Sample Category Title

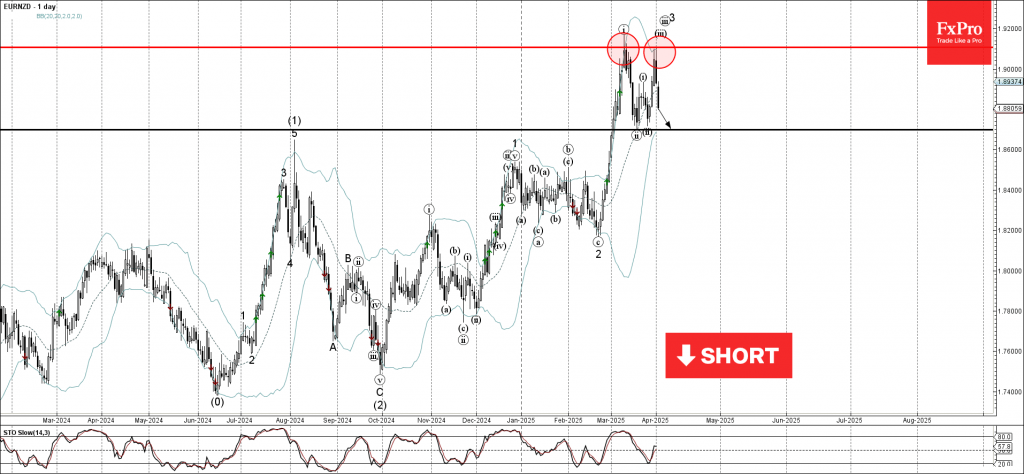

EURNZD Wave Analysis

EURNZD: ⬇️ Sell

- EURNZD reversed from resistance area

- Likely to fall to support level 1.8700

EURNZD currency pair recently reversed down from the resistance area located between the resistance level 1.9100 (which stopped the earlier sharp upward impulse wave I at the start of March) and the upper daily Bollinger Band.

The downward reversal from this resistance area stopped the earlier short-term impulse wave iii of the upward impulse wave 3 from the end of February.

Given the strength of the resistance level 1.9100, EURNZD currency pair can be expected to fall to the next support level 1.8700.

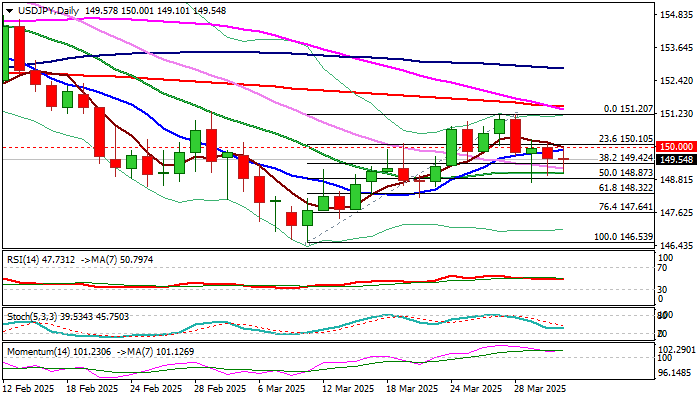

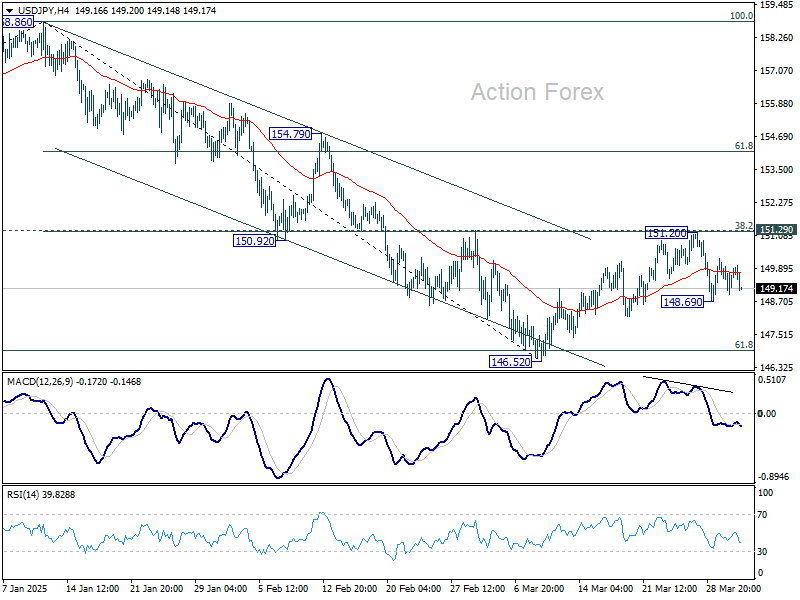

USD/JPY: Pressure Lower Boundary of Near-Term Range Ahead of Tariff Announcement

USDJPY remains at the back foot on Wednesday and dips further below 150 level, which reverted to solid resistance (three consecutive attacks stalled here).

Fresh weakness pressures 20DMA (149.06, where bears faced strong rejections in past two days) which offers good support, along with nearby 50% retracement of 146.53/151.20 upleg (148.87).

Rising risk aversion ahead of tonight’s tariff decision continues to underpin demand for safe haven Japanese yen.

The pair is likely to accelerate lower if President Trump opts for implementation of full package of import tariffs, which would escalate trade war and further destabilize already fragile conditions in the global economy.

Sustained break of 149.06/148.87 to confirm an end of corrective phase (146.32/151.20) and expos targets at 148.32 and 147.64 (Fibo 61.8% and 76.4% respectively).

Strong barriers at 150.00 (psychological/10DMA) should keep the upside protected and maintain bearish bias, while firm break higher would be a game changer.

Res: 150.00; 150.26; 151.00; 151.38.

Sup: 149.06; 148.87; 148.32; 148.00.

Sunset Market Commentary

Markets

US President Trump has been keeping the market in extreme suspense the last few weeks and especially days with what he calls “the Big One”. That’s referring to a major tariff policy plan that almost certainly trumps all the levies POTUS already introduced earlier this year. The big unveil is almost there and markets are anxious to know the outcome. And yet, mere hours before “Liberation day” there are a lot of unknowns that reportedly are still being discussed as we write. Proposals floated by the media include a tiered system with a flat 10% or 20% rate for all countries as well as a more customized reciprocal plan but with unspecified tariff levels. The baseline is to “[We] charge them what they charge us” but Trump said they’ll look beyond the obvious tariff barriers that certain countries have in place to include non-tariff barriers as well. He has for example lashed out at Europe’s VAT system which he says favours domestic companies over foreign (ie US) ones. It’s also unclear what countries the Trump administration plans to target with the scope most likely broader than just countries having a trade surplus with the US. Lastly, we don’t know whether the tariffs are scheduled to kick in immediately (according to the White House press secretary Leavitt’s “understanding”) or if there’s still some time for negotiations to try to avoid them. Finally having answers, however bad they sound, could ironically bring some relief after an initial Pavlov risk off market reaction.

Going into the announcement, markets understandably err to the side of caution regardless of solid but second-tier US data. The unofficial jobs report from ADP printed a 155k employment growth in March, picking up from 84k and beating the 120k consensus. “Despite policy uncertainty and downbeat consumers, the bottom line is this: The March topline number was a good one for the economy and employers of all sizes, if not necessarily all sectors.” ADP’s chief economist summarized. Stocks in Europe decline about 1%, Wall Street opens between 0.7-1.2%. Core bonds get a nice bid with safe haven flows pushing US Treasury yields down between 2.1-3.8 bps across the curve. The German curve bull flattens with euro area money markets pricing in the lowest end-of-year ECB policy rate (+/- 1.75%) since early February. Net daily changes amount to -0.8 to 2.8 bps. Currency markets disconnect from the typical risk aversion though with especially a lackluster dollar catching the eye. A growing stagflationary narrative has been weighing down on the greenback and tariffs are obviously not soothing any of the concerns. DXY revisits 104, EUR/USD tops 1.08(2). A strong outperformance by FX Down Under and high up north is (again) striking. EUR/SEK hits a new 2.5 year low around 10.74.

News & Views

The Hungarian debt agency (AKK) updated its 2025 funding plan. At the end of Q1, they completed 38% (HUF 4378bn) of the planned yearly gross issuance which was raised from HUF 10 096bn to HUF 12 503bn. For the remainder of the year, AKK plans to increase institutional government auctions, while lowering the expected net financing from households. The planned volume for HGB auctions increases from HUF 4742bn to HUF 5151bn. Tenorwise, AKK wants to focus more on 5-yr bonds and less on 10-yr bonds as per investor demand. Net retail financing decreases by the same HUF 408bn, from HUF 1323bn to HUF 915bn. The average term-to-maturity of Hungarian central government debt is 5.6 years, 4.2 years in case of HUF debt and 8.7 years in case of FX debt. The FX debt share will decrease below 30% by the end of the year from 30.3% currently. AKK plans some final FX-issuance (90% already covered) later this year in the Chinese markets.

The Czech Statistical Office announced that the government deficit decreased from 3.7% of GDP in 2023 to 2.2% of GDP in 2024. In nominal terms, the deficit amounted CZK 177.2bn. In the YoY-comparison, total revenue, of which mainly received social contributions, was increasing more (+6.8% YoY) than the expenditure (+2.9% YoY). The government debt ratio increased from 42.5% of GDP to 43.6% or CZK 3492.2bn in nominal terms.

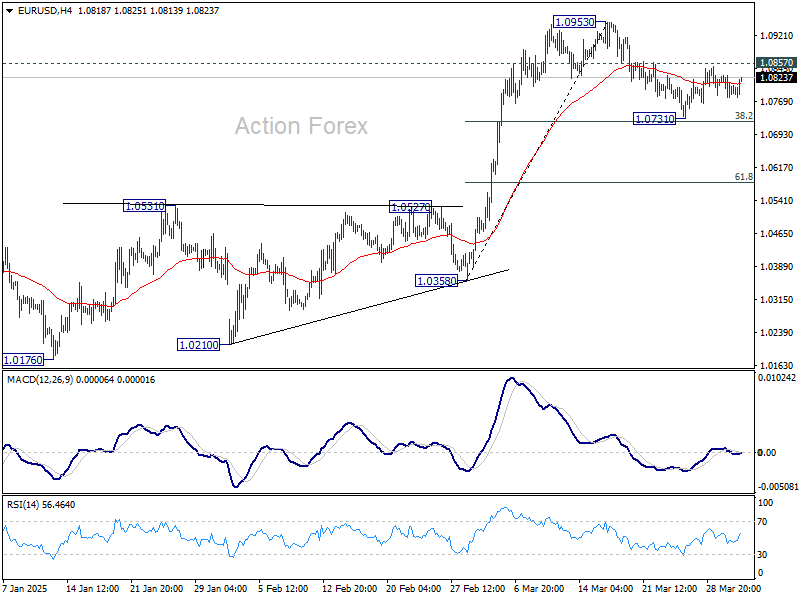

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0770; (P) 1.0800; (R1) 1.0822; More...

Intraday bias in EUR/USD remains neutral at this point. On the upside, break of 1.0857 resistance will indicate that correction from 1.0963 has completed already. Retest of 1.0953 should be seen first. Firm break there will resume the rally from 1.0176 towards 1.1274 key resistance. However, firm break of 38.2% retracement of 1.0358 to 1.0953 at 1.0726 will bring deeper correction to 55 D EMA (now at 1.0656).

In the bigger picture, prior strong break of 55 W EMA (now at 1.0692) suggests that fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 is still intact, and might be ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through a multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0531 resistance turned support holds.

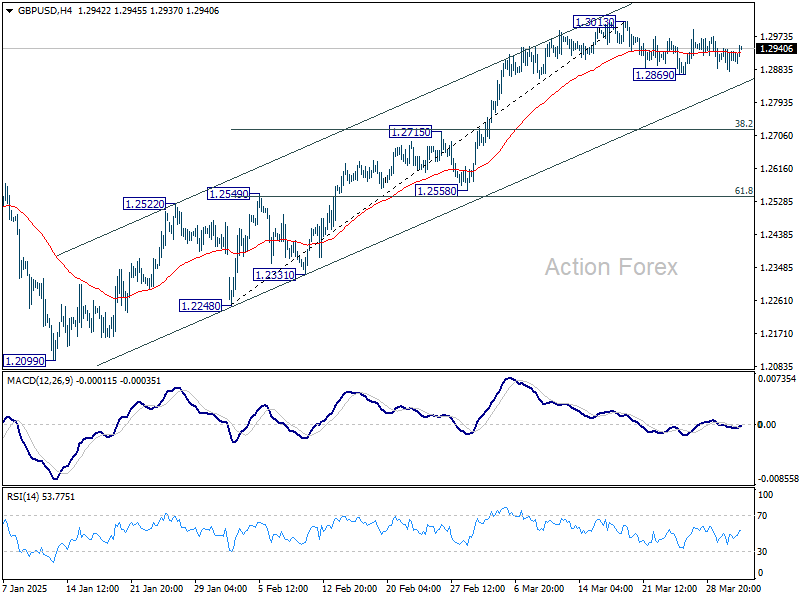

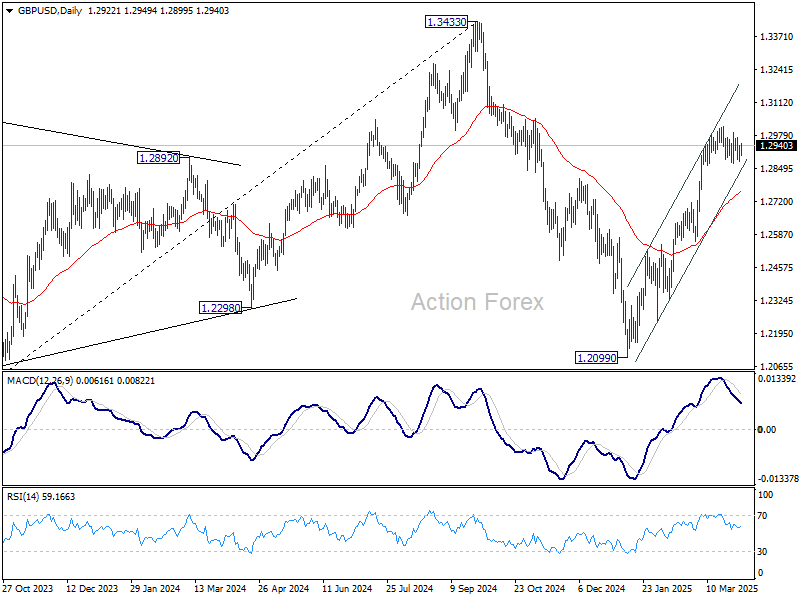

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2888; (P) 1.2915; (R1) 1.2950; More...

Intraday bias in GBP/USD remains neutral as consolidation from 1.3013 continues. On the downside, below 1.2869 will bring deeper correction. But downside should be contained above 38.2% retracement of 1.2248 to 1.3013 at 1.2721. On the upside, break of 1.3013 will resume the rally from 1.2099 towards 1.3433 high.

In the bigger picture, up trend from 1.3051 (2022 low) is not completed. Resumption is expected after corrective pattern from 1.3433 completes. Next target will be 1.4248 key resistance (2021 high). This will now remain the favored case as long as 1.2099 support holds.

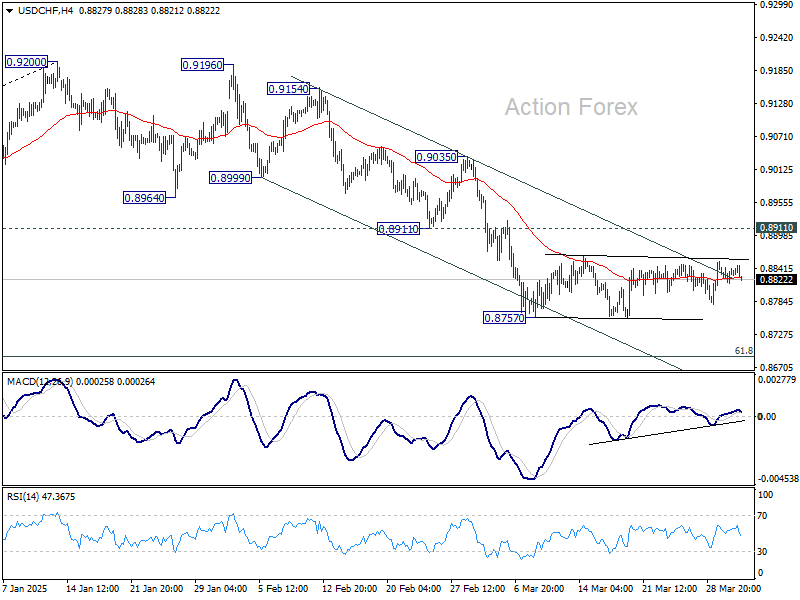

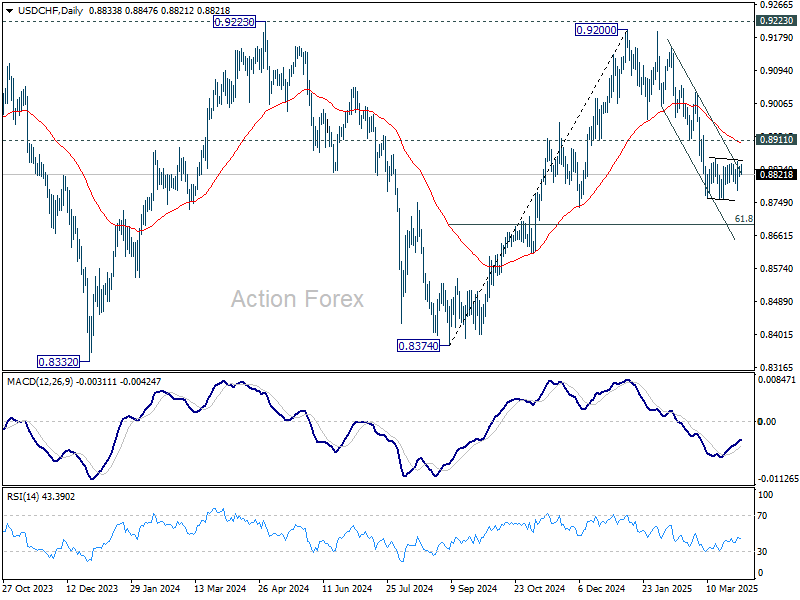

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8819; (P) 0.8835; (R1) 0.8854; More…

Intraday bias in USD/CHF stays neutral for the moment. Consolidation from 0.8757 is still in progress. In case of stronger recovery, upside should be limited by 0.8911 support turned resistance. On the downside, break of 0.8757 will resume the fall from 0.9200 to 61.8% retracement of 0.8374 to 0.9200 at 0.8690. Sustained break there will pave the way back to 0.8374 support.

In the bigger picture, rejection by 0.9223 key resistance keep medium term outlook bearish. That is, larger fall from 1.0342 (2017 high) is not completed yet. Firm break of 0.8332 (2023 low) will confirm down trend resumption.

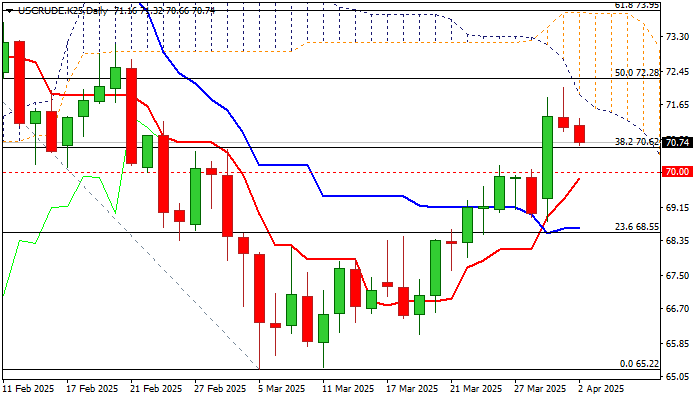

WTI Price Consolidates Under New Multi-Week High

WTI oil price is trading under new five-week high ($72.08, posted on Tuesday) after the price rallied 2.8% on Monday (the biggest daily gain since Jan 15).

Slight easing so far looks more like a consolidation rather than stronger profit-taking as markets turned to quiet mode and await the verdict about tariffs from US President Trump (due later today).

Positive factors that boost oil demand were threats from the US on imposing the secondary tariffs on buyers of Russian oil, better than expected China’s recent economic data which boost hopes for stronger demand from the world’s number one oil importer and growing tensions between the US and Iran.

OPEC+ will meet on Thursday and expect to stick to plans for further output increase from May that would partially counter the impact of supportive factors.

All eyes are now on President Trump’s tariff announcement, which is likely to be the key driver.

Market are expected to be volatile, and reaction will directly depend on size and scope of new tariffs.

Aggressive tariff rhetoric would further fuel fears of economic slowdown and inflation rise, which would have a negative impact short-term outlook and deflate oil price.

Conversely, softer than expected Trump’s stance on tariffs would keep larger bulls in play and provide fresh support to oil price.

Technical studies are mixed on daily chart, as positive momentum remains strong and north-heading daily Tenkan-sen is diverging from daily Kijun-sen after forming a bull-cross, while the price action remains weighed by falling and thickening daily Ichimoku cloud (base lays at $71.58).

Good supports lay at $70.69/62 (100DMA / broken Fibo 38.2%) followed by $70 zone (psychological, reinforced by rising daily Tenkan-sen).

Daily cloud base marks initial barrier, followed by $72.08 (new high) and $72.28/50 (50% retracement of $79.35/$65.22 / 200DMA).

Res: 72.08; 72.28; 72.50; 73.12.

Sup: 70.62; 70.42; 70.00; 69.70.

Australian Dollar Rally Continues, Trump Tariffs Loom

The Australian dollar has posted strong gains for a second straight day. In the European session, AUD/USD is trading at 0.6306, up 0.47% on the day.

RBA holds rates but hints at further cuts if trade tensions worsen

The Reserve Bank of Australia maintained the cash rate at 4.10% on Tuesday, in a move that was widely expected by markets. Still, the Australian dollar reacted positively, gaining 0.48% on Tuesday.

The RBA statement noted that underlying inflation continued to ease in line with the Bank's forecast, but the Board "needs to be confident that this progress will continue" so that inflation remains sustainable at the midpoint of the 2%-3% target band.

The statement said there was "significant" uncertainty over global trade developments, pointing to the threat of further US tariffs and possible counter-tariffs from targeted countries.

The central bank's decision was made in the midst of a hotly contested election campaign, and a rate cut would likely have been attacked by the opposition parties as political interference.

In a press conference after the meeting, Governor Michele Bullock acknowledged the uncertainty over the global outlook due to US trade policy but sought to assure the markets by saying that Australia was "well placed" to weather the potential storm of a global trade war.

Markets bracing for Trump tariffs

US President Trump has not specifically targeted Australia with any tariffs but China is Australia's number one trading partner and a US-China trade war would inflict damage on Australia's economy.

The new US tariffs are expected to be announced later today and take effect on Thursday. The financial markets remain volatile as investors look for some clarity from Washington about the tariffs, as it remains unclear which countries will be targeted and the extent of the tariff rates.

AUD/USD Technical

- AUD/USD is testing resistance at 0.6297. Above, there is resistance at 0.6315

- 0.6264 and 0.6246 are the next support levels

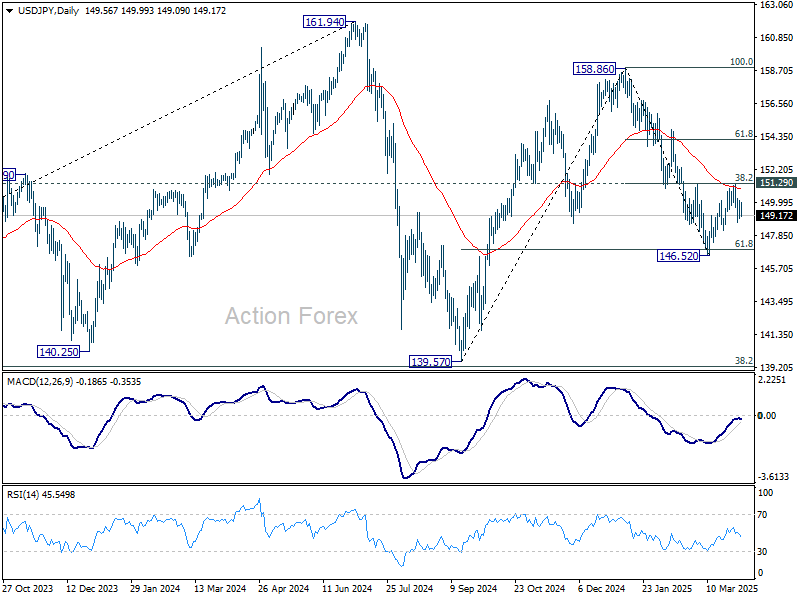

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.01; (P) 149.58; (R1) 150.19; More...

Range trading continues in USD/JPY and outlook is unchanged. Intraday bias remains neutral at this point. Corrective rise from 146.52 could have completed at 151.20 already. Risk will stay on the downside as long as 151.29 resistance holds. Below 148.69 will bring retest of 146.52 low first. Firm break there will resume whole decline from 158.86 towards 139.57 support next.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.