Sample Category Title

Technical Outlook: GBPUSD – Downside Risk To Remain I Play While 20SMA Caps

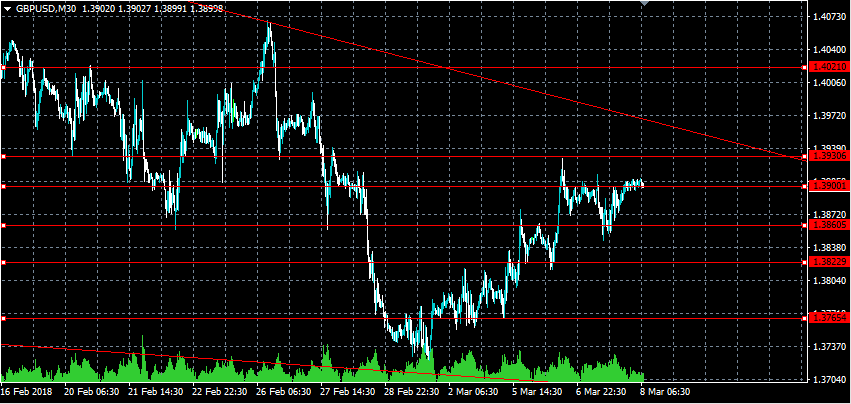

Cable shows hesitation ahead daily cloud top (1.3968) which marks key near-term barrier, as four-day rally stalled just under cloud top on Tuesday and Wednesday,s action ended in Doji, capped by 20SMA.

Trading in Asian / early European session is entrenched within tight range and remains capped by 20SMA (1.3910), generating negative signal.

Weak momentum studies on daily chart support scenario of fresh weakness on repeated upside failure, along with slow stochastic which approaches overbought territory.

Initial support at 1.3866 (10SMA) is under pressure and break lower would generate initial bearish signal for extension towards next pivot at 1.3823 (55SMA) and key supports at 1.3794/77 (Fibo 61.8% of 1.3711/1.3929 / daily cloud base).

Bullish scenario needs firm break above 20SMA to challenge daily cloud top and generate positive signal on break.

Res: 1.3910, 1.3929, 1.3960, 1.3996

Sup: 1.3866, 1.3823, 1.3794, 1.3777

Technical Outlook: EURUSD Holds In Tight Range Ahead Of ECB, Outlook Remains Bullish But Draghi’s Press Conference Closely Watched...

The Euro is holding within tight range around 1.24 handle in early Thursday's trading, awaiting the verdict from the ECB later today.

Near-term structure remains firm as 1.24 holds and despite yesterday's Doji candle, as the pair entered narrow range directionless mode ahead of two very important events, European central bank's rate decision, due later today and US Non-Farm Payrolls on Friday.

Recent break above pivotal 30SMA barrier at 1.2355, generated strong bullish signal which received confirmation on Wednesday's close above 1.2400. Bullish stance is expected to remain firm while the price holds above 30SMA and would look for test of targets at 1.2460 (Fibo 76.4% of 1.2555/1.2154 downleg, which was approached on Wednesday's spike to 1.2445 high) and 1.2493 (20-d upper Bollinger band).

Bullish daily techs remain supportive for further upside and favor dip-buying scenario while 30SMA holds.

ECB is in focus today and widely expected to keep rates unchanged, but traders will be looking for the comments from central bank's President Mario Draghi and expecting stronger hints about the ECB's steps in the near future.

Draghi faces tough job to compose central bank's statement in light of two key components: weak inflation and strong economic growth of the Euro bloc.

Res: 1.2415, 1.2415, 1.2460, 1.2493

Sup: 1.2384, 1.2354, 1.2339, 1.2317

USDJPY Hovers Around 106.00, Remains In Weak Sell-Off

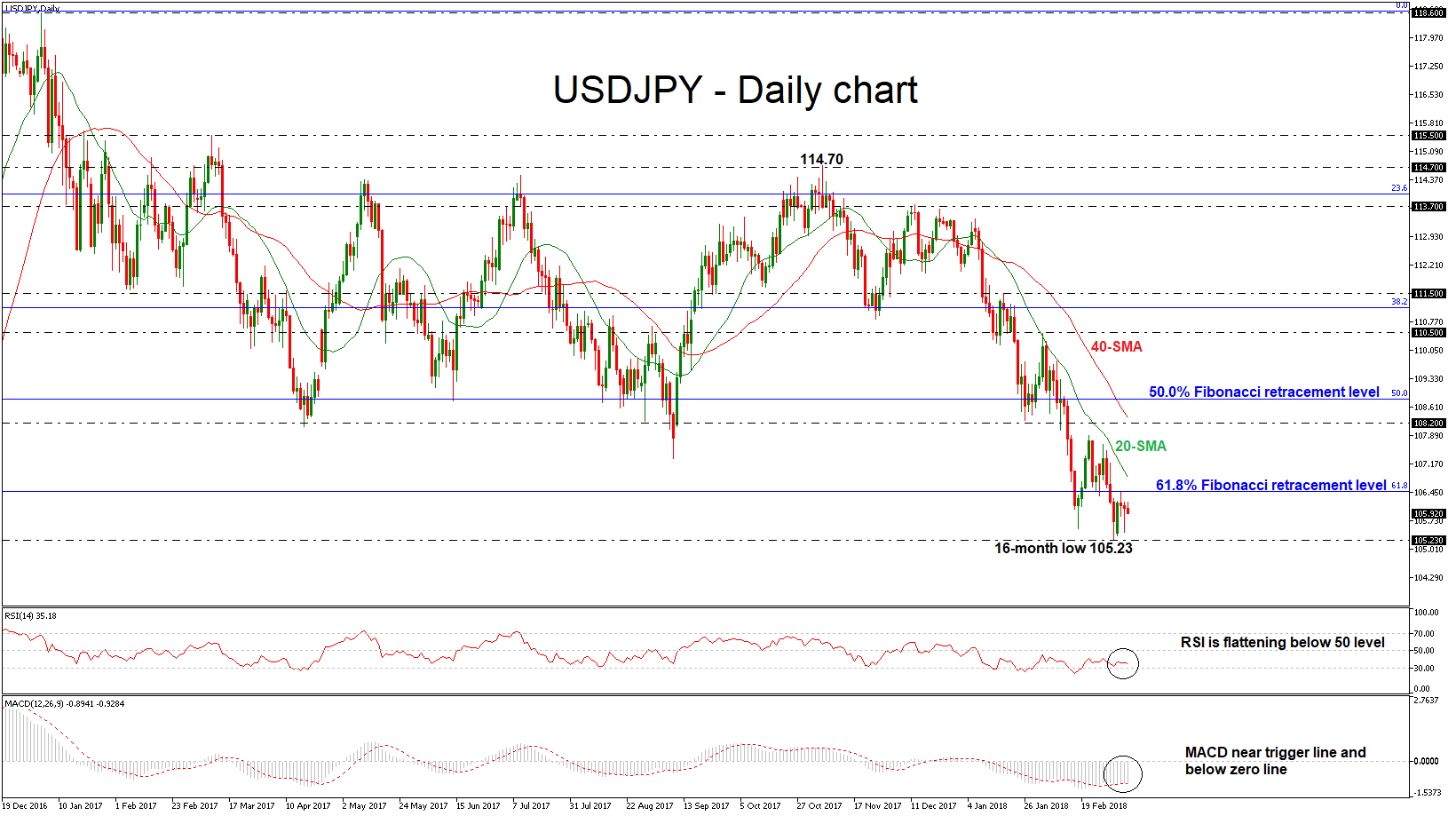

USDJPY is hovering around the 106.00 handle as it refused for the second day in a row to jump above the 61.8% Fibonacci retracement level at 106.47of the upleg from 99.00 to 118.60. When looking at the bigger picture the pair is creating a bearish trend as it slipped below the trading range within 108.20 – 114.70 in the previous weekly sessions.

In the daily timeframe, the price bounced off the 61.8% Fibonacci mark and the 20 and 40 simple moving averages are negatively aligned following the price action. The RSI indicator is flattening in the negative zone, while the MACD oscillator is holding near its trigger line. Technical indicators lack to show a clear signal.

If prices fall below the 16-month low of 105.23, there is scope to test the 101.00 strong psychological level taken from the low in November 2016. Before that, there are no any immediate support levels and the price could create a downside rally until the aforementioned obstacle.

On the flip side, a successful attempt above the 61.8% Fibonacci level, could shift the focus to the upside towards the 108.20 resistance level near the 40-SMA. However, the price needs to go through the 20-SMA. Further up, there is a resistance barrier at 50.0% Fibonacci mark near 108.80.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

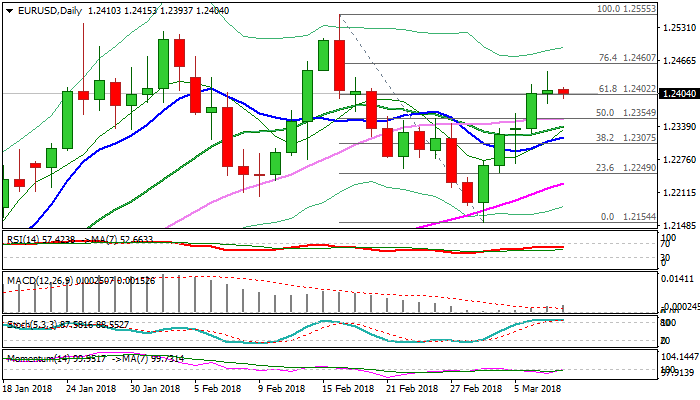

EUR/USD

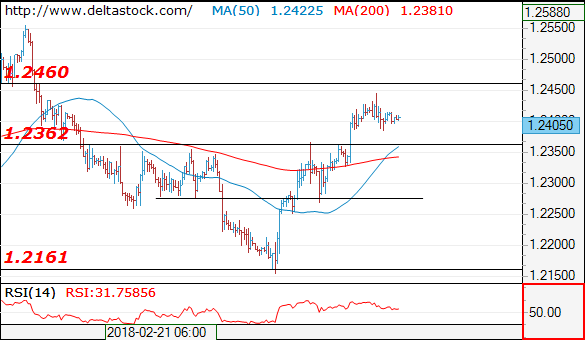

Current level - 1.2405

Intraday allow a corrective dip to 1.2360 before another leg upwards, to 1.2500.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2460 | 1.2460 | 1.2360 | 1.2160 |

| 1.2560 | 1.2560 | 1.2280 | 1.2090 |

USD/JPY

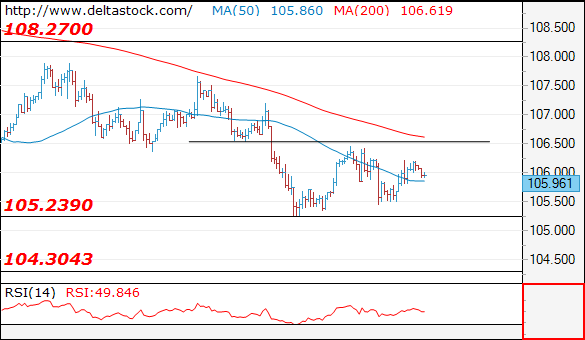

Current level - 105.96

The intraday bias is neutral within the 105.20-160.50 range and a break on the downside will challenge 104.30 and 102.40.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 106.50 | 108.30 | 105.20 | 105.40 |

| 107.60 | 110.40 | 104.30 | 102.40 |

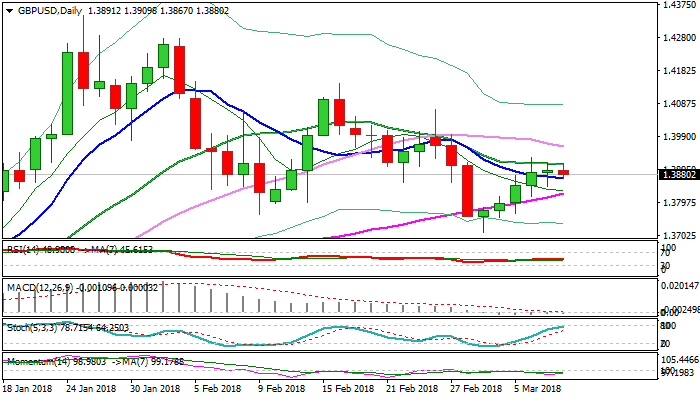

GBP/USD

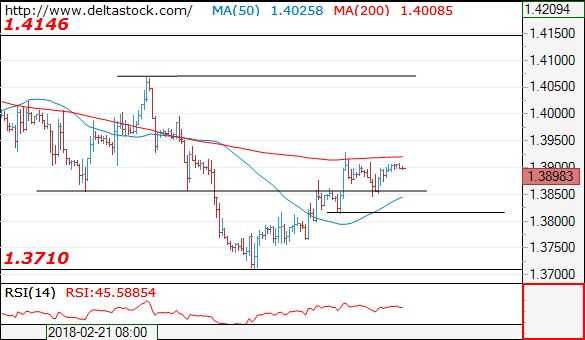

Current level - 1.3898

The uptrend is still intact, heading for a test of 1.3970 dynamic resistance. Initial support lies at 1.3850 and crucial on the downside is 1.3815 low, as a violation of the later will signal a slide towards 1.3620.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3930 | 1.4060 | 1.3860 | 1.3710 |

| 1.3970 | 1.4280 | 1.3815 | 1.3620 |

Sunrise Market Commentary

Markets

Yesterday, US Treasuries and German bounds opened in positive territory as angst for a trade war supported a modest a safe haven bid for bonds. However, gains evaporated as fears for on an escalation of the trade frictions eased after the White House signaled that import tariffs on steel and aluminum could be selective. In a daily perspective, changes in Treasury yields were less than 1 bp. This was also the case for German yields except for the 30-y (-3.4bp). Despite a cautious risk-off , 10-y intra-EMU spreads versus Germany mostly narrowed, Greece (-6bp) and Portugal (-4bp) outperforming; Ireland underperforming (0 bp). Today, the focus will be on the ECB policy decision and on US trade policy. The ECB will probably hold a cautious bias regarding policy normalization. The growth forecast will remain optimistic, but recent evidence doesn't provide a reason for an upward revision to the inflation forecast. Draghi might bring some minor changes in its communication, but probably stay vague on finishing the APP. Of late, Bunds outperformed Treasuries. The market probably already discounts a cautious ECB. In this context, any upticks in Bunds/decline in EMU yields might be modest. The rise in US yields eased recently, but bond gains were modest given the intense trade tensions. Will US yields resume the uptrend once the trade issue moves to the background? The Fed at least didn't give hints that recent developments will slow policy normalization.

Yesterday, EUR/USD and USD/JPY held tight ranges even as trade tensions intensified after Gary Cohn resigned as economic advisor of president Trump. The ADP labor market report showed job growth of 235 000 in the US private sector in February, but the dollar didn't profit. Both EUR/USD (1.2411) and USD/JPY (106.07) closed the session little changed. The trade debate and the ECB communication on monetary policy will probably also be the drivers for trading in the major FX cross rates today. We expect the ECB to hold a relatively soft tone on policy normalization, but we doubt that will be the trigger for a sustained euro decline. Easing trade tensions might gradually put a floor for the dollar. A combination of a more positive global context and strong US payrolls tomorrow (including wages) might create a more positive environment for the dollar.

Yesterday, sterling initially traded with a slight negative bias. The EU draft negotiation paper showed that the block isn't prepared the meet UK calls for a deep cooperation and free access to the EU market (including for financial services). EUR/GBP jumped temporary north of 0.8950. However, as was often the case of late, the Brexit noise again didn't change the broader picture in the EUR/GBP cross rate. The pair trades again in the 0.8925 area. This morning, the RICS house price balance was soft (0% vs 7% expected). There are no important UK eco data today. More technical trading in EUR/GBP might be in the cards.

News Headlines

US equities ended the session mixed/little changed. Indices reversed most of the initial losses as the White House indicated that countries including Canada and Mexico could be exempted from the steep tariffs on steel and aluminum. The easing of trade tensions also caused a relief rally on Asian markets this morning.

China February exports rose 44.5% Y/Y. Imports grew 6.3 percent. The data might be distorted by the timing of the Lunar New Year. Even so, combined data for January and February also showed a sharp rise in export growth. The widening in the trade surplus comes at a time when trade frictions between the US and China are mounting.

Japan's Q4 2017 GDP growth was upwardly revised to an annualised 1.6%, previously reported at 0.5% Q/Qa. Higher capital expenditure and a bigger contribution of inventories were the main drivers behind the revision.

Today, the eco calendar only contains second tier data in EMU. The US Jobless claims are expected to remain at a very low level (220 k). The ECB holds a regular policy meeting and president Daghi will give a press conference. Ireland will sell bonds.

ECB Interest Rate Decision, Canadian Housing Starts And US Initial Jobless Claims

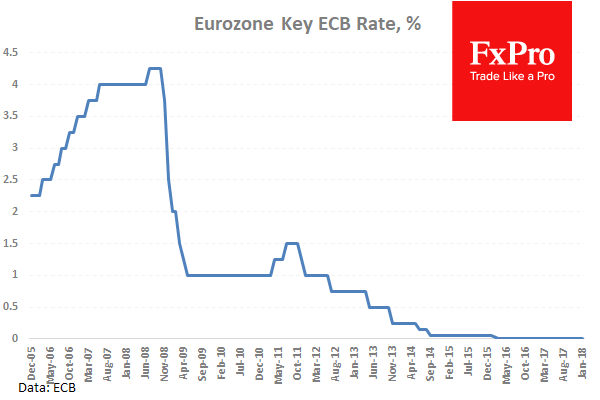

At 12:45 GMT, Eurozone ECB Deposit Rate Decision will be announced, with an expectation of -0.4% compared with a previous value of -0.4%. The ECB Interest Rate Decision will also be released at this time, with an expectation for rates to be left unchanged at 0%. This data could see volatility increase in EUR markets on the approach to the ECB Press Conference and Monetary Policy Statement at 13:30 GMT.

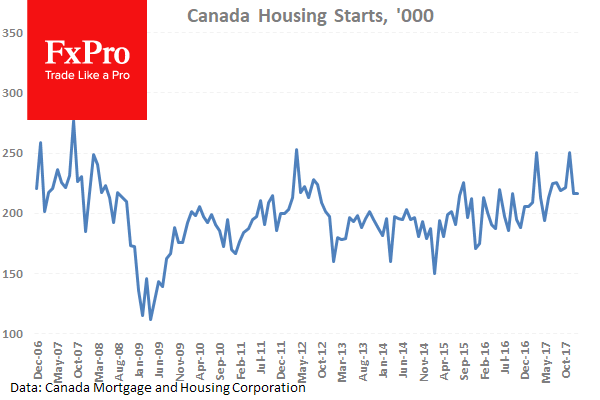

At 13:15 GMT, Canadian Housing Starts s.a. (YoY) (Feb) is expected to be 216.6K from 216.2K previously. This data may affect the CAD currency markets.

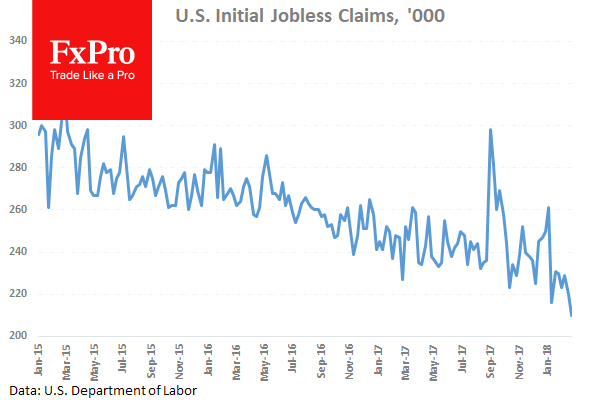

At 13:30 GMT, US Initial Jobless Claims (Mar 2) is expected to be 220K from 210K previously. Continuing Jobless Claims (Feb 23) is expected to be 1.921M from 1.931M previously. USD crosses could be moved by this data.

At 13:30 GMT, an ECB Press Conference and the Monetary Policy Statement will take place. This data may cause EUR pairs to increase in volatility. Comments from ECB President Mario Draghi will be assessed for hints on future monetary policy.

At 16:00 GMT, Canadian Gov Council Member Lane is due to speak about the March interest rate decision at the Vancouver Board of Trade. Audience questions are expected and any comments made may move CAD crosses.

At 16:00 GMT, Canadian Bank of Canada Governor Poloz is due to speak at the unveiling of the new $10 banknote, in Halifax. The text of the speech is due at the release time listed. The speech is scheduled to be delivered 15 minutes later and comments made may move CAD crosses.

Republican Lawmakers Express Concern Over Trump Tariff Proposals

The US Steel and Aluminium Tariffs remain centre stage today, as over 100 Republican Lawmakers signed a letter sent to the President expressing concern about the proposals. The White House is in the process of formalizing the tariffs, with the President expected to sign as early as Thursday evening and the tariffs coming into effect in 15 to 30 days. One ray of light comes in the form of reports that suggest a clause could exempt Canada and Mexico from the tariffs and that the exemption may also be extended to other key allied nations. Markets rallied yesterday, as traders bought the dip, following the plunge associated with the resignation of Chief Advisor Gary Cohn in opposition to the tariffs.

Eurozone Gross Domestic Product s.a. (QoQ) (Q4) was as expected, unchanged at 0.6%. Gross Domestic Product s.a. (YoY) (Q4) was also as expected, unchanged at 2.7%. This data release caused the EURUSD pair to move higher from 1.24208 to 1.24445. The QoQ number has been holding steady around 0.6% since 2017, showing stable growth across the Eurozone.

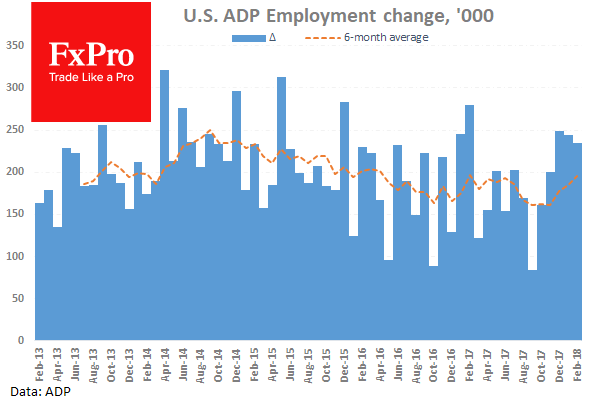

US ADP Employment Change (Feb) was 235K v an expected 195K, from 234K previously, which was revised up to 244K. This data point had been holding steady at around the 200 mark for much of 2017, with extremes at 300 above and 130 below over the course of the year. The data has remained above 100 since November of 2011, showing that the US jobs market is robust and performing steadily. The current result beats expectations and is largely in-line with the January result, showing a revision higher. USDJPY moved higher from 105.806 to 105.982 after this data was published.

US Fed’s William Dudley spoke about the economic impact of the 2017 hurricanes, in San Juan. Audience questions followed and he commented on the current trade issues saying that trade barriers impede the focus on comparative advantage.

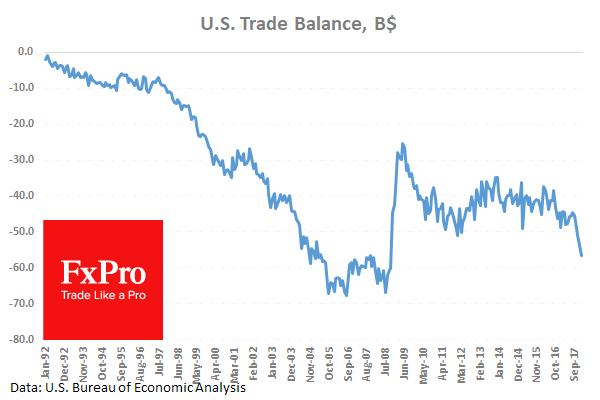

US Trade Balance (Jan) was $-56.6B v an expected $-55.1B, from a previous $-53.1B, which was revised up to $-53.9B. Unit Labor Costs (Q4) was 2.5% v an expected 2.1%, against a prior reading of 2.0%. Nonfarm Productivity (Q4) was 0.0% v an expected -0.1%, from -0.1% previously. The US Trade Balance is what much of the current global market uncertainty is based around. While this number is not generally a market mover, it will be watched for a change in trend if new trade policies are implemented. This data is then viewed over a longer period of time with any one data point largely irrelevant. The reaction to this data today was for USDJPY to slip lower to 105.786.

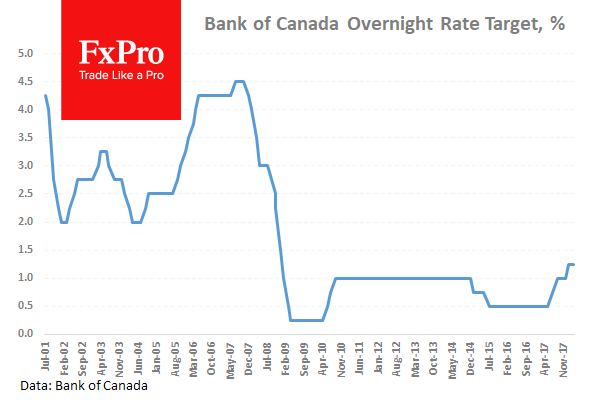

The Bank of Canada Rate Statement was released along with the Interest Rate Decision, remaining unchanged, as expected, at 1.25%. The statement was largely in line with expectations: higher rates likely warranted over time, but some continued policy accommodation will likely be needed to keep economy close to potential and inflation on target. Trade developments are an important and growing source of uncertainty but global growth is solid and broad-based. The core inflation measures have edged up, which is consistent with an economy operating near capacity. Wage growth has been firm but lower than typical in an economy with no labour market slack. USDCAD moved higher from 1.29035 to reach 1.30000 resistance.

US Consumer Credit Change (Jan) was $13.91B v an expected $17.90B, against a previous $18.45B, which was revised up to $19.21B. This data showed a drop in the amount of consumer credit outstanding, suggesting a slower rate of spending, with credit card spending up only 0.8% from 7.2% in December. Loans rose 5.6% in January, following an increase in December. This can be explained do to the surge in credit following a severe hurricane season, where property had to be replaced and repaired.

EURUSD is down -0.09% overnight, trading around 1.24000.

USDJPY is down -0.07% in early session trading at around 105.987.

GBPUSD is down -0.04% this morning, trading around 1.38882.

USDCAD is down -0.14%, trading around 1.28924.

Gold is up 0.19% in early morning trading at around $1,328.00.

WTI is down -0.23% this morning, trading around $61.12.

Euro’s pre-ECB retreat just shallow

Euro trading generally lower today ahead of ECB. But it's clearly just paring some of this week's gain as traders turn cautious. EUR remains the strongest one for the week and the month. And over the last four hours, it has indeed regained some ground, showing that the retreat is rather shallow.

There is only one important thing to note today, whether ECB will change forward guidance and drop easing bias. We believed that ECB won't do anything today and leave the options for June meeting. There are just too many uncertainties out there, including US trade tariffs and Brexit negotiation. ECB will keep the open to extend the EUR 30b a month asset purchase program after September.

There is only one important thing to note today, whether ECB will change forward guidance and drop easing bias. We believed that ECB won't do anything today and leave the options for June meeting. There are just too many uncertainties out there, including US trade tariffs and Brexit negotiation. ECB will keep the open to extend the EUR 30b a month asset purchase program after September.

Here are some suggested readings on ECB:

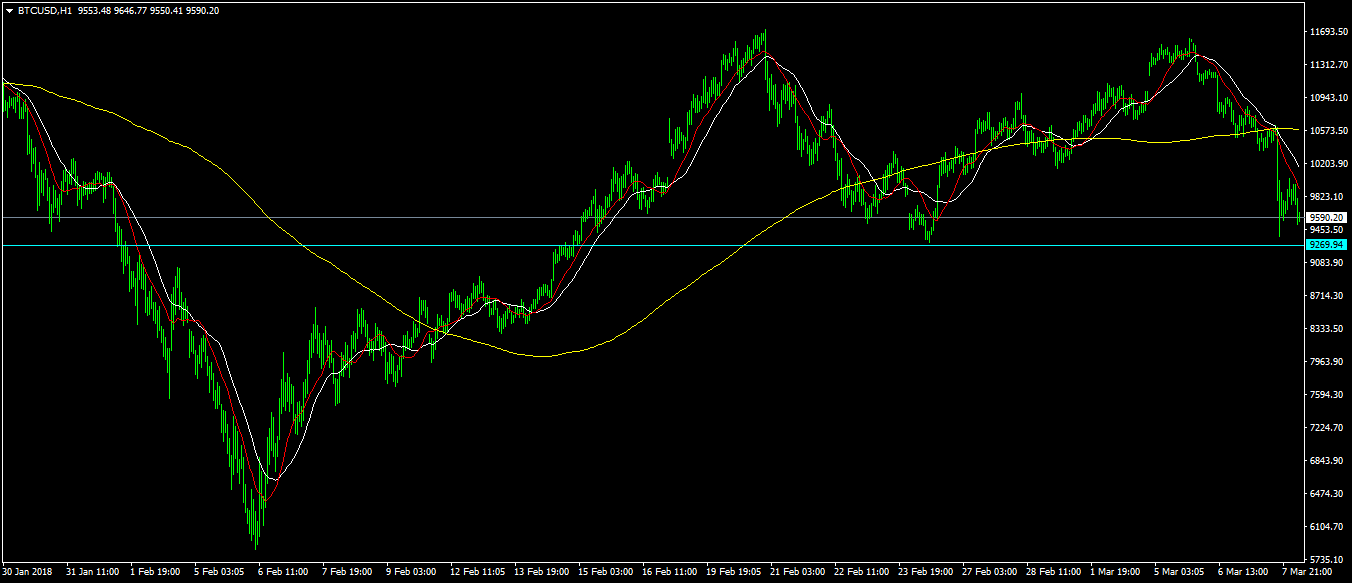

Bitcoin Falls After Sec Annoinces New Regulations For Cryptocurrencies Exchange

Yesterday, Bitcoin fell by more than 10% after SEC announced that all cryptocurrencies exchanges need to be registered. As of this writing, Bitcoin is trading below the crucial $10,000.

In a statement, the Securities and Exchange Commission said that bitcoin and other cryptocurrencies should be considered as financial assets which lie under its mandate.

The announcement came a few weeks after the SEC and CFTC met with law makers to discuss the cryptocurrencies industry and how to regulate it. In the meeting, the two agencies promised to come up with regulations to make the industry more vibrant and to protect the end users.

However, traders should take the move by the SEC positively. This is because, the industry could be more vibrant when more people have faith in it. Recently, the SEC has issued several subpoenas to exchanges in its attempt to establish better controls.

Bitcoin is currently trading at $9,575. As shown below, in recent weeks, the BTCUSD pair has created a near-perfect support and resistance trend. This means, that the pair could drop to the $9,270 level before starting an upward trend.

GBPUSD Bullish Bias Intact Above 1.3960

The British pound continues to consolidate around the 1.3900 handle against the greenback on Thursday, as traders remain cautious ahead today’s key European Central Bank policy meeting. The GBPUSD pair earlier failed to hold above its monthly pivot point, located at 1.3920, as the U.S dollar index recovered slightly. With a lack of upcoming macroeconomic data from the United Kingdom, sterling traders are likely to focus on a break of the recent narrow trading-range between the 1.3860 and 1.3930 levels.

The GBPUSD pair is intraday bullish whilst trading above the 1.3860 level, key upside targets remain 1.3970 and 1.4021.

Should the GBPUSD pair trade below the key 1.3860 support level for a sustained period, price-action will likely turn bearish and move towards the 1.3822 and 1.3765 levels.