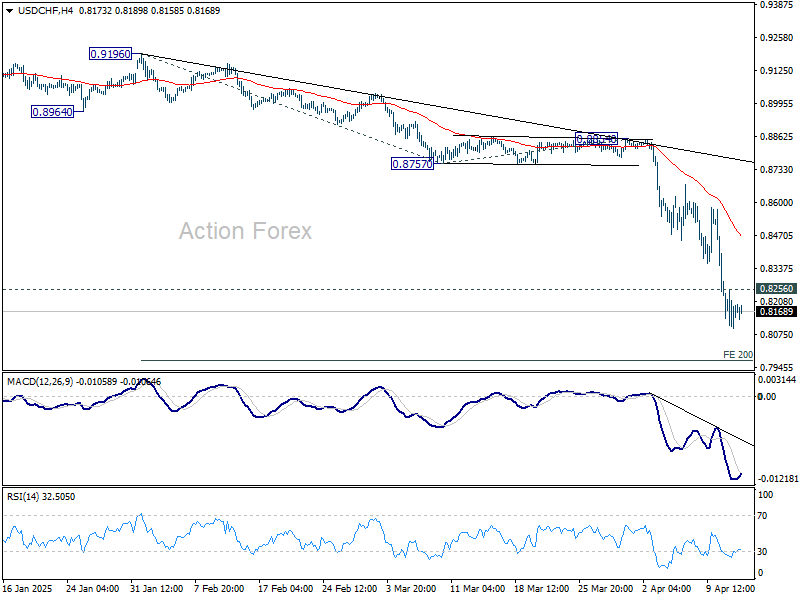

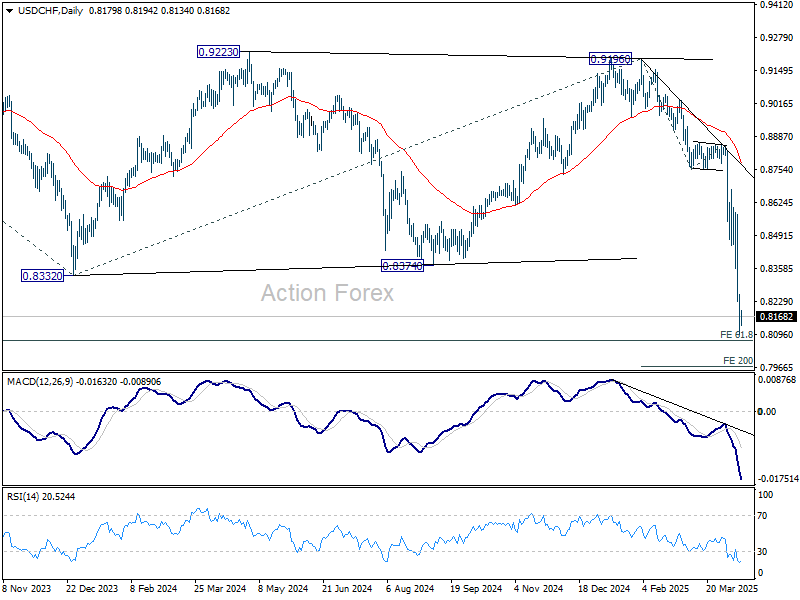

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8079; (P) 0.8173; (R1) 0.8246; More…

Intraday bias in USD/CHF stays on the downside at this point. Current down trend should target 200% projection of 0.9196 to 0.8757 from 0.8854 at 0.7976 next. On the upside, above 0.8256 minor resistance will turn intraday bias neutral and bring consolidations first, before staging another fall.

In the bigger picture, the break of 0.8332 (2023 low) confirms resumption of long term down trend from 1.0342 (2017 high). Next target is 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9196 at 0.8075. Firm break there will target 100% projection at 0.7382.

Markets Eye “Tariff Turmoil”

In focus this week

Markets are anxiously assessing US President Trump's next moves in the ongoing "Tariff Turmoil". At the time of writing, most countries face a 10% duty on most exports and a 25% tariff on cars, steel, aluminium as well as most goods from Canada and Mexico. Meanwhile China faces a 145% tariff, and we expect China to take even stronger measures than the already 125% tariff on US exports to boost domestic demand, potentially lowering the policy rate in the week after easter, but refrain from delivering a devaluation. In total this represents a substantial tightening of fiscal policy in the US - heightening recession risks. US retail sales data on Wednesday will be watched closely as an indicator of a potential slowdown in the economy.

In the euro area, we receive the final March inflation data on Wednesday. We expect the data to confirm the flash release, leading to no market reaction as focus has shifted from inflation towards growth concerns and the trade war.

On Thursday, the ECB is set to cut policy rates by 25bp to 2.25% in line with market pricing. We expect the statement to repeat "monetary policy is becoming meaningfully less restrictive" and Lagarde to highlight downside risks to growth while abstaining from giving any clear guidance on future rate decisions.

Economic and market news

What happened overnight

In the global trade war, US President Trump stated he would be announcing the tariff on semiconductors over the next week. He also remarked, "You have to show a certain flexibility. Nobody should be so rigid", while also launching a national security trade probe into the semiconductor sector. Meanwhile Chinese President Xi has embarked on his first foreign visit this year to Vietnam, Malaysia and Cambodia. Xi has previously called for greater cooperation with these countries to promote an "equal and orderly multi-polar world".

What happened over the weekend

In the global trade war, the Trump Administration excluded phones, chipmaking equipment and certain computers from the reciprocal tariffs, offering a brief moment of relief to the US tech sector. However, US commerce secretary Howard Lutnick has since cautioned that although these products are exempt from reciprocal tariffs, they are not excluded from the semiconductor tariffs anticipated before May this year.

In the US, the University of Michigan's preliminary consumer sentiment survey for April showed a significant decline in consumer sentiment while inflation expectations increased markedly, akin to the release in March. Sentiment declined to 50.8 from 57.0 (cons: 54.5), Current Conditions declined to 56.5 from 63.8 (cons: 61.5) and Expectations declined to 47.2 from 52.6 (cons: 50.8). 1Y inflation expectations increased to 6.7% from 5.0% (cons: 5.2) while ling-term inflation expectations increased to 4.4% from 4.1% (cons: 4.3).

The March PPI data showed a decline in Final Demand to 2.7% y/y from 3.2% y/y. This contrasts consensus estimates, which had anticipated a modest increase to 3.3%, likely due to expectations of producers preparing for tariffs increasing producer costs.

In Sweden, the final inflation data for March released in line with expectations, matching the flash estimates. The CPI was recorded at 0.5% y/y and CPIF came in at 2.3% y/y. Food inflation accelerated, while inflation in clothing and footwear, transport, housing and utilities declined. Overall, annual inflation readings have remained below the Riksbank's 2% target for 8 consecutive months.

Equities: Equities were generally higher on Friday, with US stocks outperforming Europe as investors rejoiced on tariff exceptions on tech. Exactly what tech products that will be exempted is not clear, but Trump will give more details today. As such, Apple was the standout on Friday. S&P 500 added 1.8% and thereby locking in an average annual equity return in one week - 8%. European equities have been more still, with Stoxx 600 unchanged both on Friday and for the week, though futures point sharply higher when markets open. It should also be noted that Europe is still outperforming US on YTD horizon. The rally appears to linger today, with European futures in catch-up and US futures another 1% higher.

FI&FX: EUR/USD slipped below 1.13 in early trading Friday as Trump's tariff exemptions on China tempered US recession concerns, providing initial support for the broad USD. With risks of a confidence crisis in USD assets still lingering and several typical market correlations breaking down, the main focus remains on whether easing tariff headlines will be sufficient to stabilise the ongoing sell-off in the USD and Treasuries, as lost credibility may prove difficult to restore. The divergence between US and European rates has been striking during last week's trading sessions. 10Y Bund yields ended the week close to unchanged at 2.55% while 10Y UST rose more than 50bp to just below 4.50% during Friday's session. NOK and SEK remain challenged with the global investment environment taking centre stage.

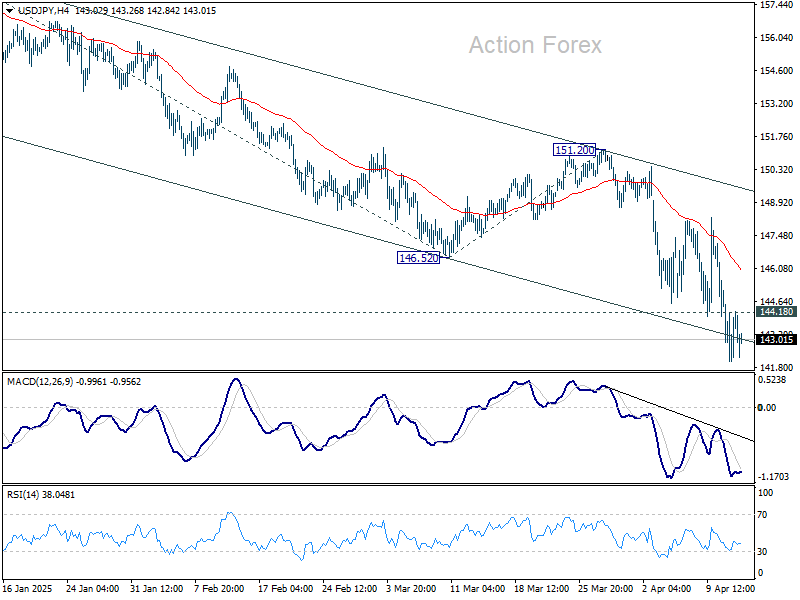

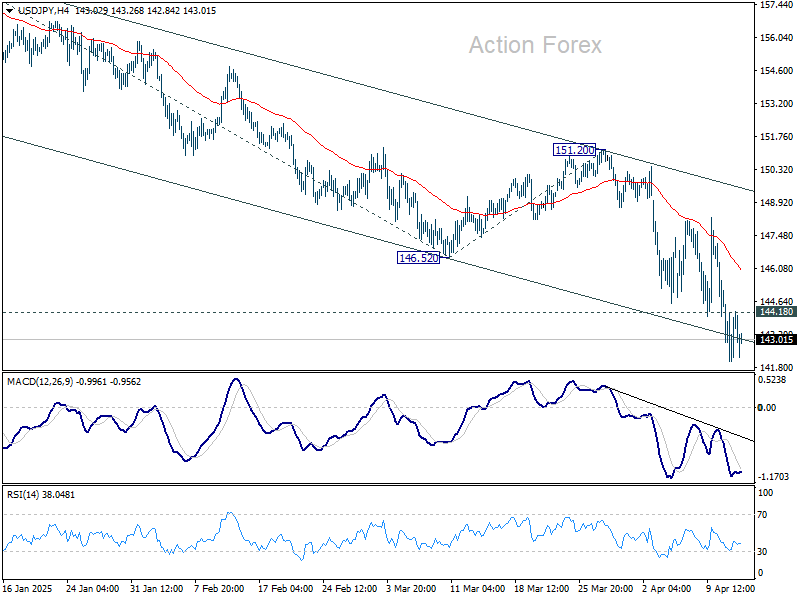

USD/JPY Daily Outlook

Daily Pivots: (S1) 142.16; (P) 143.44; (R1) 144.81; More...

Intraday bias in USD/JPY remains on the downside for the moment. Current fall from 158.86 is in progress to 139.57 support. On the upside, above 144.18 minor resistance will turn intraday bias neutral first. But outlook will stay bearish as long as 151.20 resistance holds, in case of recovery.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Markets Catch Breath After Tariff Chaos; Focus Turns to BoC, ECB and Economic Data

Financial markets opened the week on a relatively steady footing in Asia, offering investors a brief respite after last week's extreme volatility driven by US tariff chaos. Major stock indexes are trading higher, though gains appear more a product of technical consolidation than renewed optimism.

In currency markets, most major pairs and crosses are contained within Friday’s range. The exception is some Kiwi pairs, which have moved with a bit more momentum. For now, it appears that volatility has pulled back from the extremes seen over the past two weeks, giving investors a brief window of breathing space.

Nevertheless, confusion around U.S. tariff policy continues to muddy the waters. Reports emerged over the weekend that key Chinese exports such as smartphones and computers would not be subject to the full 145% tariff hike. Instead, they would face a 20% rate. However, U.S. President Donald Trump quickly reignited uncertainty by stating he would announce a separate tariff on semiconductors next week, alongside a new national security probe targeting the chip sector. This piecemeal, ad hoc rollout is making it difficult for markets to price in risk or clarity.

On the diplomatic front, Chinese President Xi Jinping’s visit to Vietnam signals a strategic push to shore up regional supply chains as China faces growing trade isolation from the US. Xi’s trip, which also includes stops in Cambodia and Malaysia, highlights Beijing’s urgency in hedging against further decoupling with the US. Meanwhile, Vietnam is caught in the middle — a beneficiary of supply chain shifts, but also under scrutiny from Washington, facing a potential 46% US tariff if it fails to enforce tighter rules of origin.

Looking ahead, the spotlight will shift BoC and ECB rate decisions, both facing the delicate balancing act of responding to weakening growth and potential inflationary shocks from tariffs. Meanwhile, a heavy slate of data—including US retail sales, Germany’s ZEW survey, UK employment and CPI, New Zealand’s inflation report, and China’s Q1 GDP—will provide further clues on the economic fallout of the trade conflict.

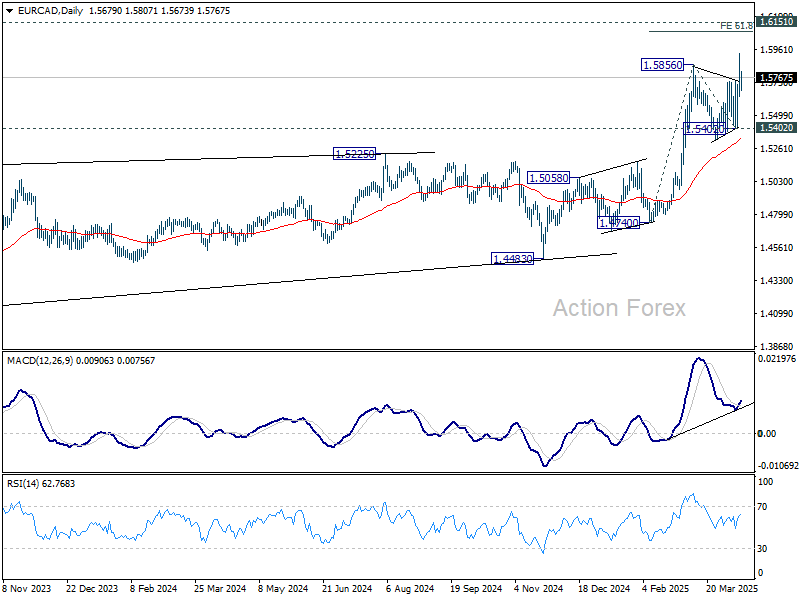

Technically, EUR/CAD's late break of 1.5856 resistance last week indicates medium term up trend resumption. Near term outlook will now stay bullish as long as 1.5402 support holds. Next target is 61.8% projection of 1.4740 to 1.5856 from 1.5402 at 1.6092. That would be close to 1.6151 key long term resistance (2018 high).

In Asia, at the time of writing, Nikkei is up 1.91%. Hong Kong HSI is up 2.43%. China Shanghai SSE is up 0.70%. Singapore Strait Times is up 1.54%. Japan 10-year JGB yield is down -0.012 at 1.334.

BoJ's Ueda: US tariffs add downside risks to Japan through various channels

BoJ Governor Kazuo Ueda warned today that the recently imposed U.S. tariffs are likely to exert “downward pressure” on both the global and Japanese economies through “various channels.”

While he did not specify the transmission mechanisms, the remarks reflect growing concerns that escalating trade tensions could weigh on exports, dampen corporate sentiment, disrupt supply chains, as well as trigger volatility in the financial markets including currencies.

Ueda reiterated BoJ’s commitment to achieving its 2% inflation target sustainably, noting that monetary policy would be guided appropriately based on evolving economic, price, and financial developments. He emphasized that the central bank will maintain a data-dependent approach and continue to scrutinize conditions “without any pre-conception”.

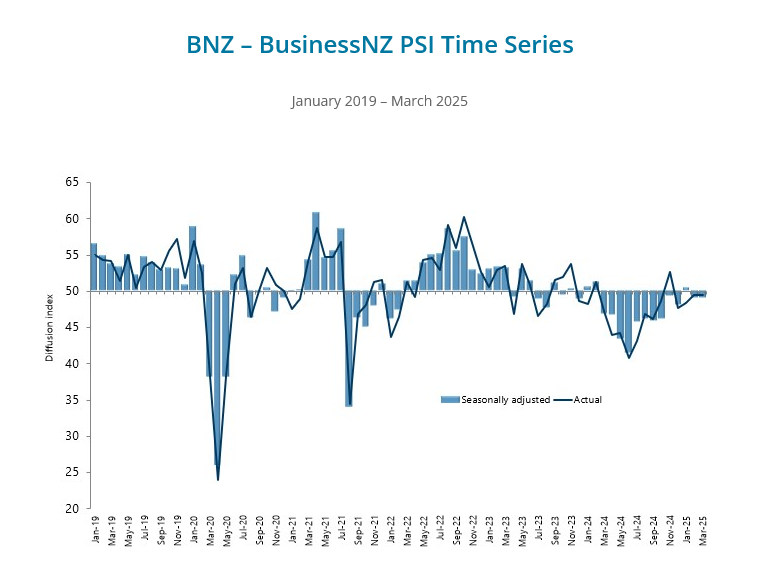

NZ BNZ services rises to 49.1, subdued despite hints of stabilization

New Zealand’s services sector remained in contraction in March, with the BusinessNZ Performance of Services Index inching up slightly to 49.1 from 49.0. This marks another month below the long-run average of 53.0 highlighting the ongoing weakness.

While the headline improvement was minimal, underlying components showed a mixed picture—activity/sales dropped from 49.1 to 47.4. But new orders/business climbed from 49.5 to 50.8, the highest since February 2024, suggesting some pickup in future demand. Employment rose from 49.1 to 50.2, ending a 15-month streak of contraction, and offering early signs that firms may be regaining confidence in hiring.

The share of negative comments from survey participants fell slightly to 56.7%, with ongoing concerns about high interest rates, inflation, weak consumer sentiment, and broader economic uncertainty. Businesses also cited external pressures such as global tariffs and rising input costs.

China’s export surge 12.4% yoy in Mar, imports down -4.3% yoy

China's exports jumped an impressive 12.4% yoy to USD 313.9B in March, significantly beating expectations of 4.4% yoy and marking a sharp acceleration from the 2.3% yoy growth recorded in January-February.

Particularly notable was the 9.18% yoy rise in shipments to the US, likely due to front-loading ahead of tariff tensions. Exports to ASEAN also strengthened with 11.6% yoy growth , with double-digit growth to major partners like Thailand (27.8% yoy) and Vietnam (18.9% yoy).

However, Vietnam, a key intermediary in China's export supply chain, is now under pressure to tighten controls on the origin of goods and materials. According to a ministry document, authorities in Hanoi are urging companies to clamp down on origin fraud to avoid punitive US tariffs, highlighting growing scrutiny on Chinese goods routed through third countries.

Meanwhile, the strength in exports contrasted with a -4.3% yoy decline in imports, resulting in a larger-than-expected trade surplus of USD 102.6B.

Fed's Kashkari: Markets searching for "new normal" amid trade policy uncertainty

Minneapolis Fed President Neel Kashkari acknowledged over the weekend that global investors are grappling with deep uncertainty surrounding the direction of US trade and fiscal policy. Speaking on CBS’s Face the Nation, Kashkari said the bond market’s recent volatility reflects an effort to “determine what is the new normal in America,” particularly regarding long-term Treasury yields.

He emphasized that Fed has “zero ability” to influence that end point, which he said is shaped entirely by trade negotiations and fiscal decisions coming out of Washington.

Kashkari underlined that tariffs are inherently inflationary, but the key question is whether their effect on prices will be temporary or more sustained. “Tariffs push up prices and push down economic activity,” he noted, describing it as a difficult scenario in which Fed’s tools are limited. The central bank’s role, he added, is "to make sure that it's only a one time adjustment in prices and nothing longer term than that."

He also made clear that monetary policy alone cannot undo the economic drag from a trade war. As the market digests new rounds of tariffs, retaliation, and policy reversals, Kashkari said, “we’re going to have to watch and see.”

"We can just keep inflation from getting out of hand," he added.

Tariff Shockwaves Test BoC and ECB Resolve

Markets head into the holiday-shortened week with anticipation as a string of key central bank decisions including BoC and ECB, as well as critical economic data are featured.

BoC meeting is shaping up to be one of the most uncertain in the past two years. Markets are split, with investors pricing in roughly a 60% chance that BoC will pause its easing cycle this week. After cutting rates again in March, the central bank emphasized that it would "proceed carefully with any further changes" due the growing complexity in the economic outlook.

The key dilemma for BoC is whether they prioritize tackling inflation risks from tariff pass-through or opt for a preemptive cut to support growth. If the BoC tilts toward the latter, it could deliver a pre-emptive 25 bps rate cut to continue its path toward a less restrictive 2.50% rate.

The decisive factor could be the March CPI data, released a day ahead of the policy announcement. If the report confirms that February’s surprise spike in both headline and core inflation was indeed transitory, BoC would have sufficient cover to proceed with another rate cut. Otherwise, a hold is the more cautious move.

ECB is also in the spotlight. According to a Reuters poll, 61 of 71 economists expect a 25bps cut to the deposit rate, bringing it down to 2.25%. A further cut to 2.00% is widely anticipated for June. While ECB policymakers have largely avoided clear forward guidance amid the rapidly shifting trade environment, the general tone suggests a growing focus on downside risks to growth rather than inflation persistence.

In Australia, minutes of RBA’s April meeting are expected to reiterate the central bank’s cautious tone and reluctance to commit to further easing just yet. However, labor market data later in the week could test RBA’s resolve. A weaker-than-expected jobs report would likely increase market bets that RBA will restart rate cuts in May. Ultimately though, Q1 CPI data due on April 30 remains the definitive piece of the policy puzzle.

On the data front, U.S. retail sales will be a critical gauge of how much the tariff-induced uncertainty has dampened actual household spending. Meanwhile, Germany’s ZEW economic sentiment index should offer a timely look at how sharply European business confidence has been hit by the escalating trade war. Other key releases include UK employment figures and CPI data, New Zealand’s CPI, and China’s Q1 GDP.

Here are some highlights for the week:

- Monday: New Zealand BNZ services; China trade balance; Swiss PPI; Canada wholesale sales.

- Tuesday: RBA minutes; UK employment; German ZEW economic sentiment; Eurozone industrial production; Canada CPI, manufacturing sales; US Empire state manufacturing, import prices.

- Wednesday: Japan machine orders; China GDP, industrial production, retail sales, fixed asset investment; UK CPI; Eurozone CPI final; US retail sales, industrial production, NAHB housing index; BoC rate decision.

- Thursday: New Zealand CPI; Australia employment; Japan trade balance; Swiss France balance; ECB rate decision; US jobless claims, Philly Fed survey, building permits and housing starts.

- Friday: Japan CPI.

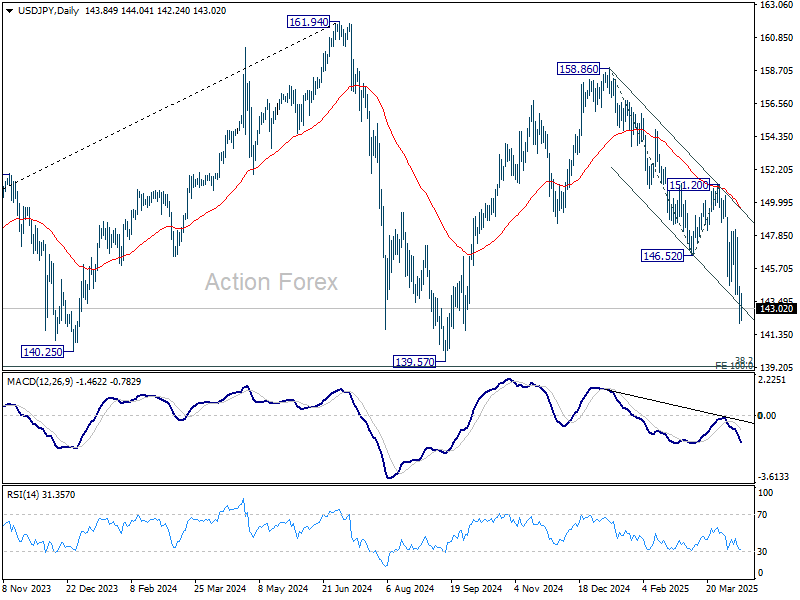

USD/JPY Daily Outlook

Daily Pivots: (S1) 142.16; (P) 143.44; (R1) 144.81; More...

Intraday bias in USD/JPY remains on the downside for the moment. Current fall from 158.86 is in progress to 139.57 support. On the upside, above 144.18 minor resistance will turn intraday bias neutral first. But outlook will stay bearish as long as 151.20 resistance holds, in case of recovery.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

China’s exports surge 12.4% yoy in Mar, imports down -4.3% yoy

China's exports jumped an impressive 12.4% yoy to USD 313.9B in March, significantly beating expectations of 4.4% yoy and marking a sharp acceleration from the 2.3% yoy growth recorded in January-February.

Particularly notable was the 9.18% yoy rise in shipments to the US, likely due to front-loading ahead of tariff tensions. Exports to ASEAN also strengthened with 11.6% yoy growth , with double-digit growth to major partners like Thailand (27.8% yoy) and Vietnam (18.9% yoy).

However, Vietnam, a key intermediary in China's export supply chain, is now under pressure to tighten controls on the origin of goods and materials. According to a ministry document, authorities in Hanoi are urging companies to clamp down on origin fraud to avoid punitive US tariffs, highlighting growing scrutiny on Chinese goods routed through third countries.

Meanwhile, the strength in exports contrasted with a -4.3% yoy decline in imports, resulting in a larger-than-expected trade surplus of USD 102.6B.

BoJ’s Ueda: US tariffs add downside risks to Japan through various channels

BoJ Governor Kazuo Ueda warned today that the recently imposed U.S. tariffs are likely to exert “downward pressure” on both the global and Japanese economies through “various channels.”

While he did not specify the transmission mechanisms, the remarks reflect growing concerns that escalating trade tensions could weigh on exports, dampen corporate sentiment, disrupt supply chains, as well as trigger volatility in the financial markets including currencies.

Ueda reiterated BoJ’s commitment to achieving its 2% inflation target sustainably, noting that monetary policy would be guided appropriately based on evolving economic, price, and financial developments. He emphasized that the central bank will maintain a data-dependent approach and continue to scrutinize conditions “without any pre-conception”.

NZ BNZ services rises to 49.1, subdued despite hints of stabilization

New Zealand’s services sector remained in contraction in March, with the BusinessNZ Performance of Services Index inching up slightly to 49.1 from 49.0. This marks another month below the long-run average of 53.0 highlighting the ongoing weakness.

While the headline improvement was minimal, underlying components showed a mixed picture—activity/sales dropped from 49.1 to 47.4. But new orders/business climbed from 49.5 to 50.8, the highest since February 2024, suggesting some pickup in future demand. Employment rose from 49.1 to 50.2, ending a 15-month streak of contraction, and offering early signs that firms may be regaining confidence in hiring.

The share of negative comments from survey participants fell slightly to 56.7%, with ongoing concerns about high interest rates, inflation, weak consumer sentiment, and broader economic uncertainty. Businesses also cited external pressures such as global tariffs and rising input costs.

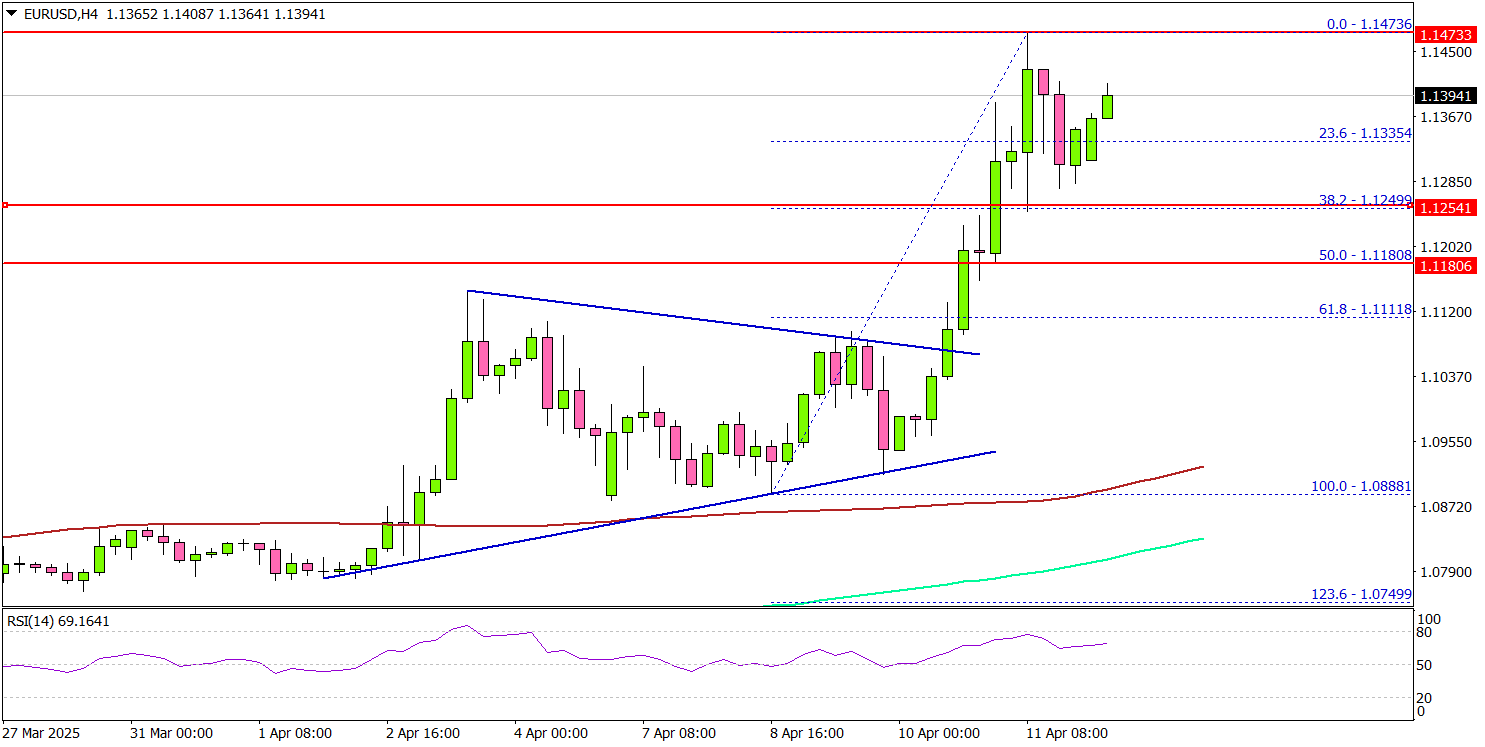

EUR/USD Gains Traction, Bulls Aim For 1.1500

Key Highlights

- EUR/USD started a fresh increase above the 1.1200 resistance.

- It broke a key contracting triangle with resistance at 1.1035 on the 4-hour chart.

- GBP/USD is again rising and might aim for gains above 1.3120.

- Gold prices rallied further and traded to a new record high above $3,200.

EUR/USD Technical Analysis

The Euro remained supported above 1.0880 against the US Dollar. EUR/USD started a fresh surge above the 1.1000 and 1.1050 resistance levels.

Looking at the 4-hour chart, the pair broke a key contracting triangle with resistance at 1.1035. There was a close above the 1.1200 resistance, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour).

The bulls pumped the pair above the 1.1350 and 1.1400 levels. A high was formed at 1.1473 and is currently consolidating gains. If there is a fresh increase, the pair could face resistance near the 1.1420 level.

The next major resistance is near the 1.1450 level. The main resistance is now forming near the 1.1500 zone. A close above the 1.1500 level could set the tone for another increase. In the stated case, the pair could even clear the 1.1550 resistance.

On the downside, immediate support sits near the 1.1320 level. The next key support sits near the 1.1250 level. Any more losses could send the pair toward the 1.1200 level.

Looking at Gold, the price started a fresh increase, and the bulls might soon aim for a move toward the $3,280 level.

Upcoming Economic Events:

- Fed's Waller speech.

- Fed's Harker speech.