Sample Category Title

Sunset Market Commentary

Markets

Today’s trading should show the Trump (bond) put at work, including the hoped-for positive spill-overs on other assets. The US president buying time/giving room to negotiate trade arrangements with the US, yesterday triggered a sharp bounce in US equities and so did Asian and European indices this morning. However, after a swift first reaction, the move stalls. European indices mostly trade off the opening top (EuroStoxx 50; +5.0%). US indices return about 2% of yesterday’s gain (S&P 500). (US) Bond markets are looking for a new equilibrium, balancing reduced need of immediate Fed help and a further hoped-for reduction in risk premia at the long end of the curve. The Trump tariff-put clearly isn’t of the same nature as an outright ‘Fed-bailout’ that occurred e.g. at the time of corona. US bond investors are taking a wait-and-see mode. (Political) policy uncertainty remains high. A flaring-up of the sell-US trade isn’t excluded yet. Intraday, US yields temporary lost a few additional bps after the release of softer than expected US March CPI (-0.1% M/M and 2.4% Y/Y from 2.8% for headline; 0.1% M/M and 2.8% Y/Y for core). This is good news, but is a photo from a different era before extreme turmoil from the reciprocal tariffs culminated. It’s a better starting point, but tells little about the dynamic going forward. The US yield curve steepens with the 2-y declining 8 bps. The 30-y yield adds 2 bps. This evening’s $22bn 30-y Treasury action for sure is a better pointer on the strength of the Trump put. For now we’re not impressed by the easing in risk premia at the long end of the US curve. German yields show different dynamics. The German 2-y yield jumps 11 bps. The 2-y swap adds 4 bps. This captures reduced expectations for ECB support to counter demand pressures from the tariffs as well as an easing of the safe haven bid for bunds. The 10-y currently adds 2 bps. The jury is still out, but if long-term Bunds indeed are gaining a bigger overall safe haven role, the modest decline in bonds/rise in yields suggests investors are in no big hurry to return protection. The US government probably hopes for an orderly further weakening of the dollar. In this respect, Trump’s tariff pause at least didn’t change a poor USD performance of late. DXY falls from an 103 open to currently trade near 101.8. EUR/USD regains strong traction testing the 1.11 area. The YTD top (1.114) is within reach. The 1.1276 2023 top is looming on the horizon. Also Brent oil fails to stay north of $65b.

Trade-related uncertainty earlier this week put hefty pressure on smaller, less liquid currencies including the likes of the Norwegian and Swedish krone and the CE currencies (CZK, HUF, PLN). They gained against the euro in thin post-European trading yesterday, but mostly trade again in the defensive today. Another pointer that overall trade-related uncertainty still lingers? A similar narrative applies to sterling. EUR/GBP yesterday evening dropped from the 0.865 area to about 0.855. Sterling today gains against an overall weak dollar, but EUR/GBP trades again at 0.86+. In this respect, the modest easing at the LT end of the UK yield curve (30-y -12 bps at 5.45%, only slightly more than halve of yesterday’s rise) also doesn’t give that much comfort.

News & Views

Last week’s preliminary Czech inflation today confirmed with prices rising 0.1% M/M and 2.7% Y/Y. Today, the Czech National Bank commented on the release. IT was slightly higher than the 2.6% projected in the February monetary policy report. Core inflation stayed at 2.5% (vs 2.4% expected). Within core inflation, prices of goods rose 0.1% and prices of services by 4.2%. Imputed rent rose 3.6% Y/Y, driving up both core and headline inflation. Inertia in services inflation, including imputed rent, continues to pose a risk to keep inflation close to target and confirms that the cautious approach to easing monetary policy is appropriate. CNB expects annual inflation to fall temporarily due to base effects. The near term effect of the trade wars could be observed in lower oil and commodity prices, but longer term tariffs may have an inflationary effect. This strengthen the case for a final 25 bps CNB rate cut in May (to 3.5%) before installing a long pause. EUR/CZK trades slightly higher today within the broad 24.90-25.50 trading range

The EU will delay for 90 days the countermeasures over 25% imports on steel and aluminum exports announced only yesterday. They targeted around €21bn of US goods but are suspended after Trump lowered the reciprocal tariff rate to EU exports from 20% to 10%. EC President von der Leyen wants to give negotiations a chance. If they fail, countermeasures will kick in. Preparatory work on further measures continues as well with the US preparing tariffs on lumber, semiconductor chips and pharmaceutical products.

Fed’s Logan: Tariff driven inflation mustn’t take root

Dallas Fed President Lorie Logan emphasized today that Fed must be vigilant in preventing tariff-related price increases from "fostering more persistent inflation".

She noted that the inflationary impact of tariffs hinges on two key variables: how rapidly businesses pass higher import costs onto consumers, and whether long-term inflation expectations stay anchored.

"A sustained burst of inflation could lead households and businesses to expect further price increases, especially following the persistently elevated inflation in recent years." she warned.

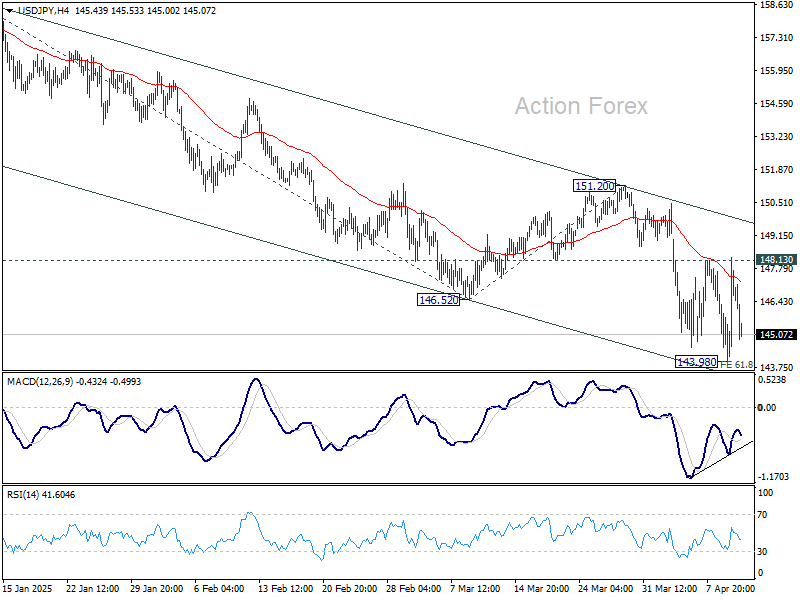

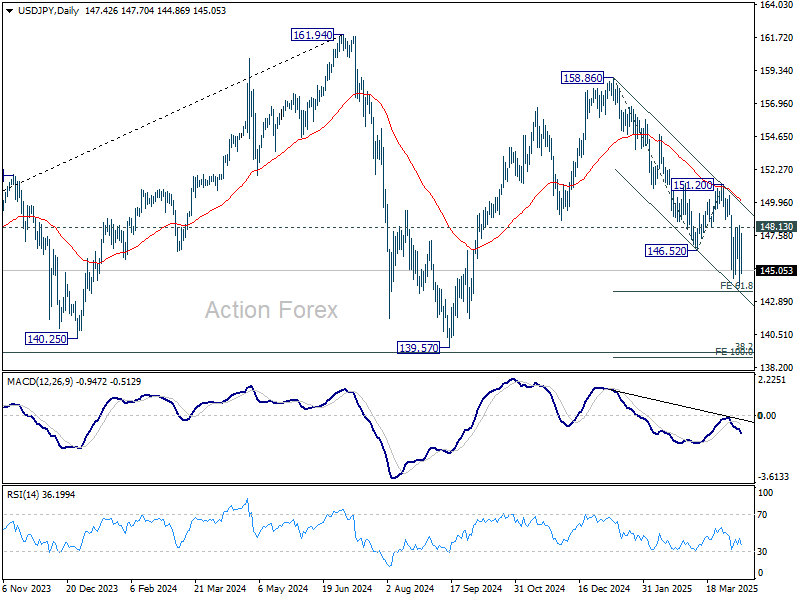

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 145.08; (P) 146.68; (R1) 149.36; More...

No change in USD/JPY's outlook and intraday bias stays neutral. On the upside, firm break of 148.13 resistance will confirm short term bottoming, and turn bias back to the upside for 151.20 resistance. Nevertheless, rejection by 148.13, followed by break of 143.98 will resume larger fall from 158.86 through 61.8% projection of 158.86 to 146.52 from 151.20 at 143.57.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

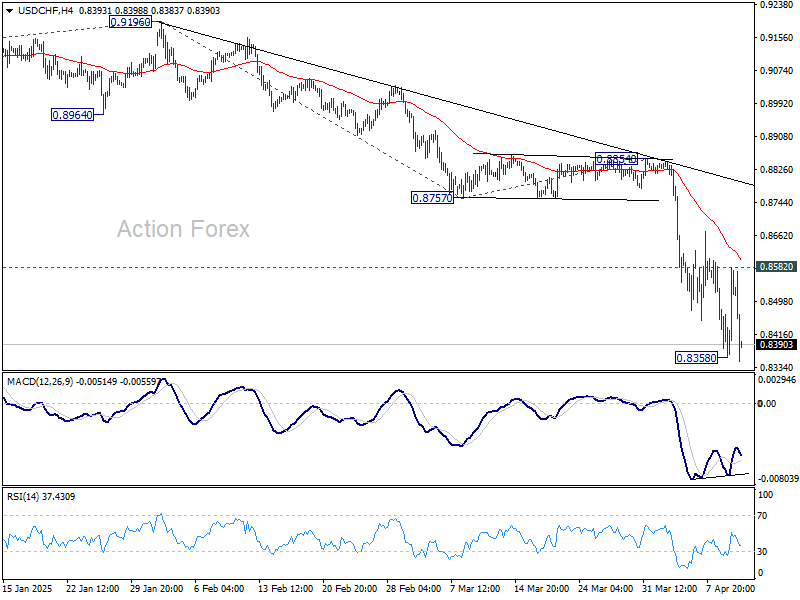

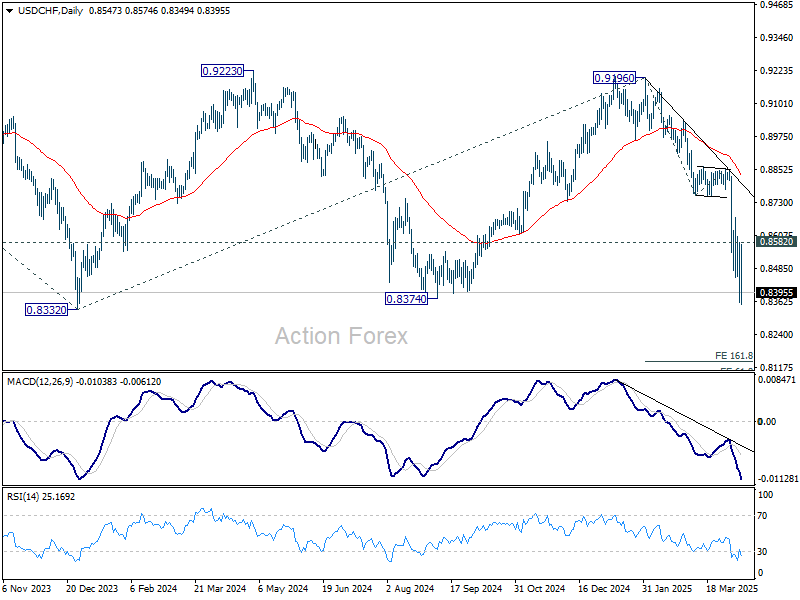

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8431; (P) 0.8508; (R1) 0.8656; More…

Intraday bias in USD/CHF is back on the downside with breach of 0.8358. Fall from 0.9196 should target 161.8% projection of 0.9196 to 0.8757 from 0.8854 at 0.8144. On the upside, above 0.8582 resistance will indicate short term bottoming and turn bias back to the upside for stronger rebound.

In the bigger picture, rejection by 0.9223 key resistance keep medium term outlook bearish. That is, larger fall from 1.0342 (2017 high) is not completed yet. Firm break of 0.8332 (2023 low) will confirm down trend resumption. Next target is 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9196 at 0.8075.

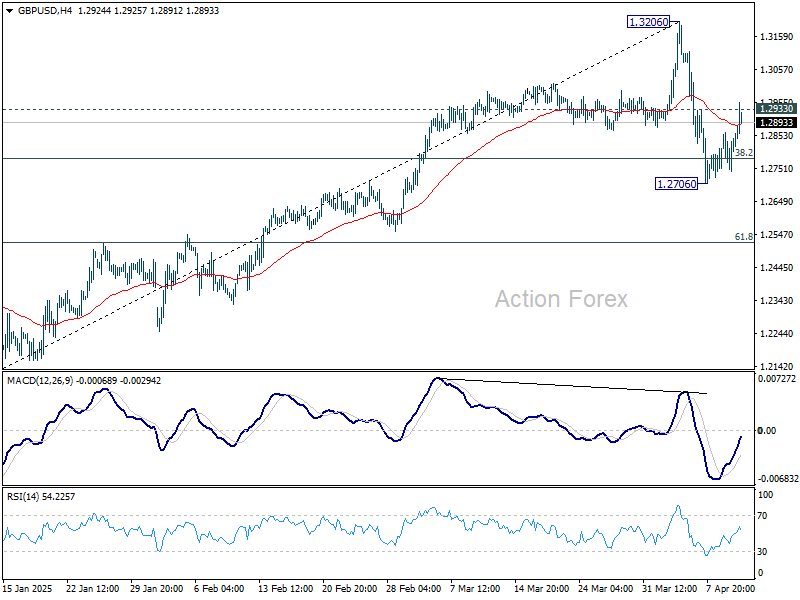

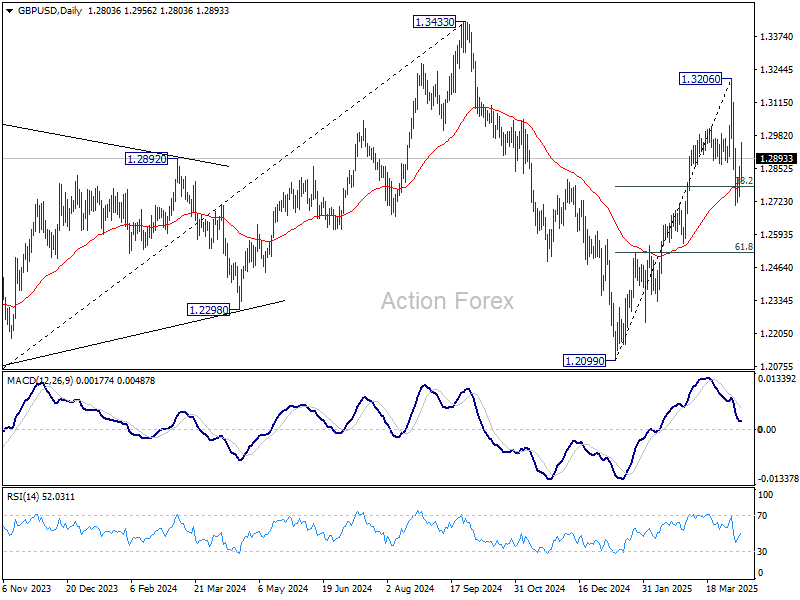

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2757; (P) 1.2811; (R1) 1.2878; More...

Intraday bias in GBP/USD stays neutral for the moment. Risk will stay on the downside with 1.2933 minor resistance intact. Break of 1.2706 will resume the decline from 1.3206 to 61.8% retracement of 1.2099 to 1.3206 at 1.2522. Nevertheless, firm break of 1.2933 will bring stronger rebound back to retest 1.3206 high.

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could be the second leg. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on break of 1.3433 at a later stage.

US: Inflationary Pressures Cool in March, But Tariff Impacts Could Start to Surface as Early as Next Month

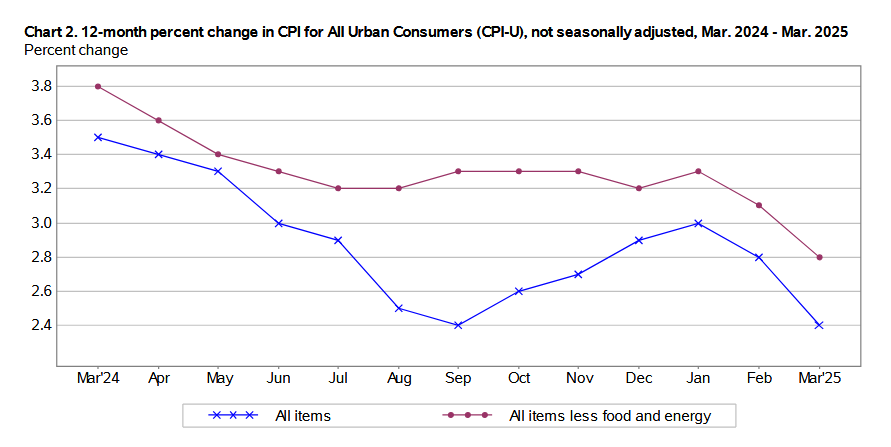

The Consumer Price Index (CPI) declined 0.1% in March, following a gain of 0.2% month-on-month (m/m) in February. On a twelve-month basis, CPI was up 2.4% (from 2.8% in February).

- Energy prices fell 2.4% m/m, thanks to a 6.3% m/m pullback in gasoline prices. Meanwhile, food prices jumped by 0.4% m/m and are up 3.0% on a year-ago basis.

Excluding food and energy, core inflation rose by a meager 0.1% m/m (0.06% unrounded) – well below the consensus forecast of 0.3% m/m – and a tick lower than February's gain. The twelve-month change slipped to 2.8% (from 3.1% in February).

Services prices rose 0.1% m/m, or the softest monthly gain since August 2021. This was due to a pullback in non-housing services (-0.2% m/m), with notable declines in vehicle insurance premiums (-0.8% m/m) and travel related costs (-4.1% m/m). Meanwhile, primary shelter costs rose 0.4% m/m, following a string of softer gains in months prior.

Core goods inflation declined 0.1% m/m, after having trended higher over the prior three months. Used vehicle prices (-0.7% m/m), medical (-1.1% m/m) and recreational goods (-0.3% m/m) all declined in March.

Key Implications

While this morning's softer inflation reading came as welcome news, the reality is the figures are backward-looking. Sweeping tariff announcements in recent weeks mean that inflationary pressure is likely to heat-up over the coming months. But the magnitude of the increase will depend on both the size and duration of the tariffs. Yesterday, President Trump delayed the implementation of all reciprocal tariffs and instead imposed a flat 10% tariff on all trading partners (except for China, where the tariff rate was raised to 125%). Sectoral tariffs, including those applied to the steel/aluminum and foreign made autos and parts, remain unchanged at 25%.

To say uncertainty is elevated at the moment would be an understatement. We see economic growth stalling out through the front half of this year, which will be accompanied by a mild increase in the unemployment rate. But with core measures of inflation likely to push higher as early as Q2, the Fed will quickly find itself stuck between a rock and hard place. Fed futures have nearly fully priced the next cut to come in June, but the recent pivot in tone from some Fed officials suggests policymakers' bias has shifted to holding rates higher for longer.

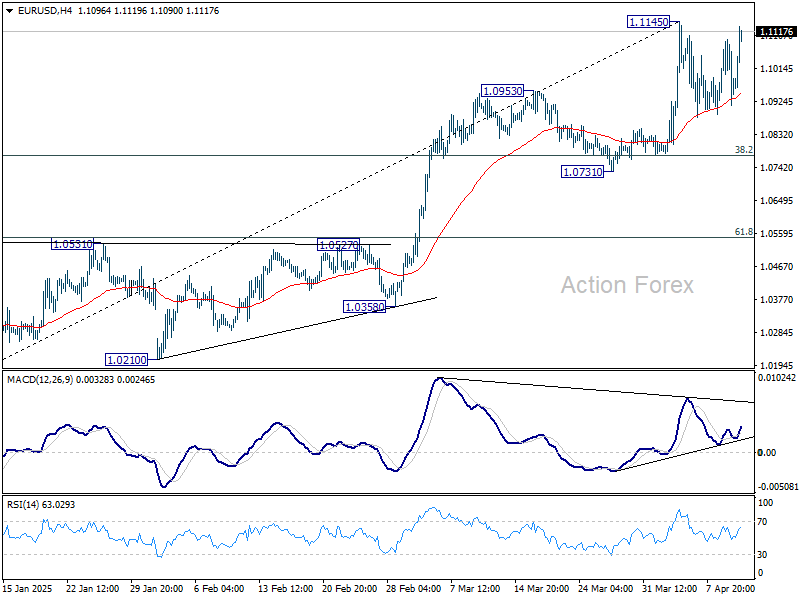

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0876; (P) 1.0986; (R1) 1.1057; More...

Intraday bias in EUR/USD remains neutral first, but focus is immediately on 1.1145 resistance with today's rebound. Firm break there will resume whole rally from 1.0176. Next target is 1.1213/74 key resistance zone next. In case of another retreat, downside should be contained by 38.2% retracement of 1.0176 to 1.1145 at 1.0775 to complete the near term consolidation.

In the bigger picture, fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through the multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0731 support holds.

Dollar Falls as Disinflation Accelerates, EU Holds Fire on Tariff Retaliation

Dollar faced renewed selling pressure in early US session, as markets digested softer-than-expected inflation data. The latest CPI report confirmed that disinflation is regaining traction, with both headline and core inflation easing more than expected in March. This strengthens the case for Fed to resume its rate cut cycle in the coming months.

A May rate cut remains unlikely — with Fed fund futures currently pricing in an 84% chance of a hold. Markets are still more confident that a move will come by June, with odds now standing around 78%. If the disinflation trend persists, that expectation could soon become consensus.

On the trade front, the mood is notably less tense today. The European Union announced a 90-day suspension of its first wave of retaliatory tariffs, originally planned in response to the US’s 25% steel and aluminum duties. This follows US decision to pause the broad reciprocal tariff for 90 days.

European Commission President Ursula von der Leyen emphasized, "We want to give negotiations a chance". But she also made clear that the EU remains ready to act if talks fail. Preparatory work for broader countermeasures remains underway, with all options said to be "on the table."

Despite this temporary de-escalation, overall market sentiment remains shaky. US futures are pointing to a weaker open after yesterday’s massive relief rally, suggesting that investors are still wary of the underlying risks. In contrast, European markets are tracking Asia higher, but overall confidence is fragile.

In the currency markets, Dollar is currently the worst performer of the week, followed by Sterling and Loonie. Swiss Franc continues to shine as a safe haven, with Aussie and Kiwi showing resilience as well. Meanwhile, Yen and Euro are positioning in the middle.

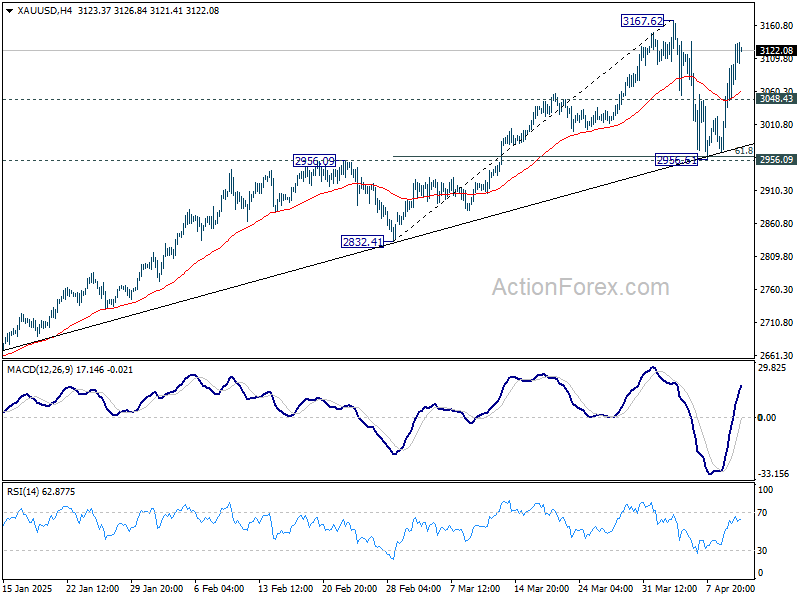

Technically, Gold's rebound from 2956.61 extended higher today. The strong support from 2956.09, as well as rising trend line, keeps Gold's up trend intact. Nevertheless, corrective pattern from 3167.62 might still be incomplete. Break of 3048.43 support will start another down leg. Though, firm break of 3167.62 will confirm up trend resumption.

In Europe, at the time of writing, FTSE is up 3.84%. DAX is up 4.83%. CAC is up 4.49%. UK 10-year yield is down -0.073 at 4.742. Germany 10-year yield is up 0.049 at 2.640. Earlier in Asia, Nikkei rose 9.13%. Hong Kong HSI rose 2.06%. China Shanghai SSE rose 1.16%. Singapore Strait Times rose 5.43%. Japan 10-year JGB yield rose 0.095 to 1.377.

US CPI surprise: Both headline and core inflation cools sharply in March

US inflation came in much softer than expected in March, with headline CPI falling -0.1% mom, surprising markets that had forecast a 0.2% mom increase. Core CPI, which excludes food and energy, also underwhelmed with just a 0.1% mom gain, well below the anticipated 0.3% mom. The pullback was led by a -2.4% mom drop in energy prices, while food costs continued to climb, rising 0.4% mom.

On an annual basis, the CPI decelerated from 2.8% yoy to 2.4% yoy, lower than the expected 2.5% yoy. Core CPI also slowed to 2.8% yoy, down from 3.1% yoy, and marked the smallest 12-month increase since March 2021. The sharp drop in energy prices, down -3.3% yoy, played a significant role, although food inflation remained sticky at 3.0% yoy.

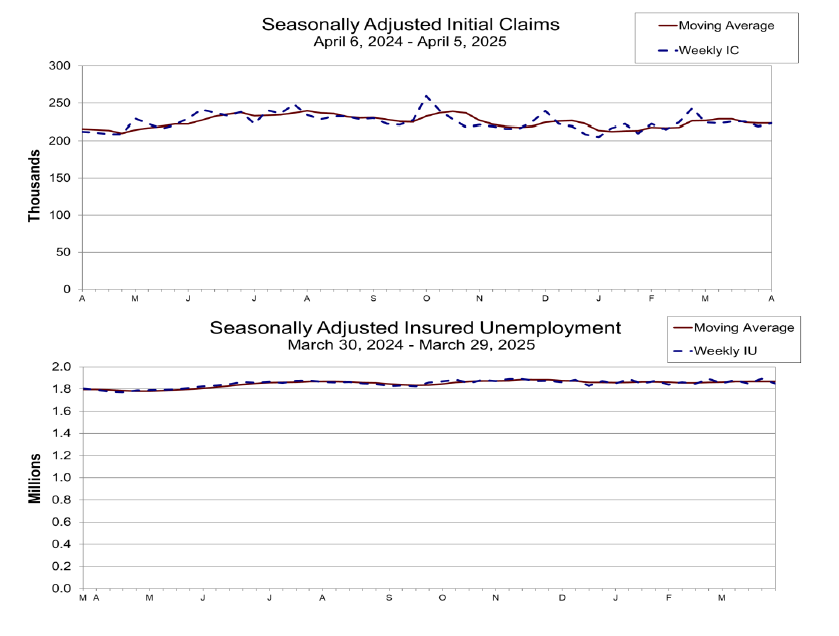

US initial jobless claims rise to 223k, vs exp 222k

US initial jobless claims rose 4k to 223k in the week ending April 5, slightly above expectation of 222k. Four-week moving average of initial claims was unchanged at 223k.

Continuing claims fell -43k to 1850k in the week ending March 29. Four-week moving average of continuing claims fell -250 to 1868k.

ECB’s Villeroy: Thank God we created Euro, as tariff turmoil undermines Dollar

French ECB Governing Council member François Villeroy de Galhau emphasized today that while the US has long championed the global centrality of the Dollar, recent policy moves on tariffs are beginning to erode international confidence in the greenback.

Speaking on France Inter radio, Villeroy said the Trump administration’s approach is “very incoherent,” and suggested that its recent actions “play against the confidence” typically held in Dollar.

He contrasted this with the Euro, praising Europe’s foresight in establishing its own independent monetary system 25 years ago. “Thank God that Europe… created the Euro,” he noted, adding that the bloc now enjoys “monetary autonomy” that allows ECB to manage interest rates in a way that diverges from US policy, something that was not possible in the past.

RBA’s Bullock: Too early to call rate path amid tariff-driven uncertainty

RBA Governor Michele Bullock stated today that it is “too early” to judge how escalating global trade war will shape the path of Australian interest rates. "it’s too early for us to determine what the path will be for interest rates," she added.

Bullock noted that “a period of uncertainty and adjustment” is inevitable as countries react to Washington’s trade moves. RBA plans to stay patient while assessing how these global shocks might affect both supply and demand dynamics. “It will take some time to see how all of this plays out,” she said.

Japan's PPI accelerates to 4.2% while import costs ease

Japan’s PPI rose 4.2% yoy in March, a slight acceleration from February’s 4.1% yoy and topping expectations of 3.9% yoy rise. The increase was broad-based, with notable gains in food prices, which rose 3.1% yoy, and energy costs, with petroleum and coal prices surging by 8.6% yoy.

Despite the uptick in domestic producer prices, import costs in Yen terms fell -2.2% yoy in March, extending the -0.9% decline in February. Export prices, however, rose a modest 0.3% yoy, slowing sharply from February’s 1.7% yoy growth.

China's CPI falls -0.1% yoy in March, PPI highlights persistent deflationary pressures

China’s consumer inflation remained in negative territory for a second straight month in March, with CPI falling -0.1% yoy, missing expectations of 0.1% yoy increase. While the decline was narrower than February’s -0.7% yoy, it still reflects subdued demand pressures across the economy.

Food prices was a drag, down -1.4% yoy, while service prices provided only modest support, rising 0.3% yoy. Core CPI, which excludes volatile food and energy prices, edged up to 0.5% yoy from 0.3% previously, offering a slight glimmer of resilience.

However, with headline inflation still hovering around zero and signs of consumer caution persisting, the broader disinflation trend appears entrenched.

On a monthly basis, CPI dropped -0.4% mom, following February’s -0.2% mom decline, suggesting continued weakness in household spending momentum.

Meanwhile, producer prices extended their decline for a 30th straight month, with PPI dropping -2.5% yoy, deeper than the expected -2.3%.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0876; (P) 1.0986; (R1) 1.1057; More...

Intraday bias in EUR/USD remains neutral first, but focus is immediately on 1.1145 resistance with today's rebound. Firm break there will resume whole rally from 1.0176. Next target is 1.1213/74 key resistance zone next. In case of another retreat, downside should be contained by 38.2% retracement of 1.0176 to 1.1145 at 1.0775 to complete the near term consolidation.

In the bigger picture, fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through the multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0731 support holds.

US initial jobless claims rise to 223k, vs exp 222k

US initial jobless claims rose 4k to 223k in the week ending April 5, slightly above expectation of 222k. Four-week moving average of initial claims was unchanged at 223k.

Continuing claims fell -43k to 1850k in the week ending March 29. Four-week moving average of continuing claims fell -250 to 1868k.

US CPI surprise: Both headline and core inflation cools sharply in March

US inflation came in much softer than expected in March, with headline CPI falling -0.1% mom, surprising markets that had forecast a 0.2% mom increase. Core CPI, which excludes food and energy, also underwhelmed with just a 0.1% mom gain, well below the anticipated 0.3% mom. The pullback was led by a -2.4% mom drop in energy prices, while food costs continued to climb, rising 0.4% mom.

On an annual basis, the CPI decelerated from 2.8% yoy to 2.4% yoy, lower than the expected 2.5% yoy. Core CPI also slowed to 2.8% yoy, down from 3.1% yoy, and marked the smallest 12-month increase since March 2021. The sharp drop in energy prices, down -3.3% yoy, played a significant role, although food inflation remained sticky at 3.0% yoy.