Sample Category Title

EUR/USD Consolidating

EUR/USD is approaching hourly support at 1.2165 (17/01/2018 low), currently trading sideways. Hourly resistance remains at 1.2434 (06/02/2018 high). The technical structure suggests sideways moves.

In the longer term, the momentum is turning largely positive. We favor a continued bullish bias. Key resistance is holding at 1.2886 (15/10/2014 high) while strong support lies at 1.1554 (08/11/2017 low).

Round Two With Fed Chair Powell

Thursday Mar 1: Five things the markets are talking about

U.S equities suffered their worst monthly decline in two years last month as investors continued to digest new Fed Chair, Jerome Powell’s, Tuesday’s comments. The S&P 500 Index slumped more than -1% yesterday, ending February with a decline of -4%.

U.S Treasuries and the dollar trade somewhat steady as the market awaits his second appearance this morning (10 am EST). Powell is due to testify on the Semi-annual Monetary Policy Report before the Senate Banking Committee, in Washington.

His comments this week has kept the door ajar to speculation that the Fed may want to quicken the pace of monetary tightening.

1. Stocks trade under pressure

In Japan, the Nikkei share average closed atop of its two-week low overnight as market sentiment was hit by the rout stateside on Wednesday. The Nikkei closed out -1.6% lower, while the broader Topix declined -1.7%.

Down-under, the Aussie ASX 200 declined -0.7%, weighed down mostly by mining heavyweights as commodity prices weakened, while the broader market retreated on fears of rising U.S interest rates. In S. Korea, the Kospi was closed for a holiday.

In Hong Kong, stocks fell to a two-week low. The Hang Seng index ended down -1.4%, while the China Enterprises index declined -2.1%.

In China, stocks recouped earlier losses to climb as consumer and banking firms rose, after a private survey showed the country’s factory growth rose to a six-month high in February. At the close, the Shanghai Composite index was up +0.6%, while China’s blue-chip CSI300 index was up +0.9%.

In Europe, regionalIndices trade lower across the board following yesterday’s weaker close on Wall street , and mostly weaker markets in the Far East.

U.S stocks are set to open in the ‘red’ (-0.2%).

Indices: Stoxx600 -0.9% at 376.1, FTSE -0.5% at 7195, DAX -1.4% at 12259, CAC-40 -1.1% at 5264, IBEX-35 -1.0% at 9745, FTSE MIB -0.8% at 22421 , SMI -0.9% at 8828, S&P 500 Futures -0.2%

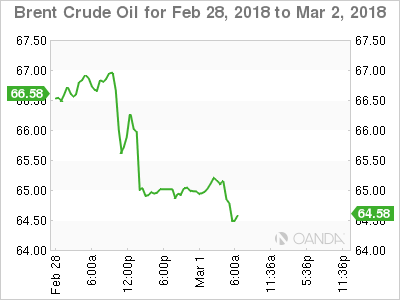

2. Oil prices capped, gold lower

Oil prices remain capped after U.S federal data yesterday showed that oil and gas are building up in storage even as U.S oil production continues to climb.

In the U.S, crude inventories grew by +3m barrels last week, and gas increased by +2.5m barrels, according to yesterday’s U.S EIA report. The market had correctly anticipated an increase, but a smaller one.

Note: On Tuesday the API group, an industry group said that its data for the week showed a +933k barrel increase in crude supplies, a +1.9m barrel rise in gas stocks and a -1.4m barrel decrease in distillate inventories.

Brent crude for May delivery is up +17c, or +0.3% at +$64.90, while the U.S West Texas Intermediate (WTI) for April delivery is up +13c, or +0.2% at +$61.77 a barrel.

Note: Both benchmark contracts fell nearly -5% in February, the first monthly declines in six-months.

Ahead of the U.S open, gold prices have dipped, pulled down, as the dollar remains better bid following Fed Chairman Powell’s comments that fanned concerns of faster-than-expected rate hikes in the U.S. Spot gold is -0.2% lower at +$1,315.36 an ounce. Prices have fallen about -1% so far this week.

3. Sovereign yields remain elevated

With central banks beginning to reduce their balance sheets should start to have a bigger effect on currencies. Policy normalization should lead to increased market volatility and also continue to impact the cost of hedging FX transactions.

Stateside, Treasury yields have notched another monthly advance in February. The yield on the U.S 10-year note has now risen for five of the past six-months as investors worry that inflation could be accelerating and that there may not be enough demand to meet additional Treasury’s issuance.

The yield on U.S 10’s has gained less than +1 bps to +2.86%. In Germany, the 10-year Bund yield has fallen less than -1 bps to +0.65%, the lowest in almost five weeks. In the U.K, the 10-year Gilt yield has declined -6 bps to +1.501%, the lowest yield in a month and the largest intraday fall in almost two-weeks.

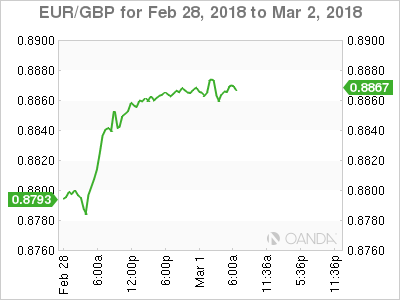

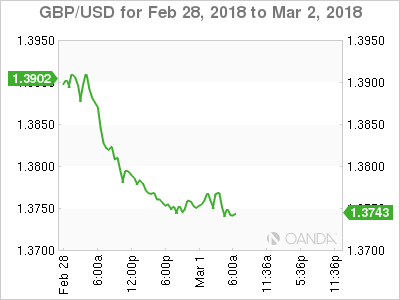

4. Sterling selling back in vogue on Brexit fears

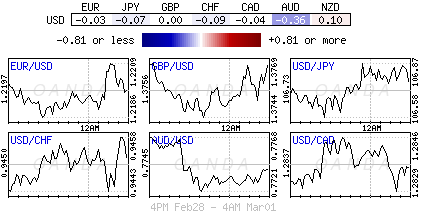

Selling sterling on concerns about the lack of progress in Brexit negotiations is back in fashion. The pound was driven to a two-week low outright overnight after the E.U published a draft Brexit withdrawal agreement. However, Prime Minister May has said she cannot accept the E.U’s proposals on the Northern Ireland border. GBP/USD last traded flat at £1.3759, up from around £1.3747 before this morning’s PMI data (see below). EUR/GBP trades roughly flat at €0.8858, having traded at around €0.8867.

Note: PM May’s will deliver a speech in Sunderland tomorrow (Mar 2) on the ” U.K’s relationship with E.U.” There is no specific time or location that has been announced yet. She has picked a strong pro-Brexit area and one that has not voted Tory in generations.

Elsewhere, the EUR has gained less than +0.05% to €1.2197.The Japanese yen dipped -0.2% to ¥106.86, while the South African rand sank -0.4% to $11.8485, the weakest in more than two-weeks.

5. German manufacturing revised higher, U.K manufacturing lower

Data this morning showed that Germany’s manufacturing PMI for February was revised up a tad to 60.6 from its flash estimate of 60.3. Digging deeper, rising input costs led many German manufacturers to increase prices – capacity issues have allowed vendors to negotiate higher prices as demand outstrips supply.

In the U.K, purchasing managers’ survey on manufacturing for February came in at 55.2, down just slightly from January’s 55.3 and in line with market expectations.

DAX Slides, As Global Stock Markets See Red

The DAX index has posted sharp losses in the Thursday session. Currently, the index is trading at 12,271.50, down 1.32% since the Wednesday close. European markets have followed the lead of the Asian and North American stock markets, which posted losses in the most recent session. On the release front, Germany and eurozone PMIs continue to point to strong expansion. German Manufacturing PMI dipped to 60.6, above the estimate of 60.3 points. It was a similar trend for the eurozone indicator, which dropped to 58.6, just above the estimate of 58.5 points. As well, the eurozone unemployment rate dipped lower to 8.6%, matching the forecast. In the US, Fed chair Jerome Powell testifies before the Senate Banking Committee. On Friday, Germany releases Retail Sales.

The eurozone continues to post steady economic growth, and the bloc’s unemployment rate has dropped to 8.6%. Still, inflation levels remain well below the ECB target of around 2 percent. In February, Eurozone CP edged lower to 1.2%, down from 1.3% in January. With plenty of slack in the eurozone economy, the ECB is not under pressure to tighten policy. The Bank will meet on March 8, and no major changes are expected. Policymakers could deliberate the possibility of removing the Bank’s easing bias towards increasing bond purchases if needed. A removal of the easing bias would likely be interpreted as a plan to tighten policy, which would be a vote of confidence in the economy and could rally European stock markets.

Jerome Powell is just settling into his new job, but it’s been an eventful few weeks for the new Federal Reserve chair. Powell was greeted by a sharp correction in US stock markets, as investors headed for the hills on fears that the Fed might accelerate its pace of rate hikes if inflation moves higher. On Tuesday, Powell testified before a congressional committee, and will speak before the Senate Banking Committee on Thursday. Powell’s message to Congress was decidedly hawkish, as the Fed chair said that the current policy of gradual rate increases would continue. He added that the economy was strong and that he expected inflation to move up to the Fed target of 2 percent. Importantly, Powell did not address the question of an acceleration of rate hikes, but his hawkish stance has increased the likelihood that the Fed will increase it projection from three to four rate hikes this year.

EUR/USD Analysis Continues Lower

During the early hours of Thursday's trading session the common European currency continued to lose ground against the US Dollar. Meanwhile, Dukascopy analysts spotted two notable facts about the pair's charts.

The decline, which followed the first testimony of the head of the Federal Reserve, has confirmed that it is occurring in a narrow descending channel pattern.

Meanwhile, analysts looked for a possible level of support, which might force a reversal of the direction. As a result of the efforts, a possible support line of a long term almost horizontal pattern has been set near the 1.2170 mark.

The zone around this line should be watched carefully.

GBP/USD Analysis Continues In Discovered Pattern

The patterns drawn on Wednesday have held their ground, as the Pound continues to trade against the Greenback in a narrow channel down pattern. However, the decline on Thursday morning turned sideways.

If one looks at the hourly chart, it can be observed that the rate made a few attempts to rebound after meeting the lower trend line of the channel down pattern. Although, the resistance of the weekly S2 has stopped the efforts of the Pound.

Meanwhile, it was noticed that the supposed sideways fluctuations were booking lower and lower rebound points. That indicates that the decline will continue.

USD/JPY Analysis Breaks Support Levels

The support level described on Wednesday did not manage to hold its ground. As a result one can spot a large, red hourly candle on the USD/JPY currency pairs charts. Although, the sudden drop was stopped by a medium scale pattern's lower trend line, which on Thursday was acting as a resistance.

Meanwhile, the large scale descending channel was once more adjusted, as its exact borders have been mysterious during this week.

However, most attention should be given to the newly spotted channel down pattern, which might guide the pair lower. That would occur after a resistance cluster is met just below the 107.00 mark.

Gold Analysis Declines As Expected

The expected decline of the yellow metal has occurred. However, it did not come into reality exactly as it was expected.

The bullion broke the narrow ranged channel down pattern. The narrow pattern turned out to represent the junior decline in the borders of a wider descending pattern.

The newly discovered pattern was the one, whose upper trend line provided the resistance needed for the speculated decline.

In regards to the near future, on Thursday morning the range down to the levels near the 1,300.00 mark was free from support.

EUR/USD: US Crude Oil Inventories

The Greenback strengthened against its European counterpart following the release of the US crude oil inventories report for the week ended 23 February. The EUR/USD exchange rate fell just seven base points, or 0.05%, to the 1.2190 level and continued to fluctuate in the 1.2200 area.

The Energy Information Administration stated that crude oil inventories rose three million barrels, which is 0.6 million barrels more than expected in the reported week, following a drop in domestic crude oil inventories as of the week before. The US Dollar keeps gaining strength after various generally positive reports including Powell's testimony that will most probably play its role for a few more weeks.

Equities In Red And USD Better Bid Ahead Of Powell Testimony And PCE Inflation

Market nervousness rises ahead of PCE inflation and Powell testimony

The Fed's favourite measure of inflation for the month of January, the core personal consumption measure or Core PCE, is due for release this afternoon. The tension is mounting among investors as this indicator is closely monitored by the Fed and could therefore influence significantly the path of monetary policy in the US. Indeed, the publication of January's CPI sparked strong reactions across financial markets as market participants adjusted their positions for a stepper path of interest rate. The headline PCE is expected to have remained stable at 1.7%y/y in January, while the core measure should come in at 1.5%y/y.

The second key event of the day is the testimony of Fed chair Powell before the Senate banking committee. We believe that Powell will be keen to soften its hawkish stance regarding the US economy. During a congressional testimony, Powell suggested that the Fed could increase borrowing rates four times this year, compared to three hikes expected by market participants and signalled by the central bank so far.

So what can investors should expect from this day? On the one hand, an upside surprise in inflation could definitely trigger a dollar; however, as discussed yesterday, higher interest rates could slowly dampen US growth against the backdrop of a leveraged private sector and an already stretched federal budget. On the other hand, Powell may use a more dovish tone today during his Senate hearing. Therefore, we believe that all-in-all the risk is skewed to the downside for the US dollar.

EUR/USD is currently trading around the bottom of its monthly range. A break of the strong 1.2165 support will open the door towards 1.20, then 1.1916 (low from January 9th). On the upside, a first resistance can be found at around 1.2350 (previous highs), then 1.2555 (high February 16th).

Indian growth wonders

Indian quarter (October – December) Gross Domestic Product published on Wednesday provided Prime Minister Narendra Modi with a big relief, given at 7.20% (consensus at 6.90%) against July-September and April – June quarters at 6.30% and 5.70%, making it the largest quarterly growth of the year. India becomes the fastest growing economy in relative numbers (India and China GDP 2017: 7.10% and 6.80%), as China starts seeing signs of slowdown in consumption and manufacture (January CPI at slowest pace since July 2017, PPI lowest rate since November 2016 and Manufacturing PMI low since July 2016).

Indian Sensex declines though the release, valued at 34'153 (-0.56%) along world equity indexes decline.

EUR/USD – Euro Takes Breather After Recent Slide

The euro is unchanged in the Thursday session, after considerable losses this week. Currently, EUR/USD is trading at 1.2188, down 0.05% on the day. Om the release front, the focus is on manufacturing PMIs, which performed well in Germany and the eurozone. German Manufacturing PMI dipped to 60.6, above the estimate of 60.3 points. It was a similar trend for the eurozone indicator, which dropped to 58.6, just above the estimate of 58.5 points. In the US, there are a host of key events, led by unemployment claims and personal spending. As well, Fed chair Jerome Powell testifies before the Senate Banking Committee. On Friday, Germany releases Retail Sales and the US publishes UoM Consumer Sentiment.

Jerome Powell is barely settled in his new office, but it’s been an eventful few weeks for the new Federal Reserve chair. Powell was greeted by a sharp correction in US stock markets, as investors headed for the hills on fears that the Fed might accelerate its pace of rate hikes if inflation moves higher. On Tuesday, Powell testified before a congressional committee, and will speak before the Senate Banking Committee on Thursday. Powell’s message to Congress was decidedly hawish, as the Fed chair said that the current policy of gradual rate increases would continue. He added that the economy was strong and that he expected inflation to move up to the Fed target of 2 percent. Importantly, Powell did not address the question of an acceleration of rate hikes, but his hawkish stance has increased the likelihood that the Fed will increase it projection from three to four rate hikes this year.

Inflation in eurozone edged lower to 1.2% in February, down from 1.3% in January. This reading met expectations, but underscores that inflation levels remain well below the ECB target of around 2 percent. Economic growth has rebounded, led by a robust German economy. Still, there is plenty of slack in the eurozone economy and the ECB is not under pressure to tighten policy. The Bank will meet on March 8, and major changes are expected. Policymakers could deliberate the possibility of removing the Bank’s easing bias towards increasing bond purchases if needed. A removal of the easing bias would likely be interpreted as a plan to tighten policy and would be bullish for the euro.