Sample Category Title

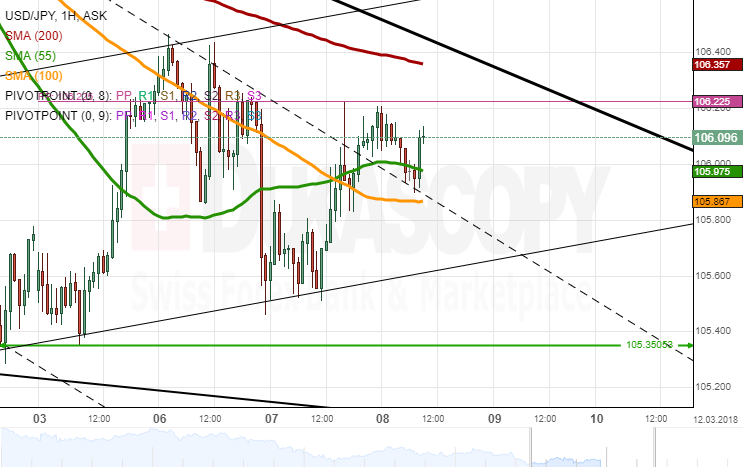

USDJPY Analysis: Forms Junior Pattern

Following a reversal from the 105.50 mark during the first part of Wednesday, the US Dollar gathered enough momentum to dash through the 55– and 100-hour SMAs and the upper boundary of a two-week descending channel.

This movement resulted in the formation of another junior pattern which is steadily guiding the rate towards the senior channel and the 200-hour SMA near 106.25. It seems that the bullish sentiment is starting to strengthen, thus sending the pair away from the 2017 low of 105.35. The guidance of the 55– and 100-hour SMA might also help the pair to edge higher within the following trading session.

Thus, the base scenario favours the Greenback moving in line with the newly-formed channel towards 106.70. The nearest resistance is likely to hinder the pair circa 106.25 today.

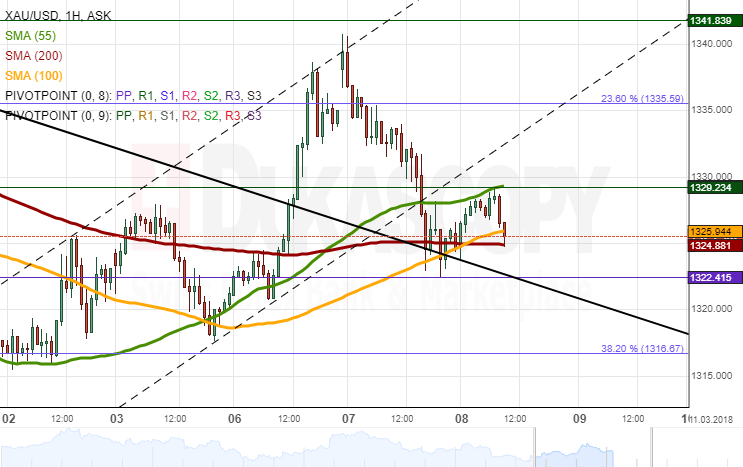

XAUUSD Analysis: Ready To Break Out Soon

Downside risks dominated the yellow metal on Wednesday, as it closed the session with a 1.09% drop against the US Dollar. As a result, the pair breached the short-term ascending channel and subsequently rebounded from the upper boundary of a senior pattern circa 1,324.00.

The morning session was spent relatively calm within the bounds of the 55- , 100– and 200-hour SMAs. Given that the northern barrier is likewise reinforced by the monthly PP, traders might be reluctant to form significant advances during the following sessions. Technical indicators are more in favour of a fall that would guide the rate back into the breached channel and towards the 38.20% Fibo retracement at 1,316.67.

In case the opposite occurs, the pair is likely to be restricted by a two-week resistance in the 1,340.00 area.

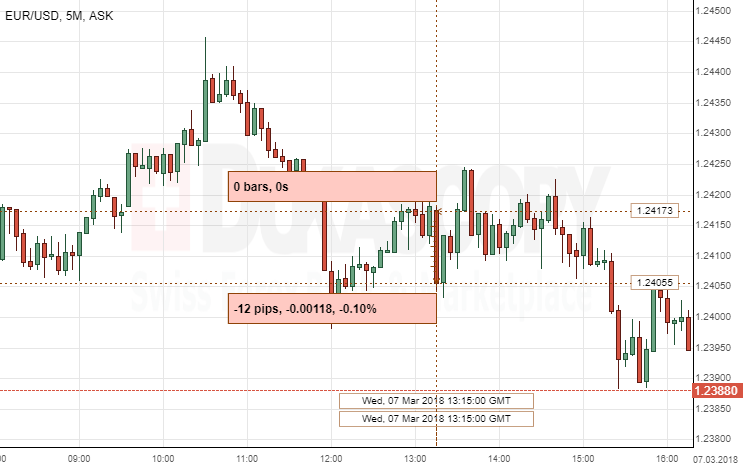

EUR/USD: US ADP Non-Farm Employment Change

The Greenback rose against its European counterpart following the release of the ADP report on non-farm payrolls for February. The EUR/USD pair lost 12 base points, or 0.10%, reaching the 1.2405 level, to be seen returning back to the 1.2415 area later on.

The US private sector created 235K jobs in the reported month, expanding at a slightly slower pace than in January. At the same time, US non-farm employment change number still surpassed the February's forecast. Ahu Yildirmaz, the Vice President and Co-head of the ADP Research Institute, said that the US labor market is keeping its growth rate uninterrupted and that persistant gains have been seen in industries related to leisure, hospitality and retail.

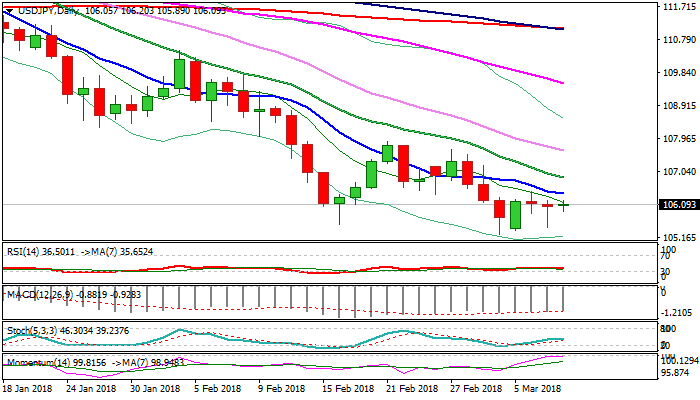

Technical Outlook: USDJPY – Directionless Mode Expected Ahead Of Friday’s Key Releases

The pair trades in extended directionless mode on Thursday, following strong rejections on both sides in past two days.

Recovery attempts were capped by Fibo barrier at 106.44 on Tuesday, while bearish acceleration was strongly rejected on Wednesday, leaving long-tailed Doji and sidelining immediate downside risk.

The pair is expected to remain within congestion, ahead key events on Friday, BoJ interest rate decision and US NFP data, which could provide fresh direction signals.

The upside is expected to remain limited by 10SMA / Fibo 23.6% of 110.28/105.24 at 106.44, with stronger upticks to be capped by falling 20SMA at 106.85.

Overall picture remains bearish and favors fresh weakness after consolidation, with Friday's releases expected to be the main driver.

Res: 106.22, 106.44, 106.85, 107.20

Sup: 106.20, 105.45, 105.24, 105.00

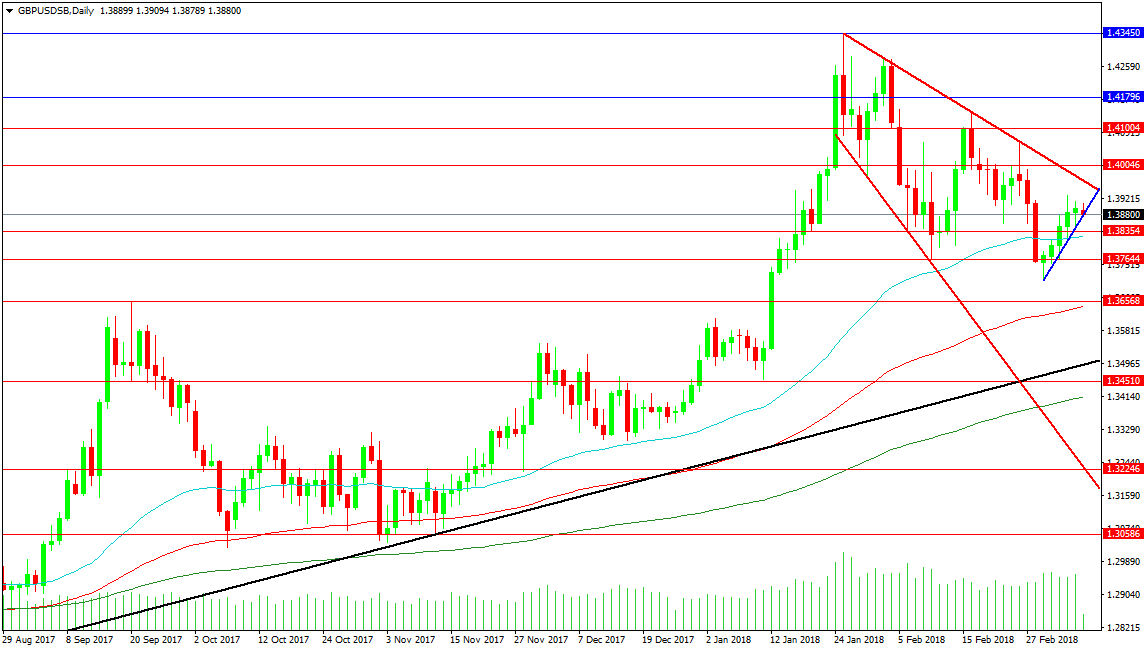

Forex Analysis: GBPUSD And EURCAD

The GBPUSD pair has formed a descending wedge pattern, with the top of the pattern at 1.39608, just below the 1.40000 level. This level has seen price consolidate around it since the end of January. Resistance can be found above the pattern at 1.40046, with touches on the trend line at 1.40695 and 1.41443 centred on the 1.41000 round number level. Higher levels of resistance can be seen at the 1.41796 level, with an intermediate high at 1.42776 and the 2018 high at 1.43450.

Support is located at 1.38354 and the 50-period MA at 1.38245, with the 1.37644 level a low from early February. The September 2017 high is found at 1.36568, close to the rising 100 DMA at 1.36447. The major rising support trend line, shown on the chart in black, is climbing closer to the 1.35000 level, with the 1.34510 level close by and the 200 DMA rising at 1.34115.

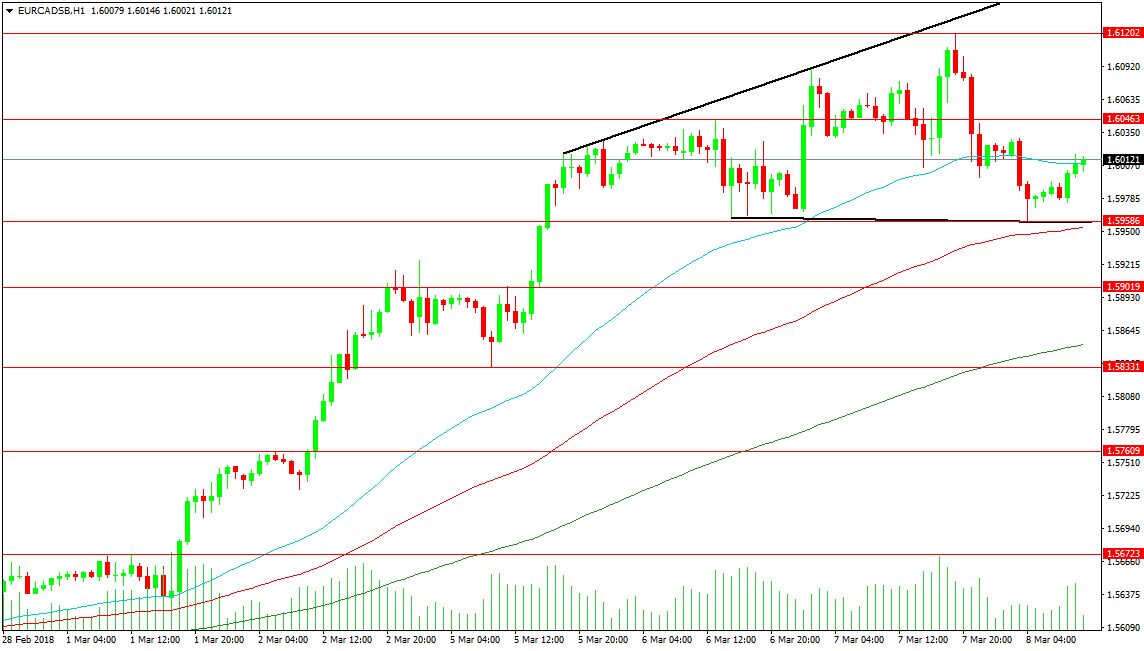

EURCAD

EURCAD

This pair is currently consolidating around 1.60000 and using the 50-period MA on the 1-hour chart. Resistance comes in at 1.60463, with the 1.61202 area as the high from recent market price action. The price is holding above 1.59586 and trend line support, with the 100-hour MA at 1.59535. A drop below this area would create another lower low and target support at 1.59019, followed by the 200 DMA at 1.58530 and 1.58331. Below this area, there is a gap in support until 1.57609. The 1.57000 level can be targeted in extension, with the 1.56723 close below.

Should the current price action form a Head and Shoulders pattern, traders would aim for a target around 1.58000, on the condition of a break below the 1.59500 area once the right shoulder is formed.

Dollar Recovers From 2-Week Low As Trade Concerns Ease, ECB Decision Looms

Here are the latest developments in global markets:

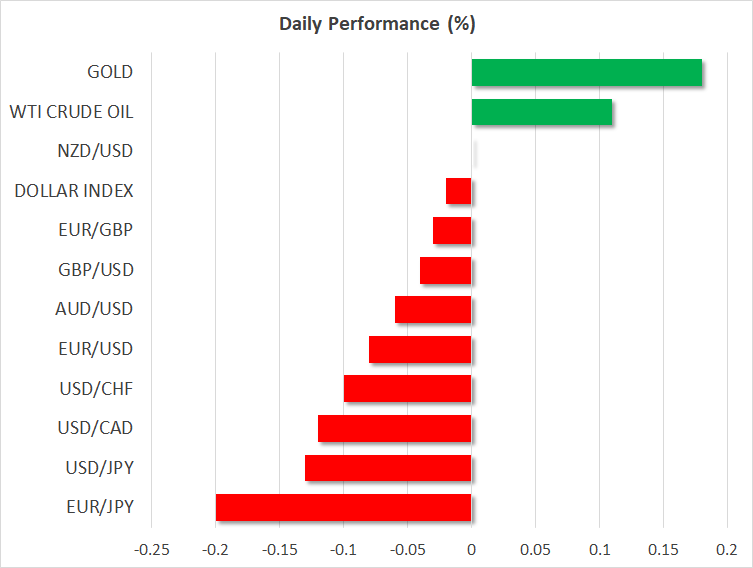

FOREX: The dollar was roughly flat versus a basket of currencies after recovering somewhat from a two-week low hit on Wednesday. The recovery came on the back of abating worries over a trade war occurring, as well as optimism on the strength of the US labor market.

STOCKS: US markets traded in a turbulent manner yesterday. They opened lower on trade concerns following Gary Cohn’s resignation, but managed to recover most of their losses before the close, after news that Canada and Mexico may be exempt from tariffs calmed the nerves of investors. The Nasdaq Composite rose by 0.3%, the S&P 500 closed marginally lower, while the Dow Jones fell by 0.3%. Futures tracking the Dow, S&P, and Nasdaq 100 are currently very close to being flat. Asian markets were a sea of green today, as trade concerns eased somewhat. In Japan, the Nikkei 225 and the Topix climbed 0.5% and 0.4% respectively, while in Hong Kong, the Hang Seng trade higher by 1.5%. In Europe, futures tracking all the major benchmarks were flashing green.

COMMODITIES: Oil prices traded marginally higher today, with WTI and Brent crude both gaining 0.1%. However, this follows a sharp tumble yesterday, which was triggered after the EIA data showed another increase in US crude inventories, and US crude production hitting a record high. In precious metals, gold traded 0.2% higher today, last seen near the $1327/ounce handle. Price action in the yellow metal continues to be driven by uncertainties surrounding trade and as such, it declined overall yesterday, as trade concerns subsided a little.

Major movers: Dollar recovers though remains close to 2-week low with trade developments still dominating attention

The possibility of Canada and Mexico, as well as some other countries, being exempted from planned US tariffs led to the easing of concerns over trade, allowing the dollar index to rise from the two-week low of 89.41 hit yesterday. At 0731 GMT, the index was at 89.62.

A White House official said overnight that the Trump administration could offer Canada and Mexico a 30-day exemption from planned tariffs on steel and aluminum imports, with the period potentially being extended based on progress in NAFTA talks.

Despite some calmness setting in among market participants, uncertainty over trade remains in place and could lead to further volatility moving forward.

February’s ADP report on positions added to the economy by the US private sector, which is viewed by some analysts as a precursor to the nonfarm payrolls (NFP) report, also spurred optimism on the strength of the jobs market and supported the greenback. The NFP reading is due on Friday.

Euro/dollar traded 0.1% lower at 1.24 ahead of the conclusion of the ECB meeting on monetary policy later on Thursday. Dollar/yen was 0.15% lower at 105.90, with the BoJ concluding its respective meeting on monetary policy on Friday. Pound/dollar was not much changed around the 1.39 handle.

The Canadian dollar revisited an eight-month low on Wednesday, with dollar/lonnie touching 1.30 as the BoC made mention to trade fears as it kept rates unchanged upon completion of its two-day meeting. The loonie recovered a bit, helped by news that Canada may be exempted from US tariffs. Dollar/lonnie was 0.1% lower at 1.2894. The Mexican peso also benefitted from the tariff-exemption news.

The aussie was little changed versus the US currency and the kiwi was flat, as market participants awaited details of US tariff plans. Australia and New Zealand rely on commodity exports and potentially stand to lose in case a trade war breaks out.

Day ahead: ECB decision to set the tone for the euro; Trump expected to formally sign off on tariffs

Today, the spotlight will be on the European Central Bank policy decision at 1245 GMT, which will be followed by a press conference from President Draghi at 1330 GMT. The Bank is widely anticipated to remain on hold and as such, investors will be on the lookout for updated signals on the future evolution of policy. Specifically, attention will be on whether policymakers will tweak their forward guidance in a hawkish direction, by removing the sentence that they stand ready to increase the QE program in size and/or duration if the economic outlook becomes less favorable.

Importantly, the ECB has been discussing a potential adjustment in its language since its December meeting. A removal of that sentence today would pave the way for an eventual end to the QE program later this year, and could unleash another round of gains in the common currency. Conversely, if the Governing Council decides to be patient and keep its guidance unchanged, that may spell bad news for the euro as investors begin to doubt whether the Bank will indeed exit its QE program this year. Besides the forward guidance, euro-traders will focus on the updated economic forecasts, as well as Draghi’s remarks, especially any comments on the exchange rate.

In the US, all eyes will be on the White House, where President Trump is anticipated to formally sign off on the steel and aluminum tariffs his administration announced last week. The timing of this event is still tentative though, and it may well be delayed until tomorrow according to officials. The US administration announced yesterday that Canada and Mexico may be exempted from the proposed tariffs, and other countries could possibly join that list as well. Thus, investors will be looking to see which other economies are exempted, as they gauge the probability of this situation escalating into a retaliatory trade war. Based on the latest market reactions though, particularly the surge in stock markets, the financial community seems to be taking the view that these tariffs will be watered down and could end up being more symbolic in nature. At this stage, however, this may be a premature conclusion to draw.

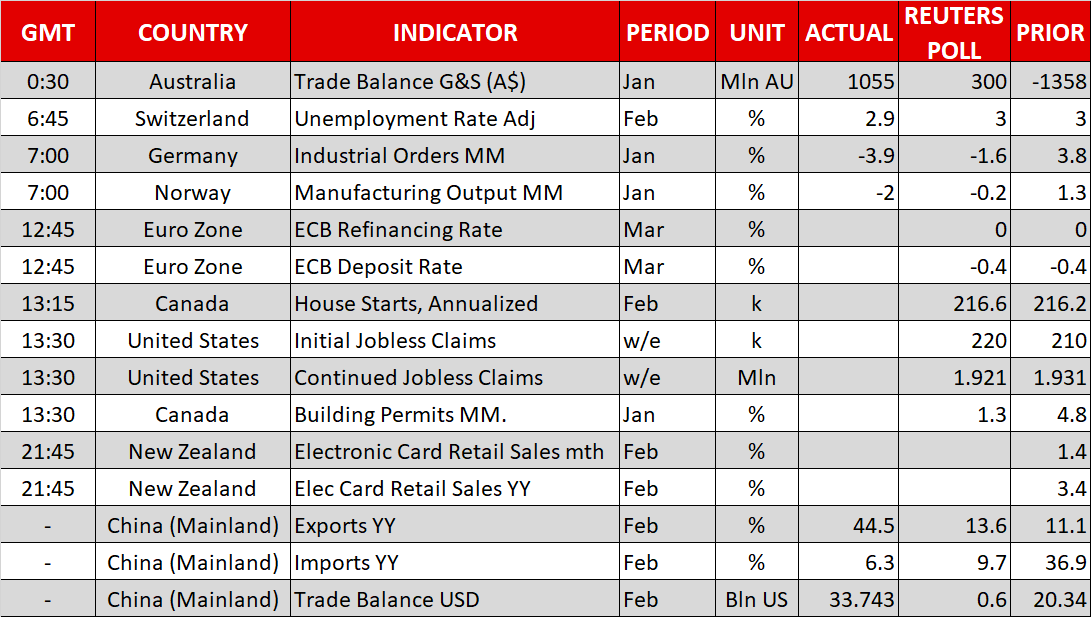

As for economic data, the calendar is almost empty today, with the only noteworthy releases being Canadian housing starts for February and US initial jobless claims for the week ended February 2, due out at 1315 GMT and 1330 GMT respectively.

Equity markets are likely to continue focusing on tariffs and how the global trading environment will evolve.

Besides ECB President Draghi, we will hear from the Bank of Canada’s Deputy Governor Timothy Lane at 2030 GMT. Investors may look to his comments for some clarity following yesterday’s policy decision, as there was no press conference after that gathering for the Bank to communicate its thinking more clearly.

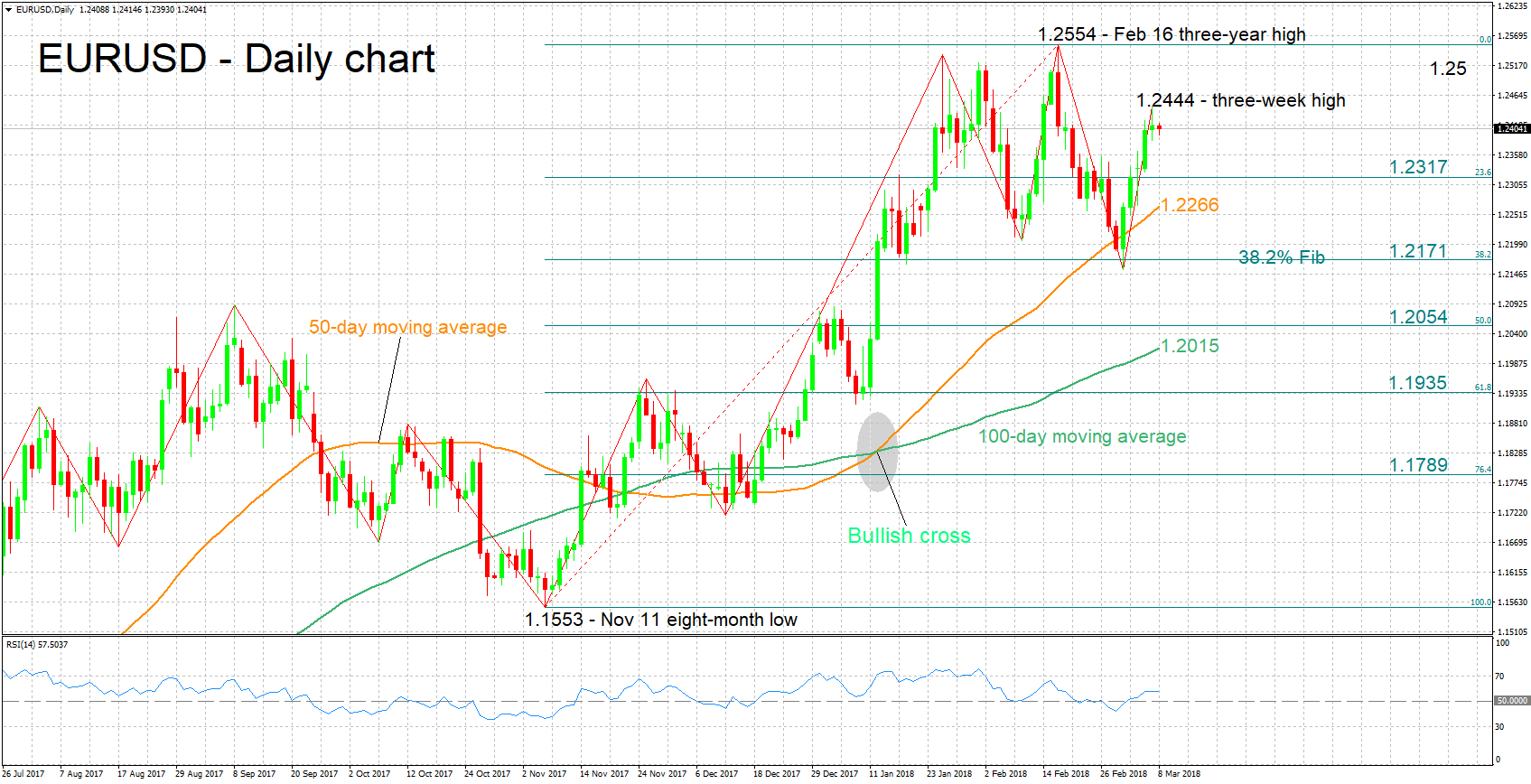

Technical Analysis: EURUSD looking neutral in the short-term ahead of ECB

EURUSD has declined a bit after hitting a three-week high of 1.2444 during Wednesday’s trading. The RSI has halted its advance and is moving sideways, pointing to a neutral short-term picture.

A hawkish message by the ECB later today is anticipated to be met with long EURUSD positions. In this scenario, some resistance could come around yesterday’s high of 1.2444 before the focus shiftis to the 1.25 handle that may hold psychological significance and could act as a barrier to the upside.

A dovish tone by the ECB on the other hand, is likely to lead to weakness in the pair. In this case, support could come around the 23.6% Fibonacci retracement level of the November 11 to February 16 upleg, at 1.2317.

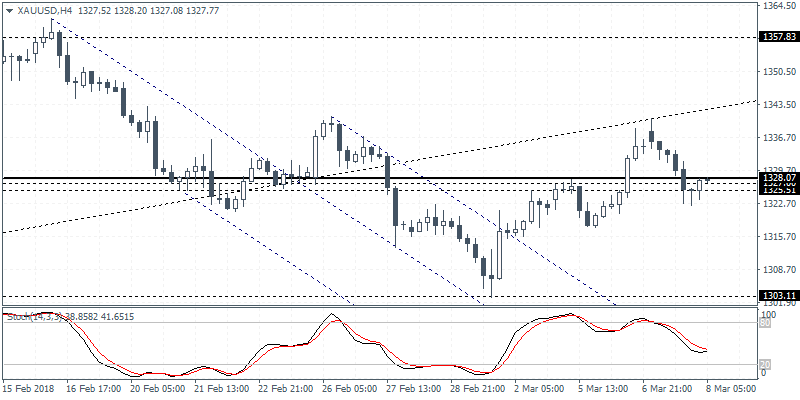

XAUUSD Intraday Analysis

XAUUSD (1327.77): Gold prices were seen closing on a bearish note yesterday following the previous day's strong gains. Price action closed below 1328 level which served as resistance previously. A follow through is required in order to confirm the resistance level at 1328. Alternately, if price action posts an upside bounce, we could expect to see further gains coming. Gold prices will need to breakout above the previous highs posted near the 1340 region in order to confirm the upside bias.

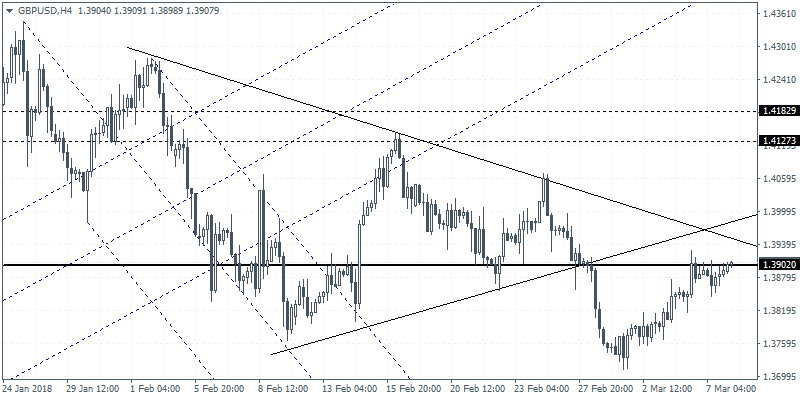

GBPUSD Intraday Analysis

GBPUSD (1.3907): The British pound was seen consolidating near 1.3902 level of resistance yesterday. A breakout above this level could signal further gains to the upside with price likely to target the previous highs established near 1.4200 region. On the 4-hour chart, the reversal back to 1.3902 marks a retest of the support/resistance level and the previous breakout from the triangle pattern. We expect to see price action continuing to consolidate near this level with the potential for a decline back to 1.3611 - 1.3589 level where support is yet to be tested.

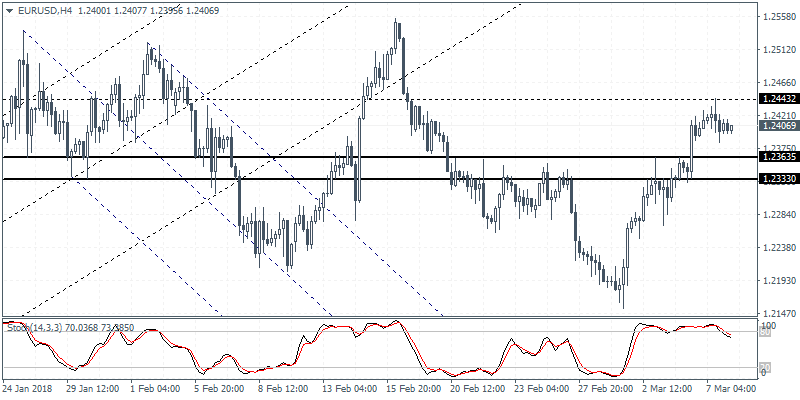

EURUSD Intraday Analysis

EURUSD (1.2406): The EURUSD was seen closing rather flat on the day following nearly four consecutive days of gains. With price action perched above 1.2363 level which previously served as resistance, any pullbacks are likely to extend to this level in the near term. The ECB's meeting today will serve as the main catalyst for EURUSD. A break down below 1.2363 - 1.2333 region could signal the downside bias in price. EURUSD is likely to extend lower targeting 1.2090 - 1.2070 level of support eventually.

BoC Votes To Keep Interest Rates Unchanged, ECB In Focus

The Bank of Canada held its monetary policy meeting yesterday as it left interest rates unchanged as widely expected. In the U.S. the markets were on the backfoot following the announcement that President Trump's chief economic advisor Gary Cohn resigned.

Looking ahead, the ECB's monetary policy meeting will be the main event that stands out today. The market expectations are mixed with the ECB expected to maintain the interest rates and the asset purchases steady. However, forward guidance could be the key factor with the markets divided on whether the ECB will be hawkish or dovish.

The Bank of Canada Governor, Stephen Poloz will also be speaking later today. The speech comes after the BoC voted to keep interest rates steady at yesterday's meeting. On the economic front, German factory orders and the weekly unemployment claims from the U.S. will be released today.