Sample Category Title

Sunset Market Commentary

Markets:

Global core bonds profited from safe haven flows during European trading as losses on stock markets amounted to 1.5%. Today's expected announcement of tariffs on steel and aluminum by US President Trump probably played a role. The German Bund briefly crossed 159.75 with the German 10-yr yield testing 0.62%. A break didn't occur, triggering return action. The intraday topping off pattern in core bonds was further enhanced by stronger than expected US eco data. PCE deflators printed in line with forecasts, but at high levels. Jobless claims dropped to historically low levels, confirming tight conditions on the US labour market. Markets are now counting down to round 2 of Fed chair Powell's testimony for US Congress. At the time of writing, changes on the US yield curve range between -1.2 bps (5-yr) and +0.7 bps (30-yr). German yields shift around 1.5 bps lower across the curve. 10-yr yield spread changes versus Germany are almost unchanged with Greece underperforming (+10 bps).

The dollar succeeded some incremental further gains today; a cautious continuation of the post-Powell rebound. The Fed-president indicating that US rates could be raised four times this year reinstalled some kind of renewed 'divergence trade'. EMU data were OK, but in line. US jobless claims dropped to a multi-decade low. The PCE deflator printed as expected at 0.4% M/M and 1.7% Y/Y. US yields tried to reverse a cautious intraday decline after the release of the data, but it didn't help any further USD gains, at least not of the dollar against the euro. Even so, the 2-yr interest rate differential between the US and Germany reached a new cycle top of 280 bps, the highest level since 1997! Interest rate differentials are not the only factor guiding currencies, but at some point this kind of premium should finally give the dollar downside protection. EUR/USD already tested the key 1.2165 area earlier today. A real break didn't occur yet, but the pressure is building. USD/JPY tries to regain the 107 barrier, but it remains an uphill battle. The focus now turns to the manufacturing ISM and even more to the Q&A of Powell's hearing before the US Senate.

Sterling showed no clear directional trading pattern (against the euro). Brexit tensions are dominating the headlines. Yesterday, EU negotiator Barnier warned that there was no guaranty on a transition deal. He also made a proposal on the Irish boarder that was inacceptable for the UK. Today, EU president Tusk said that one can't expect frictionless trade outside the bloc's single market. The political bickering continues, one day before the key Brexit speech of UK PM May. Sterling didn't decline further against the euro. EUR/GBP hovered in the 0.8840/75 area. The UK manufacturing PMI was little changed at 55.2. This remains quite a healthy level. However, it didn't change the markets' assessment on the BoE's rate intentions. The report had little impact on sterling trading on EUR/GBP.

News Headlines:

US consumer prices increased in January, with PCE core inflation (0.3% M/M & 1.5% Y/Y) posting its largest gain in 12 months, bolstering views that price pressures will accelerate this year. The PCE deflator was in line with expectations (0.4% M/M 1.7% Y/Y). January personal income (tax bump?) and spending rose by 0.4% M/M and 0.2% M/M respectively while weekly jobless claims dropped to the lowest level since 1969 (210k)! The February manufacturing ISM rose from 59.1 to 60.8 (vs 58.7 expected) with the prices paid component surging to 74.2!

The February EMU manufacturing PMI was slightly upwardly revised from 58.5 to 58.6 while the UK manufacturing PMI stabilized around 55.2. The January EMU unemployment rate declined from 8.7% to 8.6%, the lowest level since December 2008.

Japanese Yen Slightly Lower, Japanese Consumer Reports Next

The Japanese yen has posted slight gains in the Thursday session. In North American trade, USD/JPY is trading at 106.90, up 0.21% on the day. On the release front, it's a busy day. In Japan, Capital Spending gained 4.3%, beating the estimate of 3.1%. Final Manufacturing PMI dropped to 54.1, within expectations. Consumer confidence slowed to 44.3, shy of the estimate of 44.9 points. Later in the day, Japan releases Household Spending and Tokyo Core CPI. In the US, Personal Spending slowed to 0.2%, matching the forecast. Unemployment claims dropped to an impressive 210 thousand, well below the estimate of 222 thousand. Next up, Fed chair Jerome Powell testifies before the Senate Banking Committee. On Friday, the US publishes UoM Consumer Sentiment.

Jerome Powell will be on center stage on Thursday, as he testifies before the Senate Banking Committee. Powell addressed the House Finance Committee on Tuesday, and his remarks were decidedly hawkish. Fed chair said that the current policy of gradual rate increases would continue. He added that the economy was strong and that he expected inflation to move up to the Fed target of 2 percent. Importantly, Powell did not address the question of an acceleration of rate hikes, but his hawkish stance has increased the likelihood that the Fed will increase it projection from three to four rate hikes this year. Any hints that Fed will quicken its pace of rate hikes would be bullish for the US dollar.

US revised GDP came in at 2.5% in the fourth quarter, down from the initial estimate of 2.6% in January. This is considerably lower than the 3.2% expansion in the third quarter. The downward revision was attributed to lower inventory than expected. Importantly, consumer spending, a key driver of economic growth, remained unchanged at 3.8% percent in the fourth quarter. Despite the lower revision to GDP, sentiment remains positive on the US economy, and Jerome Powell's hawkish testimony earlier this week marks an important vote of confidence in the US economy.

US: Tax Cuts Boost Incomes, But Household Spending is Soft to Start 2018

Personal income rose 0.4% in January, beating the consensus expectation for a 0.3% gain. A reduction in current personal taxes led to an even more sizable gain in disposable income, which rose 0.9% on the month. Controlling for inflation, real disposable income was up a robust 0.6%.

Personal spending came in on expectations, rising 0.2% in nominal terms. In real (inflation-adjusted) terms however, spending fell 0.1%. By component, real spending on durable goods declined 1.6%, pulling back after a strong 0.6% (but downwardly revised) gain in December. Non-durable goods spending was flat, while services spending edged up 0.1%.

Prices rose 0.4% month-on-month in January, as energy prices rebounded (+3.0%). Headline inflation was unchanged at 1.7% year-on-year. Core prices firmed, rising 0.3% (m/m) in January, but core inflation remained unchanged at 1.5% year-on-year.

The personal saving rate jumped to 3.2% from an upwardly revised reading of 2.5% in December, as households held on to some of their windfall gains from lower taxes.

Key Implications

Just as it did at the beginning of 2016 and 2017, consumer spending started the year on a soft note. This despite the boost to disposable income from a smaller tax take. Some of the spending weakness is simply give back following hurricane-induced buying late in 2017. Nonetheless, it is difficult not to notice the apparent seasonal pattern even in the "seasonally adjusted data," whereby relatively strong gains in December are followed by a pullback in January.

The weakness to start the year is likely to imply a relatively slow first quarter in terms of real GDP growth. Even with relatively strong growth in February and March, both real consumption and GDP appear likely to have a one-handle in front of them. Still, we are not concerned with the apparent setback, which is likely to prove short lived. With both tax cuts and a tightening labor market likely to push up income, household demand is expected to accelerate enough to pull growth to an above-trend rate over the remainder of 2018.

While inflation remained unchanged on a year-on-year basis, the momentum has picked up in recent months. The annualized three-month moving average inflation rate currently sits at the Fed's 2.0% target. Still, there is cause to fade some of this strength – the residual seasonality in the real spending data is the flip side of seasonality on the inflation front, where price growth appears understated at the end of the calendar year and overstated in January.

US Dollar Index is Ready for Bullish Retracement; Creates 7-Week High

The US dollar index created a double bottom on February 16 near 88.20, posting a new more than 3-year low. The double bottom reversal is a bullish pattern indicating further gains on the price action as the index jumped above the significant area of 90.45. Currently, the price is recording a 7-week high near 90.75.

In the daily chart, short-term momentum indicators are also pointing to a continuation of the bullish bias. The Relative Strength Index is well above the 50 level, suggesting that the latest upswing may be running towards the overbought zone. The MACD oscillator is rising above the trigger line and has just entered the positive territory. In addition, the 20 simple moving averages is sloping to the upside, endorsing the upside scenario.

Further gains should see the 91.00 handle acting as a major resistance taken from the low on September 8. A run above this area could reinforce the bullish structure in the short-term as it could take the price towards the descending trend line near 91.50, which has been holding over the last year. Also, the 23.6% Fibonacci retracement level of the downleg from 102.23 to 88.20 is standing near the aforementioned level.

In the event of a continuation of the downside movement, the price could re-challenge the 88.20 support barrier, but the price would first need to go through the 20 and 40 SMAs.

Will Powell Deliver Another Blow to US Markets?

Hawkish Powell Weighing on Stocks

US equity markets are expected to open in the red on Thursday, as traders await the second appearance of the week from new Federal Reserve Chair Jerome Powell and a selection of economic data.

Powell's testimony in front of the House Financial Services Committee on Tuesday was very bullish on the economy and led many to believe that a fourth rate hike is on the table this year. While this isn't a million miles from what markets are pricing in, it did trigger another negative response from markets with US indices falling around two and a half percent since and positioned for further losses today.

It would appear markets are bracing for more hawkish commentary from Powell today when he appears before the Senate Banking Committee, once again discussing the semi-annual monetary policy report. Given everything that he said on Tuesday, it seems pretty clear that economic forecasts will be revised higher this month and the pace of tightening will likely therefore pick up, which may make today's less eventful as he reiterates many of the views already expressed. That said, should he wish to back pedal on anything or clarify points that have been misinterpreted, it may attract some attention.

US Inflation Data Eyed

What may be of more interest today is the US economic data that's being released. Yesterday's GDP data showed the economy growing at a decent pace in the fourth quarter and with momentum very much building and tax reform providing additional stimulus, this will likely pick up in the quarters ahead. This makes the inflation data all the more interesting, especially as the labour market slack has already been largely diminished which should put more upward pressure on prices.

The core PCE price index is the Fed's preferred measure of inflation and has been gradually ticking up again in the last few months. At 1.5%, it is still below the Fed's 2% target but close enough that any surprise beat will likely trigger a reaction in the markets, particularly following such a hawkish testimony from the new Fed Chairman. Personal income and spending figures will also be of interest, along with the two manufacturing PMI surveys.

Sterling at Six Week Low as Transition Talks Frustrate

We've already had a large number of PMI readings from across Europe this morning but, despite the numbers being broadly positive, they have failed to lift the mood in markets. The UK manufacturing PMI ticked slightly lower from a month ago, although this was largely shrugged as it remains quite elevated, with the sector having been boosted by a weaker pound over the last 18 months.

The pound is trading at six week lows against the dollar this morning, having come off its highs as Brexit discussions come back into focus, with both sides in talks over the transition period. A deal on the transition was initially intended to be completed this month, allowing for other discussions to take place over the course of the rest of the year but with both sides seemingly far apart on their expectations – to the surprise of no one – this could run over which is making traders uneasy and weighing on the pound.

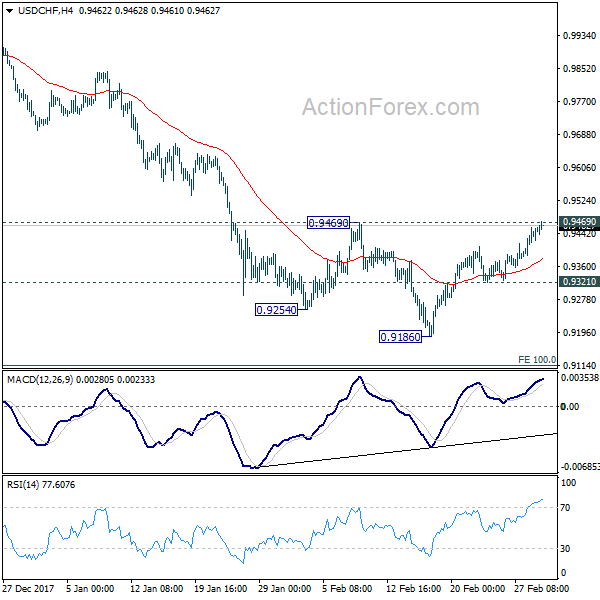

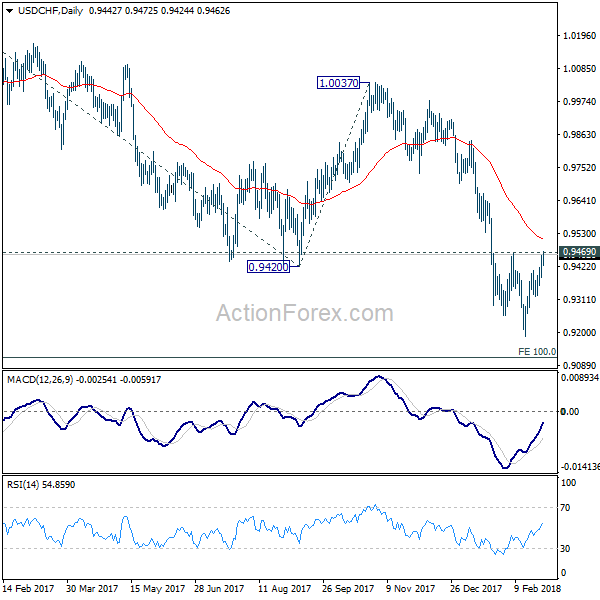

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9401; (P) 0.9429; (R1) 0.9474; More...

USD/CHF's rally continues today and is now pressing 0.9469 key near term resistance. Considering bullish convergence condition in 4 hour MACD, firm break of 0.9469 will indicate near term reversal and turn outlook bullish for 55 day EMA (now at 0.9511) and above. On the downside, below 0.9321 minor support will bring retest of 0.9186. Break there will extend the larger down trend to 0.9115 medium term projection level next.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Deeper decline should be seen to 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115. Break will target 161.8% projection at 0.8545. In any case, sustained trading above 55 day EMA is needed to be the first sign of medium term reversal. Otherwise, outlook will stay bearish even in case of strong rebound.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 106.31; (P) 106.92; (R1) 107.27; More...

USD/JPY continues to stay in tight range and intraday bias remains neutral. On the upside, break of 108.27 will be the first sign of near term reversal and will target 110.47 resistance for confirmation. On the downside, below 106.37 minor support will bring retest of 105.54 low. Break of 105.54 will extend the larger decline from 118.65 and target 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48 now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

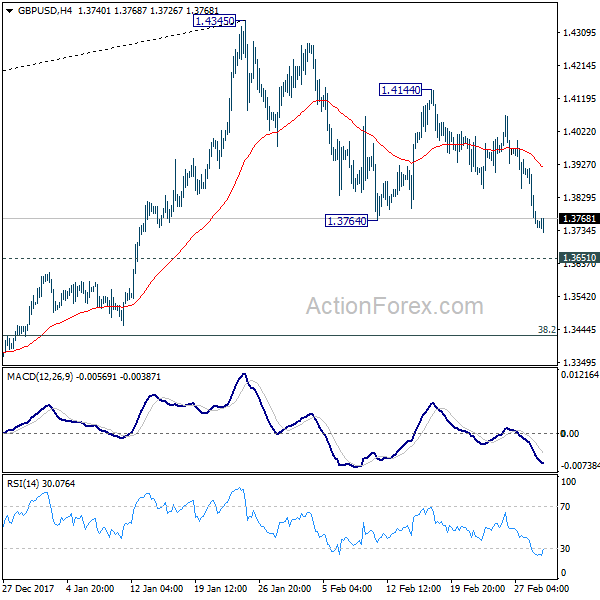

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3704; (P) 1.3810; (R1) 1.3864; More....

As noted before, fall from 1.4345 has just resumed. Intraday bias stays on the downside for 1.3651 resistance turned support and below. At this point, such fall is viewed as a corrective move. Hence, we'll look for strong support from 38.2% retracement of 1.1946 to 1.4345 at 1.3429 to contain downside and bring rebound. Nonetheless, break of 1.4144 resistance is needed to confirm completion of the decline. Otherwise, near term outlook will remain mildly bearish even in case of recovery.

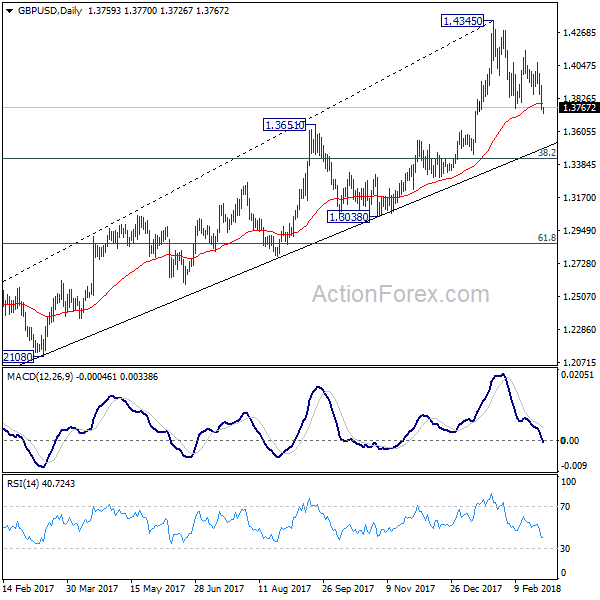

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4279) so far. Break of 1.3038 support, will suggests that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

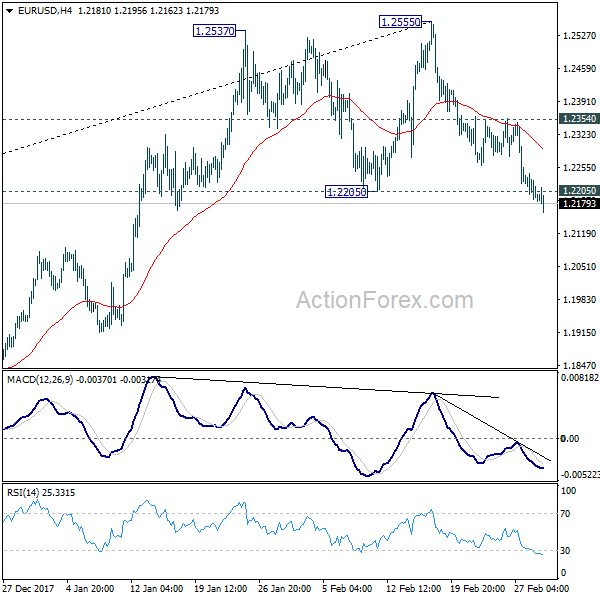

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2173; (P) 1.2207 (R1) 1.2227; More....

As noted before, the break of 1.2205 key support is taken as a tentative sign of trend reversal, after being rejected by 1.2516 key fibonacci level. Intraday bias remains on the downside for deeper fall. Sustained trading below 1.2205 will confirm and target 38.2% retracement of 1.0339 to 1.2555 at 1.1708. On the upside, above 1.2354 minor resistance will dampen this bearish case and bring retest of 1.2555 high instead.

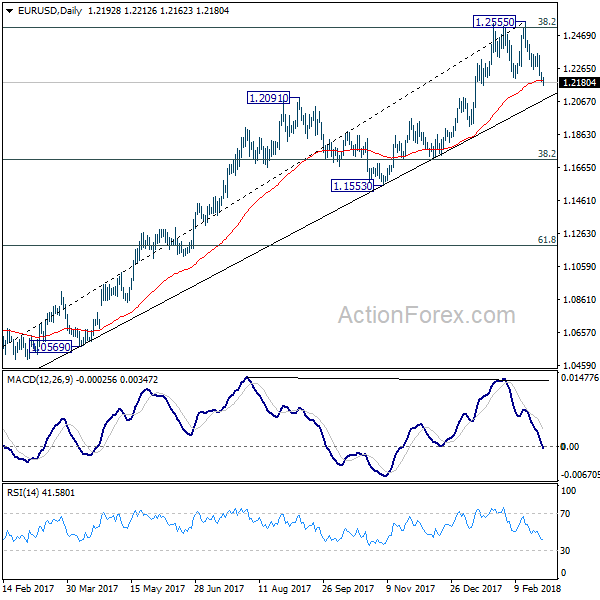

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.5553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

Spot Gold at New 2-Mth Low as Dollar Rises on Fed’s Hawkish Stance

Spot Gold hit two-month low at $1306, on fresh bearish acceleration which cracked key near-term support at $1307 (08 Feb low). The yellow metal, sensitive on changes of US interest rates, came under increased pressure after Fed's new chief Jerome Powell, in his debut testimony, pointed at strong US economic outlook, indicating that the Fed could increase the pace of rate hikes this year and sending the greenback higher. Violation of $13707 pivot is negative signal which requires confirmation on close blow support to complete failure swing pattern on daily chart and confirm double-top ($1366/61) for further weakness. Bears now eye strong supports at $1301/00 (100SMA/daily cloud base/Fibo 50% of $1236/$1366 ascend), loss of which would expose next key supports at $1286 (200SMA/Fibo 61.8% retracement). Today's break below 55SMA and formation of double bear-cross (10/30 and 10/20SMA's), along with fresh bearish momentum, increase bearish pressure and maintain negative sentiment. Broken 55SMA now marks solid resistance at $1318, which is expected to keep the upside protected.

Res: 1307; 1313; 1318; 1324

Sup: 1300; 1294; 1286; 1279