Sample Category Title

AUD/USD Weekly Report

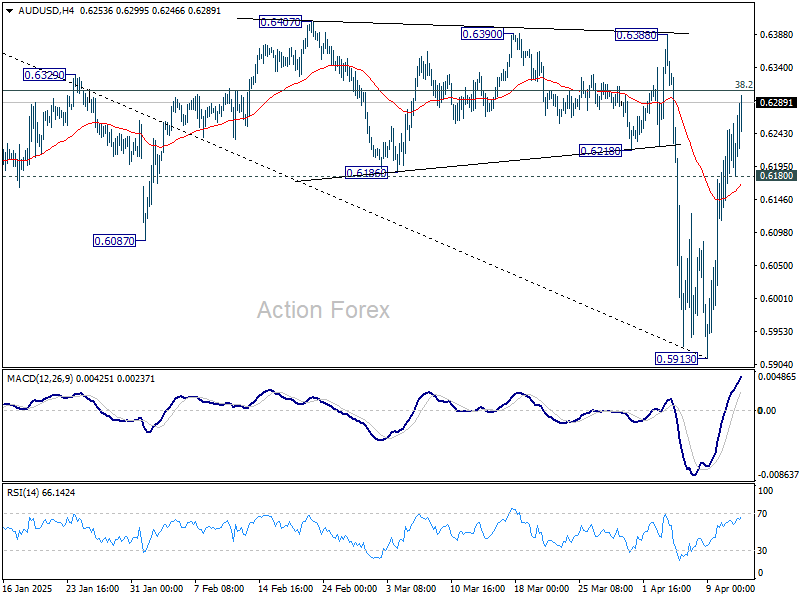

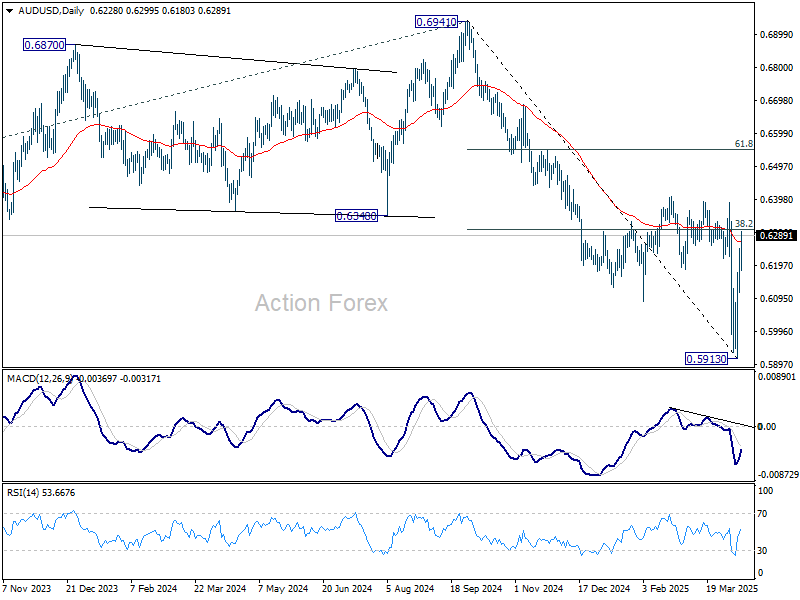

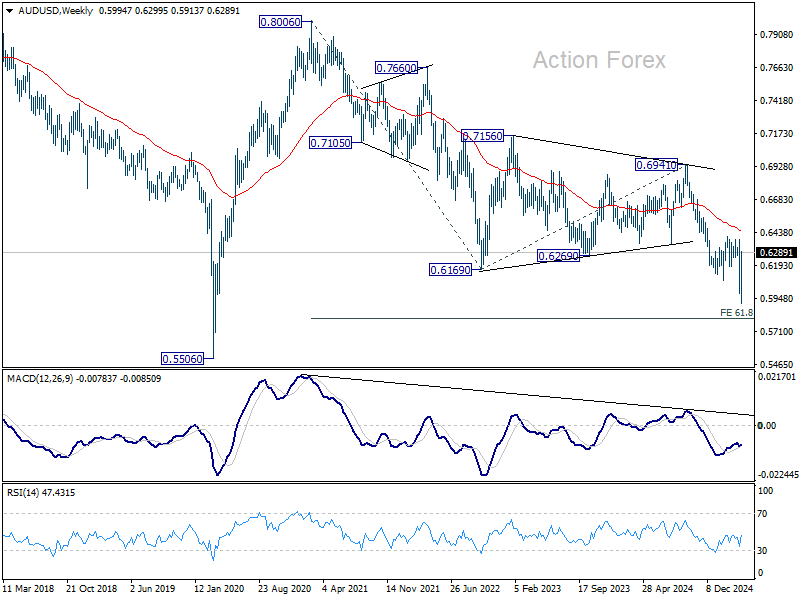

AUD/USD's extended rebound last week confirms short term bottom at 0.5913. Rebound from there is currently seen as a corrective move first. Initial bias stays on the upside this week for 38.2% retracement of 0.6941 to 0.5913 at 0.6316. Sustained break there will target 61.8% retracement at 0.6548. On the downside, below 0.6180 minor support will turn intraday bias neutral again first.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. However, sustained trading above 55 W EMA (now at 0.6446) will argue that a medium term bottom was already formed, and set up further rebound to 0.6941 resistance instead.

In the long term picture, prior rejection by 55 M EMA (now at 0.6764) is taken as a bearish signal. But for now, fall from 0.8006 is still seen as the second leg of the corrective pattern from 0.5506 long term bottom (2020 low). Hence, in case of deeper decline, strong support should emerge above 0.5506 to contain downside to bring reversal. However, this view is subject to adjustment if current decline accelerates further.

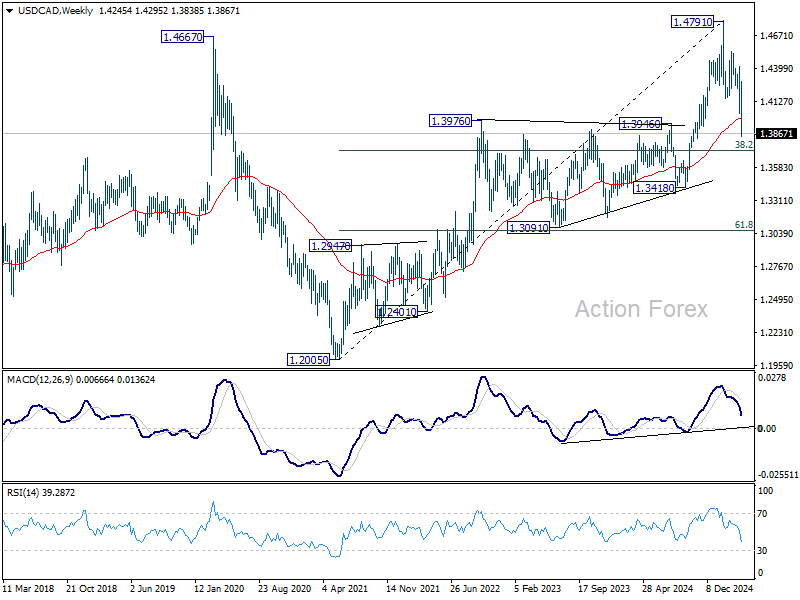

USD/CAD Weekly Outlook

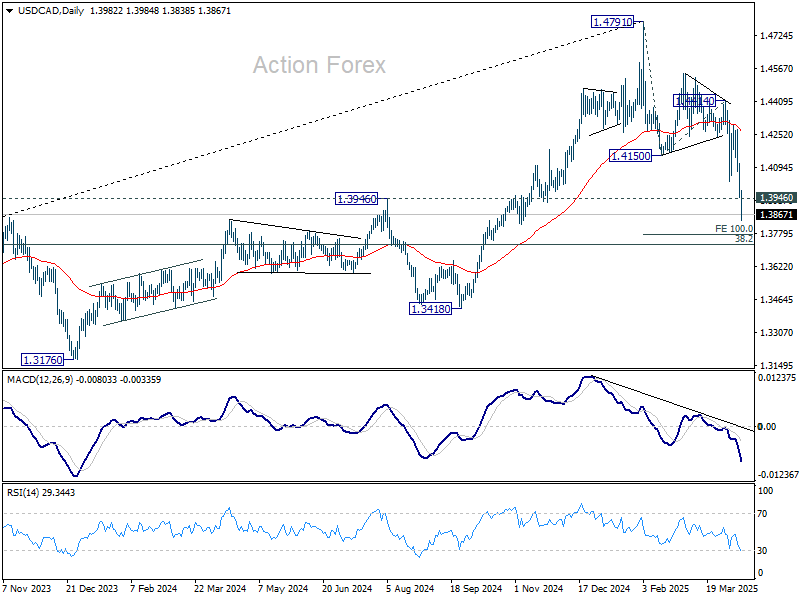

USD/CAD's fall from 1.4791 high continued last week and accelerated through 1.3946/76 key support zone. There is no sign of bottoming yet. Initial bias stays on the downside this week for 100% projection of 1.4791 to 1.4150 from 1.4414 at 1.3773. On the upside, break of 1.4150 support turned resistance is needed to indicate short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, the break of 1.3976 resistance turned support (2022 high) and 55 W EMA (now at 1.3992) indicates that a medium term is already in place at 1.4791. Fall from there would either be a correction to rise from 1.2005, or trend reversal. In either case, firm break of 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727 will pave the way back to 61.8% retracement at 1.3069.

In the long term picture, as long as 55 M EMA (now at 1.3479) holds, up trend from 0.9056 (2007 low) should still resume through 1.4791 at a later stage. However, sustained trading below 55 M EMA will argue that the up trend has already completed, with rise from 1.2005 to 1.4791 as the fifth wave. 1.4791 would then be seen as a long term top and deeper medium term correction should then follow.

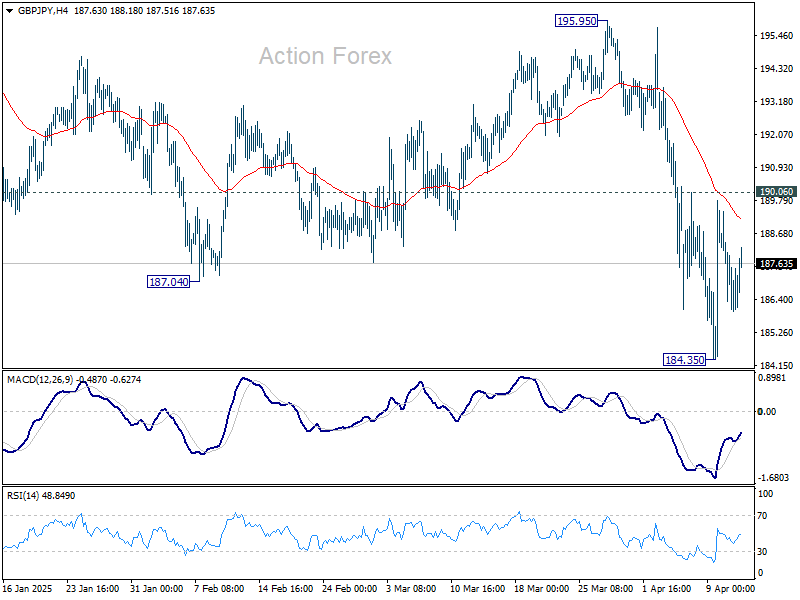

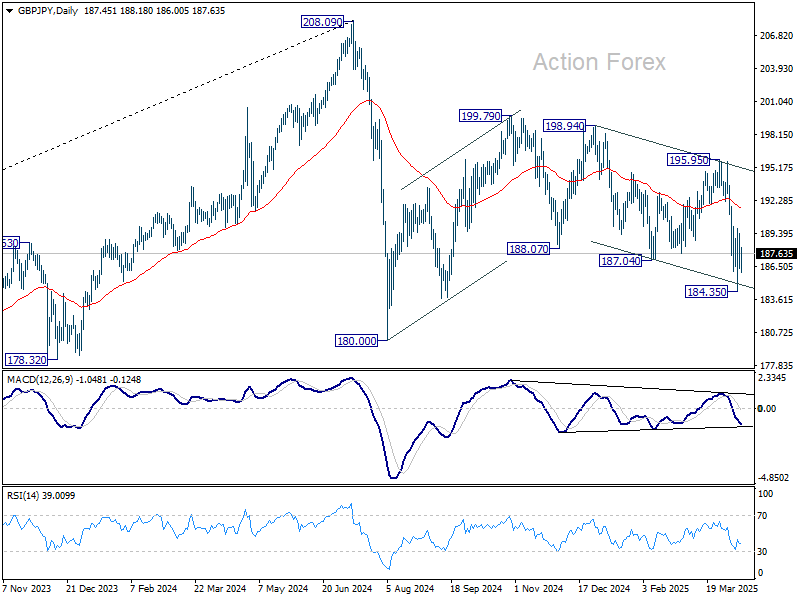

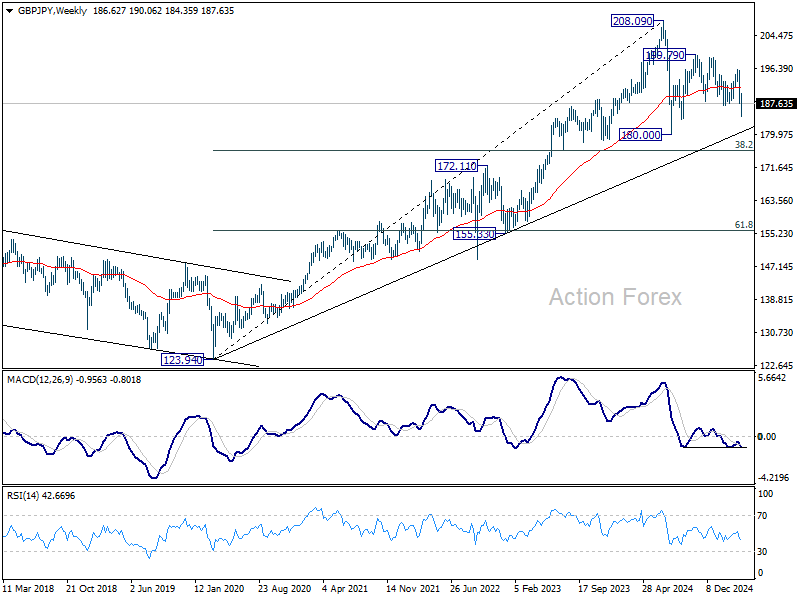

GBP/JPY Weekly Outlook

GBP/JPY's decline from 199.79 resumed last week and fell to 184.35, but then recovered. Initial bias stays neutral this week first and some more consolidations would be seen. Risk will stay on the downside as long as 190.06 resistance holds. Below 184.35 will target 180.00 low. Nevertheless, break of 190.06 will turn bias back to the upside for stronger rebound.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 175.94 will bring deeper fall even still as a correction.

In the longer term picture, while a medium term top was formed at 208.09 (2024 high), it's still early to conclude that the up trend from 122.75 (2016 low) has completed. But GBP/JPY is at least in a medium term corrective phase, with risk of correction to 55 M EMA (now at 175.14).

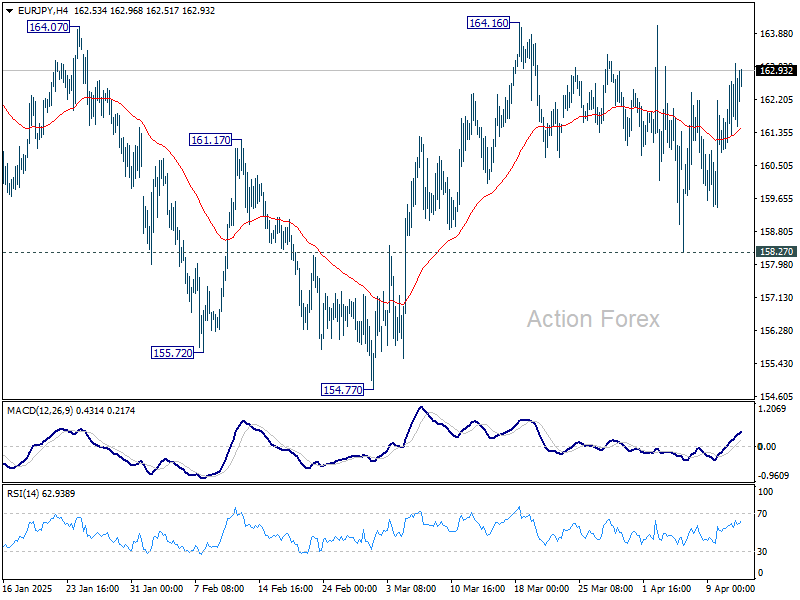

EUR/JPY Weekly Outlook

EUR/JPY dipped further to 158.27 last week but recovered recovered. Initial bias remains neutral this week first. On the upside, above 164.16 will resume the rally from 154.77 to 164.89 resistance, and then 166.67. However, decisive break of 158.27 support will bring deeper decline back to 154.77 support. Overall, sideway consolidation pattern from 154.40 is still extending.

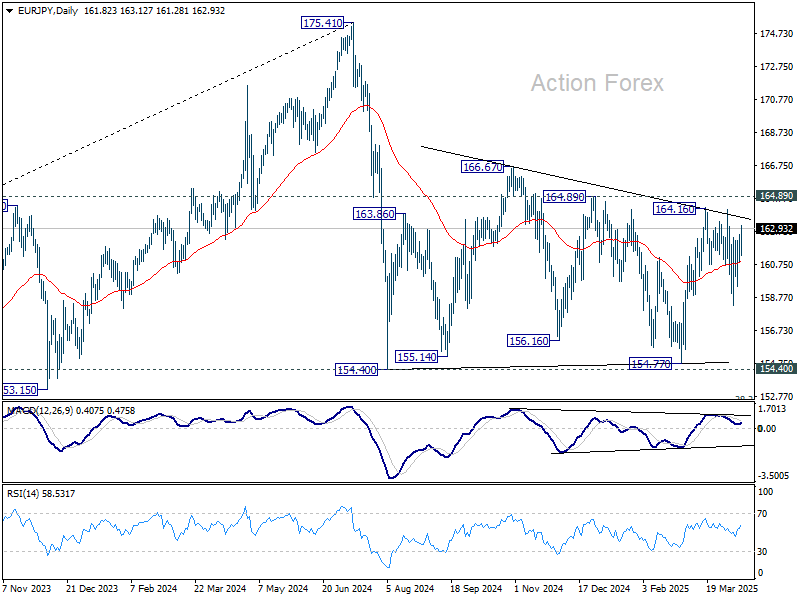

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

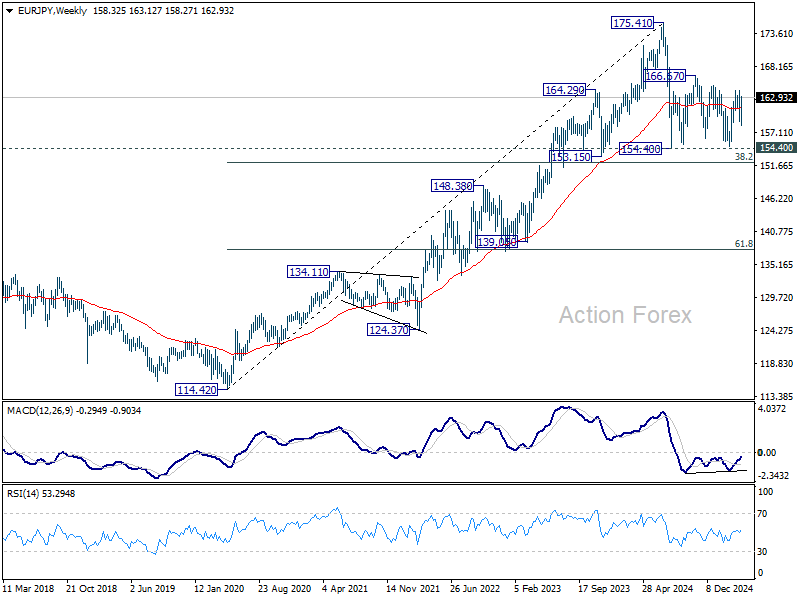

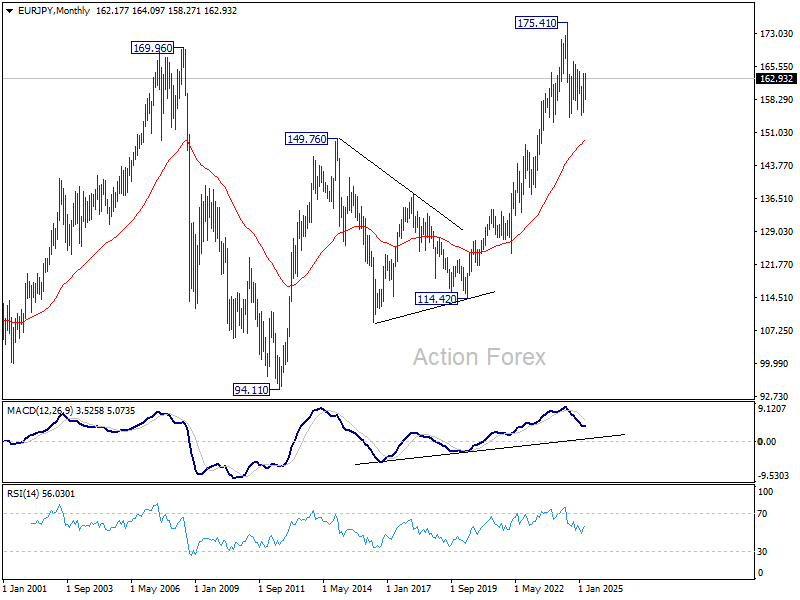

In the long term picture, while 175.41 is at least a medium term top, it's still early to conclude that up trend from 94.11 (2012 low) has completed. A medium term corrective phase is in progress with risk of deeper fall back to 55 M EMA (now at 149.44).

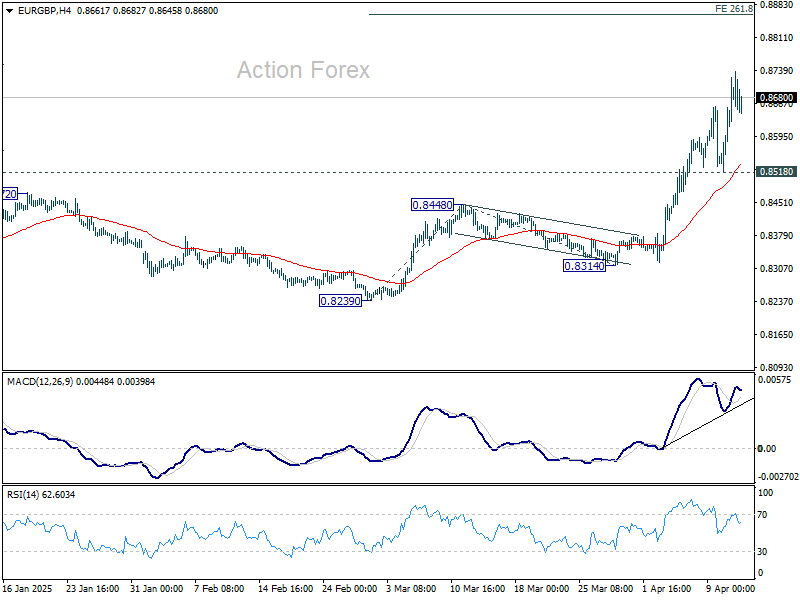

EUR/GBP Weekly Outlook

EUR/GBP's rally from 0.8221 continued last week and broke 0.8624 cluster resistance decisively. Initial bias remains on the upside this week. Next target is 261.8% projection of 0.8239 to 0.8448 from 0.8314 at 0.8861. On the downside, break of 0.8518 support is needed to indicate short term topping. Otherwise, outlook will stay bullish in case of retreat.

In the bigger picture, firm break of 0.8624 cluster resistance (38.2% retracement of 0.9267 to 0.8221 at 0.8621) should confirm the case of bullish trend reversal. That is, down trend from 0.9267 (2022 high) has completed at 0.8221, just ahead of 0.9201 key support (2024 low). Further rise should be seen to 61.8% retracement at 0.8867 next. This will now remain the favored case as long as 0.8472 resistance turned support holds.

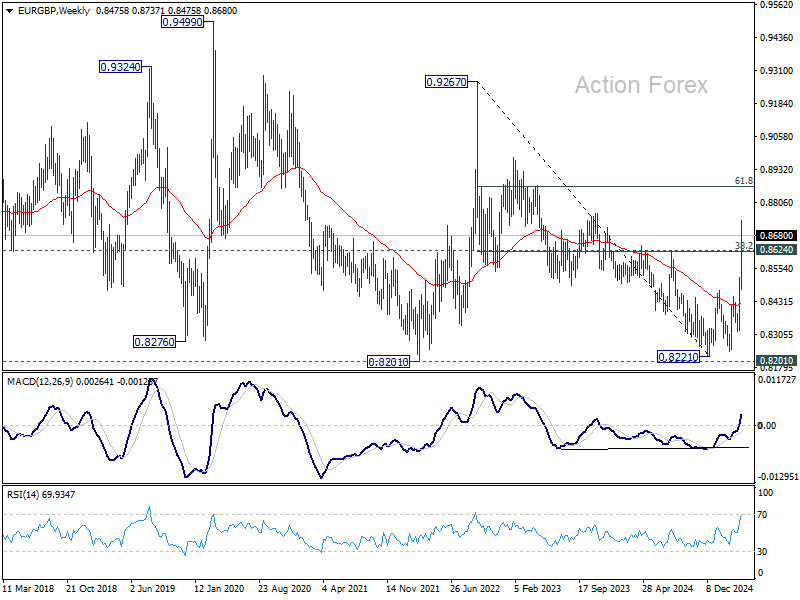

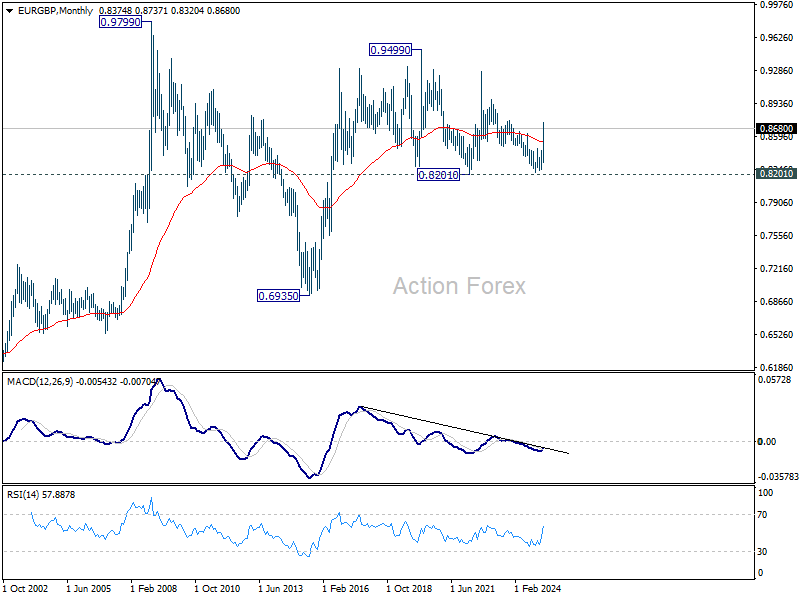

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Range trading should continue between 0.8201 and 0.9499, until there is clear signal of imminent breakout.

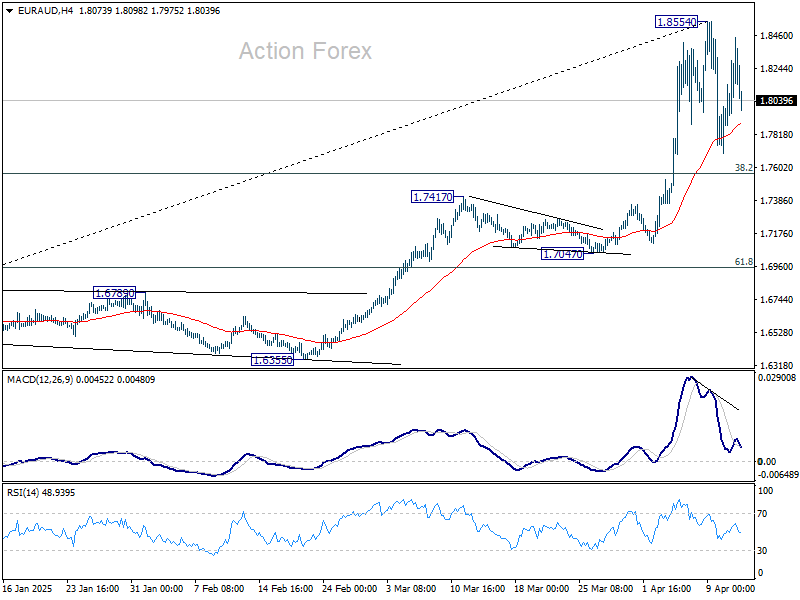

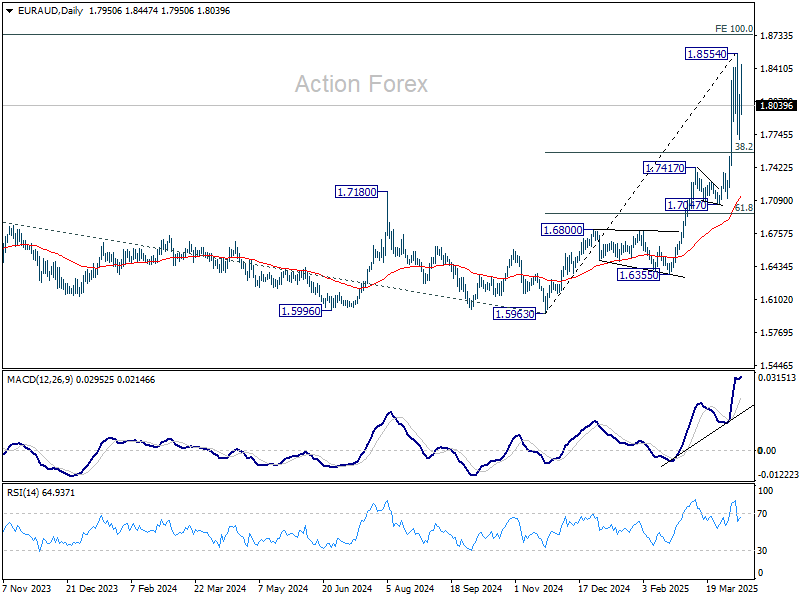

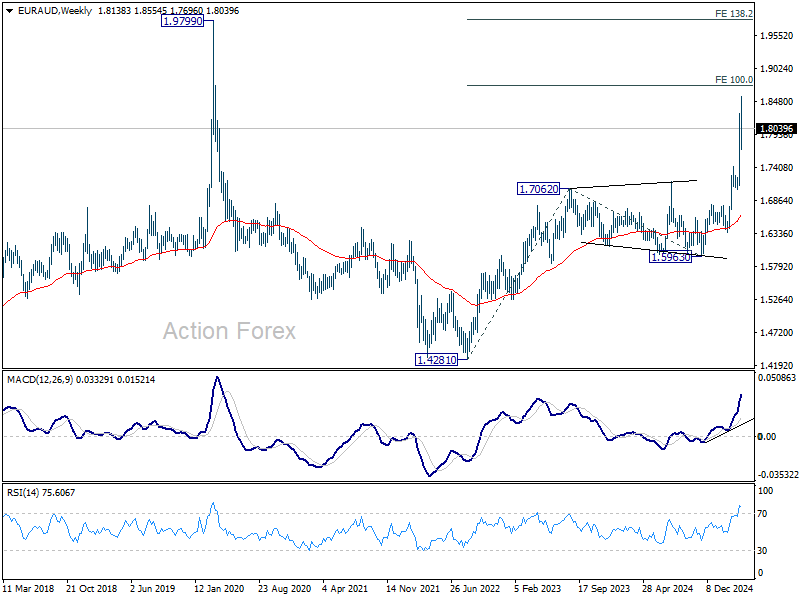

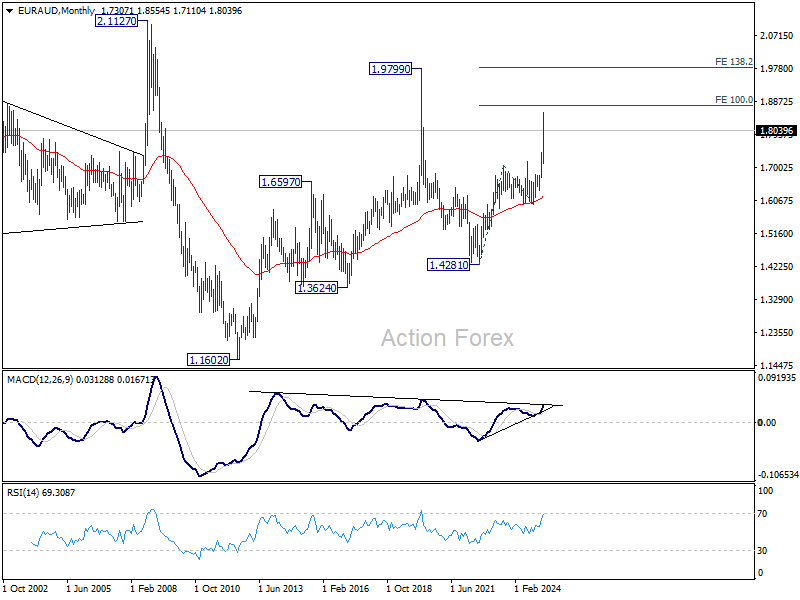

EUR/AUD Weekly Outlook

EUR/AUD edged higher to 1.8854 last week but formed a short term top there. Initial bias remains neutral this week and more consolidations could be seen. Downside of retreat should be contained by 38.2% retracement of 1.5963 to 1.8854 at 1.7750. On the upside, firm break of 1.8554 will resume larger up trend.

In the bigger picture, up trend from 1.4281 (2022 low) is in progress. Next target is 100% projection of 1.4281 to 1.7062 from 1.5963 at 1.8744. Firm break there will pave the way to 138.2% projection at 1.9806, which is close to 1.9799 (2020 high). Outlook will remain bullish as long as 1.7417 resistance turned support holds even in case of deep pullback.

In the longer term picture, rise from 1.4281 is seen as the second leg of the pattern from 1.9799 (2020 high), which is part of the pattern from 2.1127 (2008 high). As long as 55 M EMA (now at 1.6213) holds, this second leg could still extend higher. However, firm break of the above mention 1.8744 projection level with strong momentum will argue that it's indeed resuming the up trend form 1.1602 (2012 low).

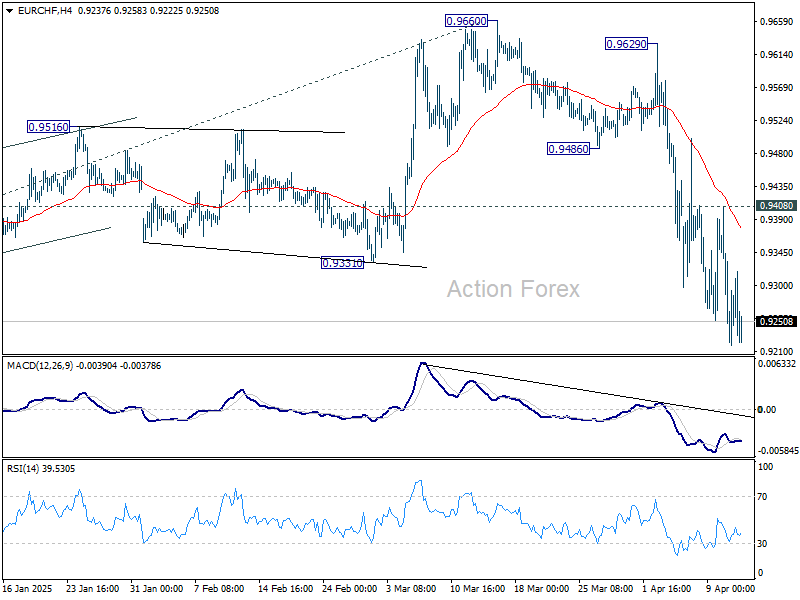

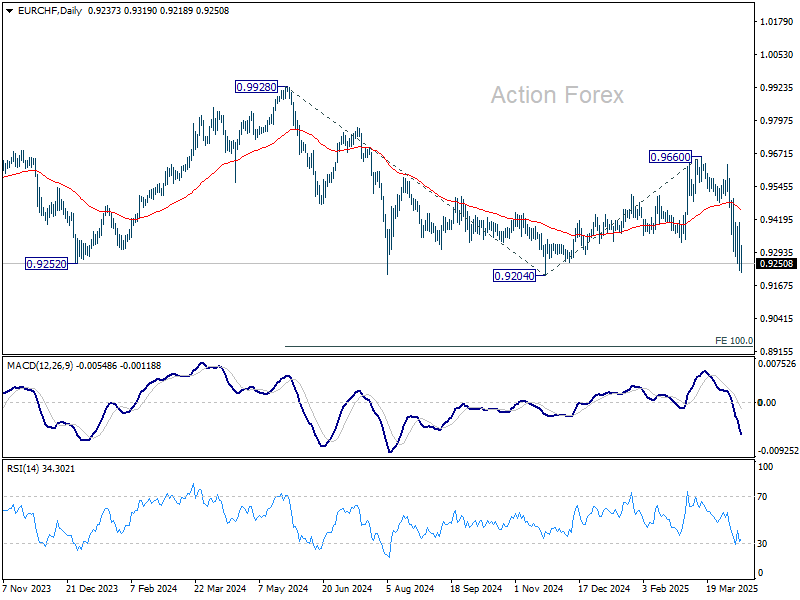

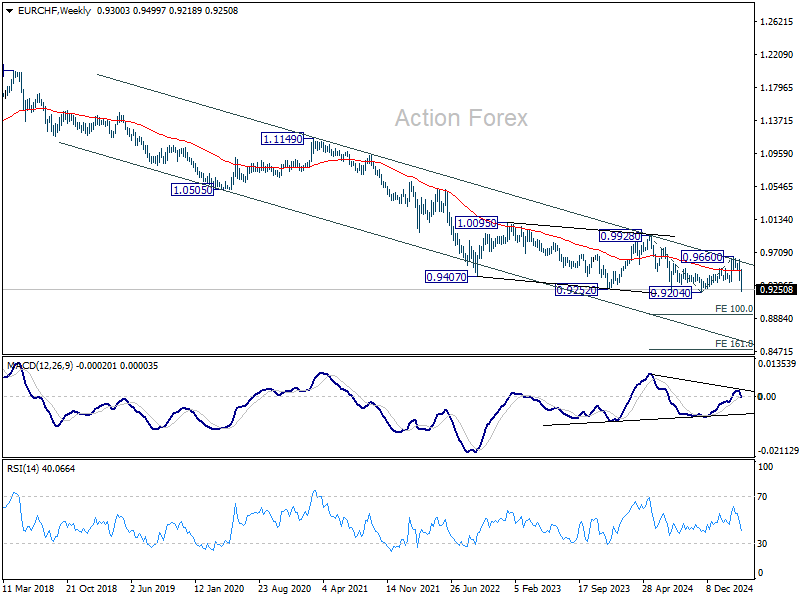

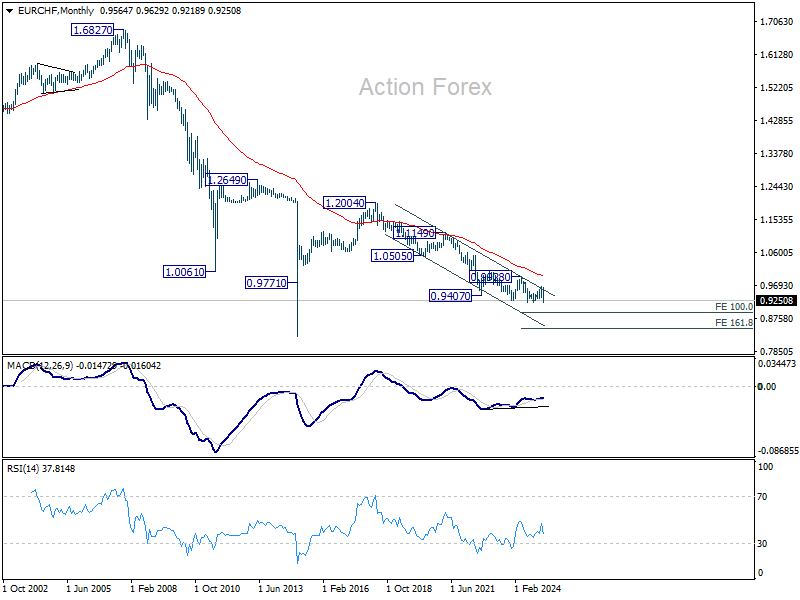

EUR/CHF Weekly Outlook

EUR/CHF's extended decline last week and break of 0.9331 support indicates that corrective rebound from 0.9204 has already completed with three waves up to 0.9660. Initial bias stays on the downside for retesting 0.9204. Firm break there will resume larger down trend. On the upside, break of 0.9408 resistance is needed to confirm short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, rejection by long-term falling channel resistance (now at 0.9600) retains medium term bearishness. That is, down trend from 1.2004 (2018 high) is still in progress. Firm break of 0.9204 (2024 low) will confirm resumption. Next target is 100% projection of 0.9928 to 0.9204 from 0.9660 at 0.8936.

In the long term picture, overall long term down trend is still in force in EUR/CHF. Outlook will continue to stay bearish as long as 55 EMA (now at 0.9936) holds.

Summary 4/14 – 4/18

Monday, Apr 14, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 22:30 | NZD | Business NZ PSI Mar | 49.1 | |

| 03:00 | CNY | Trade Balance (USD) Mar | 74.3B | 170.5B |

| 04:30 | JPY | Industrial Production M/M Feb F | 2.50% | 2.50% |

| 06:30 | CHF | Producer and Import Prices M/M Mar | 0.20% | 0.30% |

| 06:30 | CHF | Producer and Import Prices Y/Y Mar | -0.10% | |

| 12:30 | CAD | Wholesale Sales M/M Feb | 0.40% | 1.20% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 22:30 | NZD | Business NZ PSI Mar | |

| Forecast: | Previous: 49.1 | ||

| 03:00 | CNY | Trade Balance (USD) Mar | |

| Forecast: 74.3B | Previous: 170.5B | ||

| 04:30 | JPY | Industrial Production M/M Feb F | |

| Forecast: 2.50% | Previous: 2.50% | ||

| 06:30 | CHF | Producer and Import Prices M/M Mar | |

| Forecast: 0.20% | Previous: 0.30% | ||

| 06:30 | CHF | Producer and Import Prices Y/Y Mar | |

| Forecast: | Previous: -0.10% | ||

| 12:30 | CAD | Wholesale Sales M/M Feb | |

| Forecast: 0.40% | Previous: 1.20% | ||

Tuesday, Apr 15, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | RBA Meeting Minutes | ||

| 06:00 | GBP | Claimant Count Change Mar | 30.3K | 44.2K |

| 06:00 | GBP | ILO Unemployment Rate (3M) Feb | 4.40% | 4.40% |

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y Feb | 5.70% | 5.80% |

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y Feb | 5.90% | |

| 09:00 | EUR | Eurozone Industrial Production M/M Feb | 0.10% | 0.80% |

| 09:00 | EUR | Germany ZEW Economic Sentiment Apr | 10.6 | 51.6 |

| 09:00 | EUR | Germany ZEW Current Situation Apr | -87.6 | |

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Apr | 14.2 | 39.8 |

| 12:15 | CAD | Housing Starts Y/Y Mar | 238K | 229K |

| 12:30 | CAD | Manufacturing Sales M/M Feb | -0.20% | 1.70% |

| 12:30 | CAD | CPI M/M Mar | 0.70% | 1.10% |

| 12:30 | CAD | CPI Y/Y Mar | 2.60% | |

| 12:30 | CAD | CPI Median Y/Y Mar | 2.90% | 2.90% |

| 12:30 | CAD | CPI Trimmed Y/Y Mar | 2.90% | 2.90% |

| 12:30 | CAD | CPI Common Y/Y Mar | 2.40% | 2.50% |

| 12:30 | USD | Empire State Manufacturing Index Apr | -14.8 | -20 |

| 12:30 | USD | Import Price Index M/M Mar | 0.10% | 0.40% |

| 23:50 | JPY | Machinery Orders M/M Feb | 1.10% | -3.50% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | RBA Meeting Minutes | |

| Forecast: | Previous: | ||

| 06:00 | GBP | Claimant Count Change Mar | |

| Forecast: 30.3K | Previous: 44.2K | ||

| 06:00 | GBP | ILO Unemployment Rate (3M) Feb | |

| Forecast: 4.40% | Previous: 4.40% | ||

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y Feb | |

| Forecast: 5.70% | Previous: 5.80% | ||

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y Feb | |

| Forecast: | Previous: 5.90% | ||

| 09:00 | EUR | Eurozone Industrial Production M/M Feb | |

| Forecast: 0.10% | Previous: 0.80% | ||

| 09:00 | EUR | Germany ZEW Economic Sentiment Apr | |

| Forecast: 10.6 | Previous: 51.6 | ||

| 09:00 | EUR | Germany ZEW Current Situation Apr | |

| Forecast: | Previous: -87.6 | ||

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Apr | |

| Forecast: 14.2 | Previous: 39.8 | ||

| 12:15 | CAD | Housing Starts Y/Y Mar | |

| Forecast: 238K | Previous: 229K | ||

| 12:30 | CAD | Manufacturing Sales M/M Feb | |

| Forecast: -0.20% | Previous: 1.70% | ||

| 12:30 | CAD | CPI M/M Mar | |

| Forecast: 0.70% | Previous: 1.10% | ||

| 12:30 | CAD | CPI Y/Y Mar | |

| Forecast: | Previous: 2.60% | ||

| 12:30 | CAD | CPI Median Y/Y Mar | |

| Forecast: 2.90% | Previous: 2.90% | ||

| 12:30 | CAD | CPI Trimmed Y/Y Mar | |

| Forecast: 2.90% | Previous: 2.90% | ||

| 12:30 | CAD | CPI Common Y/Y Mar | |

| Forecast: 2.40% | Previous: 2.50% | ||

| 12:30 | USD | Empire State Manufacturing Index Apr | |

| Forecast: -14.8 | Previous: -20 | ||

| 12:30 | USD | Import Price Index M/M Mar | |

| Forecast: 0.10% | Previous: 0.40% | ||

| 23:50 | JPY | Machinery Orders M/M Feb | |

| Forecast: 1.10% | Previous: -3.50% | ||

Wednesday, Apr 16, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:00 | AUD | Westpac Leading Index M/M Mar | 0.06% | |

| 02:00 | CNY | GDP Y/Y Q1 | 5.10% | 5.40% |

| 02:00 | CNY | Industrial Production Y/Y Mar | 5.60% | 5.90% |

| 02:00 | CNY | Retail Sales Y/Y Mar | 4.10% | 4.00% |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Mar | 4.10% | 4.10% |

| 06:00 | GBP | CPI M/M Mar | 0.40% | |

| 06:00 | GBP | CPI Y/Y Mar | 2.70% | 2.80% |

| 06:00 | GBP | Core CPI Y/Y Mar | 3.40% | 3.50% |

| 06:00 | GBP | RPI M/M Mar | 0.60% | |

| 06:00 | GBP | RPI Y/Y Mar | 3.20% | 3.40% |

| 06:00 | GBP | PPI Input M/M Mar | 0.80% | |

| 06:00 | GBP | PPI Input Y/Y Mar | -0.10% | |

| 06:00 | GBP | PPI Output M/M Mar | 0.50% | |

| 06:00 | GBP | PPI Output Y/Y Mar | 0.30% | |

| 06:00 | GBP | PPI Core Output M/M Mar | 0.30% | |

| 06:00 | GBP | PPI Core Output Y/Y Mar | 1.50% | |

| 08:00 | EUR | Eurozone Current Account (EUR) Feb | 37.3B | 35.4B |

| 09:00 | EUR | Eurozone CPI Y/Y Mar F | 2.20% | 2.20% |

| 09:00 | EUR | Eurozone CPI Core Y/Y Mar F | 2.40% | 2.40% |

| 12:30 | USD | Retail Sales M/M Mar | 1.30% | 0.20% |

| 12:30 | USD | Retail Sales ex Autos M/M Mar | 0.40% | 0.30% |

| 13:15 | USD | Industrial Production M/M Mar | -0.30% | 0.70% |

| 13:15 | USD | Capacity Utilization Mar | 77.90% | 78.20% |

| 13:45 | CAD | BoC Interest Rate Decision | 2.75% | 2.75% |

| 14:30 | USD | Crude Oil Inventories | 2.6M | |

| 22:45 | NZD | CPI Q/Q Q1 | 0.70% | 0.50% |

| 22:45 | NZD | CPI Y/Y Q1 | 2.20% | |

| 23:50 | JPY | Trade Balance (JPY) Mar | -0.25T | 0.18T |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:00 | AUD | Westpac Leading Index M/M Mar | |

| Forecast: | Previous: 0.06% | ||

| 02:00 | CNY | GDP Y/Y Q1 | |

| Forecast: 5.10% | Previous: 5.40% | ||

| 02:00 | CNY | Industrial Production Y/Y Mar | |

| Forecast: 5.60% | Previous: 5.90% | ||

| 02:00 | CNY | Retail Sales Y/Y Mar | |

| Forecast: 4.10% | Previous: 4.00% | ||

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Mar | |

| Forecast: 4.10% | Previous: 4.10% | ||

| 06:00 | GBP | CPI M/M Mar | |

| Forecast: | Previous: 0.40% | ||

| 06:00 | GBP | CPI Y/Y Mar | |

| Forecast: 2.70% | Previous: 2.80% | ||

| 06:00 | GBP | Core CPI Y/Y Mar | |

| Forecast: 3.40% | Previous: 3.50% | ||

| 06:00 | GBP | RPI M/M Mar | |

| Forecast: | Previous: 0.60% | ||

| 06:00 | GBP | RPI Y/Y Mar | |

| Forecast: 3.20% | Previous: 3.40% | ||

| 06:00 | GBP | PPI Input M/M Mar | |

| Forecast: | Previous: 0.80% | ||

| 06:00 | GBP | PPI Input Y/Y Mar | |

| Forecast: | Previous: -0.10% | ||

| 06:00 | GBP | PPI Output M/M Mar | |

| Forecast: | Previous: 0.50% | ||

| 06:00 | GBP | PPI Output Y/Y Mar | |

| Forecast: | Previous: 0.30% | ||

| 06:00 | GBP | PPI Core Output M/M Mar | |

| Forecast: | Previous: 0.30% | ||

| 06:00 | GBP | PPI Core Output Y/Y Mar | |

| Forecast: | Previous: 1.50% | ||

| 08:00 | EUR | Eurozone Current Account (EUR) Feb | |

| Forecast: 37.3B | Previous: 35.4B | ||

| 09:00 | EUR | Eurozone CPI Y/Y Mar F | |

| Forecast: 2.20% | Previous: 2.20% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y Mar F | |

| Forecast: 2.40% | Previous: 2.40% | ||

| 12:30 | USD | Retail Sales M/M Mar | |

| Forecast: 1.30% | Previous: 0.20% | ||

| 12:30 | USD | Retail Sales ex Autos M/M Mar | |

| Forecast: 0.40% | Previous: 0.30% | ||

| 13:15 | USD | Industrial Production M/M Mar | |

| Forecast: -0.30% | Previous: 0.70% | ||

| 13:15 | USD | Capacity Utilization Mar | |

| Forecast: 77.90% | Previous: 78.20% | ||

| 13:45 | CAD | BoC Interest Rate Decision | |

| Forecast: 2.75% | Previous: 2.75% | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: 2.6M | ||

| 22:45 | NZD | CPI Q/Q Q1 | |

| Forecast: 0.70% | Previous: 0.50% | ||

| 22:45 | NZD | CPI Y/Y Q1 | |

| Forecast: | Previous: 2.20% | ||

| 23:50 | JPY | Trade Balance (JPY) Mar | |

| Forecast: -0.25T | Previous: 0.18T | ||

Thursday, Apr 17, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | NAB Business Confidence Q1 | -4 | |

| 01:30 | AUD | Employment Change Mar | 41.2K | -52.8K |

| 01:30 | AUD | Unemployment Rate s.a. Mar | 4.20% | 4.10% |

| 06:00 | CHF | Trade Balance (CHF) Mar | 5.22B | 4.80B |

| 06:00 | EUR | Germany PPI M/M Mar | -0.10% | -0.20% |

| 06:00 | EUR | Germany PPI Y/Y Mar | 0.70% | |

| 12:15 | EUR | ECB Main Refinancing Rate | 2.40% | 2.65% |

| 12:15 | EUR | ECB Deposit Rate | 2.25% | 2.50% |

| 12:30 | USD | Building Permits Mar | 1.45M | 1.46M |

| 12:30 | USD | Housing Starts Mar | 1.42M | 1.50M |

| 12:30 | USD | Initial Jobless Claims (Apr 11) | 224K | 223K |

| 12:30 | USD | Philadelphia Fed Manufacturing Apr | 6.8 | 12.5 |

| 12:45 | EUR | ECB Press Conference | ||

| 14:30 | USD | Natural Gas Storage | 57B | |

| 23:30 | JPY | CPI Core-Core Y/Y Mar | 2.60% | |

| 23:30 | JPY | CPI Core Y/Y Mar | 3.20% | 3% |

| 23:30 | JPY | CPI Y/Y Mar | 3.70% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | NAB Business Confidence Q1 | |

| Forecast: | Previous: -4 | ||

| 01:30 | AUD | Employment Change Mar | |

| Forecast: 41.2K | Previous: -52.8K | ||

| 01:30 | AUD | Unemployment Rate s.a. Mar | |

| Forecast: 4.20% | Previous: 4.10% | ||

| 06:00 | CHF | Trade Balance (CHF) Mar | |

| Forecast: 5.22B | Previous: 4.80B | ||

| 06:00 | EUR | Germany PPI M/M Mar | |

| Forecast: -0.10% | Previous: -0.20% | ||

| 06:00 | EUR | Germany PPI Y/Y Mar | |

| Forecast: | Previous: 0.70% | ||

| 12:15 | EUR | ECB Main Refinancing Rate | |

| Forecast: 2.40% | Previous: 2.65% | ||

| 12:15 | EUR | ECB Deposit Rate | |

| Forecast: 2.25% | Previous: 2.50% | ||

| 12:30 | USD | Building Permits Mar | |

| Forecast: 1.45M | Previous: 1.46M | ||

| 12:30 | USD | Housing Starts Mar | |

| Forecast: 1.42M | Previous: 1.50M | ||

| 12:30 | USD | Initial Jobless Claims (Apr 11) | |

| Forecast: 224K | Previous: 223K | ||

| 12:30 | USD | Philadelphia Fed Manufacturing Apr | |

| Forecast: 6.8 | Previous: 12.5 | ||

| 12:45 | EUR | ECB Press Conference | |

| Forecast: | Previous: | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 57B | ||

| 23:30 | JPY | CPI Core-Core Y/Y Mar | |

| Forecast: | Previous: 2.60% | ||

| 23:30 | JPY | CPI Core Y/Y Mar | |

| Forecast: 3.20% | Previous: 3% | ||

| 23:30 | JPY | CPI Y/Y Mar | |

| Forecast: | Previous: 3.70% | ||

Friday, Apr 18, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| Good Friday |

| GMT | Ccy | Events | |

|---|---|---|---|

| Good Friday | |||

| Forecast: | Previous: | ||

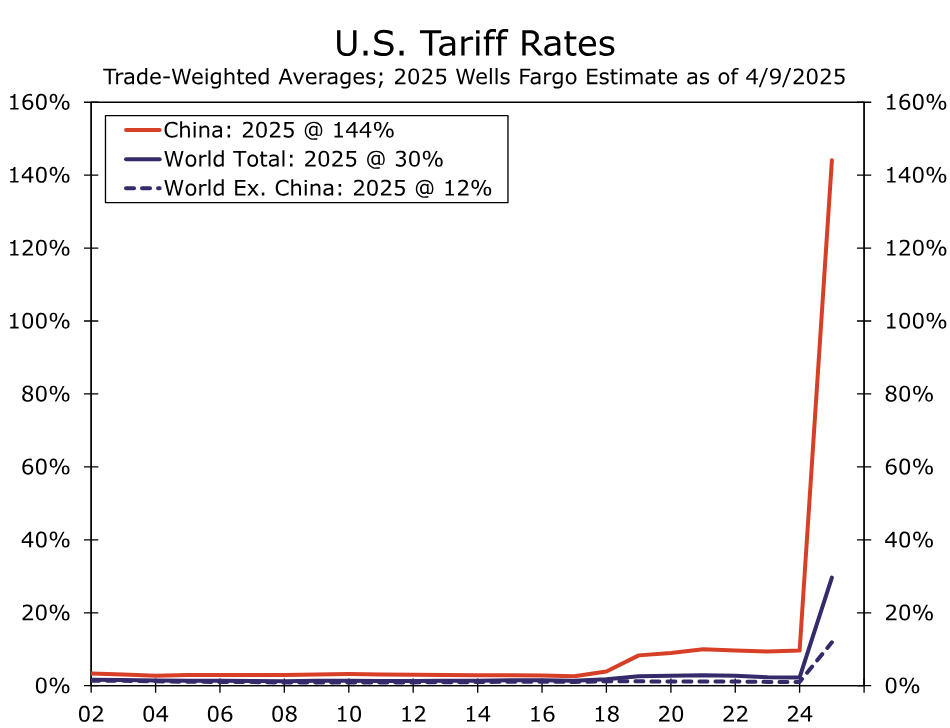

U.S.-China Trade Tensions Enter a New Phase

Summary

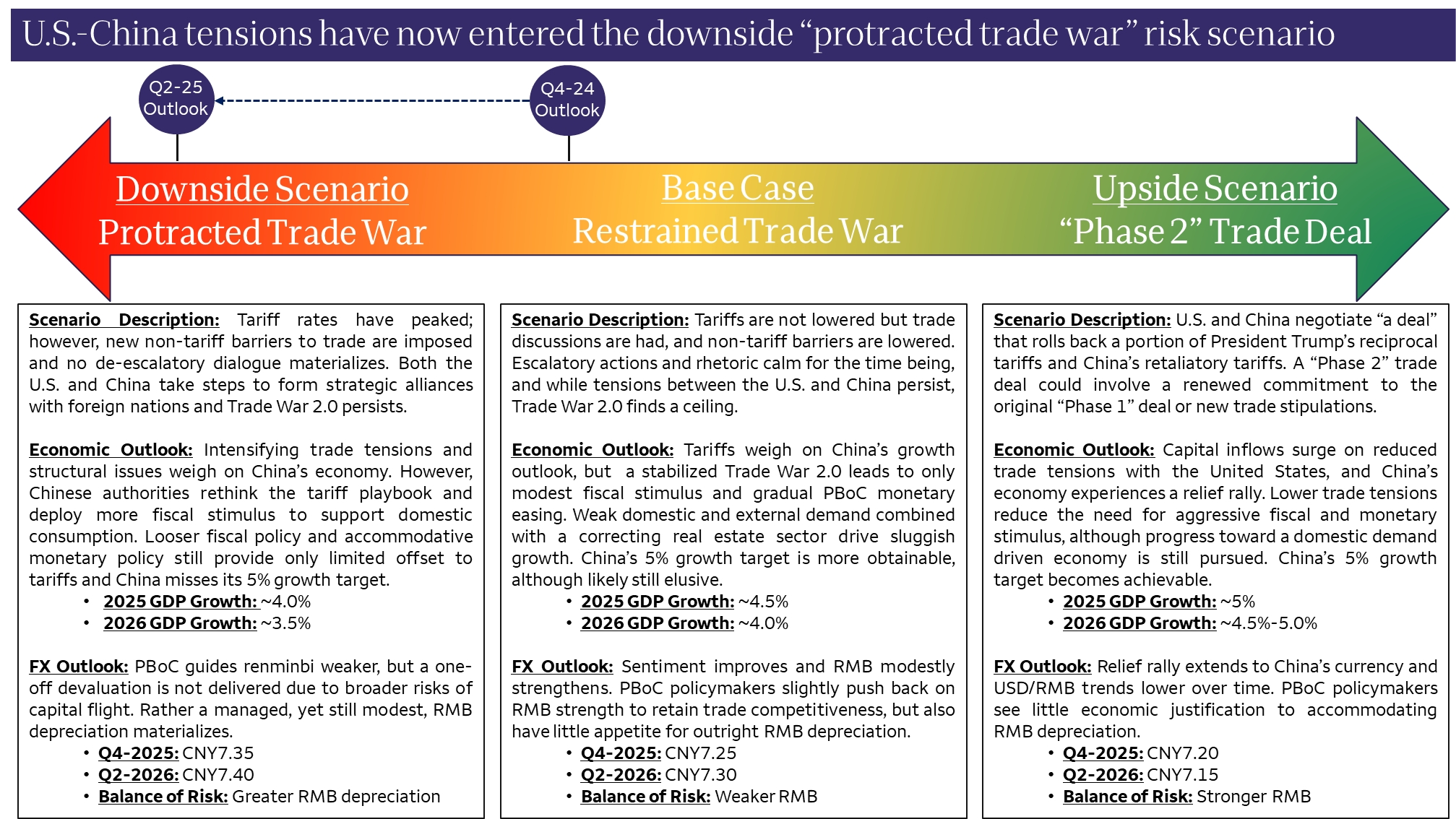

Tensions between the United States and China have ratcheted higher since “Liberation Day.” We now believe the outlook for China's economy and currency has shifted away from our original base case and into our “protracted trade war” downside scenario. The growth outlook for China has materially worsened and tensions are likely to escalate through non-tariff barriers to trade; however, we maintain our view that Chinese authorities will not engineer an FX devaluation at any point during Trade War 2.0.

Weekly Economic & Financial Commentary: What Is Going on in the Treasury Market?

Summary

United States: Thank you for your attention to this matter!

- Economic data releases took a back seat to trade policy changes again this week, with President Trump declaring a 90-day pause on many of the “reciprocal” tariffs announced on April 2. The pause still leaves the United States in a materially higher tariff environment than any time in the past century. Inflation data for March were softer than expected and sentiment data continued to deteriorate. Congressional Republicans moved forward with a reconciliation bill that promises fiscal stimulus in 2026.

- Next week: Retail Sales (Wed.), Industrial Production (Wed.), Housing Starts (Thu.)

International: Foreign Central Banks in Dovish Mood as Trade Tensions Persist

- Foreign central banks remained in an overall dovish mood this week amid ongoing trade uncertainties, as the Reserve Bank of New Zealand, Reserve Bank of India and Philippine central bank all lowered interest rates, while suggesting further easing to come. Mexico's benign CPI should also see another rate cut in May, while firm inflation and activity data should see Brazil's Cental Bank hike rates at its next meeting.

- Next week: China GDP (Wed.), Bank of Canada Policy Rate (Wed.), ECB Policy Rate (Thu.)

Interest Rate Watch: What Is Going on in the Treasury Market?

- After an initial plunge following “Liberation Day,” longer-term Treasury yields have risen this week and are now higher than they were on April 1. What is going on in the U.S. Treasury market?

Topic of the Week: Tariff U-Turn Puts China in the Hot Seat

- On April 9, President Trump announced a 90-day pause to his “reciprocal” tariff plan just hours after it went into effect, replacing the country-specific rates with a 10% baseline tariff on most countries. China is the main exception, with Trump adding additional tariffs to bring the country's effective tariff rate to 145%.