Sample Category Title

WTI Crude Oil Tanks To $60—Is Deeper Energy Market Shakeup Ahead?

Key Highlights

- WTI Crude Oil prices started a major decline below $68.00 and $65.00.

- It traded below a key contracting triangle with support at $68.50 on the 4-hour chart.

- Gold prices corrected gains and traded below the $3,020 support.

- Bitcoin took a major hit and traded below the $80,000 level.

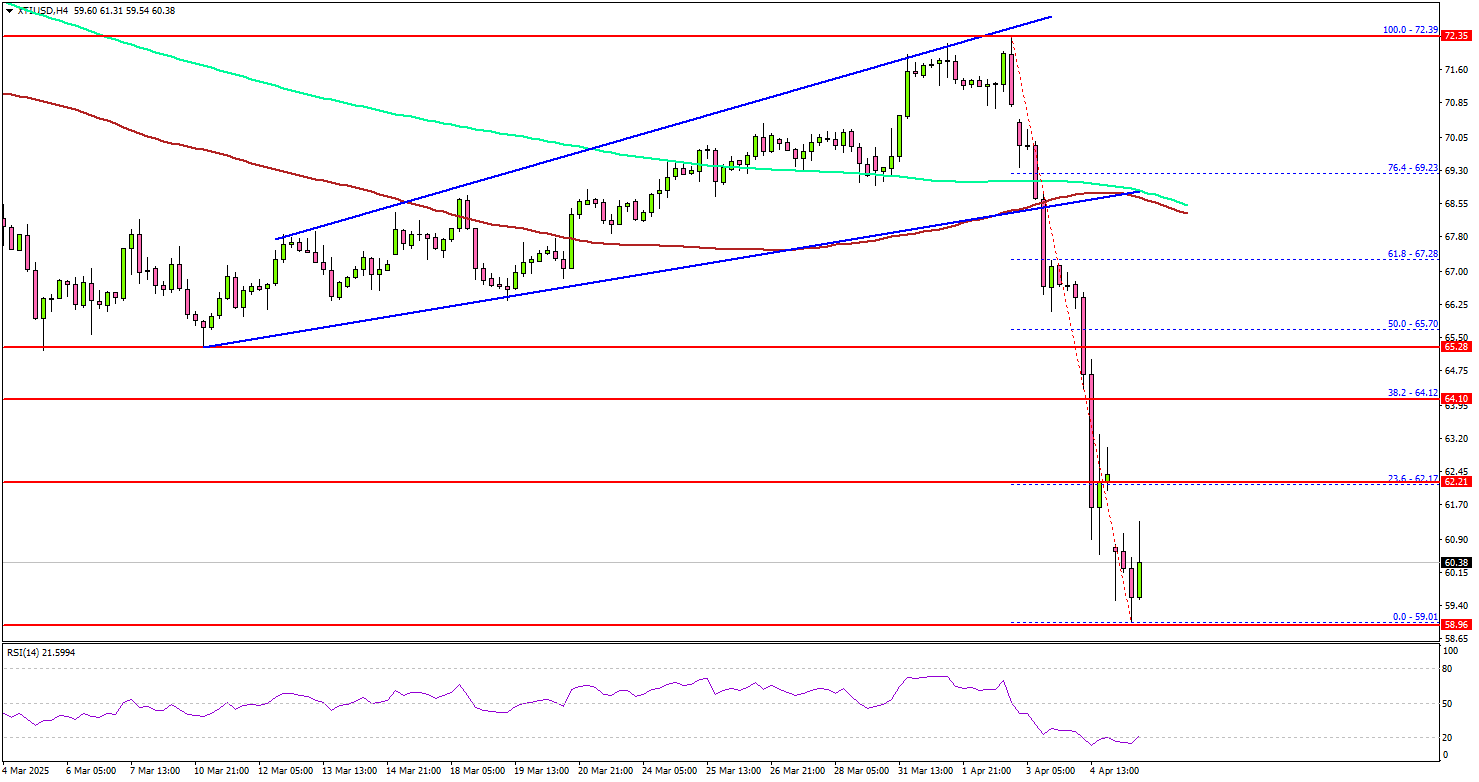

WTI Crude Oil Price Technical Analysis

WTI Crude Oil price started a major decline from $72.50 against the US Dollar. It declined heavily below the $68.00 and $65.00 support levels.

Looking at the 4-hour chart of XTI/USD, the price traded below a key contracting triangle with support at $68.50. The bears even pushed the price below the $62.00 mark. Finally, the price found some support near the $59.00 level.

The price started a consolidation zone, but remained below the 23.6% Fib retracement level of the downward move from the $72.39 swing high to the $59.01 low.

It is also well below the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour). On the upside, the price is facing hurdles near the $61.80 level. The first key resistance sits near the $62.20 level.

The main hurdle is now near the $64.00 zone, above which the price may perhaps accelerate higher. In the stated case, it could even visit the $67.50 resistance. Any more gains might call for a test of the $70.00 resistance zone in the near term.

On the downside, the first major support sits near the $59.00 zone. A daily close below $59.00 could open the doors for a larger decline. The next major support is $57.40. Any more losses might send oil prices toward $55.00 in the coming days.

Looking at Gold, there was a strong downside correction, and the bears pushed the price below the $3,050 and $3,020 support levels.

Economic Releases to Watch Today

- NFIB Business Optimism Index for March 2025 – Forecast 101.3, versus 100.7 previous.

Stock Market Today: S&P 500, Dow Jones Find Support, Tariff Clouds Linger

- The S&P 500 and Dow Jones experienced volatile trading due to ongoing tariff concerns, with initial losses followed by gains on EU counter-tariff news.

- Major tech stocks like NVIDIA, Amazon, and Meta Platforms saw gains, while Tesla and Apple struggled due to their China exposure.

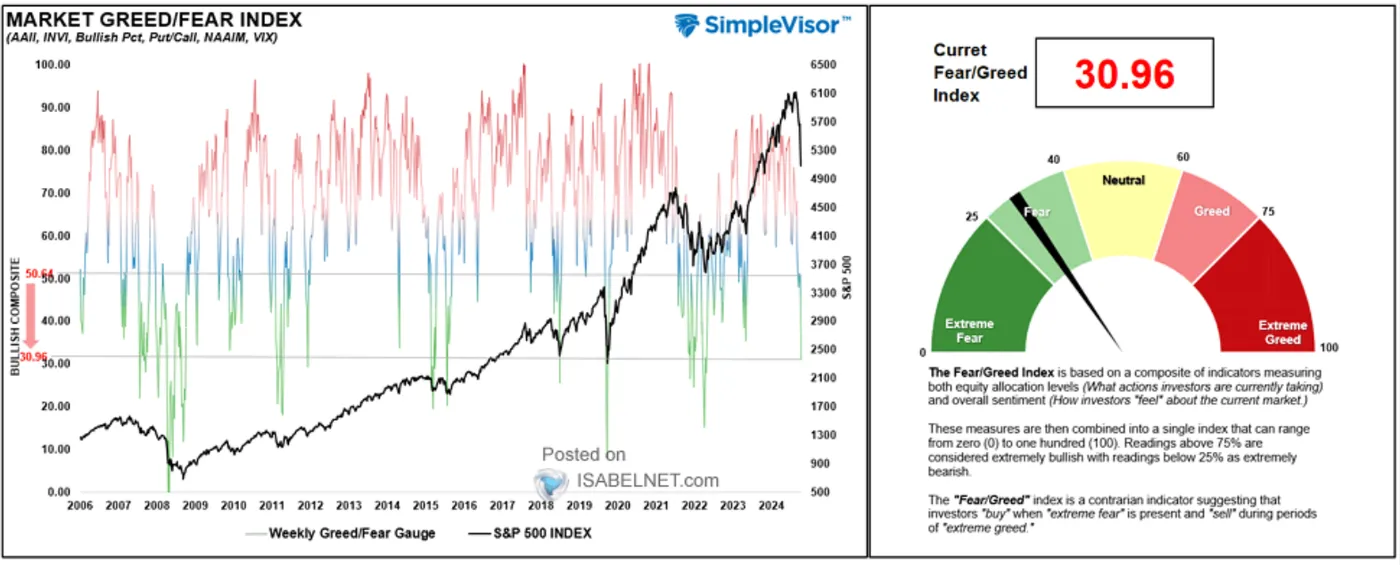

- The Market Greed/Fear Index indicates significant fear among investors, but historical data suggests sharp market declines can be followed by strong recoveries. Is it to soon?

- Expect continued market volatility and whipsaw price action in the short term as tariff news develops.

Wall Street Indexes have seen a mixed bag today with wild swings from fresh lows to small gains at the time of writing. After starting the week in the red early in the session, the S&P 500 gained on news of a document which showed the EU has proposed counter tariffs on a range of US imports at 25%.

This is in response to US steel duties while also removing US bourbon from its list of goods to face counter tariffs. About 200 or so of the S&P 500 constituents are now either flat or in positive territory.

Source: TradingView

Among the notable heavyweights, NVIDIA is up 4.53%, Amazon is up 2.92% and Meta Platforms is trading 3% higher at the time of writing.

Tesla and Apple continue to feel the weight of further trade war developments due to their heavy exposure to China. The US-China situation continues to develop as earlier in the day U.S. President Donald Trump said he will impose an additional 50% tariff on China if Beijing does not withdraw its retaliatory tariffs on the United States.

Sentiment remains fragile but is there a case for optimism?

The Market Greed/Fear Index at 30.96 signals significant fear among investors, reflecting heightened concerns about a recession and economic damage from the ongoing trade war.

Source: IsabelNet

There are also growing rumors and concerns of more US troops and military equipment heading to the Middle East which has stoked fears of an attack on Iran at a crucial time for global markets.

This begs the question, is there any reason for optimism?

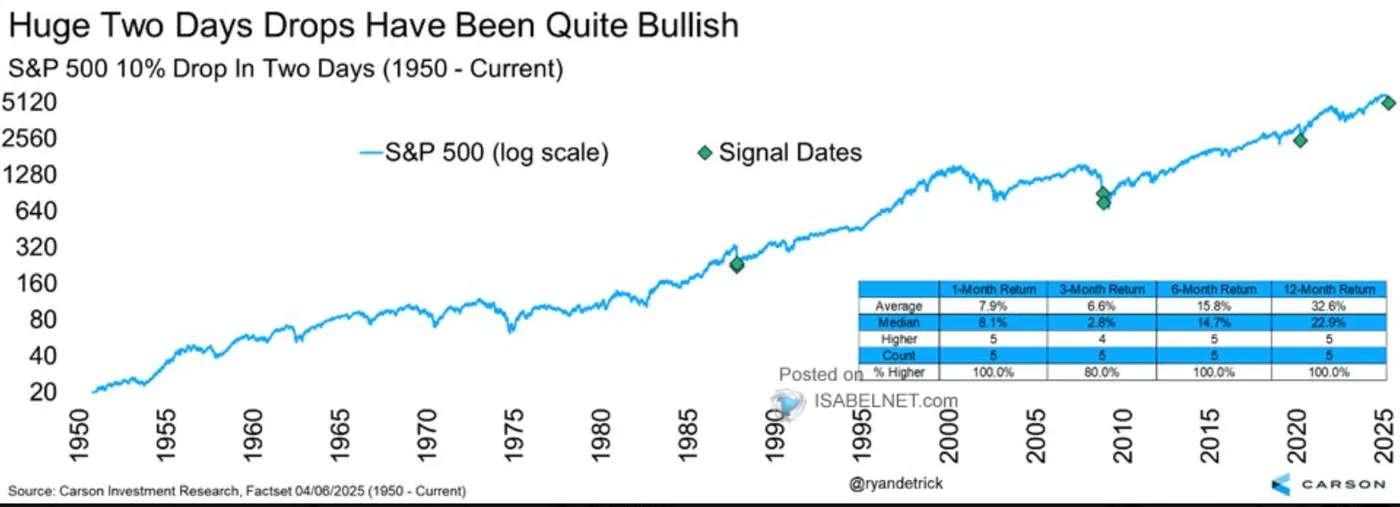

Historical data may not always be 100% accurate in predicting future movements but they do provide us with valuable insights. With that in mind, a 10% drop in the S&P 500 over two days is unusual, but history shows that sharp declines are often followed by strong recoveries, giving investors reason for optimism.

As you can see from the chart below such movements are usually followed by strong performance in the days and weeks ahead.

Source: IsabelNet

Will history repeat itself or is it too early to tell?

What can we expect moving forward?

There does seem to be a lot of conflicting views as to how markets may shape up tomorrow and the days ahead. However, if there is one thing that seems certain it is volatility.

In the short-term I expect more wild price swings as news and developments around tariffs filter through. Traditional trend trading may prove extremely difficult in the days ahead given the sharp decline and selloff last week.

A bounce cannot be ruled out as evidenced by today's move but dynamics are shifting so quickly that sustainability of such moves are likely to prove challenging.

Technical Analysis - Dow Jones

From a technical standpoint, the Dow Jones opened with a gap to the downside something which we saw across a host of markets.

The recent recovery on Wall Street Indexes has seen the Dow close the gap and record some gains before sellers returned. At the time of writing, the Dow Jones is trading 0.57% down for the day.

The 14-period RSI on a daily timeframe remains in extremely oversold territory which means a bounce remains very much in play.

Immediate resistance rests at 38256 before the 39000 handle and the psychological 40000 come into focus.

On the downside support has been found at 36600 with the next areas of support at 35700 and 35000.

Dow Jones (US30) Daily Chart, April 7, 2025

Source: TradingView (click to enlarge)

Support

- 36600

- 35700

- 35000

Resistance

- 38256

- 39000

- 40000

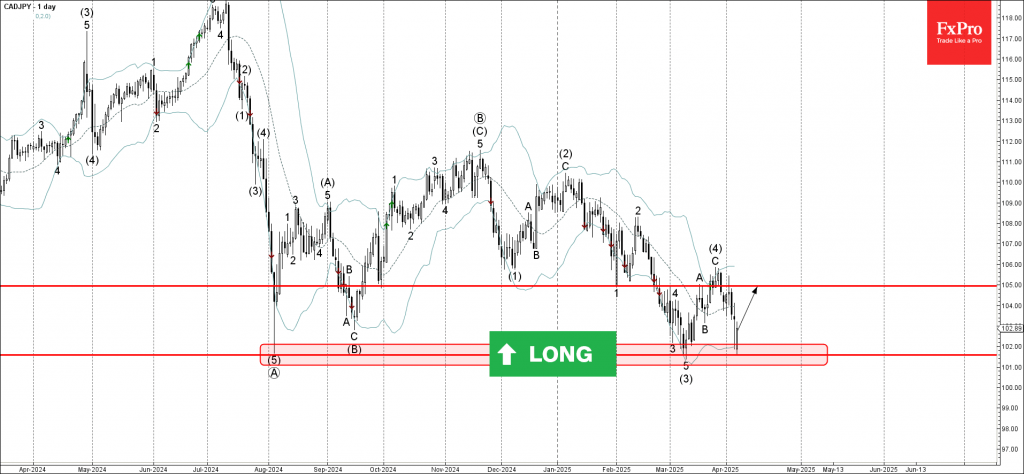

CADJPY Wave Analysis

CADJPY: ⬆️ Buy

- CADJPY reversed from strong support 101.60

- Likely to rise to resistance level 105.00

CADJPY currency pair recently reversed from the support zone surrounding the strong support 101.60 (which has been reversing the price since last August). This support zone was strengthened by the lower daily Bollinger Band.

The upward reversal from support 101.60 stopped the earlier intermediate impulse wave (5) from the end of March.

Given the strength of the support 101.60 and the bullish Canadian dollar sentiment seen today, CADJPY currency pair can be expected to rise to the next resistance level 105.00.

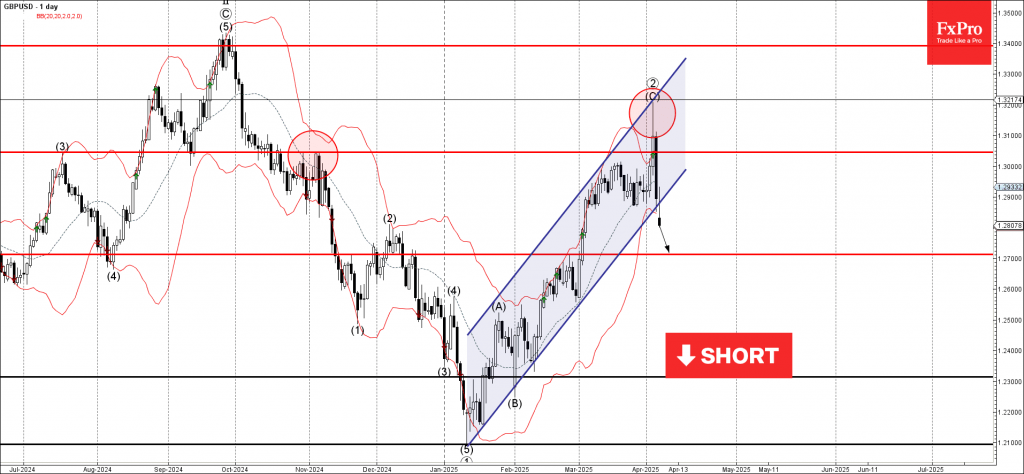

GBPUSD Wave Analysis

GBPUSD: ⬇️ Sell

- GBPUSD reversed from resistance area

- Likely to fall to support level 1.2700

GBPUSD currency pair recently reversed down from the resistance area between the resistance level 1.3050 (which reversed the price in October and November), upper daily Bollinger Band and the resistance trendline of the daily up channel from January.

The pair just broke the aforementioned daily up channel – which should accelerate the active impulse wave 1.

Given the moderately bullish US dollar sentiment seen today, GBPUSD currency pair can be expected to fall to the next support level 1.2700.

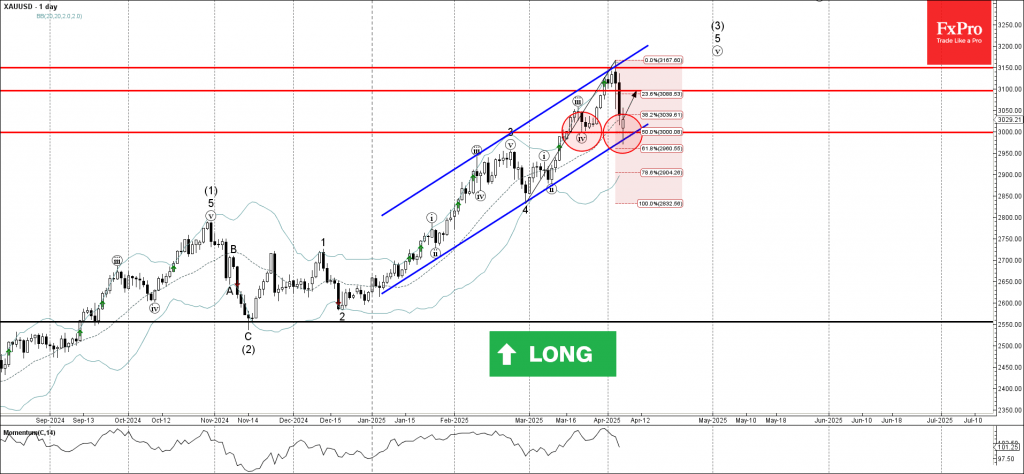

Gold Wave Analysis

Gold: ⬆️ Buy

- Gold reversed from round support level 3000.00

- Likely to rise to resistance level 3100.00

Gold recently reversed up from the support area between the round support level 3000.00 (which stopped the earlier minor correction iv in the middle of March) and the lower daily Bollinger Band.

This support area was further strengthened by the support trendline of the daily up channel from January and by the 50% Fibonacci correction of the sharp upward impulse from February.

Given the strong uptrend on the daily and weekly charts, Gold can be expected to rise to the next resistance level 3100.00.

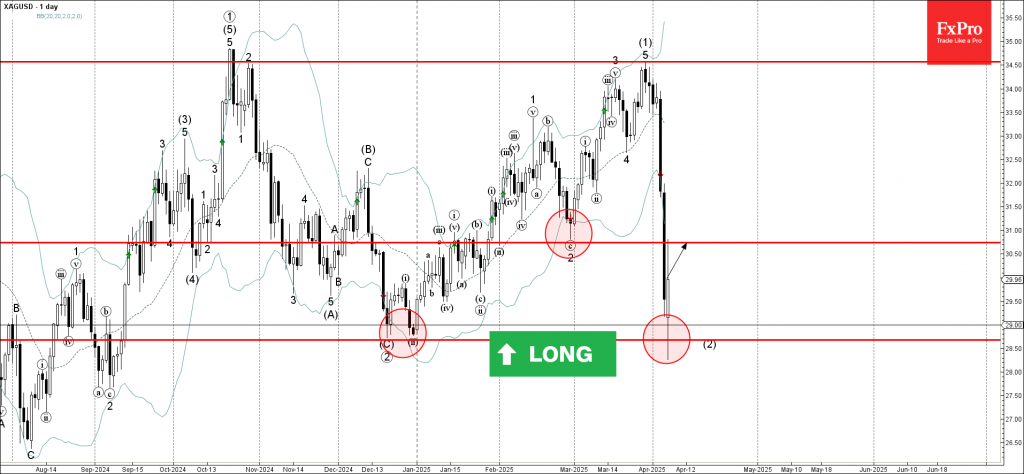

Silver Wave Analysis

Silver: ⬆️ Buy

- Silver reversed from the support zone

- Likely to rise to resistance level 30.75

Silver recently reversed up from the support zone between the strong support level 28.80 (which formed Double Bottom at the end of December) and the lower daily Bollinger Band.

The upward reversal from this support zone stopped the previous sharp downward correction (2) from the end of March.

Silver can be expected to rise to the next resistance level 30.75 (the former monthly low from February, acting as the resistance after it was broken at the start of April).

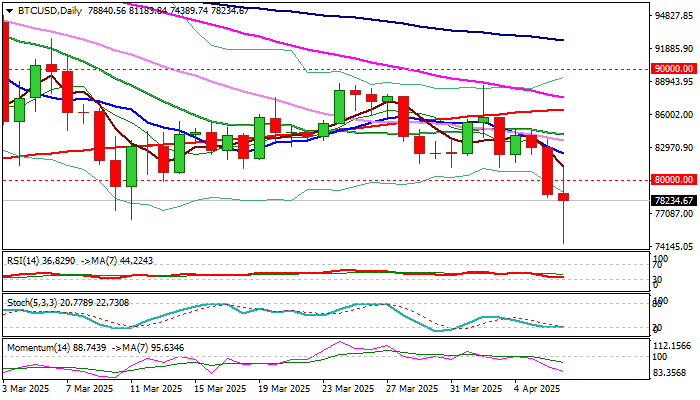

Bitcoin Struggles to Regain Traction after Being Hit by Risk Aversion and Fell to the Lowest in Five Months

Bitcoin bounced from new five-month low on Monday after broader risk aversion on fears from tariff impact, also deflated cryptos.

Fresh strength cracked psychological 80K resistance, but firm break higher is required to offset negative signal from last week’s close below this level.

Otherwise, near-term focus will remain shifted to the downside as technical studies are bearish on daily chart and fundamentals continue to weigh (economic slowdown and higher inflation as the major negative consequences of trade war escalation).

Bears eye pivotal support at 73618 (Fibo 38.2% of 15437/109582) violation of which would further weaken near term structure and expose psychological 70K support.

Conversely, close above 80K would ease immediate downside pressure however, more work at the upside will be still required to verify initial positive signal.

Res: 80000; 81183; 82479; 84144

Sup: 76550; 74389; 73618; 70000

Sunset Market Commentary

Markets

Asian markets started with an accelerated risk sell-off this morning with indices tumbling from 5.5% (South Korea), over 7%+(CSI 300 & Nikkei 225) to 13.2% (Hang Seng). China on Friday matched Trump’s 34% general tariffs for US goods which was a clear sign of the trade war escalating. It also highlighted that the Trump tariffs’ sheet doesn’t provide any kind of worst-case-scenario that could be mitigated in case of successful negotiations. US officials indicated they don’t intend to backtrack on their aim to reduce trade deficits. More (e.g. sector related tariffs) still might be on the cards. Trading partners, including the EU, are preparing retaliation measures. The complete absence of visibility makes it impossible for markets to try to make any assessment yet on the final outcome in terms of tariffs or trade flows. US President Trump and other officials currently indicated that trading partners (e.g. Japan) are prepared to negotiate, but the outcome remains unpredictable. Unpredictability a fortiori applies to the outcome regarding growth (recession, how deep of a recession?) or inflation. In this context, fiscal and monetary policy makers will also face a (prolonged) period of ‘flying blindly’, with ample risks of policy errors.

Regarding monetary policy, markets assume that central bankers at some point will (have to) step in. For the ECB, chances of a scenario of below trend growth and a potential deflationary impact of a negative demand shock are seen as opening the way for additional rate cuts beyond the April meeting. Markets now discount the ECB to cut rates to around 1.5%-1.75% (well below neutral) by the end of this year. Things are changing fast these days, but we remain skeptical whether inflation will allow the ECB to move to stimulatory territory anytime soon. In this respect, several EU governments, including the prospective coalition in Germany, is signalling fiscal stimulus to address the fall-out from the tariffs. Even so, Bund yields today again decline between 10 bps (2-y) and 2 bps (30-y) admittedly with yields well off the intraday lows. The decline in EMU swap yields is much smaller compared to Bunds. As was already the case last week, intra-EMU spreads against Germany are widening (Italy +6 bps, Spain, Portugal, Greece +4 bps). US yields opened deep in red this morning (about 20 bps at some point for the 2-y yield), but completely reversed the earlier decline(currently 2y flat, 30 y + 11 bps). Money markets have ‘scaled back’ rate cut bets for the eoy 2025 from 125 bps to about 100 bps. This of course is still far away from Fed Chair Powell’s wait-and-see guidance last Friday. Still, maybe Powell’s comments have helped to temper expectations on a (too cheap) Fed put. This kind of sharp intraday moves without high-profile news of course illustrates the absence of any visibility. The EuroStoxx 50 for now mitigates losses to 5.5%. US indices started with losses of 4%+. On FX markets, the major USD cross rates today showed no clear directional trend. Amid still wide intraday swings, the TW DXY index trades modestly higher at 103. EUR/USD trades little changed near 1.0955. The yen still marginally outperforms (USD/JPY 146.7 from 146.9). Smaller, less liquid currencies remain in the defensive. EUR/GBP blew away the 0.8474 YTD top to currently trade near 0.8575. Also the likes of the Swedish krone (EUR/SEK 11.50 from 11.0 at the open) and even more the oil-sensitive Norwegian krone are fighting an uphill battle (EUR/NOK currently at 11.95, intraday >12.00, to be compared with EUR/NOK <11.30 end last week). The zloty (EUR/PLN 4.28), and the forint (EUR/HUF 408) are meeting headwinds too. The Czech koruna outperformed, regaining part of Friday’s loss (EUR/CZK 25.16).

News & Views

Czech industrial production rose by 1.5% Y/Y in real terms in February. Growth was mainly influenced by a low comparison basis from February 2024 in electricity, gas, steam and air conditioning supply that was influenced by climatic conditions. Manufacturing production stagnated in Y/Y-terms. On a monthly basis, industrial production was 1.7% higher. The value of new industrial orders decreased for a second consecutive month, this time by 1.3% Y/Y. A moderate decrease was recorded by the automotive industry. The average registered number of employees in industry decreased by 2% Y/Y in February 2025. In a separate release, the Czech Statistical Office indicated that the goods trade balance ended February with a CZK 35.5bn surplus, which was CZK 0.5bn lower Y/Y. Exports increased by 1.3% Y/Y to CZK 400bn while imports rose by 1.6% Y/Y to CZK 364.5bn.

Stocks Extend Slump; EU Eyes Talks, US Signals Tough Stance

The global stock market rout continues to deepen today, with no clear signs of easing. Investor focus remains firmly on how the world is responding to the U.S.’s sweeping reciprocal tariffs. While equity markets crumble under the weight of growing uncertainty, developments out of Europe hint at a more constructive path—at least for now.

A cautiously optimistic signal came from Europe, where leaders appear intent on prioritizing negotiations over immediate retaliation. In Luxembourg, EU ministers convened to assess their next steps, while European Commission President Ursula von der Leyen emphasized that “Europe is always ready for a good deal.” She noted that the EU has offered “zero-for-zero tariffs” on industrial goods in its ongoing attempts to preserve open trade.

Despite this diplomatic posture, preparations for countermeasures are clearly underway. French Trade Minister Laurent Saint-Martin signaled that nothing is off the table, referencing the EU's Anti-Coercion Instrument as a possible response. This mechanism would empower the bloc to restrict US service access or exclude American firms from public procurement within the EU—an unmistakable sign that Europe is readying its arsenal if negotiations break down.

On the other hand, the tone from the US remains uncompromising. White House trade adviser Peter Navarro told CNBC that Vietnam’s offer of zero tariffs is “meaningless” without addressing non-tariff barriers, such as intellectual property theft and value-added tax disparities. “That’s a small first start,” Navarro later added, making it clear that tariff elimination alone won’t satisfy the Trump administration’s trade goals.

This hardened stance suggests bilateral negotiations with the US will likely be prolonged and complex, especially with dozens of countries seeking exemptions or deals. The realization that tariff disputes are not simply about levies but about deeper structural trade practices is pushing expectations for a swift resolution further into the distance.

In the currency markets, movement is relatively more measured compared to equities. Sterling is the weakest performer so far today, followed by Loonie and Kiwi. On the stronger end, Swiss Franc leads, followed by Aussie and Yen. Dollar and Euro are positioning in the middle. For now, FX traders may be waiting for further clarity before taking decisive positions, especially as trade negotiations unfold and market volatility remains elevated.

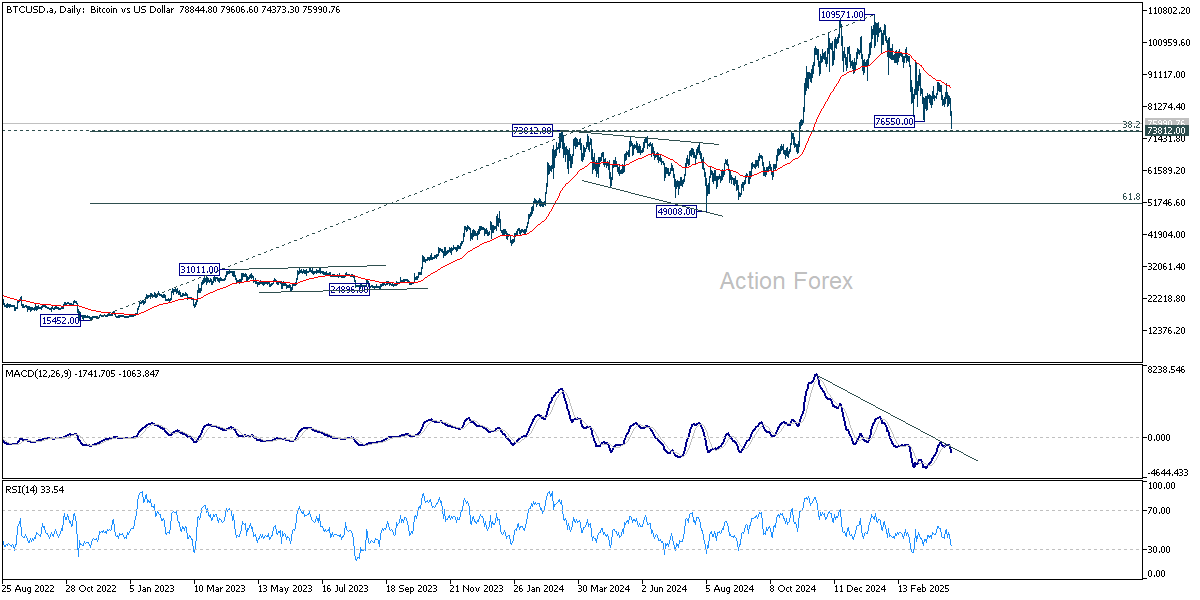

Technically, Bitcoin is resuming the fall from 109571 today, and immediate focus is now on 73812 cluster support (38.2% retracement of 15452 to 109571 at 73617). Decisive break there will open up deeper correction to 61.8% retracement at 51405 in the medium term. That would be another drag on overall sentiment if realized.

In Europe, at the time of writing, FTSE is down -4.52%. DAX is down -4.67%. CAC is down -5.02%. UK 10-year yield is up 0.092 at 4.545. Germany 10-year yield is down -0.014 at 2.566. Earlier in Asia, Nikkei fell -7.83%. Hong Kong HSI fell -13.22%. China Shanghai SSE fell -7.34%. Singapore Strait Times fell -7.46%. Japan 10-year JGB yield fell -0.04 to 1.116.

Eurozone Sentix falls to -19.5, expectations collapse to -15.8 on trade war

Investor sentiment in the Eurozone suffered a dramatic collapse in April, as the Sentix Investor Confidence Index plunged from -2.9 to -19.5, far below expectations of -8.7 and marking the lowest reading since October 2023. Current Situation Index dipped slightly from -21.7 to -23.3.

The sharpest shock came from the Expectations Index, which nosedived from 18.0 to -15.8—its lowest level in 18 months and a staggering drop of -33.8 points, the second steepest fall ever recorded in Sentix history.

Sentix directly attributed the deterioration to US President Donald Trump’s sweeping new tariff measures, stating that last month’s optimism across Germany and the broader EU had “evaporated.”

The group warned that the early indicators point to a “massive problem,” with global economic stability seriously threatened. With Trump showing no signs of reversing course, Sentix cautioned that the tariff war is likely to “drag on longer than many assume,” fueling deeper disruptions.

Eurozone retail sales rise 0.3% mom in Feb, EU up 0.2% mom

Eurozone retail sales volumes rose by 0.3% mom in February, falling short of the expected 0.5% mom increase. The breakdown showed modest improvements across key segments: food, drinks, and tobacco sales were up 0.3% mom; non-food products excluding automotive fuel also rose 0.3% mom; while automotive fuel sales edged up 0.2% mom.

Retail sales across the broader EU climbed just 0.2% mom, with notable divergence among member states. Cyprus led with a 4.7% gain, followed by Estonia (+2.2%) and Lithuania (+1.7%). Meanwhile, retail trade volumes declined in Bulgaria (-1.7%), the Netherlands (-1.4%), and Poland (-1.2%).

ECB’s Stournaras: US Tariffs definitely deflationary, growth hit could reach 1%

Greek ECB Governing Council member Yannis Stournaras warned that the US reciprocal tariffs were “worse than expected” and a source of “unprecedented” global policy uncertainty.

In an interview with the Financial Times, he characterized the tariffs as “definitely a deflationary measure” for the Eurozone.

"A notable adverse impact on growth could lead to activity being much weaker than expected, dragging inflation below our targets," he added.

While conceding it’s difficult to quantify the exact fallout, Stournaras projected a potential hit of between 0.5 to 1 percentage points to Eurozone growth.

He refrained from speculating on whether the threat justifies a 50bps rate cut but underscored the seriousness of the downside risks.

Japan’s real wages fall again despite nominal pay boost from bonuses

Japan’s nominal wages rose 3.1% yoy in February, a notable jump from downwardly revised 1.8%yoy in January, matching expectations.

However, this strong print was largely driven by a surge in special payments, which skyrocketed 77.4% yoy. Regular pay, considered a more stable indicator of wage trends, actually slowed to 1.6% yoy from the prior month’s 2.1% yoy, signaling only moderate momentum in base salary growth.

Despite the upbeat headline figure, real wages—which adjust for inflation—fell for the second consecutive month, down -1.2% yoy. This came as consumer inflation, as calculated by the labor ministry, remained elevated at 4.3% yoy, down slightly from January’s 4.7% yoy.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0889; (P) 1.0999; (R1) 1.1072; More...

EUR/USD is extending consolidations below 1.1145 and intraday bias remains neutral. Downside of retreat should be contained by 38.2% retracement of 1.0176 to 1.1145 at 1.0775 to bring rebound. On the upside, above 1.1145 will resume the rally from 1.0176 to 1.1213/74 key resistance zone next.

In the bigger picture, fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through the multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0731 support holds.