Sample Category Title

Fed’s Collins: Tariff-driven price pressures may delay further policy normalization

Boston Fed President Susan Collins said in a speech overnight that keep interest rate at current level is "appropriate for the time being" due to the "highly uncertain environment."

Collins acknowledged that "renewed price pressures" from tariffs could "delay further normalization of policy".

"Confidence is needed that the tariffs are not destabilizing inflation expectations," she emphasized.

She added that any "preemptive action" to support growth would require a “compelling” signal that economic activity is deteriorating more than expected.

Although she expects inflation to gradually return to the 2% target, she acknowledged that core inflation may rise “well above” 3% in the near term due to higher import costs. In her view, the Fed must remain vigilant to ensure these pressures do not become entrenched.

Cliff Notes: A Late Change of Heart

Key insights from the week that was.

Starting in Australia, April’s Westpac-MI Consumer Sentiment Survey – which was in the field last week – provided a first-look into households’ reaction to President Trump’s tariff turmoil. Sentiment was only slightly lower over the first half the week, before moving sharply lower after the ‘Liberation Day’ announcements, leaving the headline index down 6% at 90.1. There were significant declines across the sub-indexes tracking ‘family finances vs. a year ago’ (–8.5%), but also the year-ahead outlook for family finances (–6.2%) and the economy (–5.7%). Attitudes toward consumption, which were already precariously placed owing to the elevated cost-of-living, fell victim to this emerging uncertainty, with the ‘time to buy a major household item’ sub-index falling –7.3% to be 34% below its long-run average. Although households were more uncertain about the prospect of interest rate relief, markets have since come to our view and have fully priced in a 25bp rate cut from the RBA in May.

The subsequent rapid deterioration in trade relations between the US and China and 90-day reprieve for other nations makes for a completely different picture, however (see below for further detail). The current tariff structure, should it persist, is not expected to have a significant impact on the Australian economy, principally thanks to China’s ability to stimulate to offset the shock. Though, there is a risk that the extreme volatility of recent weeks may see consumer and business confidence remain on the backfoot for an extended period. Still, if the market volatility recedes, domestic factors are likely to once again become the focus, specifically the health of the labour market, ongoing moderation in inflation, and the prospective recovery in consumer spending.

In the US and globally, the Trump administration’s trade agenda whiplashed markets this week. Following last week’s reciprocal tariff announcement, global bourses opened sharply lower for fear of where US and global growth could end up. Then, after holding to the announced tariffs resolutely, and doubling down on China, President Trump suddenly announced a 90-day reprieve for all non-retaliating countries. Imports from these economies will now only receive a 10% tariff on entry to the US, at least for the time being. The tariffs on Mexico and Canada will remain in place, however; while, at the same time, President Trump doubled down again on China, increasing their reciprocal tariff rate from 104% to 125%. Note this rate is reportedly in addition to the initial 20% tariff, so Chinese imports now face a combined tariff rate of 145% on entry to the US. Negotiations are set to get underway between the US and numerous nations next week. It is not clear what cost President Trump will demand for US tariff relief, but Treasury Secretary Bessent has alluded to a request for other nations to also tariff China. If they do so, then the current bilateral conflict risks becoming a much broader threat to global growth, to the detriment of China but also every other country involved.

The minutes of the FOMC's March meeting highlight why President Trump may have had this change of heart. Evident in the discussions amongst members is that inflation remains the key consideration for monetary policy decisions. “Several participants noted that their contacts were already reporting increases in costs, possibly in anticipation of rising tariffs, or that their contacts had indicated willingness to pass on to consumers higher input costs that would arise from potential tariff increases." A couple of members also raised concerns over the ability of the FOMC to assess the persistence of inflation in real time. There was also a specific reference to "many firms… paus[ing] their capital spending plans", an adverse development for both growth and inflation. These views do not mean the FOMC are myopic in their focus. But simply that, as highlighted by Chair Powell last Friday, inflation is expected to remain further from target than employment, and policy needs to be set accordingly. The “Committee may face difficult tradeoffs if inflation prove[s] to be more persistent while the outlook for growth and employment weaken[s]”.

Coming back to our region, the Reserve Bank of New Zealand cut rates by 25bps to 3.5% at its April meeting, in line with market expectations. The statement noted that the "adaption of global supply chains to increased trade barriers will take longer to work through. It was noted [also] that monetary policy cannot offset the long-term negative effects of higher barriers to international trade". Looking ahead, we anticipate a further 25bp cut in May and risks are likely to remain skewed to the downside for some time thereafter, requiring careful assessment of the incoming data.

Gold Wave Analysis

Gold: ⬆️ Buy

- Gold broke key resistance level 3150.00

- Likely to rise to resistance level 3200.00

Gold today broke above the key resistance level 3150.00 (which stopped the previous impulse wave I at the start of April, as can be seen below).

The breakout of the resistance level 3150.00 accelerated the active intermediate impulse wave (3) from last November.

Given the overriding daily uptrend, Gold can be expected to rise to the next resistance level 3200.00, which is the forecast price for the completion of the active impulse wave (3).

USDCHF Wave Analysis

USDCHF: ⬇️ Sell

- USDCHF broke support zone

- Likely to fall to support level 0.8200

USDCHF currency pair recently broke the support zone between the key support level 0.8400 (which reversed the price multiple times in August and September) and the support trendline of the daily down channel from February.

The breakout of this support zone accelerated the active intermediate impulse wave (3).

USDCHF currency pair can be expected to fall to the next support level 0.8200, which is the target price for the completion of the active impulse wave (3).

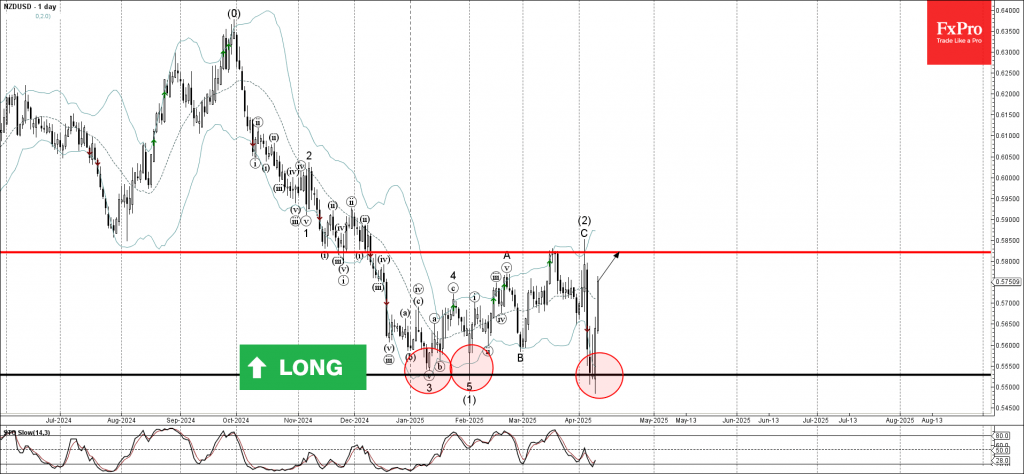

NZDUSD Wave Analysis

NZDUSD: ⬆️ Buy

- NZDUSD reversed from support zone

- Likely to rise to resistance level 0.5820

NZDUSD currency pair recently reversed from the support zone between the key support level 0.5530 (which has been reversing the price from January) and the lower daily Bollinger Band.

The upward reversal from the support level 0.5530 created the daily Japanese candlesticks reversal pattern Morning Star Doji.

Given the strongly bearish US dollar sentiment, NZDUSD currency pair can be expected to rise to the next resistance level 0.5820.

Fed’s Schmid still squarely focused on inflation outlook

Kansas City Fed President Jeff Schmid delivered a hawkish message today, emphasizing that his primary focus remains “squarely” on the inflation outlook.

He flagged a notable increase in upside inflation risks alongside rising downside risks to employment and growth, painting a challenging picture for policymakers.

However, he emphasized, "With renewed price pressures likely, I am not willing to take any chances when it comes to maintaining the Fed's credibility on inflation."

Addressing the inflationary impact of tariffs, Schmid acknowledged that while economic theory suggests a one-off price shock rather than sustained inflation, he’s not inclined to rely too heavily on that assumption under current conditions.

“I would be hesitant to take too much solace from theory in this environment,” he noted, referencing recent episodes of persistently high inflation that caught many off guard.

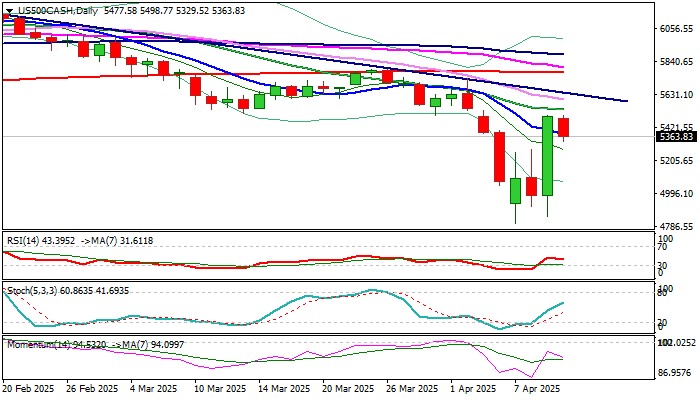

S&P Rose Sharply on Tariff Policy U-turn But More Work at the Upside Still Needed to Neutralize Downside Risk

S&P500 edged lower on Thursday after rallying 10.2% previous day (the biggest daily gains in over a decade).

Unexpected decision of President Trump to put heavy tariffs on a number of countries on hold for 90 days, revived optimism and lifted stock markets.

Although fresh rally retraced the largest part of heavy losses sparked by introduction of tariffs last week, markets remain cautious as the US tariffs on imports from China were not affected by the latest decision but were increased to 125%.

This raises worries of strong escalation of trade conflict between two world’s largest economies, which could have a domino effect on most countries.

Further development of the situation will be closely watched with positive scenario seeing a trade deal between two countries that would provide further relief and boost stock prices, while escalation would further sour the sentiment and add fresh pressure on prices.

Daily studies have slightly improved following Wednesday’s strong rally, but overall picture remains predominantly bearish and warn that downside risk still exists.

In ideal scenario, corrective dips from Wednesday’s peak should be shallow and contained above $5230 (Fibo 38.2% of $4801/$5495) to mark healthy correction and keep near term bias with bulls, though sustained break above $5500 zone, will be still needed to validate reversal signal.

Caution on dip and close below $5200/$5150 zone which could sideline fresh bulls and revive downside risk.

Res: 5457; 5496; 5532; 5636

Sup: 5330; 5267; 5230; 5200

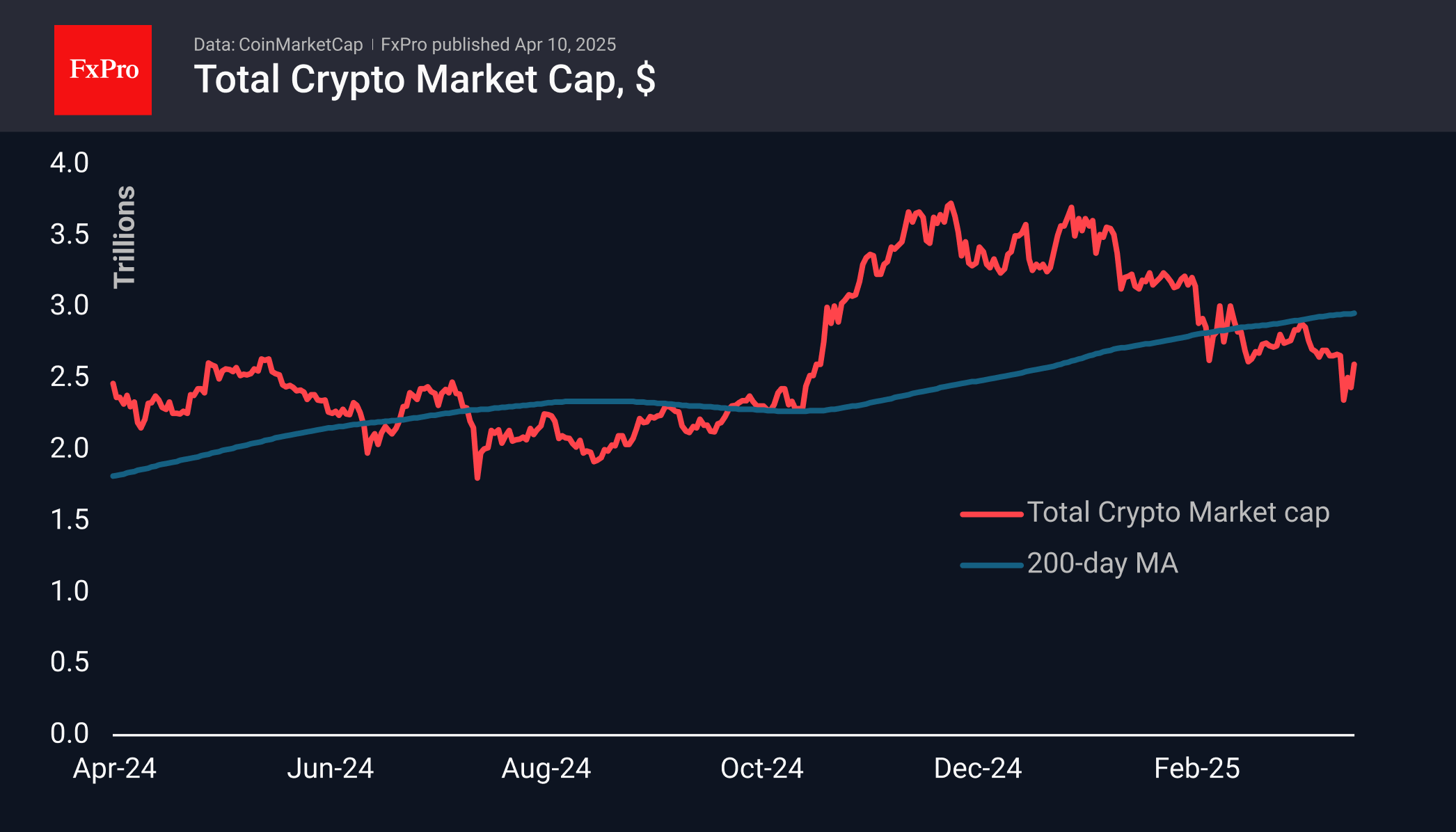

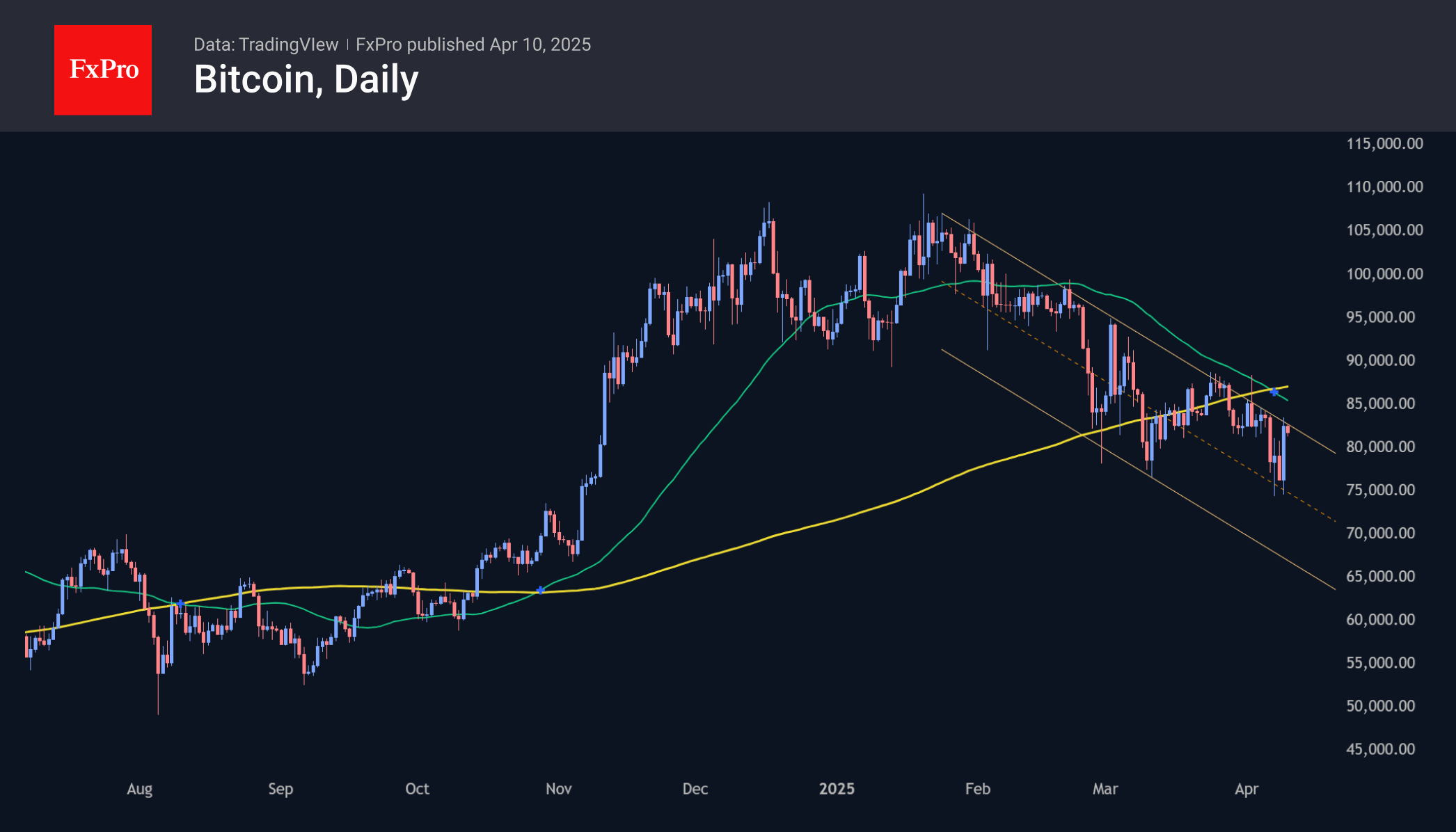

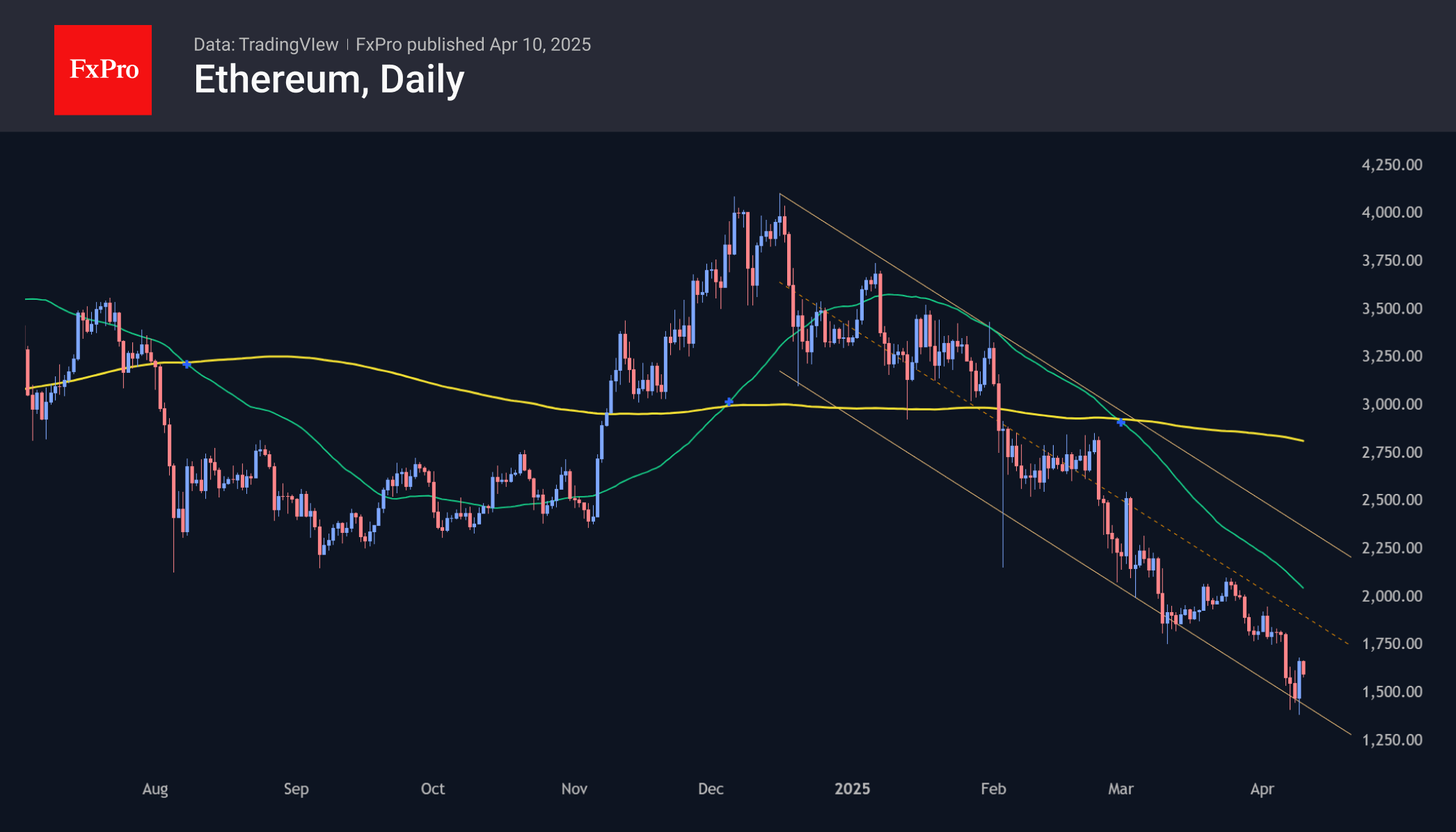

Crypto Market Stabilises After Rebound

Market Picture

The cryptocurrency market cap has stabilised near a key level since the start of the week and went up steadily on the back of tariff news following the rise in equities. However, the spurt was half that of equities. Total capitalisation reached $2.60 trillion, pushing back from support near $2.3 trillion, the level from which the rally began late last year. So far, the rise has been met with caution as capitalisation has yet to cross its 200-day moving average, which is pointing upwards and approaching $2.96 trillion.

Bitcoin held firmly below $75K support at the beginning of the week. The recent growth spurt has lifted the price above $80K, which can be considered a comfort zone. However, the first cryptocurrency approached the upper boundary of the downtrend, and the main test of the two-month trend is just beginning.

Ethereum is showing weakness relative to the market, dipping below $1400 at the lows of the week and bouncing back later to $1600. This bounced off the lower boundary of the descending corridor, and the upper boundary was near $1900. This level will be an important point to watch for a possible upside development.

News Background

Ripple announced the purchase of the Hidden Road platform for $1.25bn. The deal will strengthen the XRP ecosystem, including the RLUSD stablecoin, the XRPL blockchain, and the Ripple Payments service.

Cardano founder Charles Hoskinson said the crypto industry needed a ‘cooperative balance’ to compete with centralised tech giants in the race for Web3. He noted that DeFi’s key challenge remains the ‘closed economy.’

According to Artemis Terminal, the crypto industry has lost about 40% of active Web3 developers in a year—an important marker of the ecosystem’s poor health.

British Pound Surges Higher, UK GDP Next

The British pound has posted sharp gains on Thursday. In the North American session, GBP/USD is trading at 1.2914, up 0.78% on the day.

Markets recover as Trump suspends tariffs

Global equity markets are showing sharp volatility which is also apparent in the currency market. The pound posted sharp losses after the latest round of US tariffs took effect, but has surged higher following US President Trump's surprise annoucement that he would reduce all country-specific tariffs to 10% except for China, for 90 days. The dramatic development sent stock markets soaring on Wednesday.

Fed minutes: concern over tariffs

Overshadowed by the wild swings in the financial market, the Fed released the minutes of the March rate meeting on Wednesday. Fed officials are clearly worried about US trade policy as the minutes mentioned tariffs 18 times.

Members viewed risks to inflation to be tilted to the upside and expected inflation to rise this year due to the effect of higher tariffs. Some members warned of "difficult tradeoffs" if inflation remained persistent and growth and employment weakened.

Will the Federal Reserve accelerate its easing cycle due to the tariff turmoil? The markets don't think so, even though there is increasing concern about weaker US growth. If the US goes ahead with its stiff tariff policy, inflation would likely rise in the US, complicating the Fed's plans to gradually reduce rates during the year. The markets have priced in a rate hike in May at just 17%, according CME FedWatch.

The UK economy is stuggling and the GDP report isn't likely to show much improvement. The market estimate is 0.1% m/m for February growth after -0.1% in January. For the three months to February, the market estimate is 0.4%, following 0.2% in the previous release.

GBP/USD Technical

- GBP/USD has pushed above resistance at 1.2878. The next resistance line is 1.2932

- There is support at 1.2811 and 1.2757