Sample Category Title

Fed Provides Relief – Focus on BoE and SNB

The Fed

US markets breathed a sigh a relief following the Federal Reserve (Fed) decision. The Fed kept its policy rate unchanged as expected, cut the growth forecast and lifted its inflation outlook quite notably but Chair Jerome Powell stressed out that the potential impact of tariffs on inflation would be ‘transitory’ – implying that the Fed could continue to ease policy to support growth. And more importantly, the Fed decided to reduce the pace of Quantitative Tightening (QT) – a move that eases the tightening of the financial conditions.

As such, the Fed elegantly downplayed the long-term impact of rising inflation while cutting its growth forecast. The dot plot showed that the Fed officials continue to foresee two rate cuts on average this year, and activity on Fed funds futures now gives around 70% chance for the next cut to land in June. The decision was more dovish than expected.

The US 2-year yield slipped below the 4%, the 10-year yield eased below 4.25%. The S&P500 jumped more than 1%, Nasdaq 100 gained 1.30%, the Dow Jones recovered 0.93%, the mid-cap stocks jumped 1.26% while the Russell 2000 led gains with a more than 1.50% rebound on relief that the Fed – though cautious – is not planning to deviate from its rate cutting and policy easing plans, as again, the inflation peak due to tariffs would be ‘transitory’.

In the FX, the US dollar index rebounded on the back of a dovish and supportive Fed stance. It’s important to note that up until recently, the dovish central bank expectations would have a weakening effect on currency valuations as lower yields reduce the natural attractivity of a currency. BUT right now, the currency pricing is influenced by growth expectations. Therefore, a more dovish Fed stance increases US growth expectations, tempers the recession odds, and supports the US dollar.

The ECB

Elsewhere, the EURUSD eased below the 1.09 mark. Inflation in the Eurozone came in lower than previously printed for February, wages and labour costs eased in Q4. The latest data brought the possibility of another rate cut from the European Central Bank (ECB) before it pauses, though pause looks more likely in the next meeting due to massive fiscal spending plans. Either way, optimistic shift in EZ growth expectations remain supportive of the euro against the USD and sterling though the appreciation will likely slow provided that most of the optimism is already priced in.

The BoJ

The USDJPY resisted near the 150 offers and is swiftly sold on Bank of Japan’s (BoJ) decision to maintain its rates unchanged citing the geopolitical and trade uncertainties. Here as well, not rushing toward policy normalization is supportive of growth expectations and the currency.

The BoE

Cable keeps bumping its head against the 1.30 offers before the Bank of England (BoE) decision due today. The BoE is expected to stay seated on its hands at today’s meeting, but the MPC landscape is quite not smooth: 7 members out of 9 will probably vote for no change, while two doves are expected to favour a 50bp cut. Investors are feeling dovish regarding the upcoming BoE meeting given that the British growth numbers have taken a hit from the governments’ tax raising plans while the rising gilt yields decreased the spending potential. And the weakening potential for government spending increases the BoE’s ability to support the economy with a more supportive monetary policy, and that could be positive for sterling. But yes, it’s a bit stretched. If sterling breaks the back of the 1.30 offers against the US dollar, it will be thanks to a stronger depreciation of the US dollar than conviction in sterling.

And the SNB

Last but not least, the Swiss National Bank (SNB) is expected to announce a 25bp cut today. Mounting geopolitical and trade tensions between the U.S. and the rest of the world have largely kept neutral, non-EU Switzerland out of the direct line of aggressive tariffs. The Swiss franc has strengthened against the dollar since the start of the year while losing ground against the euro—its biggest trade partner.

This is the best of both worlds for Switzerland: a stronger franc against the dollar helps keep energy prices and inflation in check, while a softer franc against the euro preserves what remains of Swiss competitiveness against European peers, or at least prevents further deterioration.

The SMI index has gained almost 14% since the start of the year, as Swiss companies benefited from sectoral rotations. The high concentration of defensive names—such as pharmaceuticals and consumer staples—positions Swiss stocks well. Additionally, Switzerland’s diplomatic relations with the Trump administration remain manageable for now.

As such, the SMI could continue to benefit from rising appetite for defensive and value stocks, as well as a supportive SNB policy. Rates in Switzerland will likely stay low as long as inflation remains in check—and inflation is now back to 0.4% year-on-year. We maintain our preference for Swiss stocks.

Central Bank Rate Decisions in the Spotlight

In focus today

Today we receive rate decisions from the Bank of England (BoE), the Swiss National Bank (SNB) and the Riksbank.

We expect the BoE will keep the Bank Rate unchanged at 4.50% in line with consensus and market pricing. Additionally, we anticipate the BoE will stick to its previous guidance noting that "a gradual approach to removing monetary policy restraint remains appropriate".

For the SNB, we expect they will cut the policy rate by 25bp to 0.25% as inflation pressures remain muted, hovering in the lower end of the target range. Markets also favour a cut, pricing in roughly 20bp for the meeting.

We think the Riksbank will stay on hold at 2.25% and present a completely flat rate path, which is widely expected. However, we believe the risk is more likely to lean towards a dovish surprise rather than a hawkish one, considering that market pricing is slightly inclined towards the next move being a rate hike.

Norges Bank will release the Regional Survey today. We will keep an eye on the growth prospects for both Q1 and Q2. Based on leading indicators, we expect the expectations to be around 0.3-0.4% q/q, which should be well in line with Norges Bank's forecast from the December MPR. But we will put more emphasis on the capacity metrics this time around, as they are paramount for the inflation and hence rate outlook in the medium turn. This could prove decisive ahead of the monetary policy meeting next week after the latest inflation numbers.

Economic and market news

What happened overnight

In China, the People's Bank of China kept Loan Prime Rate 1Y and 5Y steady at 3.10% and 3.60% respectively. This was widely anticipated by markets and the market reaction was muted. Economic data on the Chinese economy at the start of the year was a mixed bag.

What happened yesterday

In the US, the FOMC meeting in the evening concluded with an unchanged rate decision from the Fed as widely expected. Powell sent a message as balanced as it could be. Not downplaying any downside risks but also emphasising that the Fed is not in a hurry to move. Markets reacted with lower rates, weaker USD and stronger equities. We maintain our call for the next cut in June, and a total of three cuts this year. Read more in our Fed review: Cautious stability, 19 March.

In Ukraine, the call between President Zelenskiy and President Trump was spent aligning both Russia and Ukraine in terms of their requests. We see the latest developments, namely the outcome from the Zelenskyi-Trump call yesterday, as positive for Ukraine, and for the broader long-term security in Europe. The White House is now saying their focus has shifted from the minerals deal to discussing the long-term peace deal. The limited ceasefire now seems possible in our view, but the road to a sustainable peace is still a long and rocky one, not least because there is no consensus on any credible security guarantees for Ukraine.

Equities: Global equities ended higher yesterday, with the US leading advances, closing near the day's high and interpreting the Fed's message rather positively. With the VIX ticking lower, cyclicals outperforming alongside small caps, and positive stories surrounding the MAG 7, we are likely seeing more US retail investors engaging in the buy-the-dip strategy.

In Europe, there was a slight "sell the fact" movement, with Germany lagging behind after its stellar performance, where the DAX is up 17% year-to-date. In the US yesterday: Dow +0.9%, S&P 500 +1.1%, Nasdaq +1.4%, Russell 2000 +1.6%.

Asian markets are split this morning, with both China and Japan being lower, while most other markets are higher.

European futures are unchanged (DAX slightly lower), while US futures are higher, led by the tech sector, not least due to the ambitious investment stories circulating around Nvidia.

FI&FX: This week's bunch of central bank decisions kicked off with the BoJ and the Fed yesterday - both held interest rates unchanged. USD/JPY did not move on the BoJ decision but fell below 149 after US interest rates dropped in response to the slight dovish signals from the Fed. EUR/USD was steady around the 1.09 level. EUR/SEK rose above the 11.00 level again ahead of the Riksbank rate decision today.

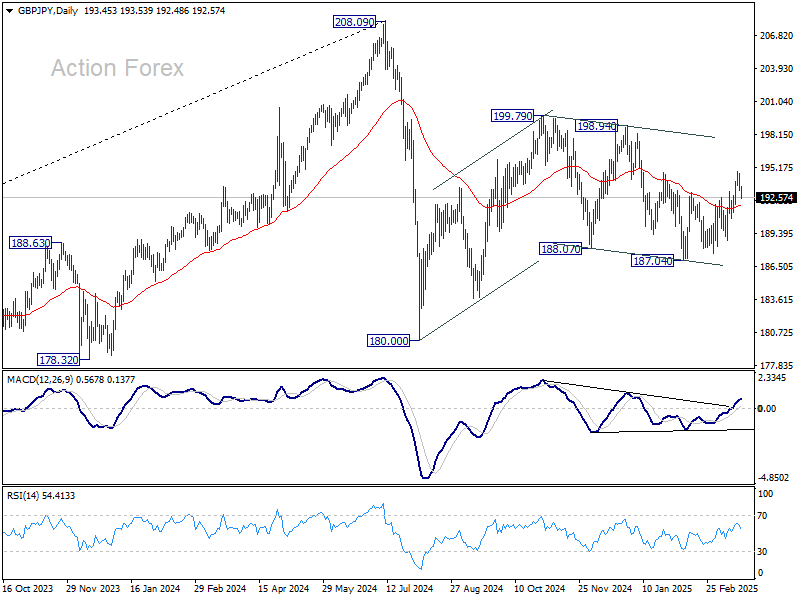

GBP/JPY Daily Outlook

Daily Pivots: (S1) 192.83; (P) 193.77; (R1) 194.29; More...

Intraday bias in GBP/JPY is turned neutral again with current retreat. On the upside, break of 194.89 will resume the rebound from 187.04 to 198.94/199.79 resistance zone. Nevertheless, break of 190.71 support will turn bias back to the downside for 188.77. Overall, corrective pattern from 208.09 is still in progress, with price actions from 180.00 as the second leg.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

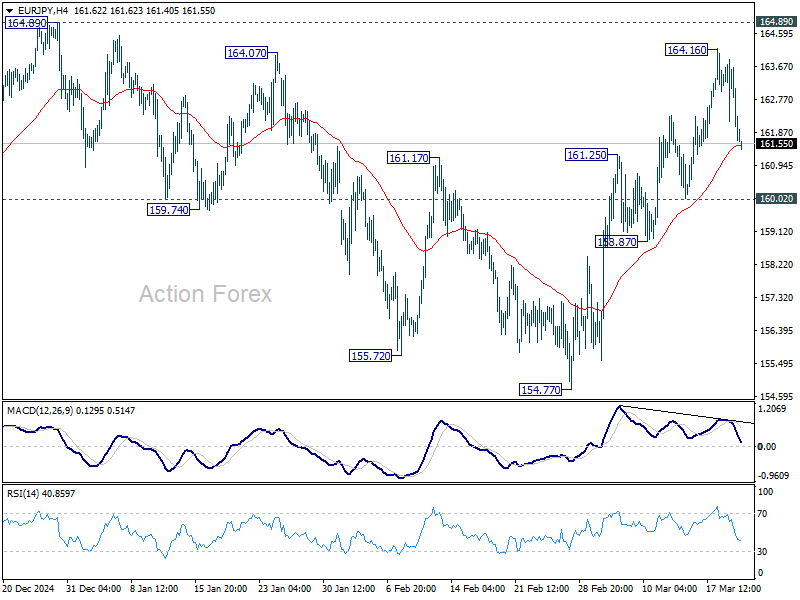

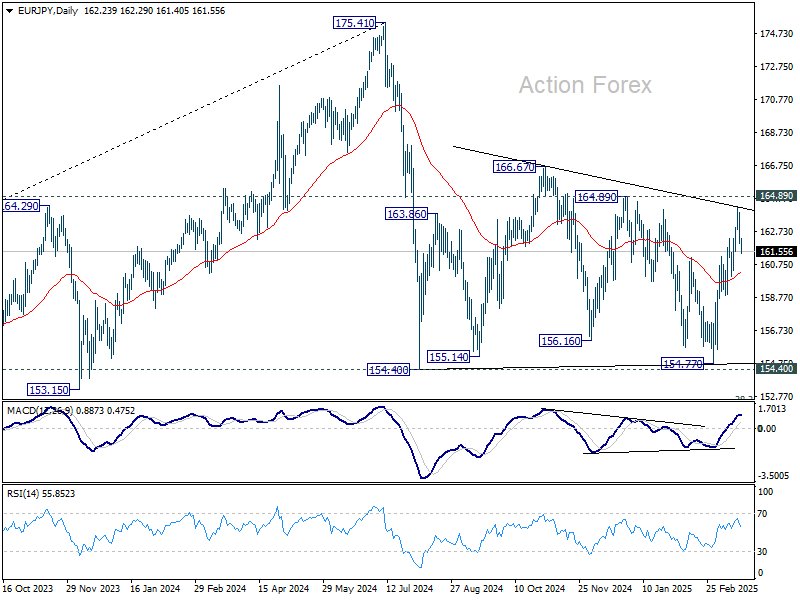

EUR/JPY Daily Outlook

Daily Pivots: (S1) 161.50; (P) 162.70; (R1) 163.32; More...

EUR/JPY reversed after hitting 164.16 and intraday bias is turned neutral first. For now, further rally is expected as long as 160.02 support holds. Above 164.16 will target 164.89 resistance. However, break of 160.02 will indicate short term topping, and turn bias back to the downside. Overall, sideway consolidation pattern from 154.40 is still extending.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

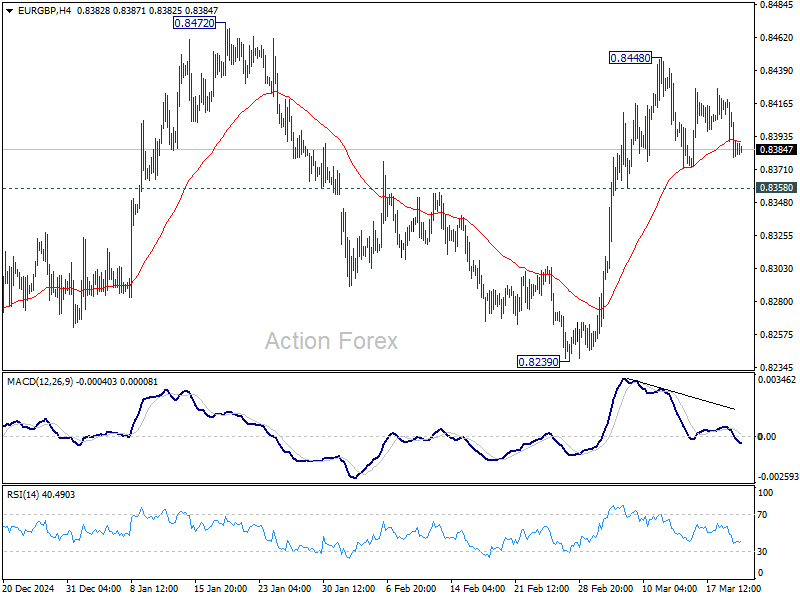

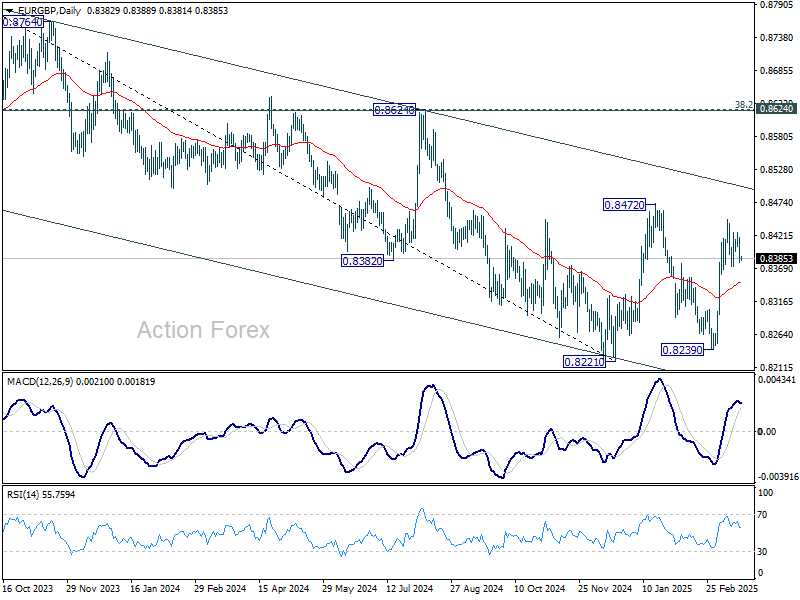

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8370; (P) 0.8395; (R1) 0.8410; More...

Range trading continues in EUR/GBP and intraday bias remains neutral. Further rally is expected as long as 0.8358 minor support holds. On the upside, break of 0.8448 will target 0.8472 resistance first. Firm break there will resume whole rebound from 0.8221 to medium term falling channel resistance (now at 0.8504). Nevertheless, break of 0.8358 will suggest that rise from 0.8239 has completed and turn bias back to the downside instead.

In the bigger picture, EUR/GBP is still bounded inside medium term falling channel. While rebound from 0.8221 might extend higher, it could still develop into a corrective pattern. Overall outlook will be neutral at best and down trend from 0.9267 (2022 high) could extend, at least until decisive break of channel resistance (now at 0.8508).

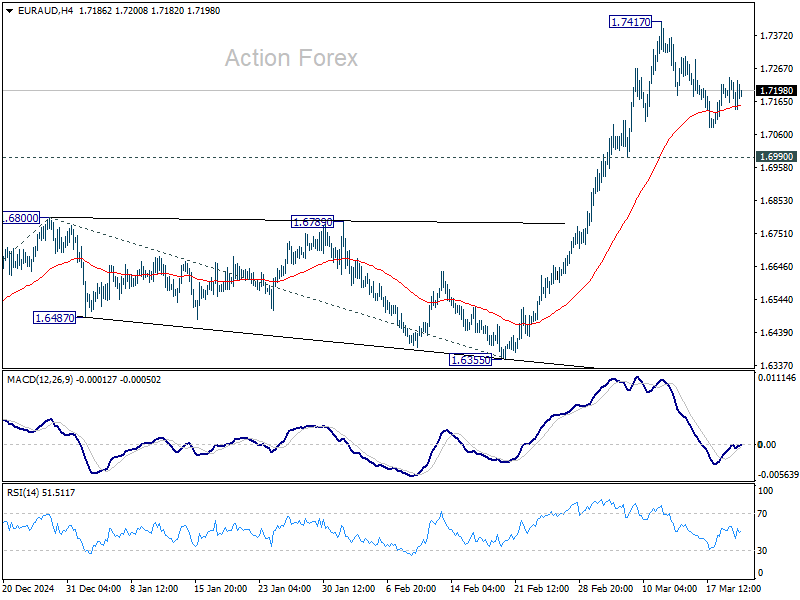

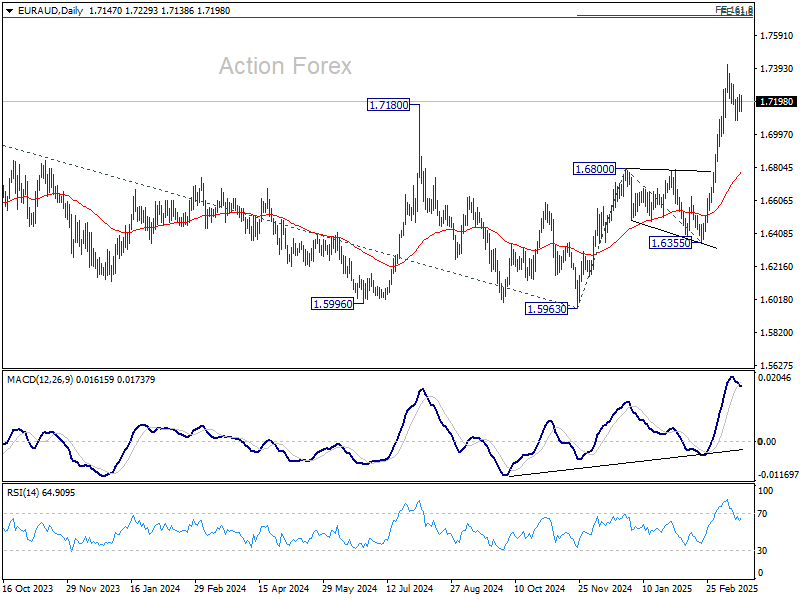

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7117; (P) 1.7179; (R1) 1.7212; More...

Intraday bas in EUR/AUD remains neutral as consolidation continues below 1.7417. Downside of retreat should be contained by 0.6990 support to bring rebound. On the upside, break of 1.7417 will resume rise from 1.6335 to 161.8% projection of 1.5963 to 1.6800 from 1.6355 at 1.7709 next.

In the bigger picture, the breach of 1.7180 key resistance (2024 high) suggests that up trend from 1.4281 (2022 low) is resuming. Sustained trading above 1.7180 will confirm and target 61.8% projection of 1.4281 to 1.7062 from 1.5963 at 1.7682, which is also close to 61.8% retracement of 1.9799 (2020 high) to 1.4281 at 1.7691. For now, this will remain the favored case as long as 1.6800 resistance turned support holds, even in case of deep pullback.

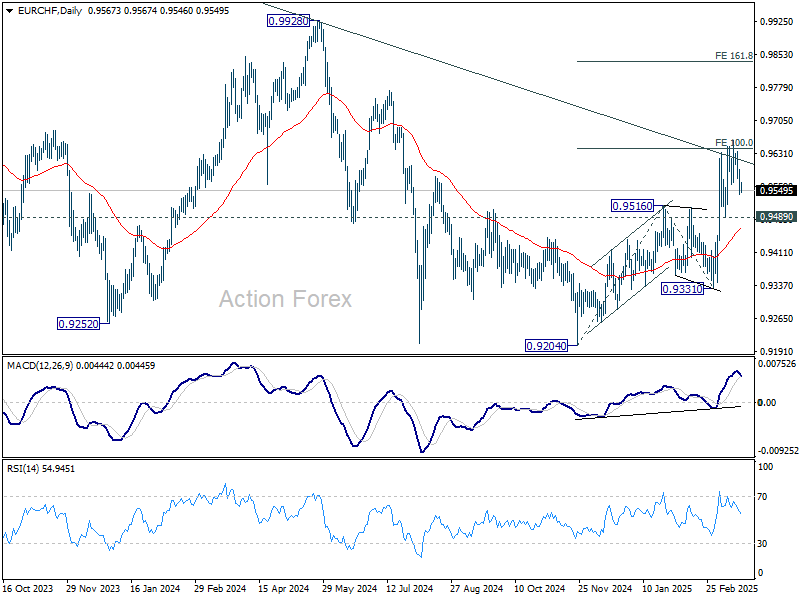

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9533; (P) 0.9577; (R1) 0.9611; More....

EUR/CHF is extending consolidations below 0.9660 and intraday bias remains neutral. Further rally is expected as long as 0.9489 support holds. Sustained trading above 100% projection of 0.9204 to 0.9516 from 0.9331 at 0.9643 will pave the way to 161.8% projection at 0.9836 next.

In the bigger picture, prior strong break of 55 W EMA (now at 0.9487) is a medium term bullish sign. Sustained break trading above long-term falling channel resistance (at around 0.9620) would suggest that the downtrend from 1.2004 (2018 high) has bottomed at 0.9204. Stronger rally should then be see to 0.9928 key resistance at least.

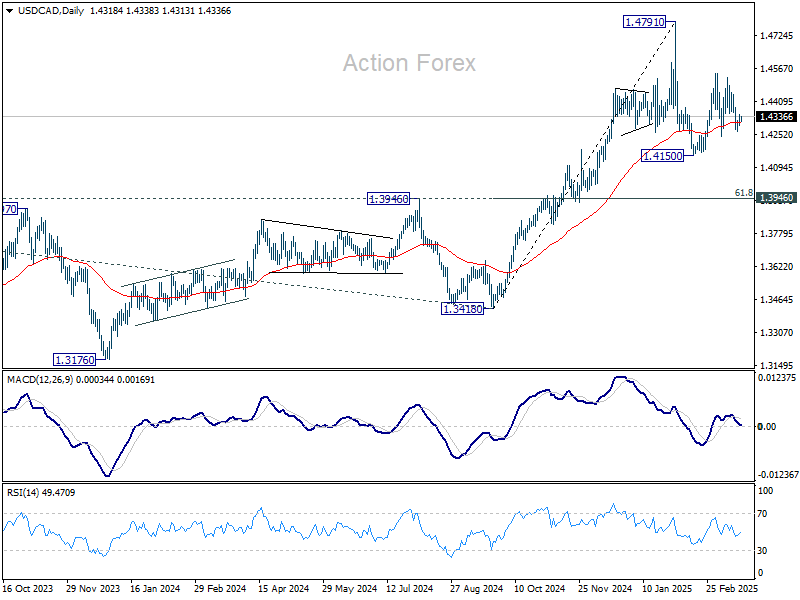

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4299; (P) 1.4324; (R1) 1.4352; More...

Range trading continues in USD/CAD and intraday bias stays neutral. On the downside, break of 1.4238 support will argue that corrective pattern from 1.4791 has started the third leg already. Intraday bias will be back on the downside for 1.4150 support and below. On the upside, though, break of 1.4541 will resume the rebound from 1.4150, as the second leg of the pattern.

In the bigger picture, long term up trend is tentatively seen as resuming with prior breach of 1.4667/89 key resistance zone (2020/2015 highs). Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. This will remain the favored case as long as 1.3976 resistance turned support holds (2022 high), even in case of deep pullback.

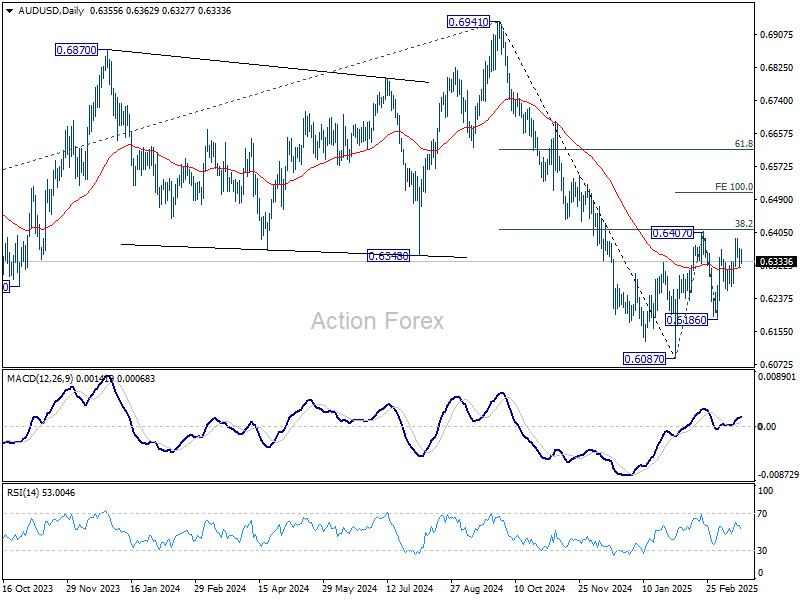

AUD/USD Daily Report

Daily Pivots: (S1) 0.6330; (P) 0.6348; (R1) 0.6376; More...

Intraday bias in AUD/USD stays neutral at this point. On the upside, sustained break of 0.6407 will resume the rebound from 0.6087 to 100% projection of 0.6087 to 0.6407 from 0.6186 at 0.6506, even still as a corrective move. On the downside, below 0.6268 will turn bias back to the downside for 0.6186 support.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6482) holds.

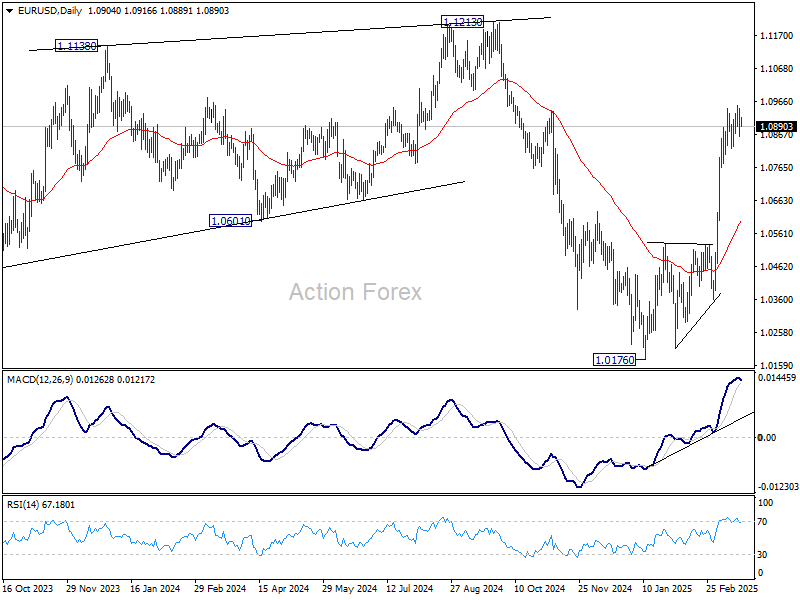

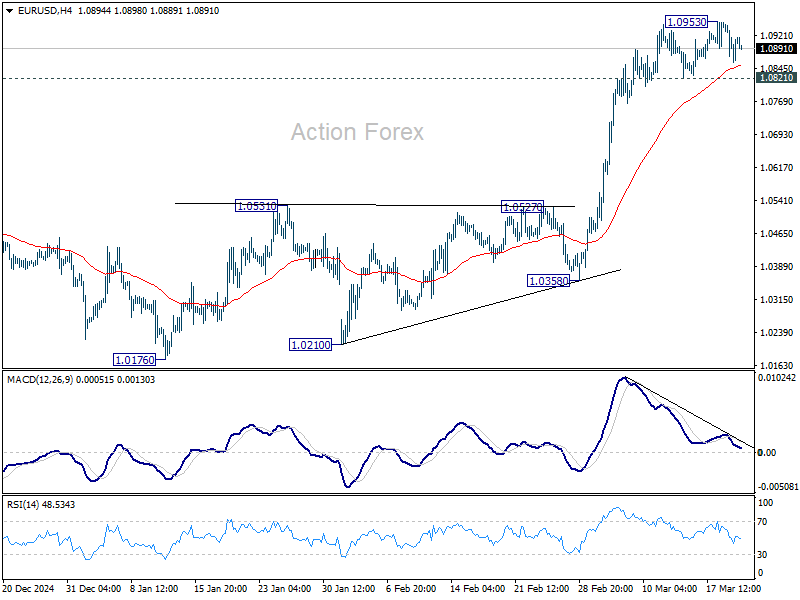

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0859; (P) 1.0904; (R1) 1.0948; More...

EUR/USD is staying in consolidations below 1.0953 and intraday bias remains neutral. Further rally is expected as long as 1.0821 support holds. On the upside, break of 1.0953 will resume the rise from 1.1076 to retest 1.1274 key resistance. On the downside, though, break of 1.0821 support will indicate short term topping, likely with bearish divergence condition in 4H MACD. That will turn bias back to the downside for deeper pullback.

In the bigger picture, prior strong break of 55 W EMA (now at 1.0675) suggests that fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 is still intact, and might be ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through a multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0531 resistance turned support holds.