Sample Category Title

USD/CHF Daily Outlook

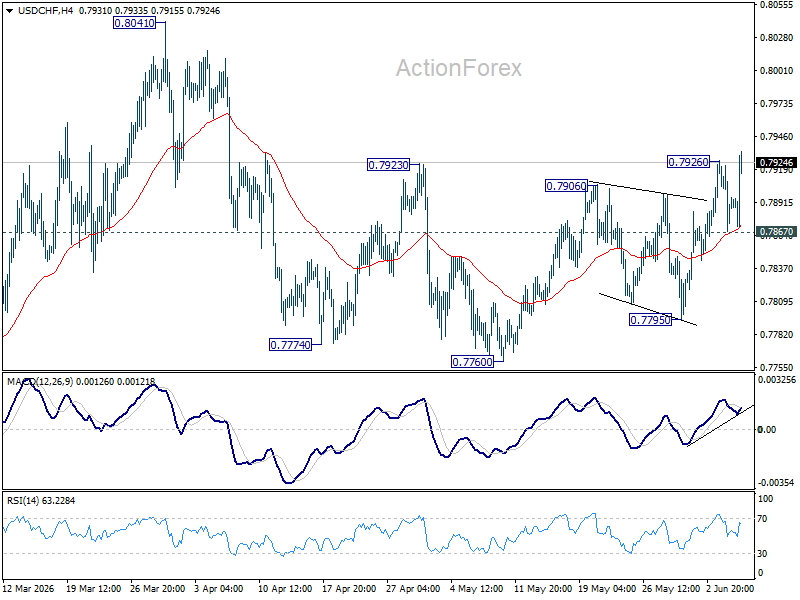

USD/CHF's rise from 0.7760 resumed by breaking through 0.7926 and intraday bias is back on the upside. Fall from 0.8041 should have completed at 0.7760. Further rally should be seen to retest 0.8041 next. On the downside, below 0.7867 minor support will turn intraday bias neutral first.

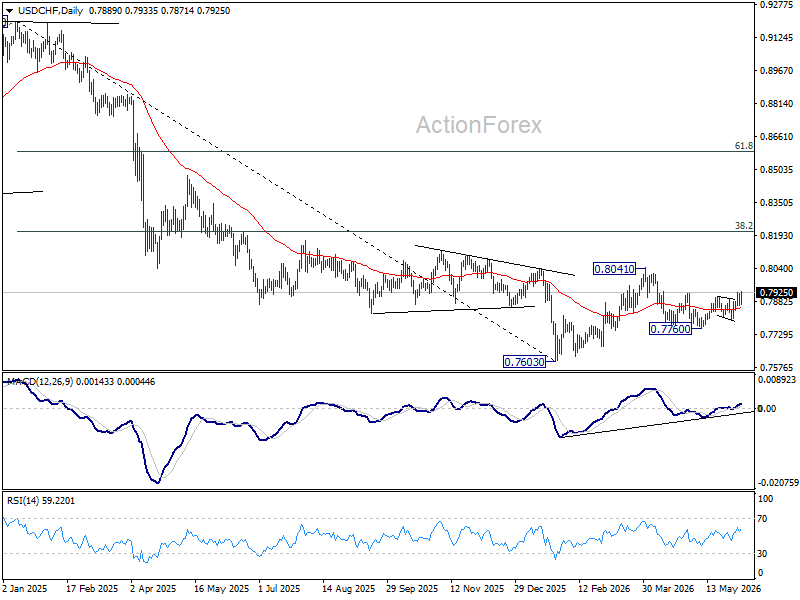

In the bigger picture, as long as 55 W EMA (now at 0.8028) holds, fall from 0.9200 is expected to continue, as part of the larger down trend. Firm break of 0.7603 will target 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382.

USD/JPY Daily Outlook

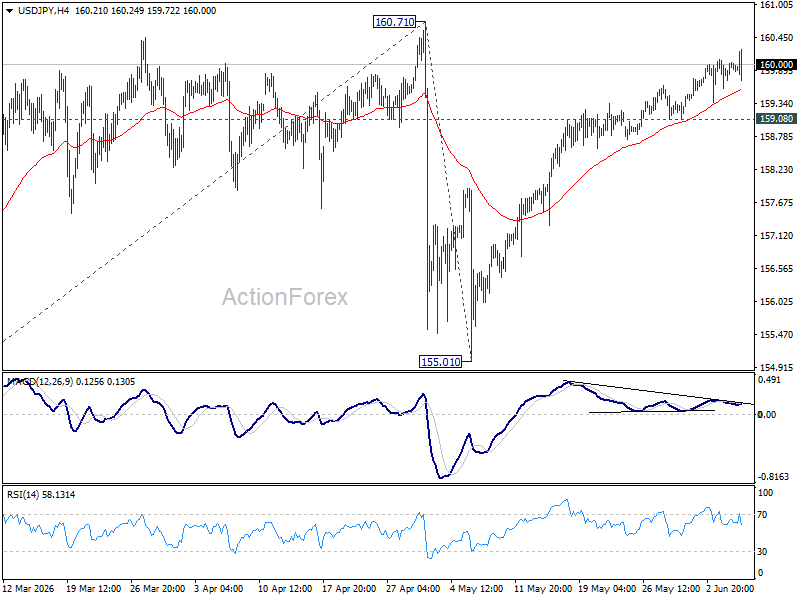

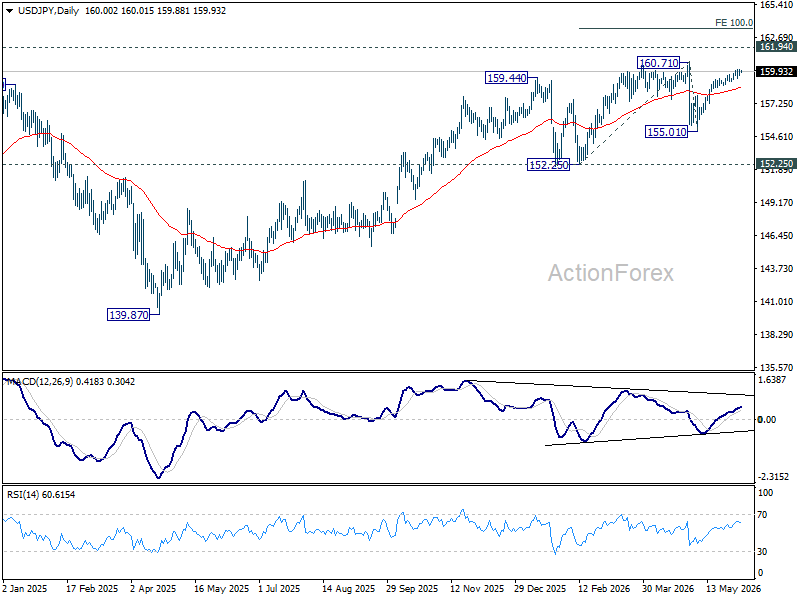

USD/JPY's rally from 155.01 is still in progress and intraday bias stays on the upside. As this rise is viewed as the second leg of the corrective pattern from 160.71, strong resistance should emerge there to cap upside. Break of 159.08 minor support will turn bias back to the downside for 55 D EMA (now at 158.56) and below. However, decisive break of 160.71 will confirm up trend resumption. That should push USD/JPY through 161.94 to 100% projection of 152.25 to 160.71 from 155.01 at 163.47 next.

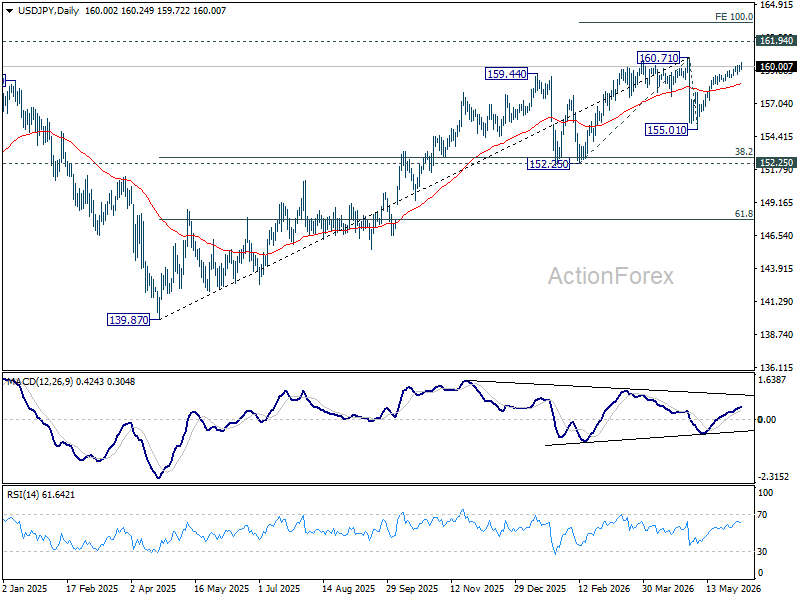

In the bigger picture, for now, corrective pattern from 161.94 (2024 high) is still seen as completed at 139.87. Rise from there is seen as resuming the long term up trend. So, break of 161.94 is expected at a later stage to resume the long term up trend. However, sustained break of 55 W EMA (now at 154.55) will dampen this view and bring deeper fall back towards 139.87 to extend the pattern from 161.94.

Dollar Rises as Strong Payrolls Reinforce Fed Patience, USD/JPY Clears 160

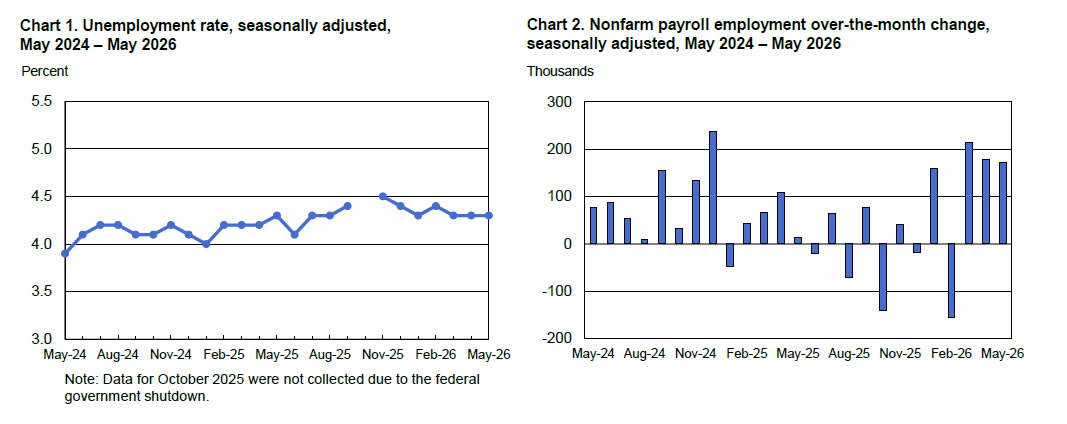

Dollar strengthened broadly in early US session after a much stronger-than-expected US employment report reinforced confidence in the resilience of the labor market. Non-farm payrolls rose 172k in May, nearly double expectations, while April's gain was revised sharply higher to 179k. Unemployment held steady at 4.3%, and wage growth remained contained, with average hourly earnings rising 0.3% mom and annual growth slowing from 3.6% yoy to 3.4% yoy. The combination of strong hiring and moderating wage pressures is likely to be welcomed by Federal Reserve officials.

Importantly, the report does not fundamentally change the Fed's current stance. Policymakers have increasingly shifted their focus away from labor-market concerns and toward inflation risks linked to elevated energy prices and the ongoing US-Iran conflict. Strong payroll growth confirms that employment remains resilient, while slower annual wage growth suggests there is still no clear evidence of a renewed wage-price spiral. For the Fed, the data provide additional room and time to assess how the oil shock is feeding through the broader economy before considering any policy response.

Markets interpreted the report as modestly supportive for the hawkish side of the policy debate. Pricing for a 25bps Fed rate hike by year-end rose to around 60% following the release. Yet the increase in tightening expectations was measured rather than dramatic, reflecting the view that one employment report is unlikely to force the Fed away from its wait-and-see approach. Instead, the data mainly strengthen the argument that policymakers can afford to remain patient while monitoring inflation developments.

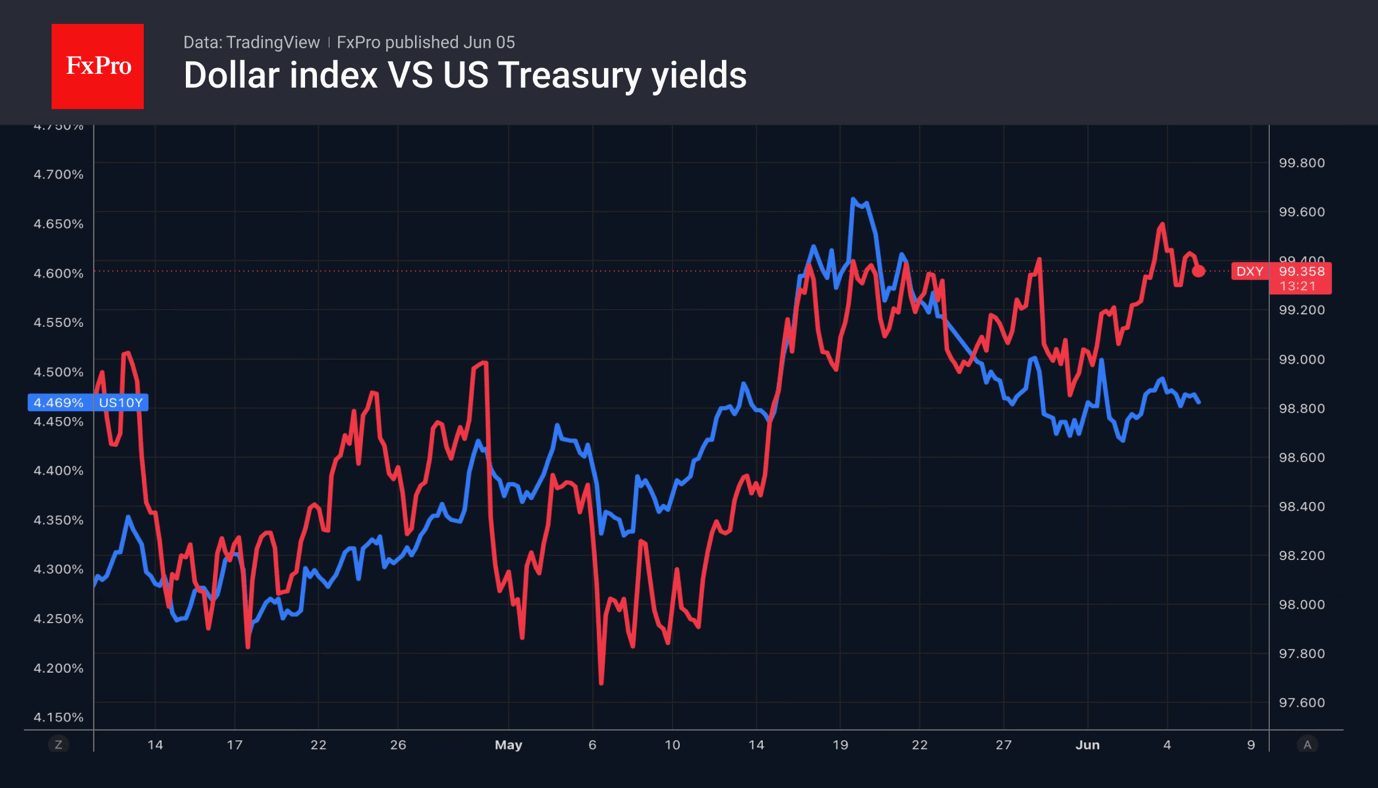

The move in Treasury yields may prove just as important as the payrolls report itself. US 10-year yields climbed back above 4.5% level, providing Dollar with an additional tailwind. If yields continue to rise in coming hours, the greenback could find broader support beyond the initial post-NFP reaction. Attention is now turning to whether Dollar can break decisively higher against Euro before the weekly close and signal a more sustained bullish momentum.

Meanwhile, strong market reaction was also seen against Yen. USD/JPY surged above the psychologically important 160 level following the payrolls release, pushing back through Japan's unofficial intervention red line. The move came despite continued warnings from Japanese officials. Earlier on Friday, reserve data showed Japan's foreign reserves fell by around USD 75 billion in May, broadly matching the Ministry of Finance's disclosure that roughly USD 73.4 billion was spent on intervention operations during the Golden Week period.

Finance Minister Satsuki Katayama reiterated that authorities would respond "appropriately at any time when necessary" and retained the right to take "decisive action" against excessive volatility. She also emphasized that Tokyo remains in close communication with Washington regarding currency developments. With USD/JPY once again above 160, markets are now focused on whether Japan will step back into the market or tolerate a fresh leg higher in the pair.

For the week so far, Dollar stands as the strongest major currency, followed by Sterling and Euro. At the other end of the table, Kiwi is the weakest performer, followed by Swiss Franc and Aussie. Loonie and Yen are positioned in the middle, reflecting support from stronger domestic data in Canada and ongoing intervention concerns in Japan.

US Non Farm Payrolls Crush Expectations with 172k Growth

The May payrolls report delivered exactly the outcome the Fed wanted to see: strong hiring, stable unemployment, and no major wage surprise. Payroll growth nearly doubled expectations, while April's figure was revised sharply higher. The result does not guarantee another rate hike, but it gives policymakers greater freedom to focus on inflation risks rather than labor-market weakness. Read More.

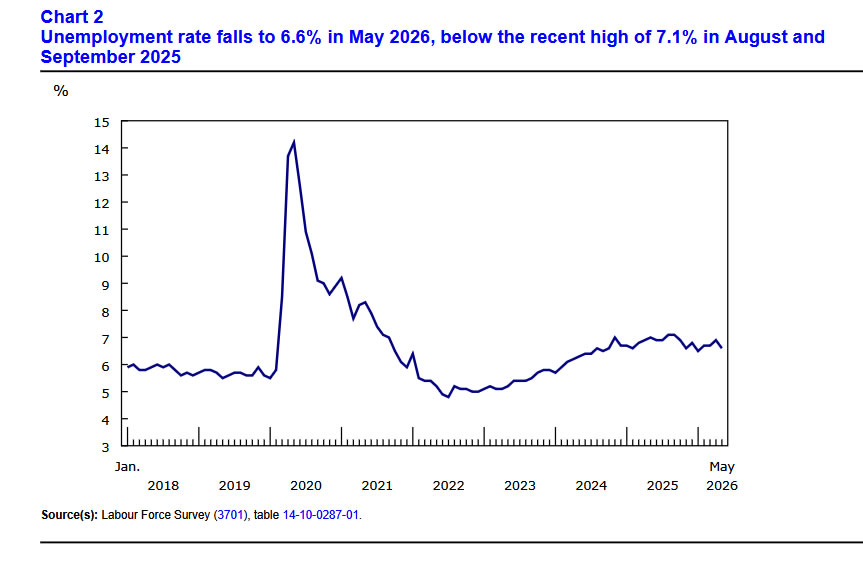

Canada Employment Surges 87.8K, Unemployment Falls to 6.6%

Canada's labor market delivered a surprise comeback in May. Employment surged by 87,800, unemployment fell to 6.6%, and full-time hiring jumped by 154,000. After losing 112,000 jobs during the first four months of the year, the report suggests the labor market may be far more resilient than recent data had implied. Read More.

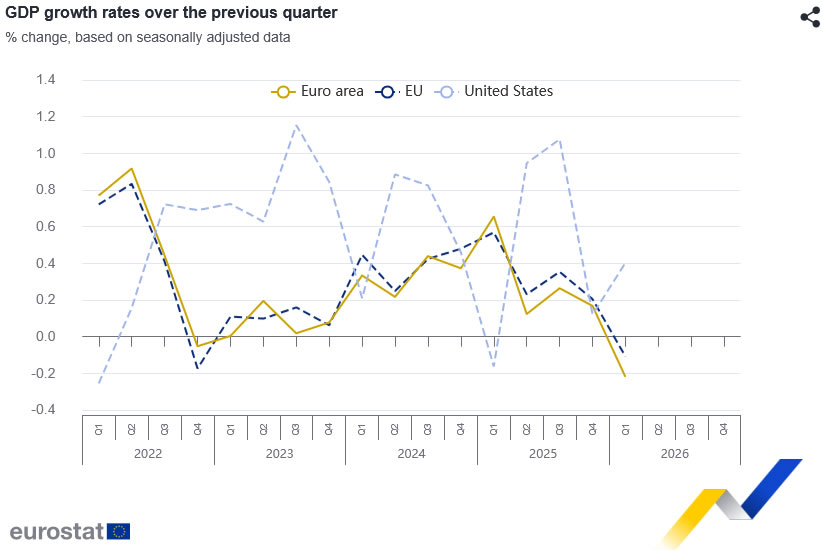

Eurozone Economy Contracts -0.2% qoq in Q1 as Trade and Investment Drag Growth Lower

The Eurozone economy contracted in the first quarter of 2026 as trade and investment weakened significantly. Household spending and government consumption continued to support activity, but not enough to offset falling capital expenditure and weaker external demand. Annual growth slowed to just 0.3%, underscoring the increasingly difficult balance facing the ECB as inflation remains elevated while economic momentum fades. Read More.

Japan Wage Growth Surges to 34-Year High Streak, Consumption Still Lags

Japan's long-awaited wage revival is gaining momentum. Real wages rose for a fourth consecutive month in April, while nominal wage growth exceeded 3% for a third straight month for the first time in more than three decades. The figures strengthen the case for further BoJ normalization, although household spending remains too weak to declare victory just yet. Read More.

USD/JPY Daily Outlook

USD/JPY's rally from 155.01 is still in progress and intraday bias stays on the upside. As this rise is viewed as the second leg of the corrective pattern from 160.71, strong resistance should emerge there to cap upside. Break of 159.08 minor support will turn bias back to the downside for 55 D EMA (now at 158.56) and below. However, decisive break of 160.71 will confirm up trend resumption. That should push USD/JPY through 161.94 to 100% projection of 152.25 to 160.71 from 155.01 at 163.47 next.

In the bigger picture, for now, corrective pattern from 161.94 (2024 high) is still seen as completed at 139.87. Rise from there is seen as resuming the long term up trend. So, break of 161.94 is expected at a later stage to resume the long term up trend. However, sustained break of 55 W EMA (now at 154.55) will dampen this view and bring deeper fall back towards 139.87 to extend the pattern from 161.94.

Canada Employment Surges 87.8K, Unemployment Falls to 6.6%

Canada's labor market delivered a much stronger-than-expected performance in May, with employment rising by 87.8k compared with expectations for a gain of just 10.2k. The increase marked the first significant monthly advance since November 2025 and followed a decline of -17.7k in April. While the result does not fully offset the weakness seen earlier this year, it represents a notable turnaround after cumulative job losses of -112k during the first four months of 2026.

The quality of hiring was particularly encouraging. Full-time employment surged by 154k, highlighting solid underlying labor demand rather than temporary or part-time hiring. As a result, the unemployment rate fell from 6.9% to 6.6%, beating expectations for an unchanged reading. The employment rate also improved by 0.2 percentage points to 60.7%, indicating broader labor-market participation and stronger workforce absorption.

Despite the sharp rebound in hiring, wage growth eased noticeably. Average hourly earnings increased 3.0% yoy in May, slowing from 4.5% yoy in April. That moderation should help alleviate concerns about wage-driven inflation pressures and may reduce any urgency for the Bank of Canada to consider tighter policy.

| Indicator | Previous | Latest | Expectation |

|---|---|---|---|

| Employment Change | -17.7k* | 87.8k | 10.2k |

| Unemployment Rate | 6.9% | 6.6% | 6.9% |

| Employment Rate | 60.5% | 60.7% | — |

| Avg. Hourly Wages Y/Y | 4.5% | 3.0% | — |

| Category | Change |

|---|---|

| Total Employment | +87.8k |

| Full-Time Employment | +154.0k |

| Part-Time Employment | -66.2k |

US Non Farm Payrolls Crush Expectations with 172k Growth

US labor market resilience was on full display in May as non-farm payrolls rose 172k, nearly double market expectations of around 85k. The report was further strengthened by a sizable upward revision to April's payroll gain from 115k to 179k, indicating that hiring momentum was considerably firmer than previously thought.

The unemployment rate held steady at 4.3%, while the participation rate was unchanged at 61.8%, suggesting labor-market conditions remain broadly stable despite growing concerns about slowing economic growth.

Wage data were largely in line with expectations. Average hourly earnings rose 0.3% mom after 0.2% in April, while annual wage growth slowed from 3.6% yoy to 3.4% yoy.

The moderation in yearly wage growth may ease some concerns about a wage-price spiral, but the combination of strong hiring, stable unemployment, and still-solid wage gains is unlikely to alter the Fed's broadly hawkish stance.

| Indicator | Previous | Latest | Expectation |

|---|---|---|---|

| Non-Farm Payrolls | 179k* | 172k | 85k |

| Unemployment Rate | 4.3% | 4.3% | 4.3% |

| Participation Rate | 61.8% | 61.8% | — |

| Avg. Hourly Earnings M/M | 0.2% | 0.3% | 0.3% |

| Avg. Hourly Earnings Y/Y | 3.6% | 3.4% | 3.4% |

*April revised from 115k to 179k

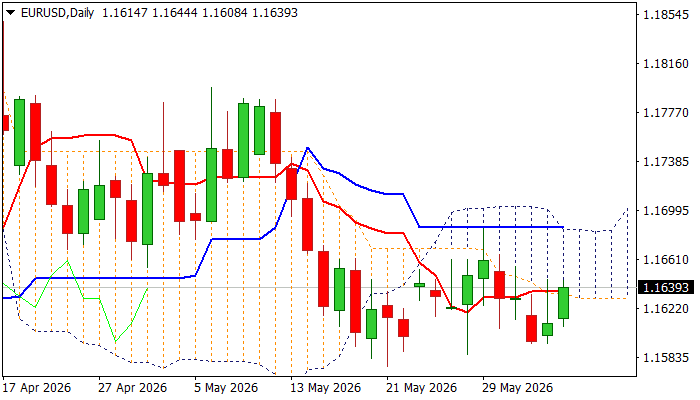

EURUSD Looks for Direction Signal to End Extended Sideways Mode

The Euro firmed on Friday and probes again through initial barrier at 1.1635 (daily cloud base / daily Tenkan-sen) after short-lived cloud penetration on Thursday which left daily candle with long upper shadow.

Daily cloud continues to cap upticks for almost two weeks, contributing to overall bearish daily structure (cluster of converged DMAs stays just above the price and created several bear-crosses / 14-d momentum remains in negative territory).

On the larger timeframe, the price remains underpinned by ascending and thick weekly cloud for the ninth consecutive week, that contributes to mixed signals, keeping the price action in directionless mode and holding within 1.1595/1.1685 range, with violation of either range boundary needed to generate initial direction signal.

Res: 1.1664; 1.1685; 1.1697; 1.1712

Sup: 1.1600; 1.1576; 1.1500; 1.1443

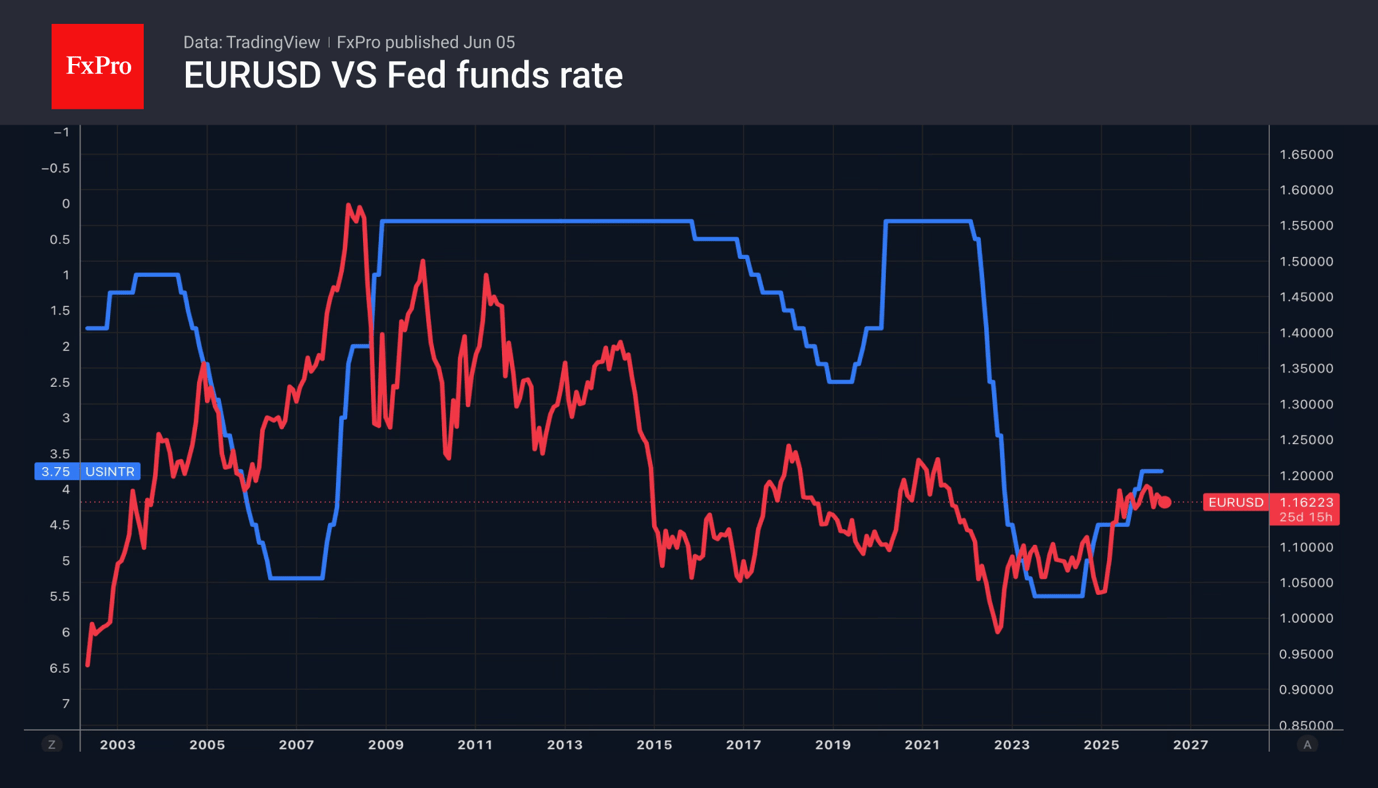

Dollar: Is History Repeating Itself?

- Mixed news from the Middle East is helping the greenback.

- Growing similarities with the 1970s for the Fed.

The US dollar has recovered after Donald Trump said negotiations with Iran are in their final stages. This contradicts Tehran’s statement that talks with Washington have made no progress and Hezbollah’s refusal to comply with the US-imposed ceasefire with Israel. Confusing developments in the Middle East are heightening uncertainty and boosting demand for safe havens.

The US dollar has stabilised despite the fall in Brent crude and the resulting decline in Treasury yields. The likelihood of the Fed tightening monetary policy in 2026 is now below 50%. According to MLIV Pulse, 45% of investors surveyed believe the federal funds rate will remain unchanged this year, 35% expect it to rise, and 15% expect it to fall. More than half of respondents expect the US currency’s correlation with oil to strengthen. More than a third of investors expect the Dollar index and Brent crude to move lower together in the medium term.

This aligns with the Reuters consensus forecast for the EURUSD exchange rate to rise to 1.18, 1.19, and 1.20 over 1, 3, and 12 months, respectively. The baseline scenario is that the conflict in the Middle East will end, helping to shift Donald Trump’s focus from foreign policy to domestic issues. This probably means the White House will resume its pressure on the central bank to cut interest rates.

The current situation in financial markets and the global economy is, in many ways, reminiscent of the events of the 1970s. Back then, the oil crisis triggered a surge in inflation. However, instead of raising the federal funds rate, the central bank began to cut it under pressure from the White House. This led to uncontrolled price rises, successive rounds of aggressive monetary tightening, and a double-dip recession.

According to research by the Boston Fed, such a scenario is most likely to be avoided, as increased oil production has made the United States more resilient to oil shocks. Whereas in the 1970s inflation rose by 2.2 percentage points, it is now expected to rise by only 1.5 percentage points. Back then, unemployment jumped by 1.8 percentage points; today, the labour market is still generating new jobs, at least for now.

Intervention or Surrender? How Far Is Japan Willing to Draw on Its $1.3 Trillion War Chest?

Japan's latest reserve data have transformed the debate around the Yen. The question is not whether Tokyo is willing to intervene. It already has. The question now is how many times it is willing to do so. Data released on Friday showed Japan's foreign reserves fell by around USD 75 billion in May. The decline closely matches the Ministry of Finance's confirmation that Japan spent a record JPY 11.73 trillion, or roughly USD 73.4 billion, intervening in currency markets through May 28.

The figures strongly suggest that Japan financed much of the intervention by drawing down foreign securities, including US Treasuries. While the country's USD 1.3 trillion reserve stockpile remains enormous, the latest data provide the clearest evidence yet that intervention carries a real financial cost. Markets now have a benchmark for how much Tokyo is prepared to spend defending the currency. That benchmark is substantial, but it has not fundamentally altered the underlying trend. After briefly stabilizing, USD/JPY is once again pressing toward the psychologically important 160 level.

Japanese officials continue to signal readiness to act. Finance Minister Satsuki Katayama reiterated on Friday that authorities would respond "appropriately at any time when necessary" and retain the right to take "decisive action" against excessive volatility. She also stressed that Japan remains in close communication with the United States regarding exchange-rate developments. The verbal warnings have helped slow the pace of Dollar gains, but they have not changed the market's broader focus on widening policy divergence between the Federal Reserve and the Bank of Japan.

That divergence may face its next major test with the US non-farm payrolls report. A strong employment report, particularly one accompanied by faster wage growth or lower unemployment, could reinforce expectations that the Fed will remain focused on inflation risks rather than labor-market weakness. Such an outcome would likely push Treasury yields and Dollar higher across the board. If USD/JPY surges through 160 again, Japanese policymakers may soon face the same decision they confronted only weeks ago: intervene once more or tolerate further Yen weakness.

From a technical angle, the situation is finely balanced. The current rise from 155.01 is still viewed as the second leg of the corrective pattern from 160.71 high. Under that interpretation, another push higher should eventually be capped below 160.71 followed by a reversa. Firm break below 55 D EMA, currently around 158.62, would strengthen the case that the third leg lower has already begun and bring 155.01 back into focus.

However, the risks are not one-sided. Decisive break above 160.71 would invalidate the corrective view and suggest that the broader uptrend has resumed. Such a move would open the way to a through 2024 high at 161.94 to 100% projection of 152.25 to 160.71 from 155.01 at 163.47.

Eurozone Economy Contracts -0.2% qoq in Q1 as Trade and Investment Drag Growth Lower

The Eurozone economy contracted in the first quarter of 2026. GDP fell by -0.2% qoq, reversing the 0.2% expansion recorded in the previous quarter, while annual growth slowed sharply to 0.3% yoy from 1.2% yoy. Across the broader EU, GDP declined by -0.1% qoq, with annual growth easing to 0.7% from 1.4%.

The details suggest that domestic demand remained relatively resilient but was not strong enough to offset weakness elsewhere. Household consumption and government spending each contributed 0.1 percentage point to growth in both the Eurozone and EU, indicating that consumers and the public sector continued to provide modest support despite a challenging economic environment.

However, investment activity weakened, with gross fixed capital formation subtracting -0.1 percentage point from growth. Inventories also dragged on Eurozone GDP, while the largest negative contribution came from trade. Net exports reduced growth by -0.3 percentage point in the Eurozone and -0.2 percentage point in the EU, underscoring the impact of softer external demand and a sluggish global trade backdrop.

Performance across member states was highly uneven. Denmark led growth with a 1.9% quarterly expansion, followed by Estonia and Malta at 1.1%. At the other end of the spectrum, Ireland posted a sharp 12.1% contraction, while Lithuania, Sweden, and France also recorded declines.

The broad picture is one of a Eurozone economy losing momentum just as inflation remains elevated, complicating the ECB's task and reinforcing concerns about a stagflationary environment.

| Indicator | Q1 2026 | Q4 2025 | |

|---|---|---|---|

| Eurozone GDP Q/Q | -0.2% | +0.2% | |

| EU GDP Q/Q | -0.1% | +0.2% | |

| Eurozone GDP Y/Y | +0.3% | +1.2% | |

| EU GDP Y/Y | +0.7% | +1.4% |

| Component | Eurozone Contribution | EU Contribution |

|---|---|---|

| Household Consumption | +0.1 pp | +0.1 pp |

| Government Consumption | +0.1 pp | +0.1 pp |

| Fixed Investment | -0.1 pp | -0.1 pp |

| Inventories | -0.1 pp | 0.0 pp |

| Net Exports | -0.3 pp | -0.2 pp |

Chart Alert: EUR/USD Finds Support as ECB Hawkishness Offsets Fed Strength Ahead of NFP

Key takeaways

- EUR/USD remains resilient ahead of the US Nonfarm Payrolls report, supported by expectations that the European Central Bank will maintain a more aggressive tightening path than the Federal Reserve despite weak Eurozone growth.

- Interest-rate expectations are becoming increasingly supportive for the euro, with the Eurozone-US policy rate differential narrowing as markets price additional ECB rate hikes while the Federal Reserve faces a more balanced growth-versus-inflation trade-off.

- Technical indicators suggest EUR/USD may be forming a near-term base above key channel support at 1.1580, with improving momentum signalling a potential short-term recovery toward the 1.1645–1.1720 resistance zone.

Ahead of today’s critical US Nonfarm Payrolls release, the EUR/USD pair has been grinding sideways around the 1.1610-1.1620 zone, showing resilience amid a fundamentally strong US Dollar environment.

Diverging growth vs. converging hawkishness

The primary catalyst today will be the US labour market data. According to Reuters, the US economy is expected to have added 85,000 jobs in May, representing a slowdown from April’s 115,000, while the unemployment rate is forecast to remain unchanged at 4.3%.

A “slow-hire, slow-fire” equilibrium continues to anchor the US labour market, keeping conditions stable enough for the Federal Reserve to maintain its higher-for-longer stance. In fact, market pricing from the Fed funds futures market currently reflects a roughly 60% probability of a 25-basis-point hike by the Fed at its December 2026 meeting under new Chair Kevin Warsh.

Earlier this week, mixed signals, from stronger ADP and JOLTS data to an uptick in weekly jobless claims (225K), have kept traders cautious, clipping the USD slightly in recent sessions.

On the other side of the Atlantic, the Euro is being supported by an aggressively hawkish European Central Bank (ECB). Despite the Eurozone facing stagflation risks, with Q1 GDP growth a meagre 0.1% q/q, inflation remains sticky, hitting 3.2% y/y, largely driven by energy shocks.

Consequently, the latest Reuters polling indicates the ECB is highly likely to hike its deposit rate to 2.25% next week, providing a solid floor for the single currency and countering the dollar’s strength.

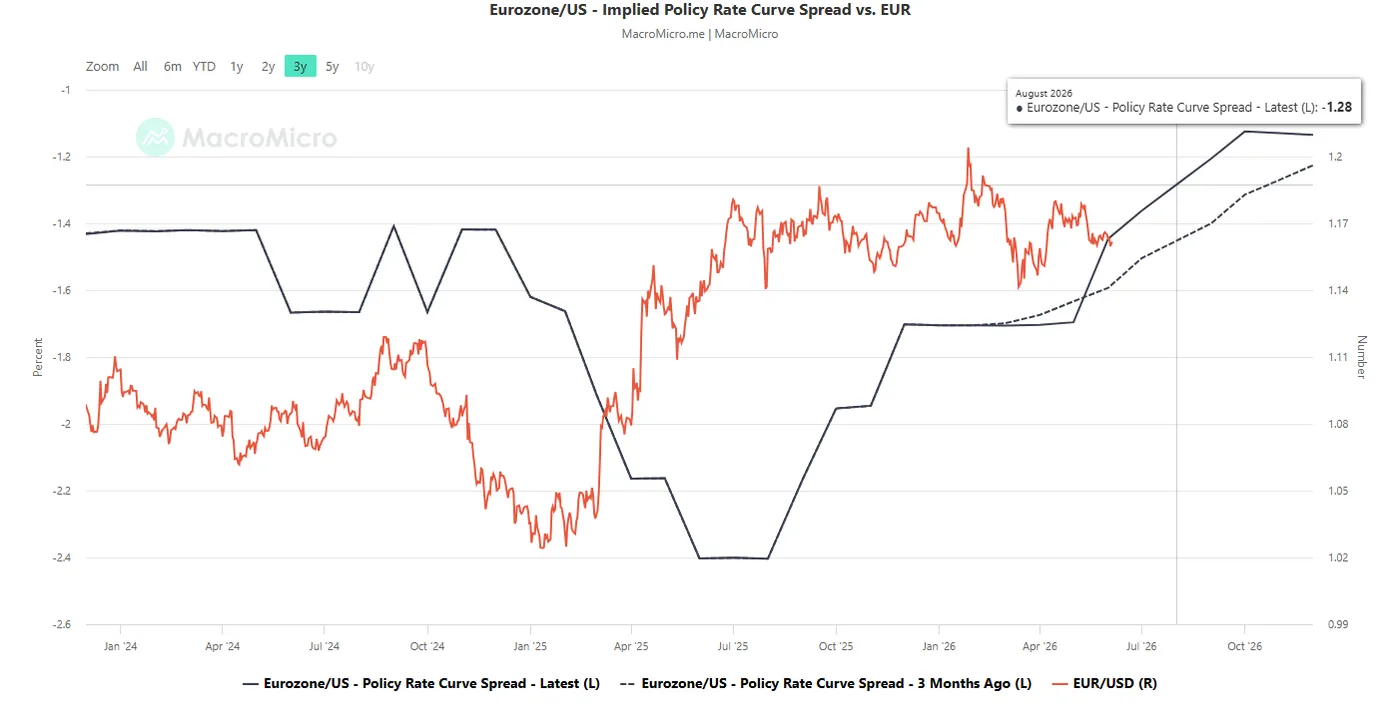

Further steepening of the Eurozone/US implied policy rate curve spread

Fig. 1: Eurozone/US implied policy rate curve spread as of 5 Jun 2026 (Source: MacroMicro). The information presented is historical information, and past performance is not indicative of future performance.

Also, the monthly implied future policy interest rate curves for the Eurozone and the US, based on short-term interest rate futures, have steepened.

The Eurozone/US implied policy rate curve spread in August 2026 has increased to -1.28% from June 2026’s print of -1.45% and shifted upwards from -1.45% three months ago (see Fig. 1).

These observations suggest that the ECB is likely to be more hawkish or less dovish than the Fed, reinforcing a “floor” on the EUR/USD.

Let’s now focus on the short-term trajectory (1 to 3 days) of the EUR/USD from a technical analysis perspective.

Forming a potential minor base above the medium-term ascending channel support

Fig. 2: EUR/USD minor trend as of 5 Jun 2026 (Source: TradingView). The information presented is historical information, and past performance is not indicative of future performance.

Trend bias: Bullish bias above 1.1580 medium-term pivotal support for a minor recovery (see Fig. 2).

Resistances: 1.1645/1660 (also the 20-day moving average), 1.1685 (also the 200-day moving average), 1.1720 (also the 61.8% Fibonacci retracement of prior decline from 6 May 2026 high to 21 May 2026 low).

Supports: 1.610/1595 (4 June 2026 minor low & medium-term ascending channel support from 13 Mar 2026 low), 1.1580 (MT pivot), 1.1555 (7 April 2026 congestion).

Key elements to support the near-term bullish bias on EUR/USD

- The recent sideways movement in EUR/USD since 21 May 2026 has formed a base/floor just above the lower boundary of the medium-term ascending channel in place since the 13 March 2026 low.

- The hourly RSI momentum indicator has staged a bullish breakout after finding support on its ascending trendline, suggesting a potential resurgence of short-term bullish momentum.