Sample Category Title

First impressions: NZ GDP, December quarter 2024

New Zealand’s GDP rose by 0.7% in the December quarter, ahead of market forecasts. Seasonal issues are overstating the strength of the rebound, but there’s some genuine growth in there as well.

Key results

- Quarterly change: +0.7% (last: -1.1%, Westpac f/c: +0.5%, market f/c: +0.4%, RBNZ +0.3%)

- Annual change: -1.1% (last: -1.6%)

New Zealand’s GDP rose by 0.7% in the December quarter of 2024, providing some relief after steep consecutive declines of 1.1% in the two previous quarters. Revisions to recent history were minimal, with the September quarter being revised down slightly from -1.0%.

The December quarter result was ahead of our forecast of +0.5%, which in turn was at the higher end of the range of market forecasts (median +0.4%). We’d call this a genuine upside surprise, in the sense that the growth was driven more by real activity and less by the seasonal issues that we identified in our preview.

Sector-by-sector growth added up to around 0.3%, with better-than-expected contributions from a range of service sectors including healthcare, professional services, and art and recreation. The non-additive component remains an issue for the interpretation of this data though, adding 0.4% to the growth rate for the quarter.

On an annual basis, GDP was down 1.1% on the same time a year ago. Again, that was better than the -1.3% that we expected, and was an improvement on the -1.6% in the September quarter.

Implications

While the result was ahead of the RBNZ’s forecast, they have tended to downweight the GDP figures in recent times, due to the difficulty of interpreting its volatility and the extent of revisions – instead focusing on a range of higher-frequency indicators. That said, with the RBNZ’s most recent projections sitting somewhere between two and three more OCR cuts this year, these figures favour our view that it’s more likely to be two.

Dow Jones (DJIA), S&P 500 React to Fed Rate Decision

- The Federal Reserve kept interest rates steady but hinted at possible rate cuts later in the year.

- The Fed also expects slower economic growth and higher inflation.

- US stock indexes, including the Dow Jones and S&P 500, rose following the Fed's announcement.

- Technical analysis suggests the Dow Jones faces immediate support at 42000 and potential resistance at 42446 and 42764.

Wall Street Indexes continued their advance after the Federal Reserve kept rates unchanged. The central bank decided to keep interest rates steady at 4.25%-4.50% but suggested two small rate cuts might happen later this year, staying consistent with earlier predictions. The Fed also expects slower economic growth and higher inflation ahead.

Policymakers were divided on what to do next, showing uncertainty about how to address the impact of the Trump administration's policies.

The Fed also announced it would slow down the reduction of its large balance sheet. This comes as the central bank faces difficulties evaluating market conditions during a standoff in Congress over raising the government’s borrowing limit.

Source: LSEG

Summary of Fed Chair Powell's Comments

- Economy is strong, inflation remains "somewhat elevated"

- Tariffs have driven inflation expectations higher

- Fed is not "in a hurry" and will await further clarity

- If the labor market weakens, Fed can ease if needed

- If economy remains strong, policy restraint can be maintained

- Made technical decision to slow balance sheet decline

The Fed remains in "wait and see" mode.

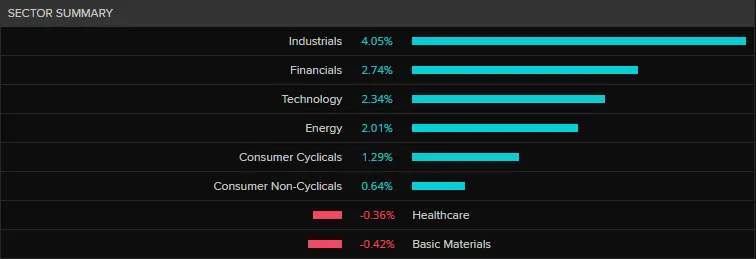

US Indexes had risen prior to the FOMC meeting with the meeting injecting some fresh liquidity and pushing all major indexes higher. The S&P 500 is trading up around 1.70% with the Dow Jones up around 1.47%.

From a sector perspective, Industrials were the big winners with gains of around 4.05% followed by Financials and Tech, with gains of 2.74% and 2.34% respectively.

Source: LSEG

Individual stocks on the move include Boeing with gains of around 7% followed closely by NVIDIA and American Express with gains of 3.2% and 3.3% respectively.

Technical Analysis - Dow Jones

From a technical standpoint, the Dow Jones has moved above a key area of resistance around the 42000 handle.

The question will be whether the daily candle will close above this handle which would hint at further upside. The Dow has had a slight pullback from the post FOMC highs and is currently flirting with support at the 42000.

The 14 period RSI is approaching the neutral 50 level with a break above further supporting the idea of a deeper recovery. A rejection of the 50 level may be seen as a sign that momentum still remains with the bears and could lead to a retest of recent lows.

Immediate support rests at 42000 before the 41400 and 41100 handles come into focus.

If the bullish momentum continues, immediate resistance rests at 42446 and 42764.

Dow Jones (US30) Daily Chart, March 19, 2025

Source: TradingView (click to enlarge)

Support

- 42000

- 41400

- 41100

Resistance

- 42446

- 42764

- 43402

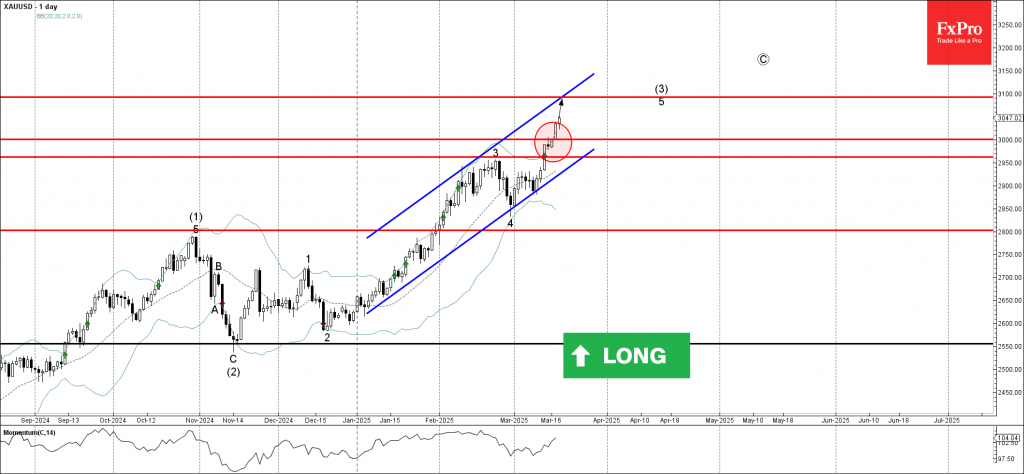

Gold Wave Analysis

Gold: ⬆️ Buy

- Gold continues daily uptrend

- Likely to rise to resistance level 3100.00

Gold rises sharply after breaking the resistance zone between the resistance 2956.00 (top of the previous impulse wave 3) and the round resistance level 3000.00.

The breakout of this resistance zone accelerated the active impulse wave 5 of the higher order impulse wave (3) from November.

Given the clear uptrend, Gold can be expected to rise to the next resistance level 3100.00 (target price for the completion of the active impulse wave 5).

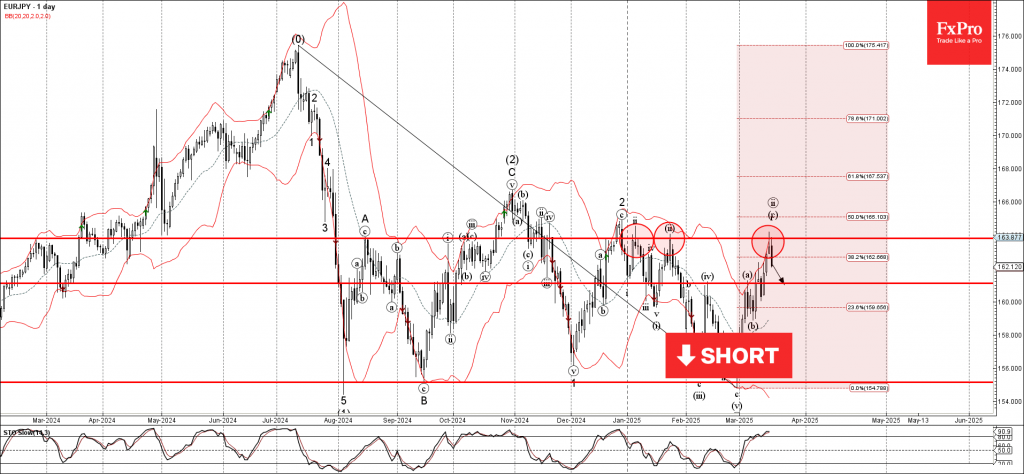

EURJPY Wave Analysis

EURJPY: ⬇️ Sell

- EURJPY reversed from resistance zone

- Likely to fall to support level 161.00

EURJPY currency pair recently reversed down from the resistance zone between the resistance level 163.80 (which has been reversing the price from January) and the upper daily Bollinger Band.

The downward reversal from this resistance zone created the daily Japanese candlesticks reversal pattern Shooting Star.

Given the overbought daily Stochastic, EURJPY currency pair can be expected to fall to the next support level 161.00.

FOMC Keeps Rates on Hold Amid Increased Uncertainty

Summary

- The FOMC voted unanimously today to keep its target range for the federal funds rate unchanged at 4.25%-4.50%. The Committee also decided to dial back the pace of quantitative tightening by allowing only $5 billion worth of Treasury securities to roll off the Fed's balance sheet every month.

- In a change from the last post-meeting statement, today's statement noted that "uncertainty around the economic outlook has increased," an apparent reference to the uncertain outlook for U.S. trade policy and the effects it may have on the economy.

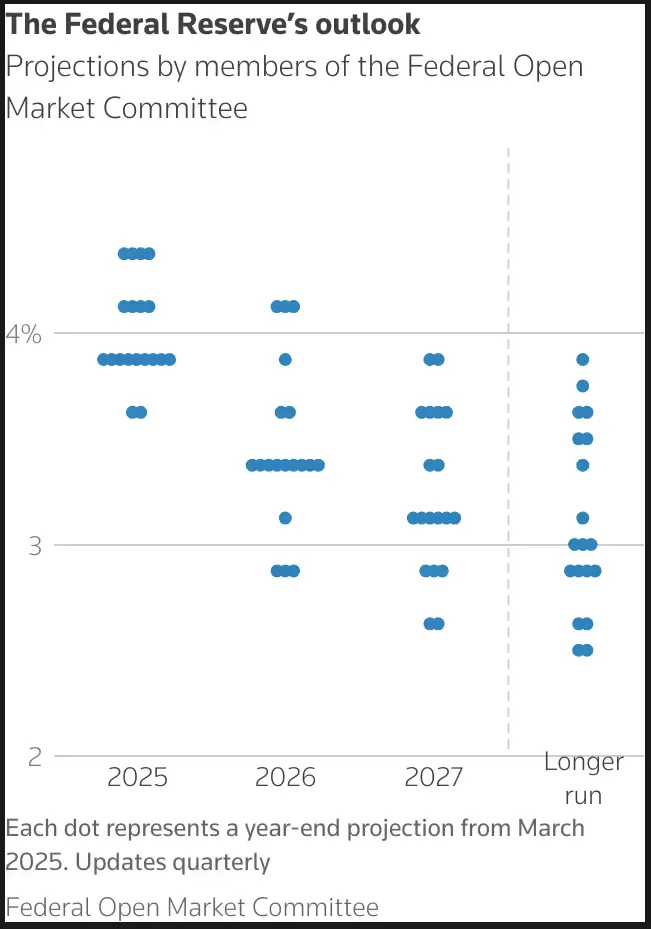

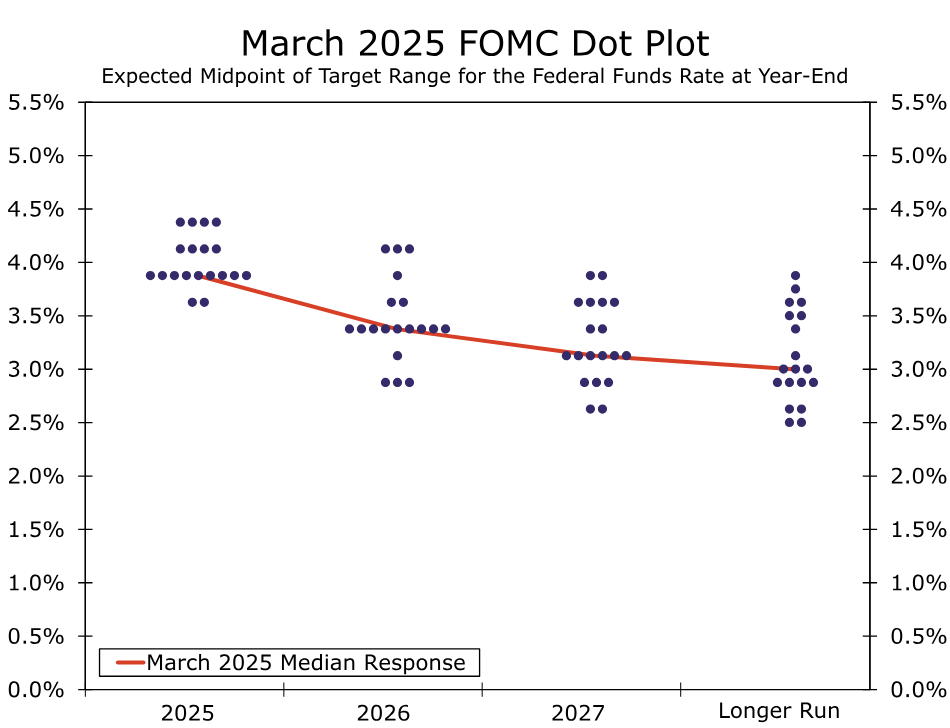

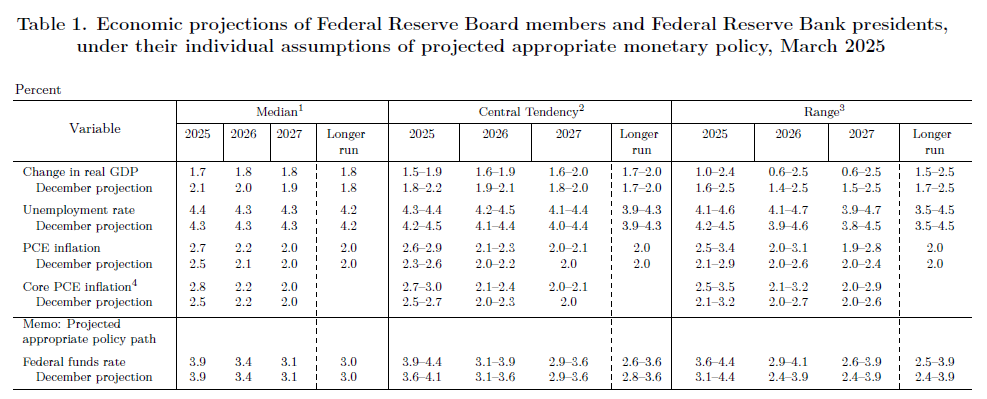

- The median GDP growth forecast for this year in the Summary of Economic Projections was downgraded while the core PCE inflation forecast was pushed higher.

- The median dot in the dot plot continues to look for 50 bps of rate cuts this year. However, there are now more FOMC members who think that less than 50 bps of easing would be appropriate than members looking for more than 50 bps of rate cuts.

- We look for 75 bps of easing by the end of the year, which we acknowledge is not a view that is currently shared by most FOMC members.

- If the economic slowdown that we forecast eventually leads the FOMC to place more weight on the "full employment" objective of its dual mandate than on its "price stability" objective, then we believe the Committee will ultimately conclude that lower rates are warranted and commence an easing cycle this summer.

FOMC Keeps Rates Unchanged While Dialing Back Pace of QT

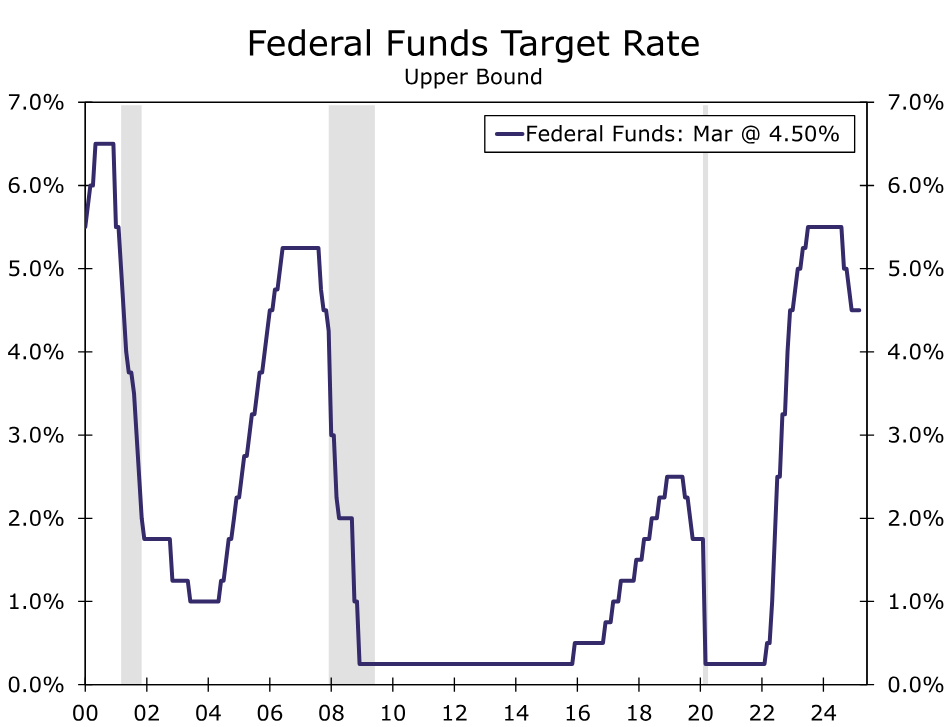

As universally expected, the Federal Open Market Committee (FOMC) held its target range for the federal funds rate unchanged at 4.25%-4.50% at its policy meeting today, a decision that was unanimously supported by all 12 voting members of the Committee. After cutting rates by a cumulative 100 bps at three consecutive policy meetings between September and December, the FOMC has now been on hold for the past two meetings (Figure 1).

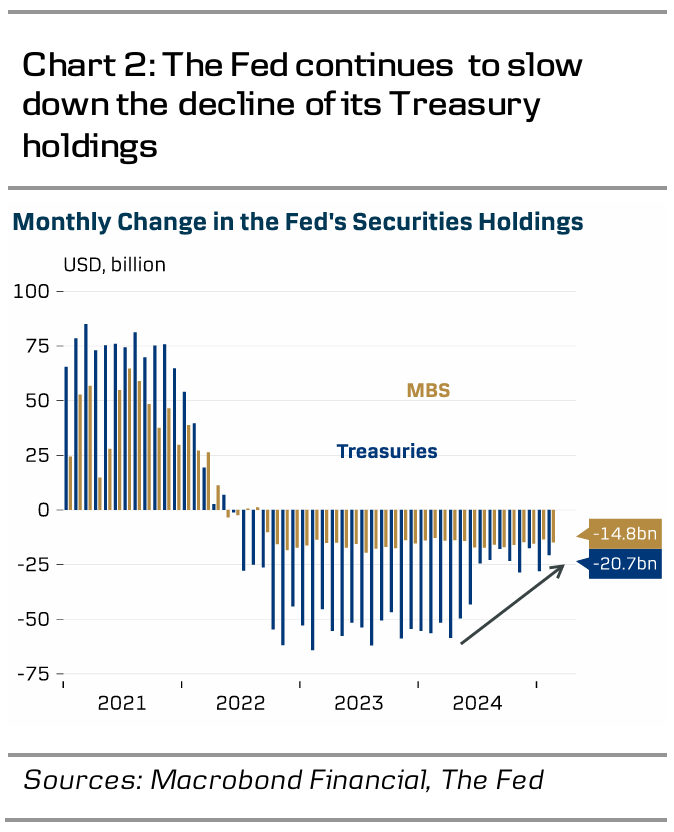

The FOMC also decided today to slow the pace of quantitative tightening (QT). Beginning in April, the Federal Reserve will allow only $5 billion of Treasury securities to roll off its balance sheet every month. Previously, the monthly cap was $25 billion per month. (The Fed will continue to allow up to $35 billion worth of mortgage-backed securities to roll off the balance sheet every month). Governor Waller, who wanted to keep the monthly cap for Treasury securities unchanged at $25 billion per month, dissented in the decision related to QT. As we discussed in detail in our most recent "Flashlight" report, technical considerations related to the looming debt ceiling decision may have played a role in the FOMC's decision to slow the pace of QT. That said, Chair Powell implied in his post-meeting press conference that the FOMC likely will not return to a faster pace of QT once the debt ceiling debate is resolved.

Heightened Uncertainty

In deciding to keep rates on hold today, the Committee continued to note in its post-meeting statement that "economic activity has continued to expand at a solid pace." The statement also continues to characterize inflation as "somewhat elevated." Indeed, the year-over-year change in the core PCE deflator, which most Fed officials believe is the best measure of the underlying rate of consumer price inflation, stood at 2.6% in January, above the FOMC's target of 2%. Notably, the Committee stated that "uncertainty around the economic outlook has (emphasis ours) increased," which likely is a reference to the uncertainty surrounding tariff policy. This heightened uncertainty appears to have led the FOMC to change its view of the balance of risks. Previously, the Committee judged "that the risks to achieving its employment and inflation goals are roughly in balance." Today's statement merely noted that "the Committee is attentive to the risks to both sides of its dual mandate." In short, it's difficult to assess where the balance of risks lie if the outlook for economic policy is considerably clouded.

We Look for Policy Easing Later This Year

The central bank also released the quarterly Summary of Economic Projections (SEP) that contains the Committee's macroeconomic forecasts. As we prognosticated in our recent "Flashlight" report, the median GDP growth forecast for 2025 was lowered from 2.1% in the December SEP to 1.7% while the median forecast for core PCE inflation was pushed up from 2.5% to 2.8%. In other words, the current SEP looks for a bit more stagflation in 2025 than the previous SEP, which was released in December. The median forecast in the so-called dot plot continues to look for 50 bps of rate cuts this year, although four FOMC members now think that only 25 bps of rate cuts will be appropriate this year while another four members think it will be appropriate to keep rates on hold all year. (Figure 2). In December, three members looked for 25 bps of rate cuts in 2025 while only one member thought it would be appropriate to refrain from easing this year.

We have a more dovish view of monetary policy in coming months than the collective FOMC. We forecast that the FOMC will reduce its target range for the federal funds rate by 75 bps by the end of the year. (Only 2 of the 19 FOMC members think it appropriate to cut rates by 75 bps by the end of 2025). As we discussed in more detail in our most recent U.S. Economic Outlook, our forecast is predicated on our assumption that the Trump administration will lift tariff rates meaningfully, with most trading partners retaliating, in coming months. Although the levies should cause only one-off increases in prices of tariffed goods, the resulting modest rise in inflation should only be temporary, at least in our view. Meanwhile, the negative hit to GDP growth likely will cause the unemployment rate to rise, which could remain elevated if policy remains restrictive. We do not know what individual FOMC members have assumed about trade policy in coming months. But if the economic slowdown that we forecast eventually leads the FOMC to place more weight on the "full employment" objective of its dual mandate than on its "price stability" objective, then we believe the Committee will ultimately conclude that lower rates are warranted and commence an easing cycle this summer.

That said, we agree with the FOMC's assessment that uncertainty regarding the economic outlook has increased, and we think it likely that the Committee will keep rates on hold again at its next meeting on May 7. The outlook for Fed policy clearly depends on the evolution of economic policy, especially trade policy, in coming months. In our view, the FOMC's near-term policy decisions will be dictated by incoming economic data.

Fed Review: Cautious Stability

- The Fed maintained its policy rates unchanged in the March meeting as expected.

- The Fed's balance sheet run-off (QT) will be tapered to USD5bn per month for Treasuries (prev. redemption cap USD25bn per month) starting from April, also in line with our expectations. MBS redemptions remain unchanged.

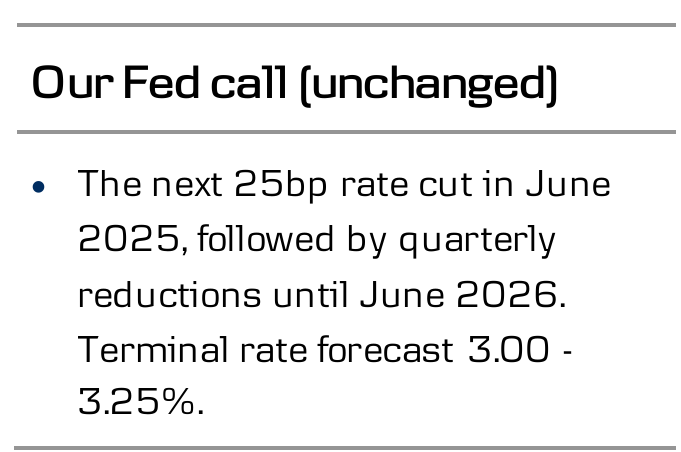

- Overall financial conditions eased modestly with UST yields declining across the curve, EUR/USD ticking higher and equities rising. We make no changes to our Fed call and still look for a total of three cuts in 2025 with the next one in June. Markets price 5bp for May, cumulative 20bp by June and 65bp by December.

The Fed's updated economic projections sparked an initial dovish reaction in the markets, as 2025 GDP forecast was taken down to 1.7% (from 2.1%). Inflation forecasts were revised up for both headline (2.7%, from 2.5%) and core (2.8%, from 2.5%). The widely followed median rate projection remained completely steady through 2025 -2027 and also the distribution of individual forecasts was little changed.

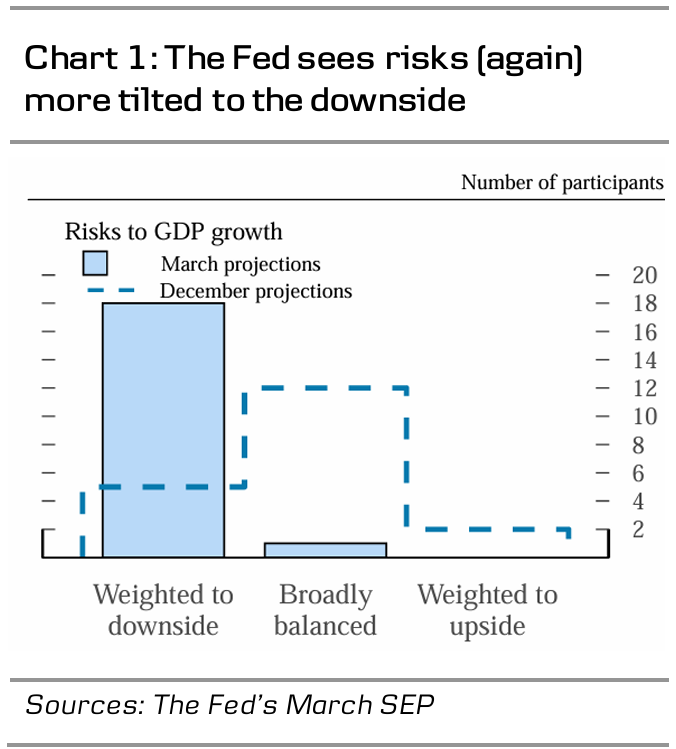

The relatively larger change was seen in the perceived balance of risks. Back in December, the risks around the GDP outlook were seen mostly as balanced, but now 18 out of 19 FOMC participants saw them as weighed to the downside. This was reflected in Powell's remarks as well, as he emphasized that the real economy remained solid both in terms of labour markets and consumer spending, but that the Fed remains mindful of the more cautious signals seen in soft sentiment indicators.

While Powell refrained from specifying how much the expectation of tariffs had influenced the inflation forecasts, he flagged that the 'base case' is still for tariffs to cause no persistent inflation. The Fed pays close attention to inflation expectations, but 'most' longer-term measures remain anchored near the target (with the Michigan survey as a notable 'outlier').

When asked about the possibility of a rate cut in May, Powell did not close the door, but mentioned several times that the Fed is not in a hurry to move. We still look for the next cut in June, followed by quarterly 25bp reductions until the terminal rate of 3.00-3.25% is reached in June of 2026. Our profile is close to market pricing for 2025, but our terminal rate assumption remains below market's expectations.

The Fed also announced tapering of the balance sheet run-off (QT) as we wrote in our Fed preview, 14 March, and RtM USD - Time to taper, 18 March. The redemption cap for Treasury holdings will be lowered to USD5bn per month from April (from USD25bn), while the redemption cap for MBS will be maintained unchanged at USD35bn. The cap on MBS has not been binding (redemptions have averaged USD15-20bn per month) and Powell signalled that the Fed has 'strong desire [for] MBS to roll off the balance sheet'. He flagged that the upcoming potential liquidity tightening due to the raise in debt ceiling and rebuild of Treasury cash balance sparked the debate for tapering QT, but also that the move fits well with the general idea of allowing the run-off to progress slower but longer. Reserves remain ample for now (and we agree) but the Fed sends a clear signal for the market not to worry about potential abrupt tightening of liquidity also going forward.

Fed holds rates, slows balance sheet reduction, downgrades growth outlook

As widely expected, FOMC kept interest rates steady at 4.25-4.50%. At the same time, Fed announced a key shift in its quantitative tightening strategy, stating that beginning in April, it will slow the pace of balance sheet reduction from USD 25B to USD 5B.

In its accompanying statement, Fed acknowledged that recent economic data continues to indicate "solid" expansion, with "low" unemployment and "solid" labor market conditions. Meanwhile, Fed noted that inflation remains "somewhat elevated", reinforcing the need for cautious policymaking.

The updated economic projections showed no change in Fed’s rate-cut outlook, with the median federal funds rate projection still pointing to just two cuts this year, leaving rates at 3.9% by the end of 2025. Looking further ahead, Fed continues to see rates at 3.4% by the end of 2026 and 3.1% by the end of 2027

Fed’s GDP growth forecasts were revised downward, reflecting growing concerns over economic headwinds. The US economy is now expected to grow by just 1.7% in 2025, down from 2.1% in the previous forecast, while 2026 and 2027 growth projections were also slightly trimmed to 1.8%.

Meanwhile, core PCE inflation projections for 2025 were revised higher, from 2.5% to 2.8%, suggesting that price pressures may prove more persistent than previously anticipated. However, core inflation forecasts for 2026 and 2027 remained unchanged at 2.2% and 2.0%, respectively, signaling confidence that inflation will gradually trend back toward the 2% target.

(FED) Federal Reserve Issues FOMC Statement

Recent indicators suggest that economic activity has continued to expand at a solid pace. The unemployment rate has stabilized at a low level in recent months, and labor market conditions remain solid. Inflation remains somewhat elevated.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. Uncertainty around the economic outlook has increased. The Committee is attentive to the risks to both sides of its dual mandate.

In support of its goals, the Committee decided to maintain the target range for the federal funds rate at 4-1/4 to 4-1/2 percent. In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage‑backed securities. Beginning in April, the Committee will slow the pace of decline of its securities holdings by reducing the monthly redemption cap on Treasury securities from $25 billion to $5 billion. The Committee will maintain the monthly redemption cap on agency debt and agency mortgage-backed securities at $35 billion. The Committee is strongly committed to supporting maximum employment and returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Michael S. Barr; Michelle W. Bowman; Susan M. Collins; Lisa D. Cook; Austan D. Goolsbee; Philip N. Jefferson; Adriana D. Kugler; Alberto G. Musalem; and Jeffrey R. Schmid. Voting against this action was Christopher J. Waller, who supported no change for the federal funds target range but preferred to continue the current pace of decline in securities holdings.

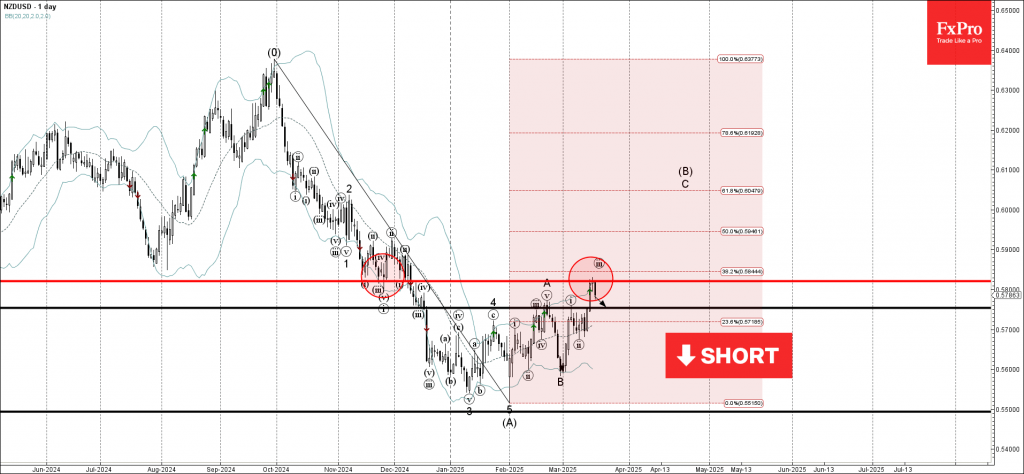

NZDUSD Wave Analysis

NZDUSD: ⬇️ Sell

- NZDUSD reversed from the resistance level 0.5820

- Likely to fall to support level 0.5750

NZDUSD currency pair recently reversed down from the strong resistance level 0.5820 (former strong support from the end of November).

The resistance level 0.5820 was strengthened by the upper daily Bollinger Band and by the 38.2% Fibonacci correction of the downward impulse from September.

Given the multi-month downtrend, NZDUSD currency pair can be expected to fall to the next support level 0.5750 (former support from February and the start of March).