Sample Category Title

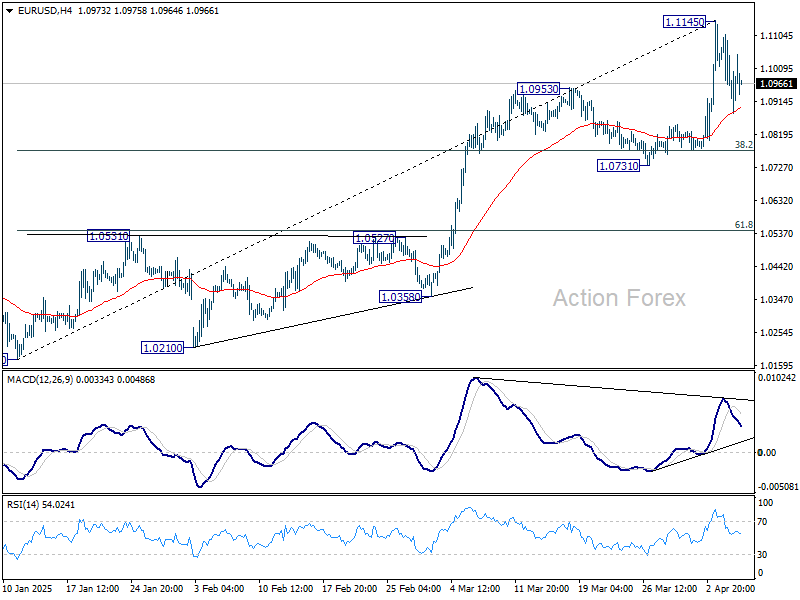

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0889; (P) 1.0999; (R1) 1.1072; More...

EUR/USD is extending consolidations below 1.1145 and intraday bias remains neutral. Downside of retreat should be contained by 38.2% retracement of 1.0176 to 1.1145 at 1.0775 to bring rebound. On the upside, above 1.1145 will resume the rally from 1.0176 to 1.1213/74 key resistance zone next.

In the bigger picture, fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through the multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0731 support holds.

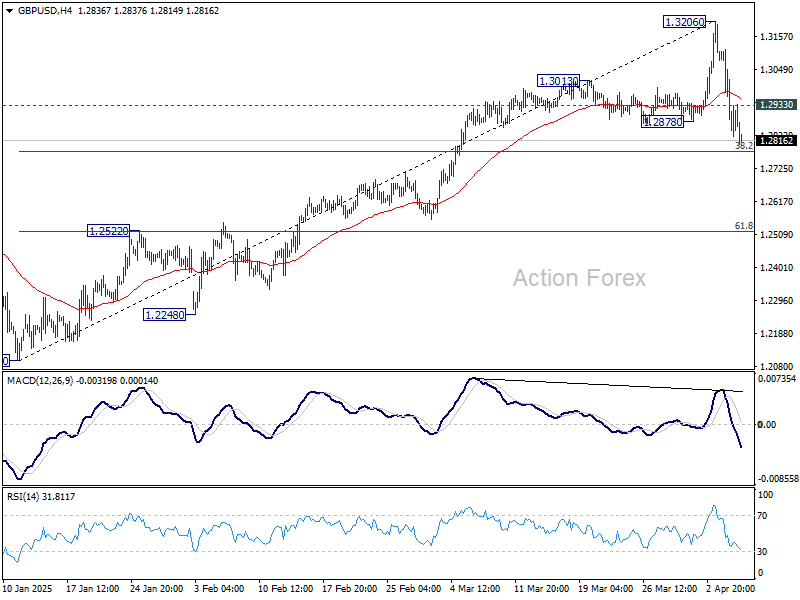

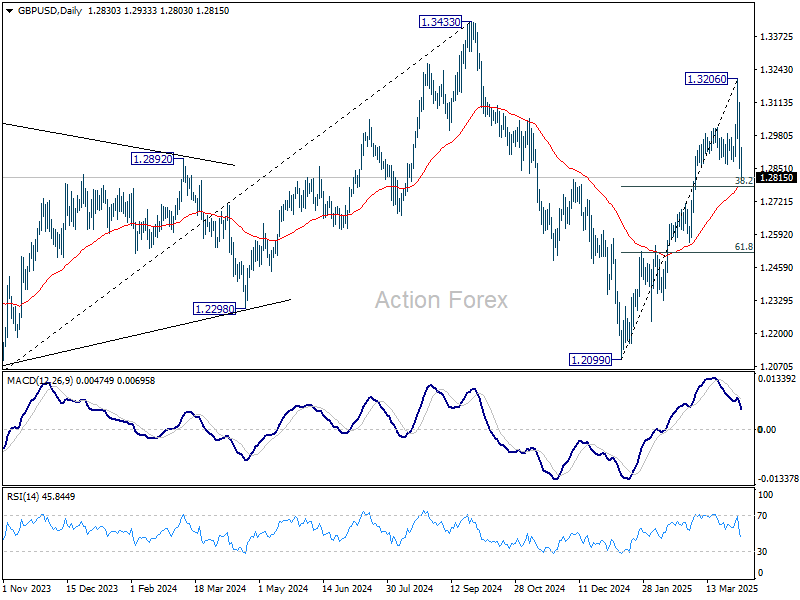

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2789; (P) 1.2959; (R1) 1.3066; More...

GBP/USD edges lower today and intraday bias stays on the downside. Fall from 1.3206 short term top should extend to 38.2% retracement of 1.2099 to 1.3206 at 1.2783. Decisive break there will target 61.8% retracement at 1.2522. On the upside, above 1.2933 minor resistance will turn intraday bias neutral first.

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could be the second leg. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on break of 1.3433 at a later stage.

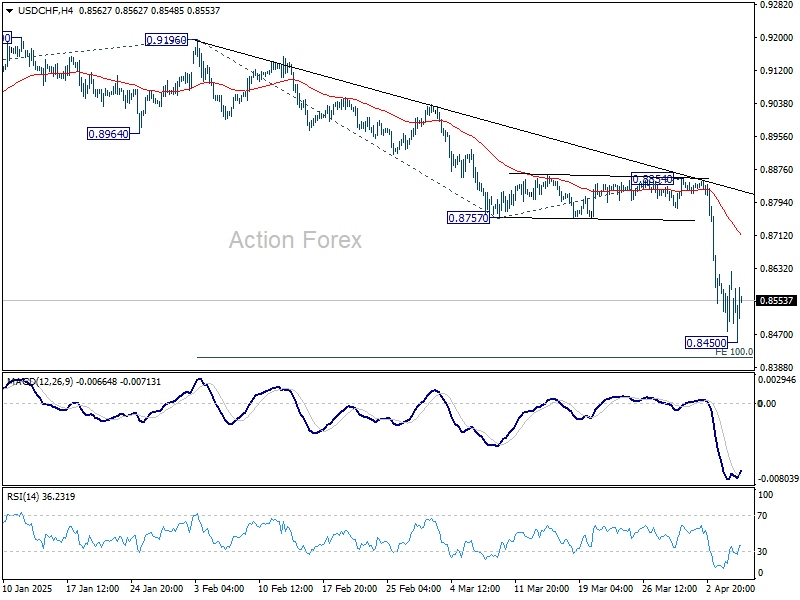

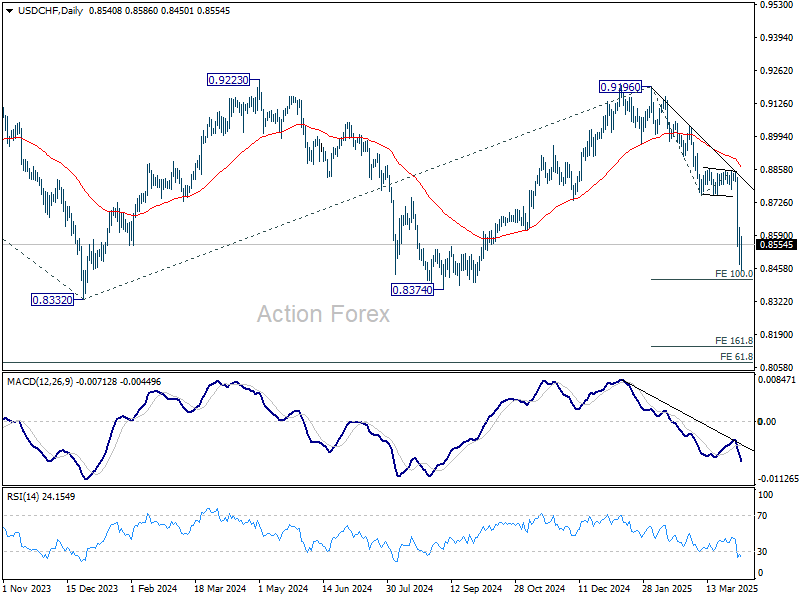

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8515; (P) 0.8570; (R1) 0.8663; More…

USD/CHF edged lower to 0.8450 but quickly recovered. Intraday bias stays neutral and more consolidations could be seen. Upside of recovery should be limited below 0.8757 support turned resistance. On the downside, below 0.8450 will resume the fall from 0.9196 and target 100% projection of 0.9196 to 0.8757 from 0.8854 at 0.8415.

In the bigger picture, rejection by 0.9223 key resistance keep medium term outlook bearish. That is, larger fall from 1.0342 (2017 high) is not completed yet. Firm break of 0.8332 (2023 low) will confirm down trend resumption. Next target is 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9196 at 0.8075.

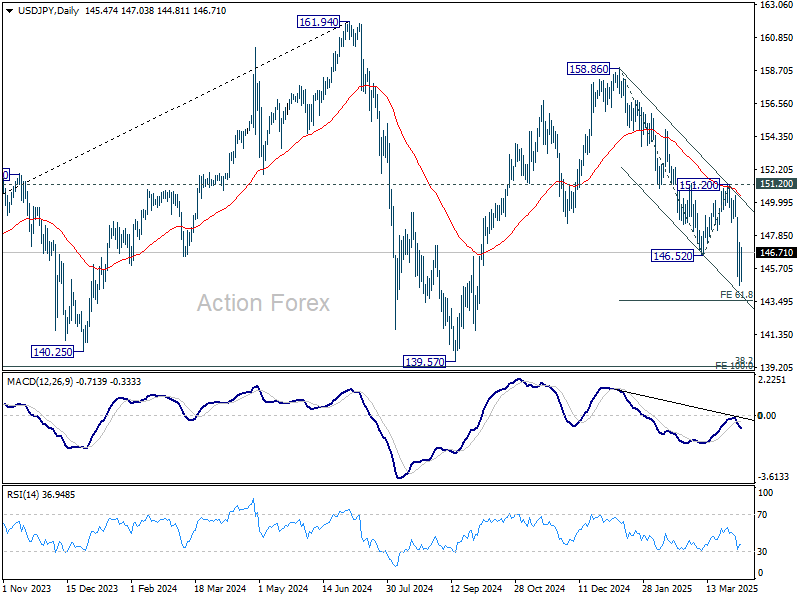

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 145.24; (P) 146.34; (R1) 148.12; More...

USD/JPY is extending consolidations above 144.54 temporary low and intraday bias remains neutral. Upside of recovery should be limited below 151.28 resistance. On the downside, below 144.54 will resume the fall from 158.86 and target 61.8% projection of 158.86 to 146.52 from 151.20 at 143.57. Break there will target 139.57 low.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

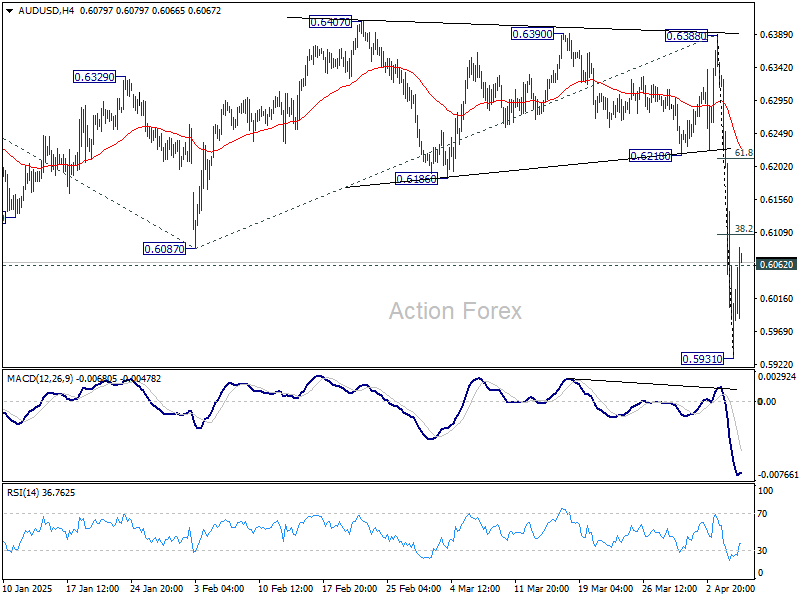

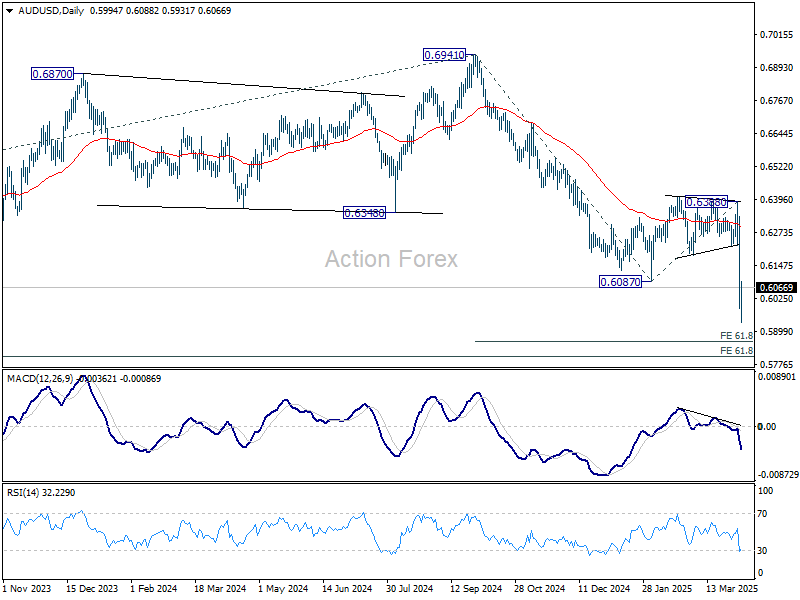

AUD/USD Mid-Day Report

Daily Pivots: (S1) 0.5907; (P) 0.6120; (R1) 0.6252; More...

A temporary low should be formed at 0.5931 with today's recovery. Intraday bias in AUD/USD is turned neutral first. Stronger rebound cannot be ruled out. But upside should be limited below 0.6210 support turned resistance to bring another fall. On the downside, break of 0.5931 will resume larger decline to 61.8% projection of 0.6941 to 0.6087 from 0.6388 at 0.5860.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 0.6388 resistance holds.

Gold Technical Outlook: On the Cusp of Transforming into a Potential Multi-Week Corrective Decline

- Gold (XAU/USD) has failed to have a positive follow-through in April after March’s stellar monthly gain of 9.3% despite a global risk-off environment seen in the past two weeks.

- The stagflation environment arising from the latest US reciprocal trade tariffs may have already been priced into Gold (XAU/USD).

- Technical factors are taking the driver's seat in the short to medium-term over fundamentals as earlier bullish positioning may see adjustments and unwinding.

- Watch the US$2,936 potential downside trigger level on Gold (XAU/USD).

This is a follow-up analysis of our prior report “Gold: Stagflation fears are supporting fresh new all-time highs” published on 5 February 2025.

Since our last publication, the price actions of Gold (XAU/USD) have staged the expected up move and rallied by 11%. The bullish impulsive up move sequence surpassed the US$3,084 medium-term resistance highlighted in our prior analysis on 28 March and printed a recent fresh all-time intraday high of US$3,168 on 3 April.

However, Gold (XAU/USD) seems to be facing the typical “buy the rumour, sell the news” syndrome. After a recent strong rally in March, where it recorded a monthly gain of 9.3% on the backdrop of stagflation fears, it has failed to have a positive follow-through so far in April.

Hence, the increased probability of the stagflation environment arising from the latest US reciprocal trade tariffs may have already been priced in by the movements of gold during the up move in March.

Fundamentals are still supporting the continuation of Gold’s major uptrend phase

Fig 2: US 10-YR Treasury real yield medium-term & major trends as of 7 Apr 2025 (Source: TradingView)

The ongoing major uptrend phase of Gold (XAU/USD) has been in place since early October 2023 and has an indirect correlation with the longer-term US 10-year Treasury real yield, where its price actions have been evolving within a major descending range channel over the same period (see Fig 1).

Gold (XAU/USD) is considered a zero-yielding asset as it does not generate fixed interest income. Thus, if sovereign bond yields go down such as the yields on US Treasuries, the opportunity costs for holding gold will be lower, in turn, driving up demand for gold, which eventually may see an increase in the price of gold.

The 10-year US Treasury real yield has dropped by 69 basis points (bps) since the 15 January high of 2.37% to print a recent low of 1.68% on last Friday, 4 April. It may face further downside pressure as it continues to trade below its key 200-day moving average, with the risk of retesting the 17 September 2024 medium-term swing low of 1.48% if the 1.66% level is broken down to the downside.

However, this fundamental catalyst is not having a positive impact on the price actions of Gold (XAU/USD), while technical factors are likely to be in the driver's seat at this juncture. Thus, the prices of Gold (XAU/USD) now may see some form of bullish positioning adjustments and unwinding.

Bearish MACD trend condition

Fig 2: Gold (XAU/USD) medium-term & major trends as of 7 Apr 2025 (Source: TradingView)

The daily MACD trend indicator of Gold (XAU/USD) flashed out a bearish crossover on last Friday, 4 April, and an earlier bearish divergence condition on Thursday, 3 April.

These observations suggest that there may be a change of direction for its medium-term uptrend phase from the 30 December 2024 low towards a potential multi-week corrective decline sequence.

A similar bearish condition on the daily MACD indicator has been flashed in the past on 1 November 2024, where the price actions of Gold (XAU/USD) shaped a multi-week decline of 7.60% before a swing low was formed on 14 November 2024 (see Fig 2).

Watch the US$3,149/3,168 key medium-term pivotal resistance, and a break below the intermediate support of US$2,936 (also the 50-day moving average) may trigger a potential multi-week corrective decline to expose the medium-term support zone of US2,834/2,787.

On the other hand, a clearance above US$3,168 invalidates the bearish scenario for the continuation of the bullish impulsive up move sequence for the next medium-term resistances to come in at US$3,250, and US$3,335/3,350.

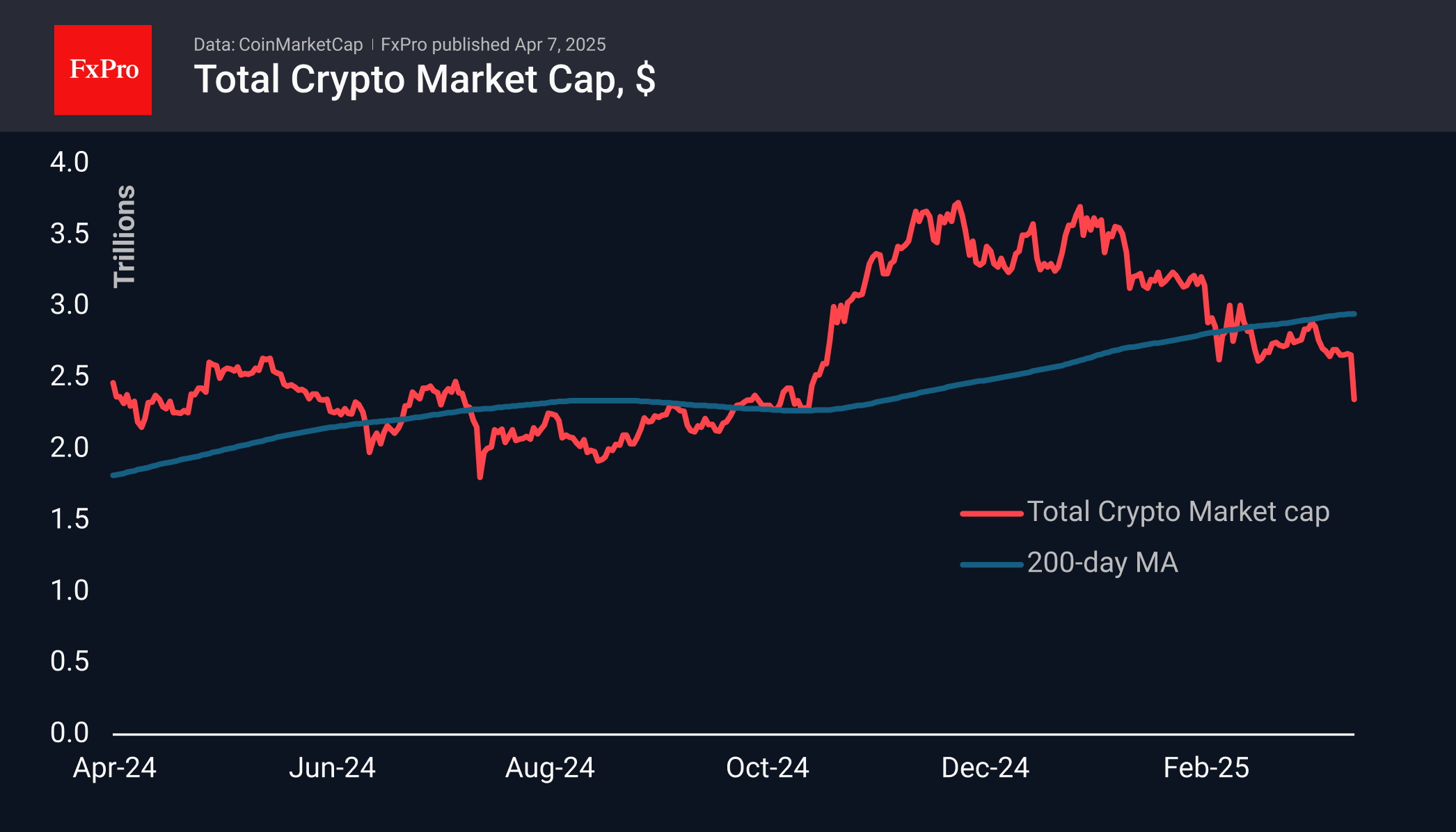

Crypto Market Slides Down

Market Picture

The crypto market capitalisation took a corkscrew turn over the weekend, falling to $2.35 trillion, a low since mid-2024 and a loss of 11.5% in 24 hours. The market has pulled back to levels seen in early November last year when Trump’s victory triggered a break of resistance. At these levels, the market looks emotionally oversold, which increases the chances of a bounce. However, for a rebound to be a reversal, fundamental changes are required, and these are not yet in place.

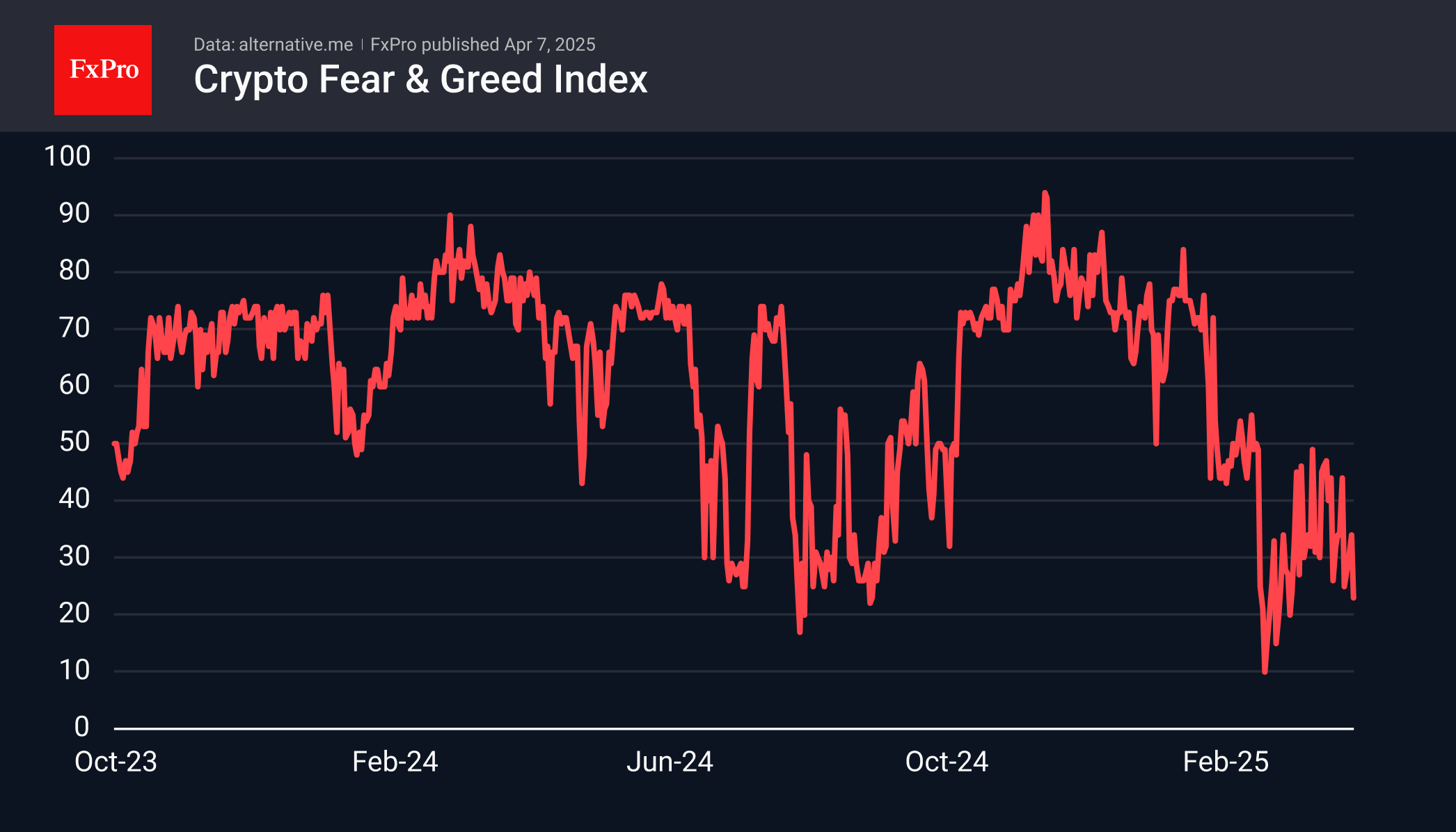

Crypto market sentiment has returned to the extreme fear zone of 23, which is significantly higher than what we see in equities. Meanwhile, nominal prices are updating multi-month lows. This does not mean that cryptocurrency investors are more confident about the future. Rather, it signals that the sell-off here is more organised, making it more dangerous.

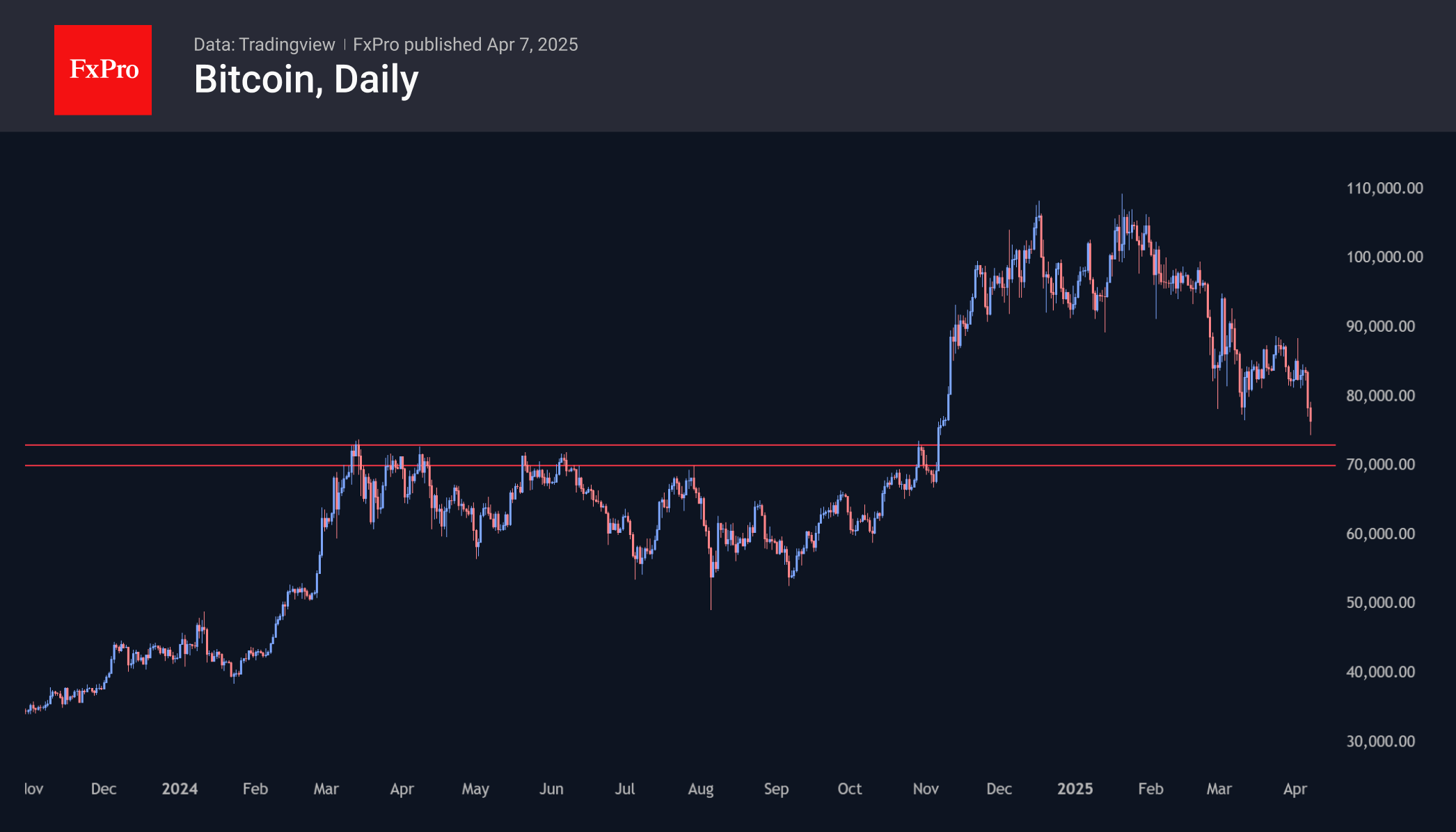

Bitcoin fell below $75K at the start of the day on Monday, its lowest level since November 6th. There are signs of a bounce forming in European trading, but this is more due to the excessive failure from late Sunday. On the daily timeframe, there are no visible obstacles up to the $70-73K level, which has acted as resistance for most of last year. It is hoped that a return to this level will attract buyers.

News Background

The Bull Score index developed by CryptoQuant is down to 10 points. 100 points on the index corresponds to a maximum bullish environment and 0 to a bearish one. The move into a seller-dominated zone (40 points or lower) came after Bitcoin fell below $96,000.

Technical analyst Ali Martinez also points to the risks of a further correction amid a slowdown in on-chain activity. To get back on a growth trajectory, BTC needs to rise above the short-term market participants’ realised price ($90,570).

Tether will release a new asset specifically for the US market if USDT fails to meet the new requirements.

Japanese Yen Rallies as Financial Markets Slide

The Japanese yen continues to gain ground against the US dollar. In the European session, USD/JPY is trading at 146.05, down 0.58% on the day. On Friday, the yen improved to 14.5.54, its strongest level since Sep. 2024.

Japan's real wages decline for second consecutive month

Japan's nominal wages rose 3.1% in February, in line with expectations and about the 1.8% gain in January. However, adjusted for inflation, real wages dropped in February for a second straight month, with a 1.2% decline. This follows a revised 2.8% decline in January as higher inflation continues to eat away at consumer purchasing power.

The Bank of Japan is widely expected to continue raising interest rates as it normalizes monetary policy. However, the latest round of US tariffs have muddied the economic landscape. The BoJ could decide to hold rates at its May 1 meeting in order to better assess the impact of the tariffs on Japan. The US has imposed a 25% tariff on auto imports as well as a reciprocal 24% tariff on all Japanese goods. A global trade war would be disastrous for Japan's export-dependent economy.

US nonfarm payrolls stronger than expected

US nonfarm payrolls surprised on the upside with a gain of 228 thousand, up from a revised 117 thousand in February and above the market estimate of 135 thousand. This was the strongest nonfarm payroll reading in three months.

The positive employment report was overshadowed by the latest round of US tariffs which have sent the financial markets tumbling lower. There are increasing fears that the US tariffs and expected counter-tariffs could upend the US economy and tip it into a recession.

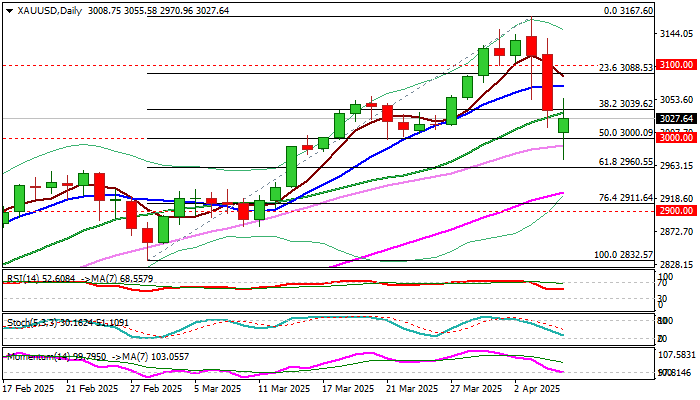

XAU/USD: Reaction at Key $3000 Level to Provide Fresh Direction Signals

Gold dipped below $3000 and hit the lowest in three weeks in early Monday trading, in extension of pullback from new record high in past two days.

Sharp selloff surprised markets as gold price should have risen further in situation of strong risk aversion and growing uncertainty, but heavy losses in stock markets prompted investors to liquidate profitable positions in gold to cover part of losses and margin calls.

Fresh bears cracked $3000 level, which I previously marked as key support (psychological / former higher base / 50% retracement of $2832/$3167 upleg), but subsequent bounce signaled increased headwinds at this zone, highlighting the importance of support.

Reaction at $3000 level will probably provide clearer direction signals, with ability to hold above this level (to register minimum two daily closes above) to generate initial signal that correction is nearing its end.

The notion is partially supported by fresh dovish signals from Fed as markets in new reality, see growing chances for more rate cuts this year than initially estimated.

However, more work at the upside will be required to validate signal with rise above $3050 zone (today’s high / Fibo 38.2% of $3167/$2970 pullback) to revive bulls and close above $3070 zone (50% retracement / 10DMA) to confirm and shift near term focus higher.

On the other hand, unchanged fundamentals (with threats of deterioration) keep the downside at risk.

Sustained break of $3000 trigger to sideline larger bears and open way for deeper correction and unmask targets at $2970/60 and $2926 in extension.

Res: 3039; 3055; 3070; 3088.

Sup: 3000; 2970; 2950; 2926.

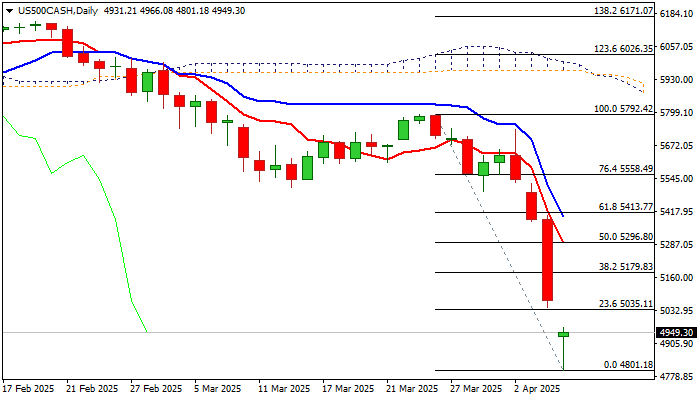

S&P 500 Opens With Gap Lower But Bears May Pause for Consolidation After Last Week’s 8.75% Loss

S&P500 opened with one full figure gap lower on Monday and hit the lowest levels since mid-January 2024, in extension of last week’s 8.75% drop.

The price tumbled after President Trump announced implementation of tariffs on all goods imported to US last week, which sent strong shockwaves through global markets and sparked a panic selloff in wider risk aversion.

The index remains in a bearish path for the second consecutive month, with strong acceleration lower seen last week that makes the total loss of 20% from new all-time high, hit in mid-February.

Although bears slowed on Monday and move within a narrower range, persisting high uncertainty about the magnitude of negative impact from US tariffs on global economy, keeps overall picture very bearish.

Oversold conditions add to signals that bears may take a breather for consolidation / limited correction which should (if general conditions do not improve significantly) offer better selling opportunities.

Formation of bear trap pattern (under Fibo support at $4889) add to signals of consolidation / correction.

Initial resistances at $5040 zone should ideally cap and keep the gap unfilled, while stronger bounce would face significant obstacles at $5179 (Fibo 38.2% of 5792/$4801) and $5296 (50% retracement / daily Tenkan-sen) where extended upticks should be capped.

Res: 5000; 5050; 5179; 5296

Sup: 4889; 4801; 4680; 4591