Sample Category Title

Markets Weekly Outlook – Tariff Rollercoaster Continues, ECB Rate Decision and Inflation Data in Focus

- US dollar weakens amid market concerns, hitting 2022 lows.

- Tariff changes and global economic fears drive market volatility.

- Gold prices surge, while oil faces losses due to supply and demand issues.

- Upcoming week focuses on US tariffs, inflation data, and ECB meeting.

Week in review: US Dollar on the ropes following topsy-turvy week

It's been a wild ride to say the least for financial markets this week. Wild swings, multi year highs and lows being tested, tariffs being pulled back and of course the escalating tensions between the US and China.

The developments this week necessitate us starting with FX markets as the US dollar endured heavy losses hitting 2022 lows in the process.

The FX market tells an interesting story. Among G10 currencies, only the less-traded Norwegian krone hasn’t moved against the dollar since last Friday. Other currencies have gained, with the pound up 0.8%, the euro, Australian dollar, and New Zealand dollar rising 2-3%, and the Swiss franc leading with a 4.5% increase.

Markets are clearly telling us that there is a crisis of confidence in the US dollar at the moment. Whether I believe there should be or not is an entirely different and irrelevant discussion given what we have already seen from markets.

On Thursday we saw investors move away from US assets. Both stocks and Treasury bonds dropped, even though core inflation came in much lower than expected (0.1% instead of the predicted 0.3% for the month).

Markets are definitely telling us that data is not the main driving force behind market moves. This honor is taken by concern about the combined threat of inflation and growth deceleration.

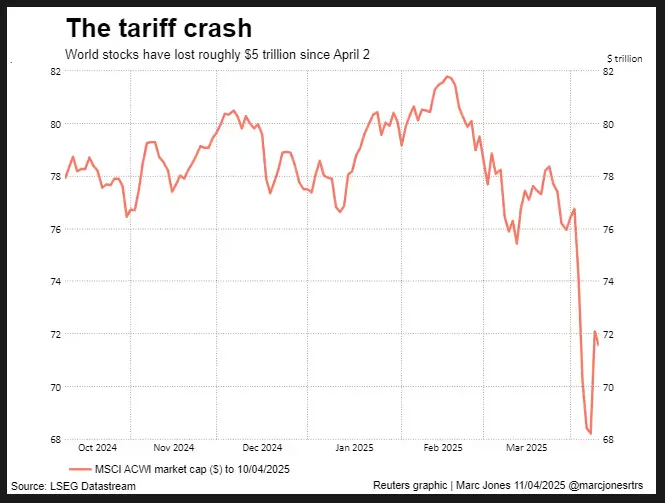

A perfect example of the challenges facing global markets is reflected in the losses for stock markets around the world. More than $5 trillion in market value has vanished from the MSCI all-country index of world stocks during the roller-coaster ride since April 2.

Source: LSEG

These developments have helped Gold prices once more with the precious metal making multiple fresh highs this week. Gold peaked on Friday at around $3245/oz at the time of writing. The precious metal is on course to finish the week around 6.5% up

Oil prices rose on Friday but both Brent and WTI are set for a second consecutive week of losses.Tariffs being the instigator here as well as recessionary fears are impacting oil demand forecasts just as OPEC + increased output. Earlier today, President Trump's administration said the President wants the US to pump more and more oil, further exacerbating demand and supply dynamics.

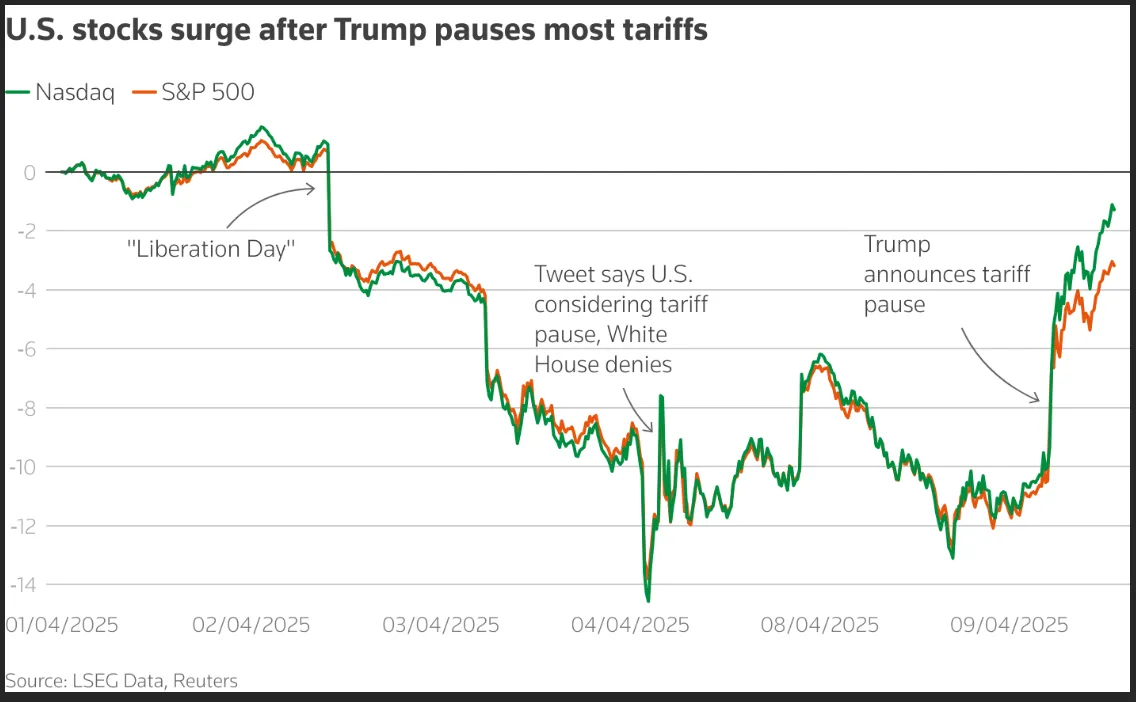

US Equity Indexes finished the week on a positive note with the Dow Jones increasing by 648.65 points (1.64%) to 40,242.31. The S&P 500 went up 93.70 points (1.78%) to 5,361.75, and the Nasdaq climbed 312.92 points (1.91%) to 16,700.23. The week was a positive one for US stocks following President Trump's pause on his ‘liberation day tariff agenda’. The move has seen US indexes recover most of the losses which occurred since the April 2 announcement.

Source: LSEG

The biggest story this week aside from the US dollar comes from the US Treasury market. U.S. 10-year Treasury yields saw their biggest weekly jump in over 20 years on Friday. Rumors of selling, or lack of buying, by foreign investors are adding to concerns over the market with rumors that hedge funds and asset managers were getting margin calls.

Another reason cited for the performance comes through the unwinding of basis trades, a strategy where investors earn from the gap between cash Treasury prices and futures. Many believe this is a large factor behind this week's volatility.

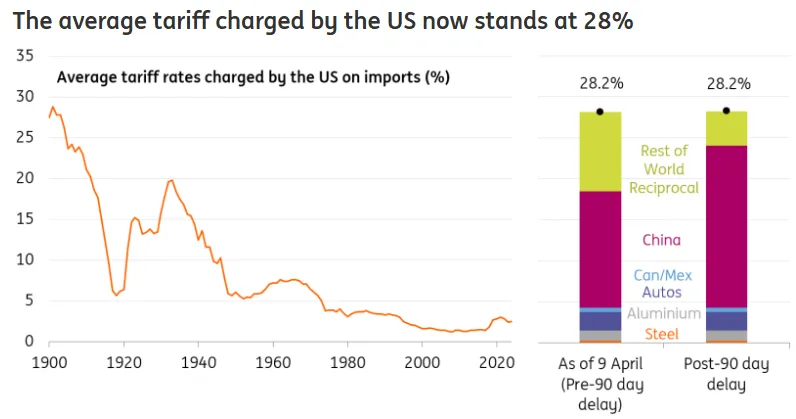

An interesting take from ING THINK caught my attention this week. To summarize, the piece opined that U.S. tariff policies haven’t changed much overall. Here’s why:

Before Trump took office, the average U.S. tariff on imports was 2.5%. By Wednesday morning, with actions like 25% tariffs on metals and autos, and up to 50% on China, that average rose to 28%—the highest since the early 20th century.

Midweek, some countries like the EU and parts of Southeast Asia saw their tariffs drop to 10%. However, China's tariffs, already high at 104%, jumped to 145%.

These adjustments balanced out, leaving the average tariff rate unchanged at 28%.

Source: US Census data, White House, ING calculations

**Only non-USMCA compliant goods from Canada and Mexico are subject to a 25% tariff. Assumes latest China tariff of 145%, as per latest Bloomberg reports. Colored bars show the contribution to the latest average tariff rate from the tariffs charged on different countries and products.

I found this to be an interesting take and something i had partly anticipated having paid attention to President Trumps previous term. However it does not hold much weight in the current climate as markets are still moving and that is the reason why we are here after all.

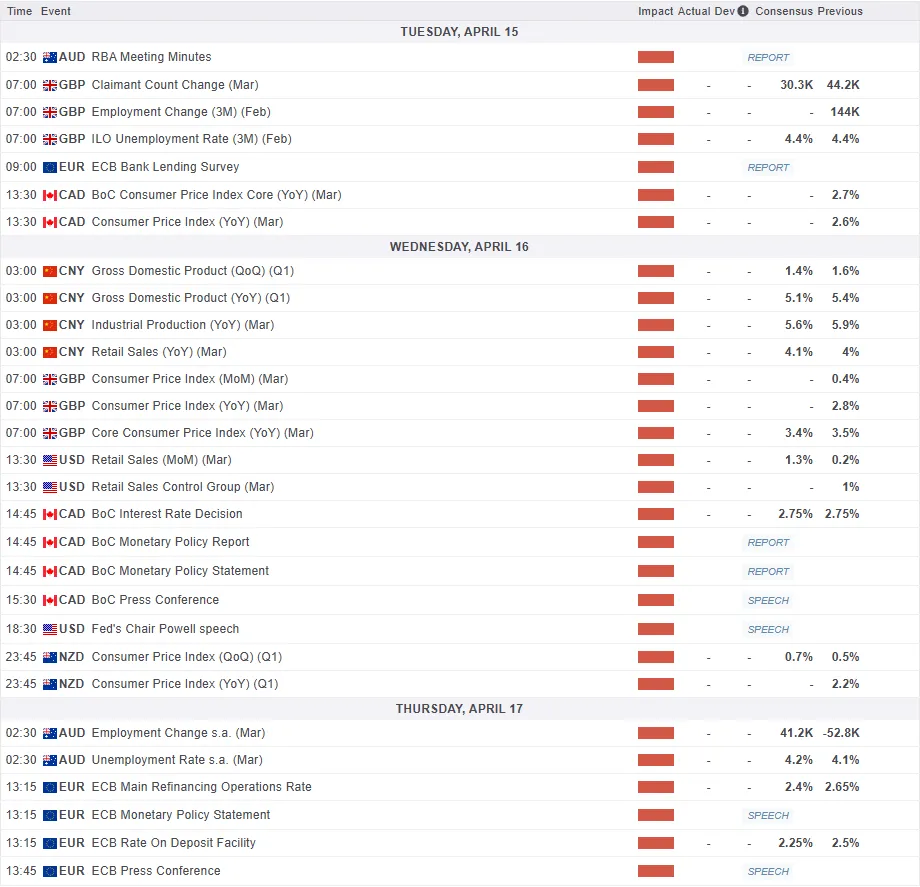

The week ahead: Shortened trading week brings a host of data releases

The upcoming week will focus on U.S. President Donald Trump's plans for new tariffs. Alongside this, markets will also watch U.S. jobs data, an Australian central bank meeting, and a key eurozone inflation report.

Asia Pacific Markets

The main focus this week in the Asia Pacific region will be Japanese inflation and a host of data releases from China.

In Japan, inflation is expected to rise, but the Bank of Japan (BoJ) is likely to keep its rate cuts on hold. Goods being shipped early to the US are expected to boost machinery orders and exports.

However, this positive trend might not last beyond the first quarter due to tariff uncertainties. Consumer prices are predicted to go up in March, mainly due to higher service costs. Earlier fresh food price hikes are also expected to show up in eating-out and processed food costs. The BoJ will keep a close eye on how US tariff policies affect the economy while maintaining current rates for now.

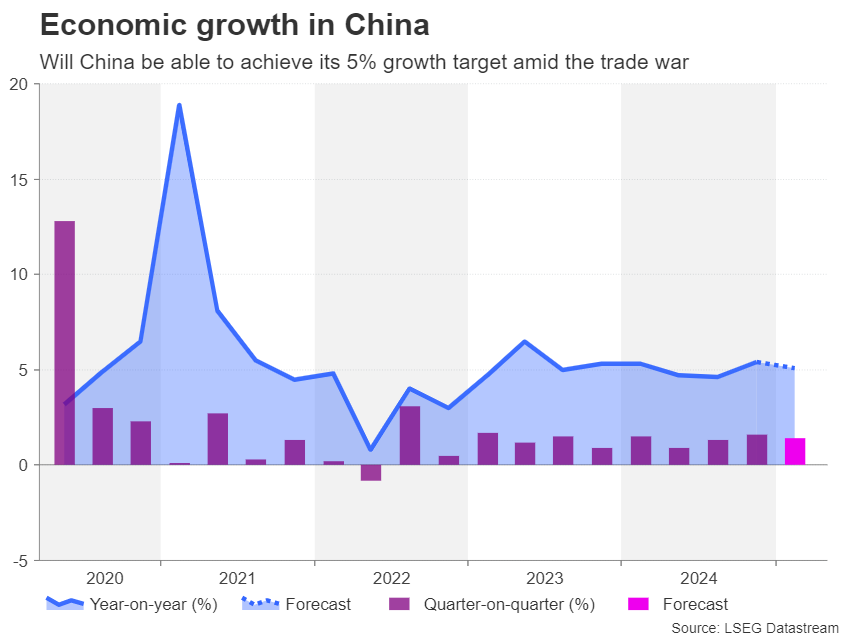

It's a busy data week in China as the country grapples with the escalating trade war with the US. None of the tariffs so far are expected to show any impact on the data yet but should do so moving forward.

China will release key data for March, including first-quarter GDP on Thursday. A 5.3% year-on-year growth is expected, though this is before tariffs start impacting from the second quarter. For now, domestic activity seems steady, with retail sales and industrial production likely to grow by 4.5% and 6.0%, respectively. Fixed-asset investment is expected to stay mostly stable at 4.0%. Trade is slowing as tariffs take effect, but bigger impacts may come later.

Property prices will also be watched to see if market volatility has pushed them down further. Supporting domestic demand is the focus this year, though falling home prices make it hard to boost household confidence. While prices in major cities have stabilized, it’s unclear if this is the bottom.

Meanwhile, all attention is on how China will respond to the 145% tariffs imposed by Trump with a 125% tariff on US goods due to start on April 12.. The market expects possible rate cuts, lower reserve requirement ratios (RRR), and new fiscal policies to support domestic demand.

In the Pacific region we have some high impact data from both Australia and New Zealand. On Tuesday we have the RBA minutes followed by Wednesday's New Zealand CPI release. The week ends on Thursday with employment data out of Australia.

Europe + UK + US

In developed markets, the US is enjoying a bit of a data break next week but the tariff conversations will remain at the forefront. The Euro Zone and the UK have a bit more to offer on the data front next week with the ECB interest rate meeting taking center stage.

The US is expected to have a calmer week due to Easter, but challenges remain. Tariffs have been delayed by 90 days, yet price hikes are still looming. Households are dealing with three key issues: higher prices reducing spending power, job loss fears due to federal budget cuts, and stock market drops making people cautious about major purchases.

March retail sales are likely to show strong growth as consumers rushed to buy before tariffs take effect. Auto sales rose 10.6%, and credit card data points to high demand for electronics and appliances. This may keep GDP growth positive in the first quarter, but future weakness is a concern.

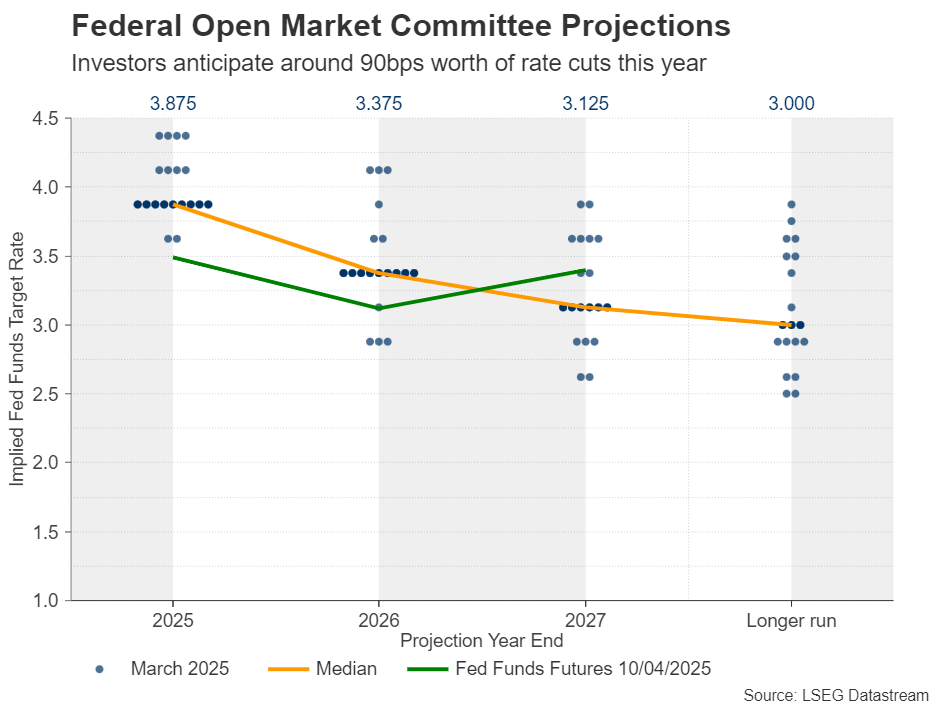

Industrial output will be under the spotlight as Trump pushes for reshoring. However, unclear trade policies and fears of retaliation are making businesses nervous. Meanwhile, the Fed is expected to cut rates by around 90 basis points this year, with three or four 25bp cuts looking likely.

The rise in employers' national insurance could slow the job market, but so far redundancy data hasn't increased. Watch for any drop in job vacancies or payroll numbers, though it seems unlikely.

Lower petrol prices may slightly reduce overall inflation in March, but services inflation is unlikely to fall much yet. More improvement could come in the second quarter if annual price adjustments are less steep. This is why the Bank of England may continue cutting rates each quarter through 2025 and into 2026.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Chart of the Week - US Dollar Index (DXY)

This week's focus remains on the US Dollar Index as it looks to recover from levels last sen in 2022.

The DXY has pushed below the psychological 100 barrier as well for the first time since July 2023. The last time the DXY breached this level the move proved short-lived with the DXY going on an extended rally to the upside thereafter.

Given the dynamics at play this time around, such a move sees unlikely. However, a push back above the 100.00 barrier cannot be ruled out.

Given the speed of the selloff this week, coupled with the RSI period-14 hovering in oversold territory and the downside wick in Friday, a bounce cannot be ruled out.

Immediate resistance rests at 100.00 before the 100.617 and 101.18 handles come into focus.

If the selloff continues next week, immediate support rests at 99.57 and 99.00. A break of the 90.00 mark could result in a swift move lower toward the 97.70 support handle.

US Dollar Index (DXY) Daily Chart - April 11, 2025

Source: TradingView.Com (click to enlarge)

Key Levels to Consider:

Support

- 99.57

- 99.00

- 97.70

Resistance

- 100.00

- 100.61

- 101.18

The Weekly Bottom Line: Tariff Rollercoaster Continues, Trade Fight with China Escalate

Canadian Highlights

- Canada managed to steer clear of new tariff announcements this week but will still be subject to the fentanyl/immigration tariffs put in place last month.

- The Bank of Canada outlook surveys revealed that an increasing share of businesses and consumers expect a recession in the coming year.

- The Bank of Canada will be weighing the near-term inflation and GDP growth expectations as they make their next interest rate policy announcement next week.

U.S. Highlights

- Market sentiment soured earlier this week as ‘reciprocal’ tariffs went into effect. Equities sold off initially, but so did Treasuries, with the 10-year Treasury yield up sharply on the week.

- A decision to ease U.S. tariff measures on most countries targeted last week, while increasing tariffs on China, sent markets on a rollercoaster.

- Inflation came in lower than anticipated in March, with core CPI easing to 2.8% year-on-year from 3.1% previously.

Canada – Navigating Tariffs

Another week, another flurry of tariff-related announcements. As it stands, global trading partners will now only be subject to a baseline 10% tariff, with a 90-day pause granted on the reciprocal-tariff component announced just last week. The exception is China, who will now face an eye-watering 145% tariff rate. Canada (and Mexico) managed to stay out of the crosshairs of Trump’s about-face but will still be subject to the “fentanyl/illegal immigration” tariffs imposed over the past month. Nonetheless, Canadian financial markets still felt the sting from rumbling trade conflicts, down by as much as 6% before recovering to a 1% loss on the week. Yields spiked higher by 26 and 38 bps in the 2 and 10-year space, respectively, while the Canadian dollar rallied almost 2 cents to 72 U.S. cents.

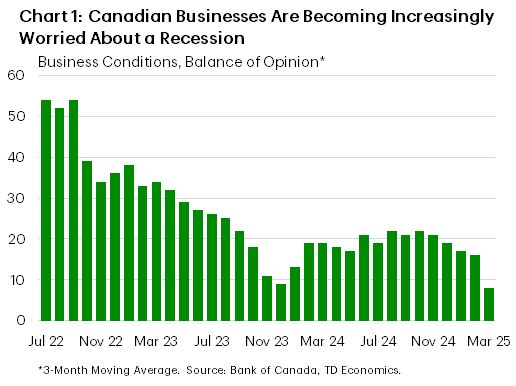

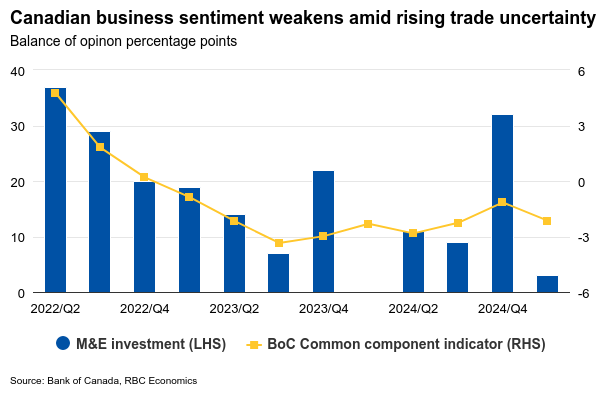

Economic data north of the border was light this week, with only the Bank of Canada’s (BoC) companion business and consumer outlook surveys released. On the business side, a drop in future sales expectations and the sizeable reduction in investment intentions point to a much weaker outlook than in our recent forecast for Q1 2025. What’s more, a third of respondents indicated belief that a recession will occur over the next year (Chart 1), a sentiment mirrored by two-thirds of consumers. Keep in mind, both businesses and consumers were polled in the middle-weeks of February, suggesting that overall sentiment has likely soured further since the release.

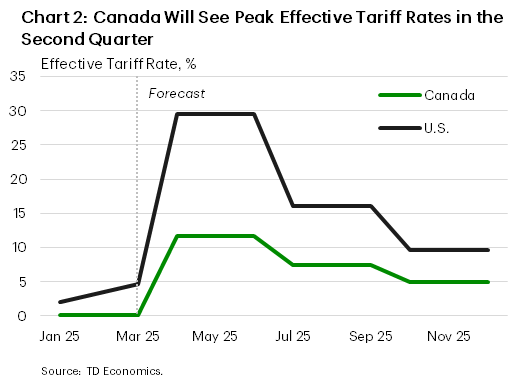

Next week’s inflation update for March could see price growth stay in warm territory after February’s inflation data printed above consensus expectations. Past this, we anticipate a couple quarters of elevated price pressures as tariffs pass through the economy before the inevitable demand hit puts inflation back on a downward trend. Our forecast assumes that the U.S. effective tariff rate on Canada remains elevated for the second quarter at around 10% before gradually lowering thereafter (Chart 2). This is on the basis that an increasing share of Canadian companies will initiate the process of declaring their products USMCA compliant, exempting them from tariffs. As a reminder, Canada has so far retaliated with $120 billion worth of tariffs on U.S. imports–$30 billion on March 4th, $30 billion on March 12th in response to Trump’s 25% steel and aluminum tariffs, and $60 billion targeted towards U.S. auto imports.

The BoC will make a widely anticipated policy announcement to cap off the holiday-shortened week. The door is certainly open for the Bank to trim the policy rate by another 25 bps as a precautionary measure, a view we are leaning toward. That said, taking a pause is still a potential option. Markets are tilted more toward this outcome, trimming bets for a rate cut to 32% from just over 40% before Trump’s most recent tariff announcement. This likely reflects the fact that the overall economic health of Canada is in otherwise decent standing as the economy entered the year with significant momentum. Balancing the opposing forces of inflation and growth will keep the BoC on their toes in the coming months.

U.S. – Tariff Rollercoaster Continues, Trade Fight with China Escalates

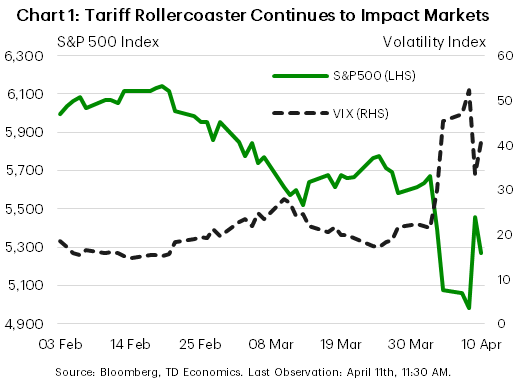

Another tumultuous week has followed for financial markets. On the heels of last week’s announcement that the U.S. would implement higher reciprocal tariffs on a number of countries, some appeared to have reached out for negotiation, while a few others announced their own countermeasures. What stood out was China’s commensurate retaliation to the 34% additional U.S. tariff on Chinese goods. But this was only the beginning, with the trade fight escalating throughout the week. As higher reciprocal tariffs came into effect, equity markets sold off. Normally when this happens, Treasuries (considered a safe-haven asset) tend to rally. But, in a very concerning move, Treasuries sold off too. Yields (which move opposite to bond prices) shot higher. The dollar also lost considerable ground against a basket of foreign currencies. Before long, the White House appeared to extend an olive branch. In a surprising move, Pres. Trump announced a 90 day pause to last week’s reciprocal tariffs, while also lowering the country-specific rate to a universal 10% for all targeted countries, except for China. Tariffs on the latter were jacked up further. Stock markets rejoiced initially, staging a sharp recovery on Wednesday. But when it came to yields and the dollar, the weak trends described above resumed later in the week (Chart 1).

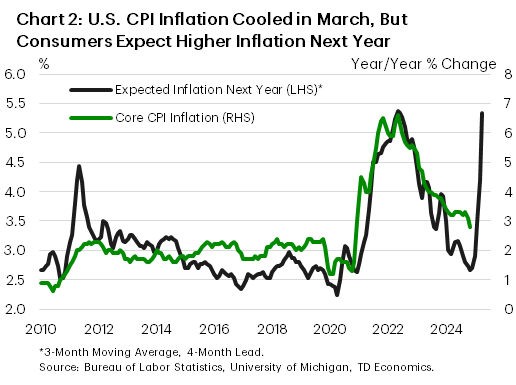

Pulling back the lens on the many twists and turns from this week’s events, one thing is clear – the U.S. is softening its tariff stance with most partners targeted last week, but is tightening the screws on China. The White House has clarified that the tariff increases on China so far add up to 145%, while this morning China announced it will increase retaliatory tariffs on U.S. goods to 125%. If tariffs were to hold at these high levels for a while, a large chunk of trade with China would effectively be cut off. While China’s economy would undoubtedly take a hit, as its $439 billion worth of goods sent to the U.S. last year dwindle to something much lower, there Chart 2 shows Core CPI inflation and consumer inflation expectation over the next year. The two measures are correlated. The chart shows that one-year inflation expectations have shot higher recently, indicating that consumers are positioning for higher inflation ahead. will be major consequences at home too. Reduced access to the Chinese market for U.S. exporters is a first. But perhaps a more concerning aspect is the prospect of product shortages, along with higher prices for inelastic products that can’t be sourced from elsewhere in short order. Domestic production cannot fill the void that will be left by China over the near-to-medium term. In this vein, the trade war will also remap supply chains, with the U.S. inclined to seek product substitutes from other countries, while Chinese exporters will seek to expand in other markets, such as in Europe.

Apart from leaving a mark on financial markets, trade uncertainty is also weighing on consumers and businesses, with the NFIB small business confidence measure continuing to trend lower in March. On a more positive note, producer prices, and inflation as measured by CPI, both came in softer than anticipated last month. Lower energy prices dragged down total CPI inflation (2.4% year-on-year (y/y)), but core inflation also eased, cooling to 2.8% y/y from 3.1% previously. Still, considering the tariffs and the fact that consumers are positioning for higher inflation, this trend looks set to reverse course soon (Chart 2). This leaves the Fed in a difficult position. Minutes from the mid-March FOMC meeting suggest that the central bank wasn’t ready to alter its course yet, with Fed officials leaning against preemptive rate cuts. While a lot has changed in the last three weeks, messaging from Fed officials appears consistent, with several speeches this week driving home the point that the bar for rate cuts remains high.

BoC Expected to Cut Interest Rates Again But It’s a Close Call

Wednesday’s interest rate decision for the Bank of Canada will be another close call for policymakers, but we expect they will ultimately opt to add another “insurance” 25 basis point cut in the face of escalating U.S. tariff risks.

Minutes from the last BoC meeting largely confirmed that the central bank would have foregone a cut to the overnight rate in March if not for heightened trade risks. We continue to think that fiscal policy is better positioned to provide the kind of timely, targeted, and temporary support needed for the economy as needed than changes in interest rates.

Our tracking of consumer spending has been more resilient than the plunge in consumer confidence measures in March alone would suggest. But, business investment and hiring intentions have weakened considerably with employment plans falling below pandemic-era lows in the BoC’s Q1 Business Outlook Survey . About 32% of firms surveyed now expected a recession in the next 12 months, up from 15% in the previous quarter. March employment data reinforced these concerns with the job count falling and unemployment rising. And, housing markets have shown clear signs of slowing—reducing the odds that near-term interest rate hikes will lead to another round of surging house prices.

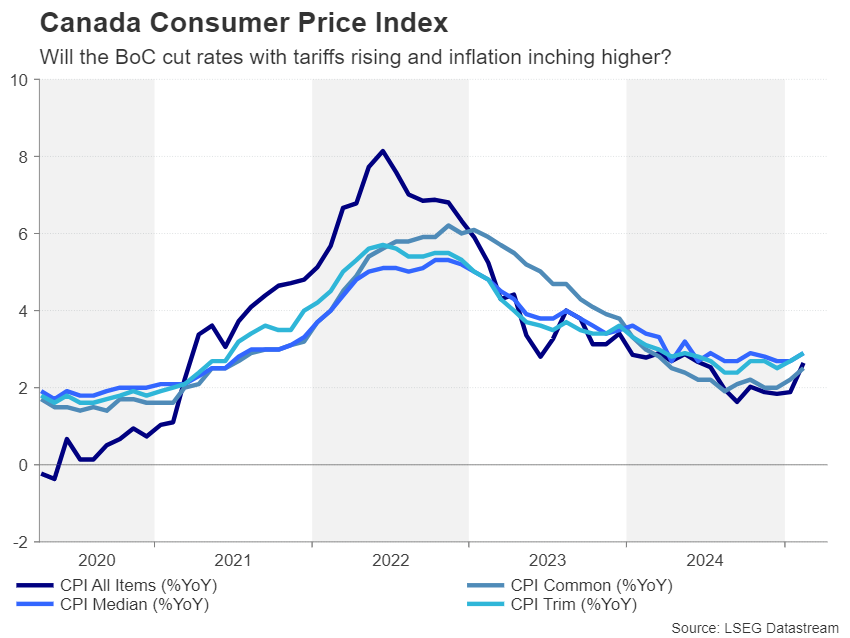

Complicating the BoC’s decision is inflation has broadly surprised to the upside in recent months. We expect March's headline inflation will hold at 2.6% year-over-year on Tuesday, matching February’s rate with lower gasoline prices in March offset by further unwinding of the GST/HST tax holiday that ended mid-February. Much of that increase outside of the drop in fuel costs is expected to show up in after-tax prices for restaurant meals.

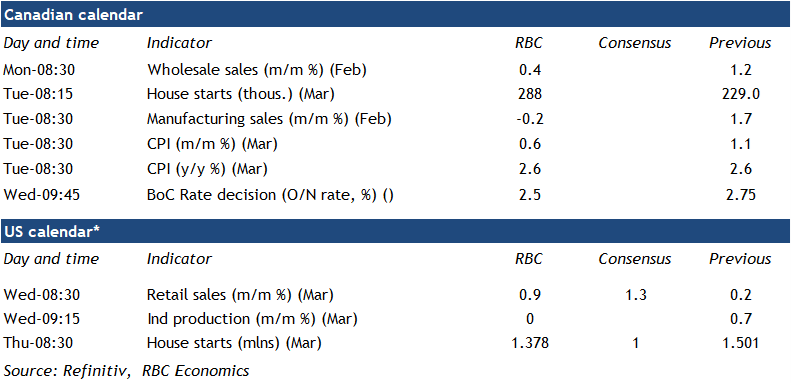

Week ahead data watch

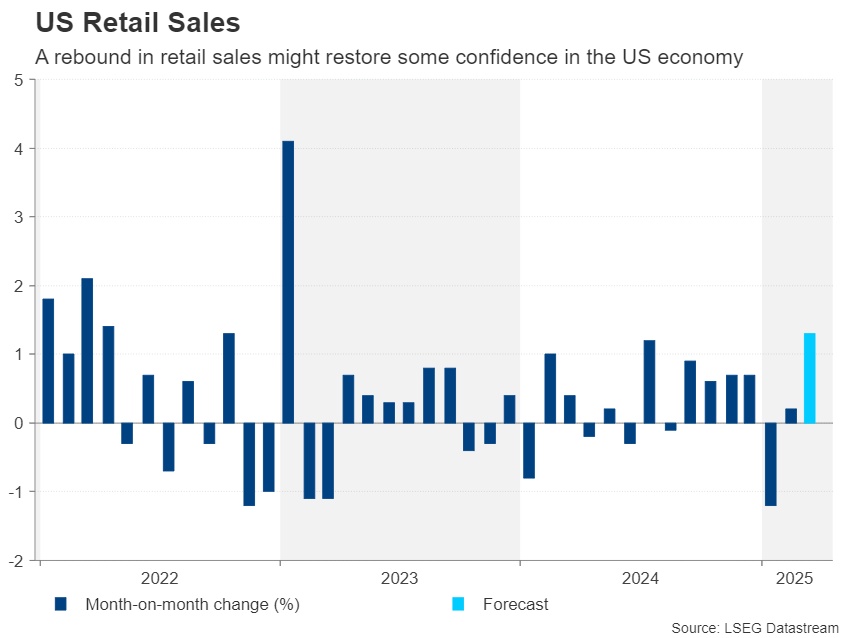

U.S. retail sales likely bounced back in March, fueled by a 10% jump in unit auto sales as buyers rushed to get ahead of tariffs imposed on motor vehicles starting in April. Sales at gasoline stations likely declined on lower prices at the pump.

Canadian housing starts are anticipated to come in at 288,000 in March, up from 229,000 in February. This partly reflects a rebound from a weather-induced drop in February, while building permits have been exceptionally strong this year.

We expect Canadian core wholesales sales to tick up 0.4% in February, in line with Statistics Canada’s preliminary estimate, and slower than 1.2% growth in the prior month. Most of that growth was supported by higher sales in the machinery, equipment and supplies’ subsector.

Canadian manufacturing sales likely dipped 0.2% in February, following a solid print (1.7%) in January. The largest sales declines came from the food, petroleum and coal subsectors.

Week Ahead – ECB Set to Cut, BoC Might Pause as Trump U-Turns on Tariffs

- ECB is expected to trim rates, but the BoC might pause this time.

- CPI data also in the spotlight; due in UK, Canada, New Zealand and Japan.

- Retail sales the main release in the United States.

- China GDP eyed as Beijing not spared by Trump.

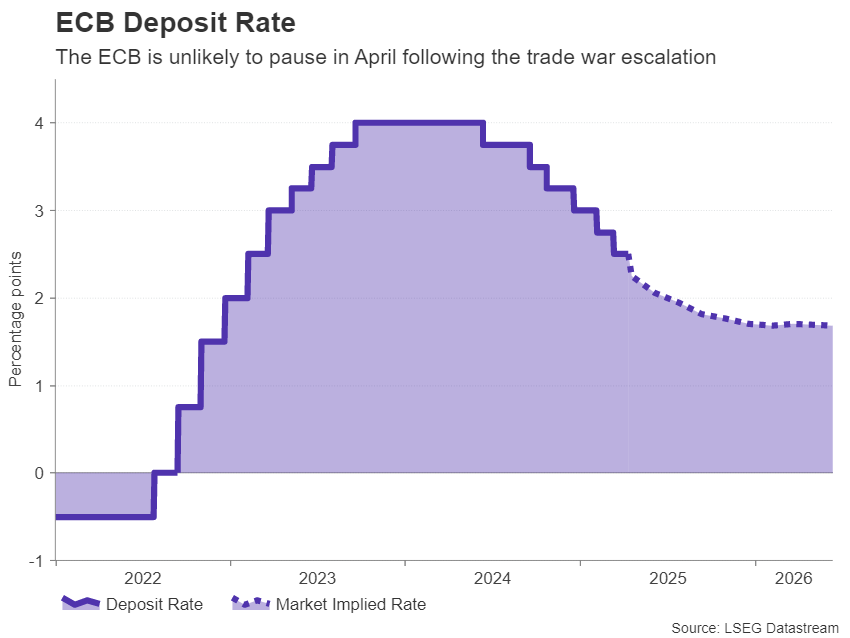

ECB puts rate pause on the back burner

The European Central Bank meets on Thursday to set monetary policy amidst a turbulent time for financial markets as US President Trump’s trade policies continue to wreak havoc. Having already lowered its deposit rate by 150 basis points to 2.50%, the ECB was contemplating a pause in April to assess the impact of the previous easing. But the economic outlook has deteriorated markedly since the beginning of April when Trump launched his reciprocal tariffs, targeting virtually all of America’s trading partners.

Whilst it is too soon to gauge the immediate hit on businesses, the scale of the market fallout suggests investors are in panic mode. For the ECB, the outlook is complicated by German’s massive fiscal stimulus, as it’s uncertain whether this will be enough to cushion the entire Eurozone from Trump’s trade salvos.

Nevertheless, with inflationary pressures across the euro are subsiding once again, playing it safe and cutting rates further is probably the better option for the ECB. Traders are convinced policymakers will lower rates by 25 bps at the April meeting and have priced in further two cuts before the year end.

The dovish expectations haven’t been a huge drag on the euro, however, as the Eurozone’s large trade surplus with the rest of the world has been providing the currency with some safe-haven attributes during this tumultuous period. And with the US dollar coming under pressure again, the euro has jumped above the $1.13 level.

Unless President Christine Lagarde surprises with a very dovish rhetoric in her press briefing, the euro is unlikely to react much. In fact, a greater risk is if Lagarde disappoints the markets by not sounding dovish enough.

On the data front, Germany’s ZEW economic sentiment index will be watched on Tuesday, along with the Eurozone’s final CPI estimate for March on Wednesday.

Is a BoC cut a coin toss?

A day of before the ECB, the Bank of Canada will announce its decision but it’s doubtful if it will cut rates again. The minutes of the BoC’s March meeting revealed that policymakers would have kept rates unchanged at 3.0%, instead of cutting them, had it not been for Trump’s tariffs. Trade tensions have only intensified since the last meeting, but investors see only a 40% chance of a 25-bps reduction.

Canada has obtained a temporary reprieve from the White House, with the 25% tariffs on pause for the goods that fall under the USMCA agreement. Yet, the high degree of uncertainty about what level of duties Canadian exporters will be facing in the months and years ahead is likely to weigh on the economy.

The problem for the BoC, however, is that it’s already slashed rates by a total of 225 bps, and more importantly, CPI readings have started to pick up again. With Canada imposing its own retaliatory tariffs on some US goods, inflation will probably rise further in the coming months.

Hence, investors will be watching Tuesday’s CPI report very closely, as there’s a reasonable chance the BoC may opt for another rate cut the following day.

If that turns out to be the case, the Canadian dollar might suffer a mild pullback against the US dollar.

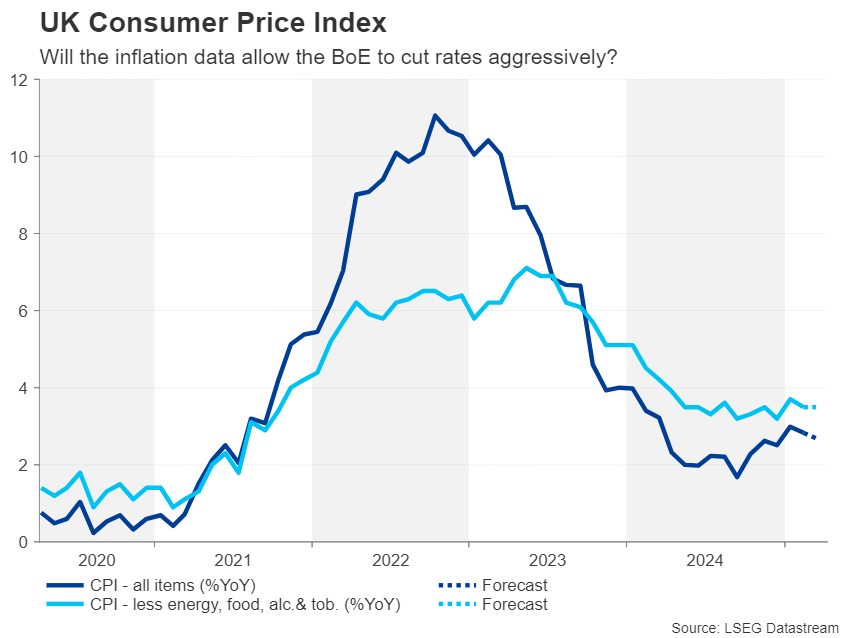

UK CPI and wage growth on pound’s radar

The pound initially benefited from the dollar’s weakness but as the stock market selloff accelerated, the bulls ran out of steam and cable took a tumble. Aside from the risk-off sentiment and worries about the impact of tariffs on the UK economy, rising gilt yields have also been weighing on sterling as this would make it more difficult for Keir Starmer’s government to respond to an economic slowdown with looser fiscal policy.

The primary strain on sterling, however, is the expectation that the Bank of England will need to reduce rates more aggressively this year amid the worsening outlook. A 25-bps rate cut is 90% priced in for the May meeting, but those expectations could change next week if the incoming employment and CPI data fuel concerns about persisting inflation.

The headline rate of CPI fell more than forecast in February to 2.8% y/y and may ease further in March before edging up again. The CPI report is out on Wednesday, while ahead of that on Tuesday, the latest employment stats will come to the fore. In particular, wage growth will be key for the BoE decision.

Stronger-than-expected numbers could dampen rate cut bets, potentially giving the pound a leg up.

China GDP growth to remain within target, for now

China will publish its latest GDP estimate on Wednesday as it refuses to give in to Trump’s demands for fairer trade treatment, escalating the war. The Chinese economy grew by 5.4% y/y in the fourth quarter of 2024 but is projected to have slowed to 5.1% in Q1.

Industrial production and retail sales numbers for March will also be released on the same day. The data is unlikely to spur much reaction even if there’s a significant surprise either to the downside or upside as investors will be more concerned about how China navigates itself through Trump’s trade storm.

With Chinese exports now being charged 125% levies and US goods facing similar tariffs, trade between the world’s two largest economies could shrink drastically in the coming months. The government may therefore choose to accompany the GDP press conference with a fresh stimulus announcement as it tries to boost domestic consumption to counter Trump’s tariffs.

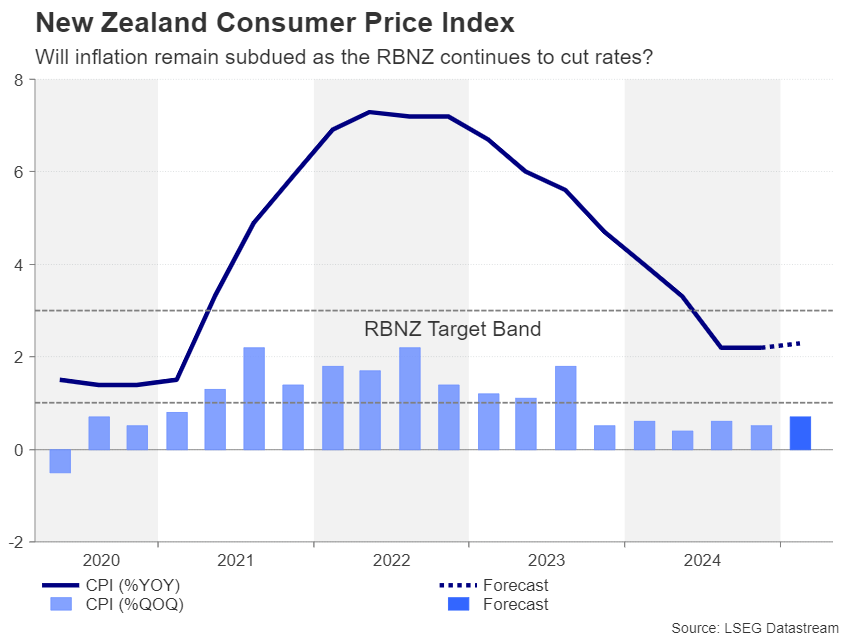

Aussie jobs, New Zealand and Japanese CPI on tap

The Australian dollar would be the biggest beneficiary from any significant stimulus update out of Beijing, as speculation grows about whether or not the Reserve Bank of Australia will cut rates at its next meeting on May 20. A 25-bps rate cut has become fully priced in following the spike in trade frictions and next week’s employment report, due on Thursday, may not necessarily change those bets much.

The New Zealand dollar has also endured quite a bit of volatility since Trump’s reciprocal tariffs were unveiled, as risk-sensitive currencies have been caught between the swings in equity markets, hopes of more stimulus by China, and expectations of steeper domestic rate cuts.

However, the focus for the kiwi on Thursday will be the quarterly CPI prints. The Reserve Bank of New Zealand just trimmed its cash rate to 3.5% and another 25-bps cut is almost fully baked in for the May meeting.

A hotter-than-expected CPI figure could dent those expectations slightly but probably not too significantly.

Staying in the region, Japan will also be publishing CPI numbers. Prior to the market turmoil, the Bank of Japan was expected to deliver nearly two rate increases in 2025. But the odds have now fallen to less than one hike. If the March CPI readings out on Friday show that inflation in Japan is not going to dissipate quickly, the yen could stretch its latest advance against the greenback.

US data might get overshadowed by trade mayhem

Finally, retail sales figures will be the highlight in the United States where it’s going to be a relatively lighter agenda. Tariff headlines are bound to dominate, however, as the uncertainty sparked by Trump’s erratic decisions is making markets nervous even as he rows back on some of the measures.

Trump’s position on China is in particular focus as neither side appear to be easing up on their defiant stance.

Still, an upbeat retail sales report on Wednesday could lift sentiment on Wall Street and provide support to the US dollar by lessening the risk of a recession.

Retail sales are forecast to have risen by 1.3% m/m in March, compared to a 0.2% increase in the prior month.

Industrial production figures are also due on Wednesday. Other data will include the Empire State manufacturing index on Tuesday, as well as building permits, housing starts and the Philly Fed index on Thursday.

Most Western markets will be shut on Friday for the Easter celebrations.

Is a Recession Looming?

- Wall Street skyrockets after Trump announces tariff delay.

- But gains remain limited as Trade War with China continues.

- Recession odds have eased, but investors remain fearful.

- The worst may not be over, deeper market wounds still possible.

Trump delays several tariffs, but continues to hit China

With a new Trade War between the US and China unfolding, investors have been afraid that a recession may be looming for the US economy.

On so-called ‘Liberation Day’, US President Trump announced a 10% baseline tariff on all imports to the US, along with higher duties on some of the nation’s biggest trading partners. The 10% baseline duties went into effect on April 5, while the higher reciprocal rates that kicked in on April 9, were postponed by 90 days in less than 24 hours.

Wall Street skyrocketed that day, with the S&P 500 recording its biggest winning day since the Great Recession and the tech-heavy Nasdaq rallying more than 12%, the most since 2001.

That said, China had a different treatment. Following the announcement by the world’s second largest economy that they will raise levies on US products to 84% and proceed with restrictions on nearly 20 US firms, the US President raised the 104% tariff on Chinese imports to 145%.

The further escalation in the US-Sino trade conflict suggests that the worst may not be behind us, even after the 90-day pause announcement reduced the odds for a US recession. After all, no one can say with certainty that Trump will not change his mind in the following days.

Recession not fully factored in, but concerns remain

So, how likely is a recession, and how much of it did the markets price in?

Before the delay announcement, JPMorgan, which was among the most pessimistic commercial banks was estimating a 60% chance for a recession in the US, while Goldman Sachs was seeing 45%. Although the former bank maintained its forecast, the latter withdrew its recession odds, and it is now estimating growth.

What’s more, the Fed itself appears in no rush to lower interest rates aggressively, with Fed Chair Powell saying on Friday that this is not the moment for a “Fed put” – the term used for actions to shore up free-falling stock markets. This suggests that the Fed is not quite anticipating a recession, although they are acknowledging the increasing risks.

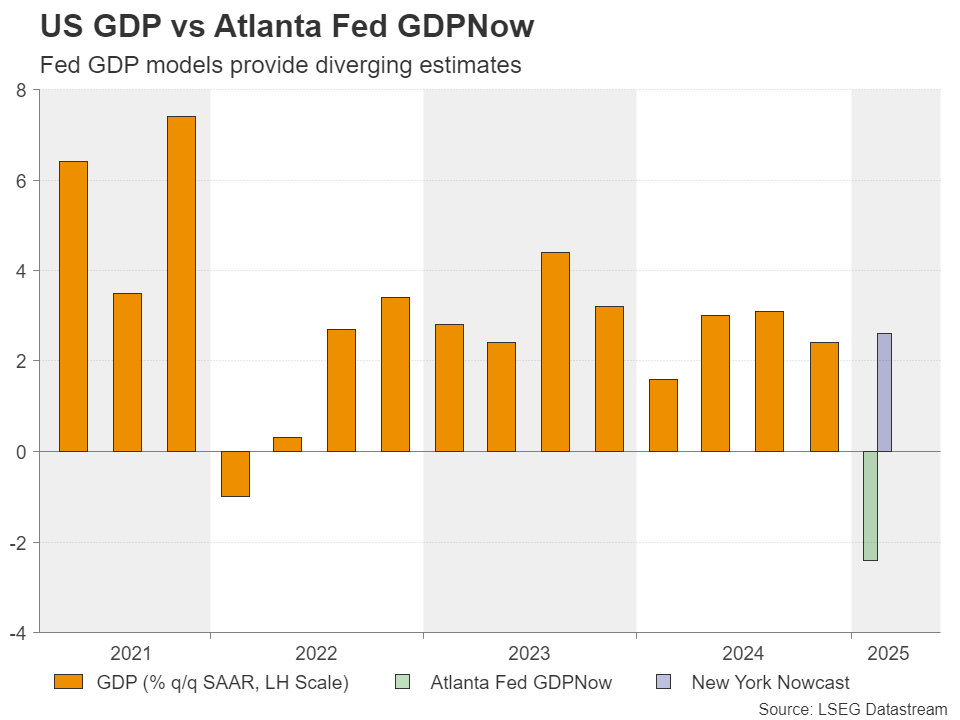

Fed models that estimate US GDP corroborate that view. Although the Atlanta Fed GDPNow model is expecting a 2.4% contraction for Q1, the New York Nowcast is anticipating a 2.6% expansion in Q1, and only a slowdown to 2.44 for Q2.

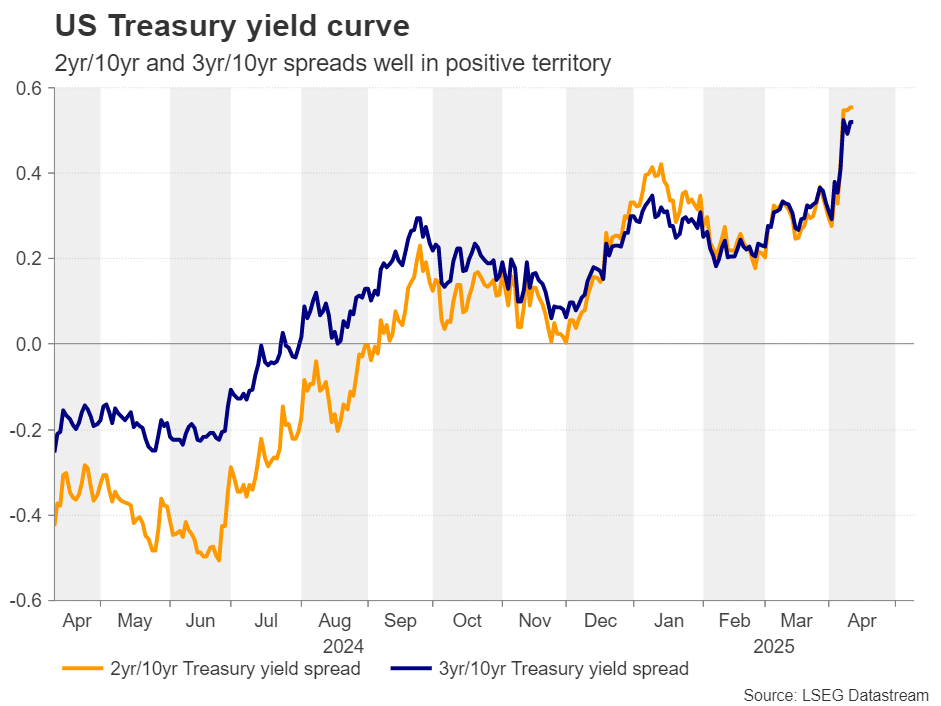

The market appears to be a bit more fearful, despite the impressive rally on Wall Street on April 9. After all, just the next day, equities pulled back again. Also, Fed fund futures are still pointing to around 90bps worth of rate cuts by the end of the year. Yet, investors are not certain about a recession, and this is evident by the fact that although that VIX – Wall Street’s fear gauge – surged to levels last seen during the COVID crisis, the US Treasury yield curve is not inverted.

Wall Street could still trade south

Therefore, there may be more to digest should the trade landscape worsen. Not only could US-Sino tensions intensify, but Trump could withdraw the delay adding pressure on the US allies to deal with a new reality. In other words, if the tit-for-tat tariff game between the US and other major economies continues, Wall Street may extend its decline as investors become even more convinced that a recession could occur this year.

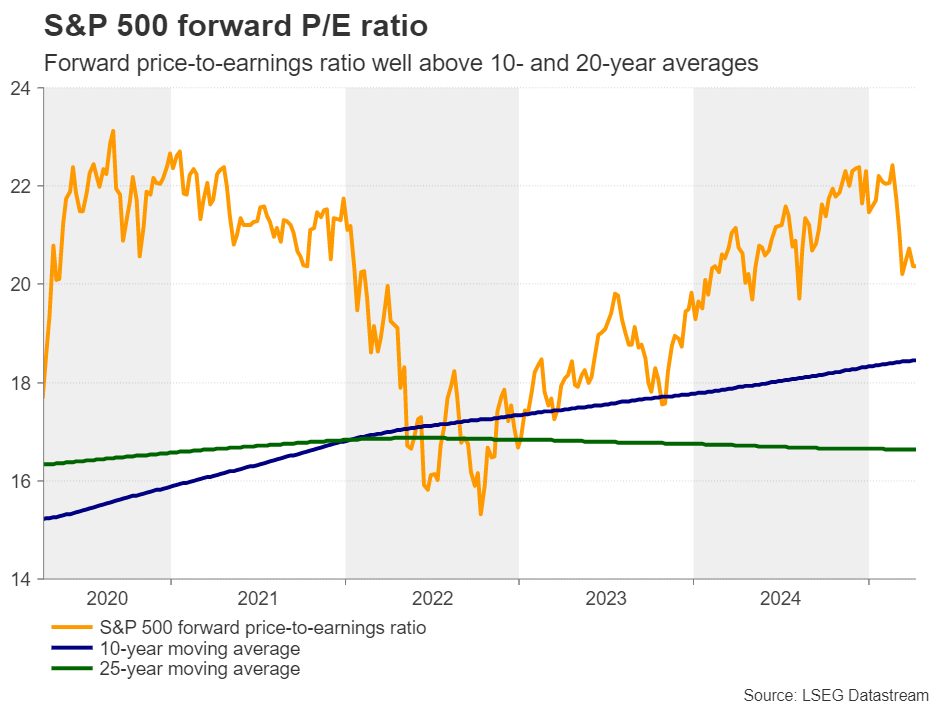

Looking at valuations, although the forward price-to-earnings ratios of stocks have fallen sharply, they are still at very high levels. For example, the forward P/E ratio of the S&P 500 is still above the levels seen in August 2024, and well above its 10- and 20-year moving averages. This adds more credence to the view that there may be more declines in store. Even bargain hunters may not feel comfortable to jump back into the action should things get worse.

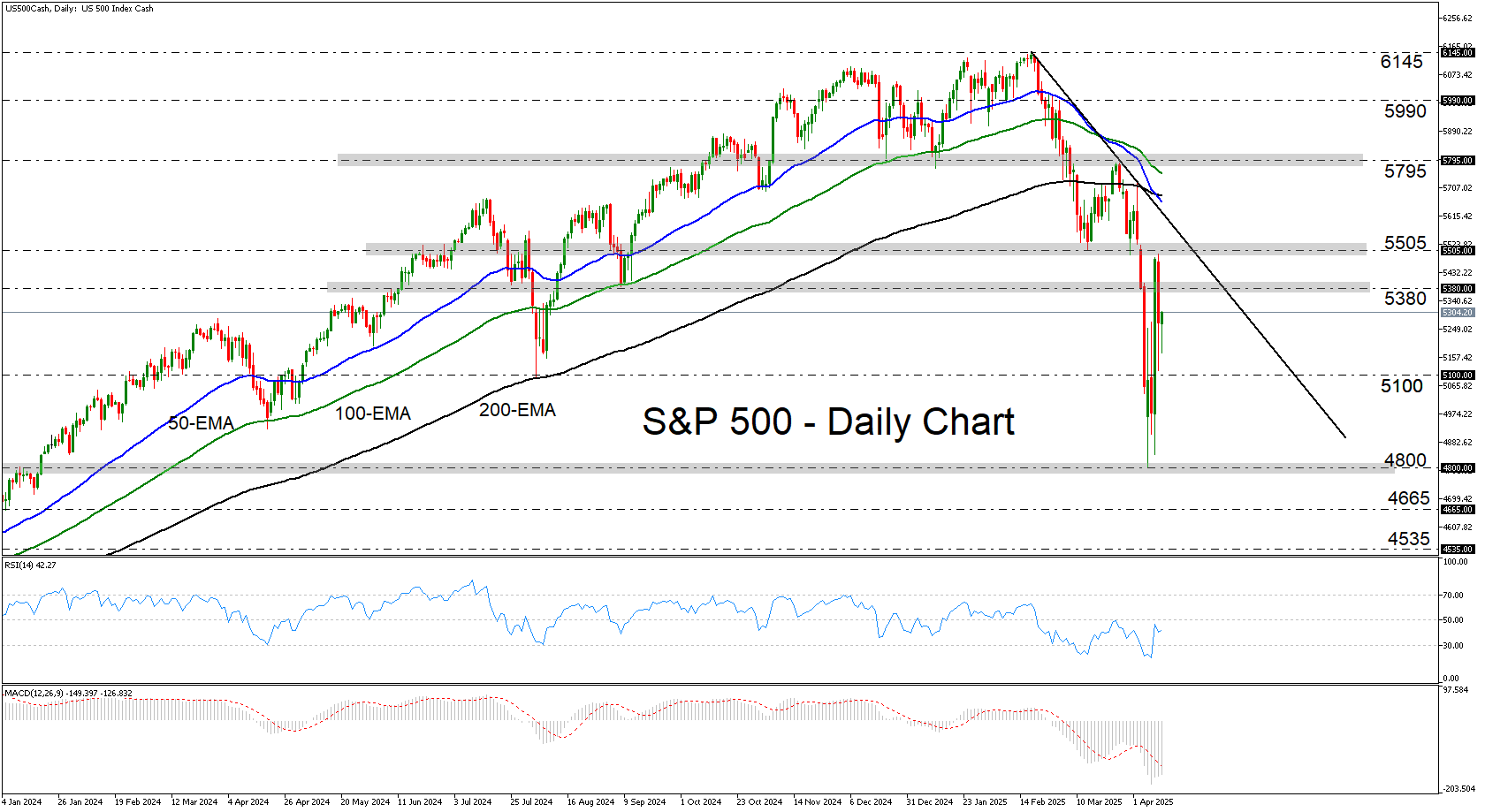

Despite impressive rally, S&P 500 remains below downtrend line

From a technical standpoint, the S&P 500 skyrocketed on Wednesday, but the rally was stopped near the 5505 zone, marked as support by the inside swing low of March 13. The bears took charge again from that zone, leaving the door open to further declines, as the index remains below all the plotted moving averages and below the downtrend line drawn from the high of February 19.

Should the bears stay in charge, they could aim for another test near the 4800 zone, the break of which would confirm a lower low and could aim for the 4665 and 4535 zones. For the outlook to turn positive, the index may need to stage a much stronger recovery than it did on Wednesday. Not necessarily within a day, but the price may have to rise above the peak of March 25 at 5795.

Weekly Focus – Trade War Lingers on as 90-Day Halt Offers Limited Relief

It has been an extremely volatile week in global financial markets that got some relief following Donal Trump's 90-day halt on the sweeping 20% tariffs he originally imposed on all US trading partners at 'Liberation Day', but at the same time the increased tensions with China caused a further increase in US Treasury yields and the EUR/USD. The 90-day halt is not absolute as countries still face a 10% duty on most exports and the 25% tariffs on cars, steel, aluminium as well as most goods from Canada and Mexico remain. Additionally, Trump boosted tariffs on China to 145% following their hike of tariffs on all US goods to 125%. Hence, the trade war is far from over and we continue to expect it to slow down global growth, but the change in Trump's plans limits the hit especially in Europe and increases the chances of tariffs being used as a negotiation tool rather than a permanent source of income. However, even with the 10-percentage point lower universal tariff rate, the increase in tariffs on China means that the effective rate with unchanged trade volumes is higher than the original tariff scenario. We are thus still talking about a substantial tightening of fiscal policy in the US, that increases recession risks.

We expect China to continue to retaliate forcefully as they believe they have just as goods cards as the US in the trade war. Xi Jinping does not seem to be about to call Trump to make a deal, but when the tit-for-tat measures calm down, lower-level talks would likely start. China believes tariffs at 145% will harm the US economy as most trade will likely stop, making it harder and more expensive to get iPhone, laptops, etc., which would put pressure on Trump especially also from farmers that lose their biggest export market. To protect the economy, we expect China to take even stronger measures to boost domestic demand but not a devaluation.

In contrast to the political news, there has been very limited data this week. The sole highlight was the US March CPI inflation, which surprised to the downside, falling to 2.4% y/y (cons: 2.5% y/y) from 2.8% y/y. Energy prices contributed negatively, while food inflation accelerated. On the core side, inflation declined to 2.8% y/y (cons: 3.0% y/y) from 3.1% y/y due to lower services inflation. Data was collected ahead of the tariff announcements and core goods inflation actually declining on a monthly basis. Hence, inflation was on a positive trend for the Fed ahead of Trump's tariff announcement that are expected to raise prices significantly in the coming year.

In the coming two weeks the main focus will be on the ECB and PBoC rate decision, the April PMI report, and US retail sales. We expect the ECB to cut the policy rates by 25bp on 17 April, bringing the deposit rate to 2.25% in line with market pricing. We expect the statement to repeat "monetary policy is becoming meaningfully less restrictive" and Lagarde to highlight downside risks to growth while abstaining from giving any clear guidance on future rate decisions. China might lower the policy rate in the week after Easter to stimulate the economy amid tariff increases. The PMI report in two weeks will be very interesting amid the growth concerns from the trade uncertainty that could show up in lower new orders. Confidence and behaviour of the US consumers are key to watch to estimate the likelihood of a severe slowdown in the US economy so the retail sales data will be watched closely. Weekly Focus will be back in two weeks and Danske Bank Research wishes all readers happy holidays!

How the ANZACs Might Handle the Trade Shock

This note discusses the key similarities and differences of the Australian and New Zealand economies with reference to how they might fare in this global trade shock.

Trade policy uncertainty is at extreme levels and could significantly impact the small open economies of Australia and New Zealand. Both countries could lose to some extent as global demand and the pattern of trade flows adjust. But beyond this common thread there are key differences that could determine how New Zealand and Australia will fare.

Trade and economic policy uncertainty has been very high for months now but really erupted this week. Financial markets swung wildly, especially in equity markets which ranged widely and where implied volatility levels have moved up towards the levels seen only during Covid, the 2012 European debt crisis and the 2008 global financial crisis.

There have been similar movements in the rules governing global trade flows. Tariff policies in the US and China especially have moved a lot – in some cases, in both directions. We are now in a transitional position of US tariffs of 10% tariffs on most countries and 145% tariff on China, while China has retaliated with 84% tariffs on US imports.

None of this is set in stone, as negotiations are ongoing, and US tariffs on non-Chinese imports are to be reviewed again in three months. And frankly, the US and China are not negotiating right now but are engaging in tit-for-tat retaliation. Hence uncertainty will remain very high.

There will be a lot of debate around the ultimate size of the change in global trade rules that the Australasian economies will need to adjust to. It’s hard to put a finger on the scale of that now. But it is interesting to reflect on the ways in which our economies might be both similarly and differently impacted as we go forward.

There are many common factors. Both countries are trade orientated; hence this global trade shock could have potentially profound implications for incomes and growth over both the short and longer term. We both have strong trade linkages with the US, China and South-east Asia. Hence weaker demand in those jurisdictions has the potential to impact our incomes – especially though lower export commodity prices.

We both have strong macroeconomic frameworks (including independent central banks) that should help us navigate any troubles to come. Our floating exchange rates will buffer us should very negative scenarios emerge. Our government debt loads are low and credit ratings top tier, providing resilience.

The bottom line in terms of the commonalities is that we are both exposed to the worsening global trade environment but have resilience factors which will help even as the global trade environment shifts to greater protectionism and balkanization of trade flows.

But there are also some key structural and cyclical differences that may matter. On the positive side of the ledger for Australia: its current account and fiscal position is unequivocally stronger than New Zealand’s and should imply more resilience to the global trade shock. Cyclically, Australian fiscal policy is easing from a position of strength, providing some support to consumption and growth. That will matter. Another key Australian strength is that it enters this period of uncertainty with stronger growth and output that is close to trend. Australian growth has been disappointing by historical standards, but the economy is not on the ropes already. The labour market in particular remains in decent shape, notwithstanding recent debates on whether the NAIRU is lower than previously appreciated and associated productivity questions.

On the New Zealand side of the ledger: a strength is that NZ is further through the monetary easing cycle than Australia – so there is more stimulus already in the pipeline. Both countries have room to ease if required, but Australian inflation may be a little higher than NZ inflation in core terms, reflecting the different positions in the cycle. New Zealand’s commodity prices have been strongly on the up in the last year as resilient demand has combined with constrained supply of agricultural export products.

New Zealand will be more resilient if global manufacturing weakens relative to consumption given its export focus on agricultural and food commodities compared to Australia’s industrial commodities and energy exports. Global industrial production could come off worse in the new tariff environment and supply chains may have further to adjust. People will still eat whereas global steel demand may or may not be resilient.

New Zealand’s main issue is that we go into this more uncertain environment with output significantly below trend, which is why policy has been easing. While the trade sector is well positioned to absorb a trade shock, it’s less the case for the domestic economy. A further issue is the New Zealand government is trying to tighten fiscal policy even though aggregate debt levels are low by global norms. The finance minister noted this week a determination to continue the consolidation process even in the face of a weaker global economy. That’s going to be a challenge.

The pattern of trade is quite interesting and could favour either country depending on how the global growth environment pans out. Australia’s trade is more heavily tilted towards China, North and South-east Asia. New Zealand is more reliant on trade with the US. Both countries have roughly the same sensitivity with respect to trade with developed countries. If US growth and consumption were to be hit relative to Asia, then New Zealand could be worse off. And of course, the opposite also applies.

The uncertainty around how the global economy will evolve means it’s hard to know whether there will be any ‘winners’ at the end of the day. Hopefully we both lose little in the end. But it’s important to consider the differences in the economies as we move forward into this mist of uncertainty.

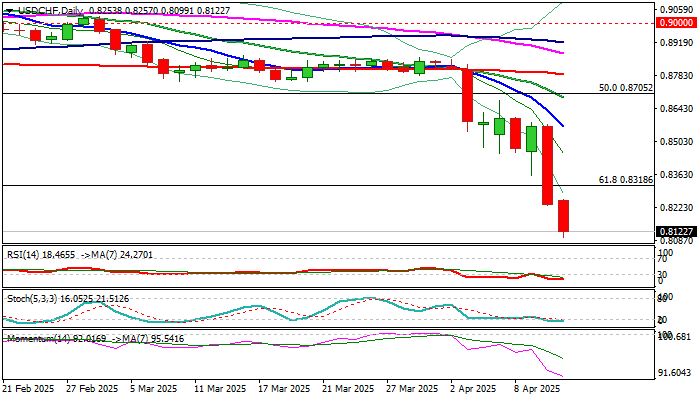

USD/CHF: Safe Haven Swiss Franc Hits Highest Levels in a Decade vs US Dollar as Trade War Escalates

USDCHF fell to the lowest in ten years on Friday as safe-have Swiss franc shined on strong migration into safety, sparked by escalation of US-China trade war.

Friday’s drop of 1.7% until early US trading comes in extension of nearly 4% loss on Thursday (the biggest one-day drop in almost three years) and the pair is on track a weekly drop of around 4.5% (the biggest weekly fall since the second week of November 2022).

Fresh weakness broke below the floor of broader range on monthly chart that generates bearish signal of continuation of larger downtrend from parity zone (tops of Oct/Nov 2022) and exposes targets at 0.8000 (psychological) and 0.7840 (Fibo 76.4% of larger 0.7067/1.0343 uptrend).

Meanwhile, price adjustments on profit-taking could be anticipated, with likely limited upticks in very favorable environment for the Swiss franc, to provide better selling levels.

Swiss National Bank had no comments so far, but intervention to curb sharp gains of the national currency, cannot be ruled out.

Res: 0.8815; 0.8851; 0.8885; 0.8906

Sup: 0.8762; 0.8725; 0.8690; 0.8615

Sunset Market Commentary

Markets

The US of A is in decay. The improvised hawkish trade policy which will likely end in a US recession puts US assets for sale. China doesn’t back down. They raised tariffs on all US goods from 84% to 125%, still below the US level (145%) but starting tomorrow. The Chinese government vowed to resolutely counterattack and fight to the end. In a Ministry of Finance statement, Beijing states: “Given that American goods are no longer marketable in China under the current tariff rates, if the US further raises tariffs on Chinese exports, China will disregard such measures.” They call US actions a joke. President Xi Jinping warned that one that goes against the world risks being isolated themselves. The US trade policy in any case helps thawing the relation between the EU and US, as witnessed by talk on a late July summit, the Spanish visit to China and discussions on lowering tariffs on EV’s. In the meantime, the EC by name of President von der Leyen warned to expand the trade war to US services if talks during the 90-day pause in applying reciprocal tariffs fail. US President Trump is on a mission to narrow the US’s $1.21tn goods deficit with the world, but seems to forget the $295bn surplus on the services trade balance (financial services, travel, big tech,…). Taxing those services would be a huge and damaging measure.

It started with US equities, it spilled to long-term US Treasuries and now it arrived at the dollar. The trade-weighted dollar (DXY) lost the 2024 low (100.16) and briefly fell below the 2023 low (99.59) to test 62% retracement on the 2021-2022 USD-rally (98.98). Losing this support area would be highly significant from a technical point of view and suggest medium term full retracement to 89.21. EUR/USD already crushed this matching resistance zone (2024 top/2023 top/62% retracement at 1.1214/74/76). The pair set an intraday top at 1.1473, just below the 2022 top at 1.1495 which can be considered as intermediate resistance in the chase back to 1.2349. Apart from USD-weakness, the euro and other European assets (eg German Bunds) stand out as safe haven asset. Daily changes on the German yield curve currently range between -6.2 bps (2-yr) and -8.5 bps (30-yr). We see a different picture in the UK and the US where the very long end of the curve is again underperforming. A new Treasury sell-off is the key risk for the remainder of today’s session. The April Michigan consumer survey which grabbed market attention last months because of a huge spike in both short term (1y) and long term (5y-10y) inflation expectations only confirmed the stagflationary fears. Sentiment tumbled further (50. 8 from 57.0). At the same time 1-y inflation expectations jumped from 5.0% to 6.7%! LT expectations from 4.1% to 4.4% The US 30-y yield adds 6.0 bps and is holding near the 5.0% barrier (4.93). An uncontrolled sell-off has the potential to trigger emergency (liquidity) measures by the Fed (this weekend?) or a second Trump fold in the trade story.

News & Views

Brazilian inflation rose 0.56% M/M and 5.48% Y/Y in March, on the higher side of the consensus expectations and compared to 1.31% M/M and 5.06% Y/Y in February. All of the nine sub-components added to the monthly rise in inflation. The biggest contributor was food prices rising by 1.17% M/M (7.68% Y/Y). Indicators of core inflation and core services inflation still suggest persistent inflationary pressures. Bloomberg estimates the average of the core inflation measures of the BCB at 0.51% M/M. Y/Y inflation also moves further above the target band of the Central bank of Brazil (3.0% +/- 1.5% tolerance). The data confirm a scenario of another further rate hike at the May 7 monetary policy meeting, even the impact of global uncertainty might enter the debate. The central bank raised the policy rate from 13.25% to 14.25% at the previous meeting on March 19.

According to Reuters reporting and referring to domestic media and government sources, Japanese Prime minister Shigeru Ishiba today set up a task force to oversee trade talks with the US. The task force is presided by Economy Minister Akazawa. According to the local press, the Economy minister will on 17 April meet US trade representative Jamieson Greer and Treasury secretary Bessent. Akazawa indicates that US policy makers are interested in discussing non-tariff barriers but also FX policy. In this context, it won’t be easing for Japanese authorities to take action against a further rise of the yen against the USD. Aside from the negotiations with the US, Ishiba is also said have instructed his cabinet to compile an a supplementary budget as early as next week to put in place measures to respond to rising prices and to the effects of the high tariffs of the Trump administration for the Japanese economy.

US Michigan consumer sentiment crashes to 50.8; inflation expectations highest since 1981

US consumer sentiment plunged to 50.8 in April, far below expectations of 55.0 and down from 57.0 in March, according to the preliminary University of Michigan survey. This marks the fourth straight month of declines, with the index now down over 30% since December 2024.

The fall was broad-based: the current conditions gauge dropped from 63.8 to 56.5, while expectations fell from 52.6 to 47.2, highlighting growing concerns about economic prospects amid the intensifying trade war.

The timing of the survey is notable—it was conducted between March 25 and April 8, just before the US partially reversed some tariffs on April 9. Thus, the data largely reflects public reaction to the earlier escalation.

Perhaps the most alarming data point was the surge in year-ahead inflation expectations, which jumped from 5.0% to 6.7%—the highest since 1981. This marks the fourth consecutive month of half-percentage-point increases or more, underscoring the risk that inflation expectations could become unanchored.