Sample Category Title

Trump to Impose Steel and Aluminum Tariffs, Markets Cried No!

The broader markets responded very negatively to US President Donald Trump's push for steel and aluminum import tariffs. DOW closed down -420 pts or -1.68% at 24608.98, breaking key near term support at 24792.99. S&P 500 lost -36.16 pts or -1.33% to close at 2677.67, breaking equivalent support at 2697.77. NASDAQ, the relatively stronger one recently, also dropped -92.45 pts or -1.27% to close at 7180.56, confirming failure below 7505.77 record high. Treasury yields also suffered with 10 year yield dropping -0.064 to 2.80. It looks like TNX has already topped below 3% handle. Asian markets follow with Nikkei losing over -500 pts or -2.3% at the time of writing. Hong Kong HSI is down -430 pts or -1.4%.

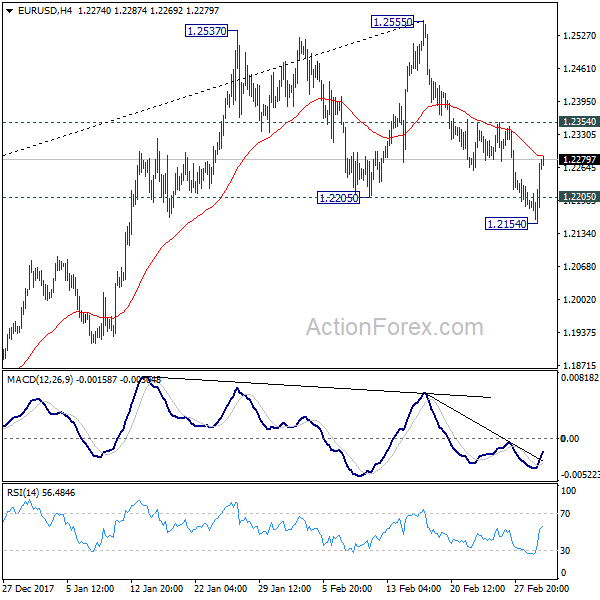

It once looked like Dollar is finally reversing the down trend as dollar index hit as high as 90.93. But it ended lower at 90.32 after failing to break through 91.01 key resistance. EUR/USD's breach of 1.2205 key support proved to be brief as it's now back at 1.2275. While more downside is in favor in EUR/USD with 1.2354 resistance intact, the bearish case is clearly dampened. Similarly, USD/CHF breached 0.9469 resistance but failed to sustain above there, now trading at 0.9400. More weakness is indeed seen in USD/JPY, which broken 106.37 minor support and should be heading back to 105.54 low. But overall in the currency markets, Yen is trading as the strongest one for the week, followed by Dollar. Canadian Dollar is the weakest one, followed by Sterling and then Aussie.

Chain reactions, retaliation and political uncertainty for Trump's tariffs

Trump told steal and aluminum industry executive that he will impose tariffs of 25% on steel and 10% on aluminum yesterday. And he plans to make the formal announcement next week. Trump also emphasized that the tariffs with apply to all countries. If there is exemptions, all other countries would request similar treatment. And that would also just open a back door for imports through the exempted country.

Accord to data of IHS Global Trade Atlas, in 2017, Canada was the top supplier of steel to the US, with 16% share. It's followed by Brazil (13%), South Korea (10%), Mexico (9%), Russia (9%), Turkey (7%), Japan (5%), Taiwan (4%), Germany (3%) and India (2%). China is outside of top 10 at 11.

The stock markets reaction showed broadly speak, Trump's move is not welcomed. Heavy steel and aluminum companies like Boeing and Ford Motors would be heavily hit. And the impact would likely spread further to other sectors. Secondly, there is serious threat of retaliation by his trade partners. US is already in NAFTA renegotiation with Canada and Mexico, who are the country's top and fourth largest steel supplier.

More importantly, we believed that markets were hit by political uncertainties within Trump's camp. The Politico reported that Trump's top economic adviser Gary Cohn spent a frantic 24 hours with others trying to stop Trump on the move on tariffs. Cohn has been on the brink of leaving Trump last year following the latter's comment regarding a white supremacist march in Charlottesville. But it's reported Cohn stayed for the main reason to stop Trump from starting trade war.

Fed Powell: Don't get behind the curve

In the second round of his Congressional Testimony, Fed Chair Jerome Powell said that "there is no evidence the economy is overheating." And, while the unemployment rate at 4.1% is "at or near or even below" the figure of full employment, there is no evidence of a "decisive move up in wages". He added that "nothing in that suggests to me that wage inflation is at a point of acceleration." To Powell, risks are "more two-sided" at this early stage of recovery. But he emphasized that "the thing we don't want to have happen is to get behind the curve." Hence, Fed will continue to "gradually raise interest rates" and that's the "appropriate path."

Regarding trade, Powell said it as a "net positive" for the US economy with some winners and some losers. But he also said "the tariff approach is not the best approach. The best approach is to deal directly with the people who are affected rather than falling back on tariffs."

Fed Dudley: Protectionism is a dead end

Separately, New York Fed William Dudley said that even if Fed will hike four times this year, "it would still be gradual". He also warned that "raising trade barriers would risk setting off a trade war, which could damage economic growth prospects around the world." And, "in the longer term it would almost certainly be destructive." He added that there will be "often backfire" of retaliation, higher consumer costs, higher production costs and lowered competitiveness. And, "the expectation that higher trade barriers would save jobs ignores these critical second-round effects." He emphasized that "there are many approaches to dealing with the costs of globalization, but protectionism is a dead end."

No major policy shift at ECB March meeting

Reuters quoted unnamed sources saying that ECB will likely discussion a minor tweak in the communication in the March 8 meeting next week. But there will not be any major policy shift. One source said that "there is general concern about market volatility and inflation has been heading down so it's clearly not the right time." And, "the easing bias could easily go but even that might have to wait." And that source expressed concern that "there is fear about signaling too much and increasing market volatility."

Meanwhile, according to a Reuters poll of 80 economist taken between February 26-28, Eurozone GDP growth is expected to average 2.3% this year and 2.0% next. Inflation would average 1.5% this year and 1.6% next, staying well below ECB's 2% target. Over 70% of economists expected ECB to announce ending of the asset purchase program at or before June meeting. 90% expected ECB to keep interest rates unchanged for many months after ending asset purchases. And, 70% of 51 economists who answered a separate question noted that Eurozone's growth momentum has peaked.

UK PM May to set out five tests for Brexit deal

UK Prime Minister Theresa May will deliver her high profile speech regarding UK-EU relationship today. Accord to the extracts by her office, May would seek "broadest and deepest possible agreement - covering more sectors and co-operating more fully than any Free Trade Agreement anywhere in the world today." And, "rather than having to bring two different systems closer together, the task will be to manage the relationship once we are two separate legal systems."

May is expected to set out five "tests" for the deal with EU. They are:

- That any deal must respect the referendum result

- That any deal must not break down

- That any deal must protect jobs and security

- That any deal must be "consistent with the kind of country we want to be" - modern, outward-looking and tolerant

- That any agreement must bring the country together

However, so far, there is no information on how May would handle the issue of the border of the Irelands. Would it be a hard border that violate what May has promised in the join report back in December? Or would it be a "common regulatory area" as EU proposed? Or would May come up with something creative?

On the data front

New Zealand building permits rose 0.2% mom in January. Japan unemployment rate dropped sharply to 2.4% in January, monetary base rose 9.4% yoy in February, Tokyo CPI rose to 0.9% yoy. Looking ahead, German retail sales and import price will be released in European session. Eurozone will also release PPI. UK construction PMI will be featured. Later in the day, main focus will be on Canada GDP.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2173; (P) 1.2207 (R1) 1.2227; More....

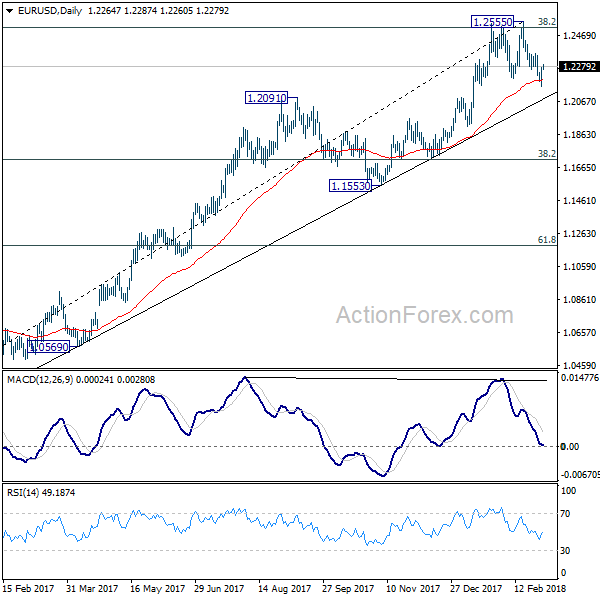

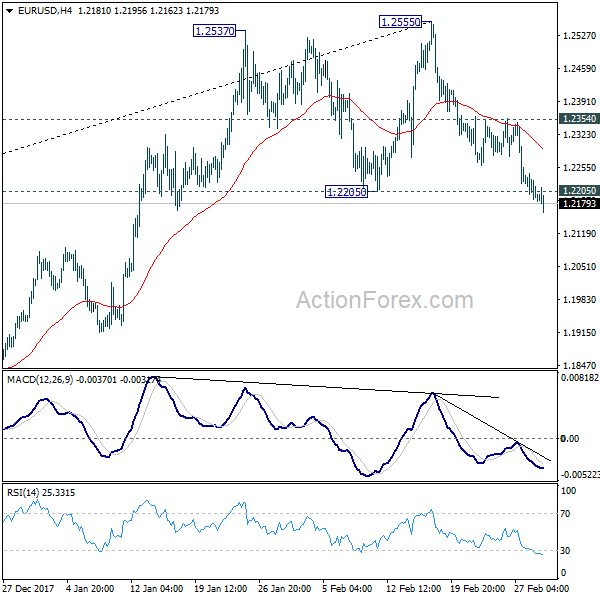

Despite dipping to 1.2154, EUR/USD could not sustain below 1.2205 key support and recovered. Intraday bias is turned neutral first. With 1.2354 resistance intact, we're still favoring the case of trend reversal. That is, EUR/USD has topped at 1.2555 and was rejected by 1.2516 key fibonacci level. But sustained trading below 1.2205 is needed to confirm. Break of 1.2154 should send EUR/USD lower to 38.2% retracement of 1.0339 to 1.2555 at 1.1708. On the upside, above 1.2354 minor resistance will invalidate this bearish case and bring retest of 1.2555 high instead.

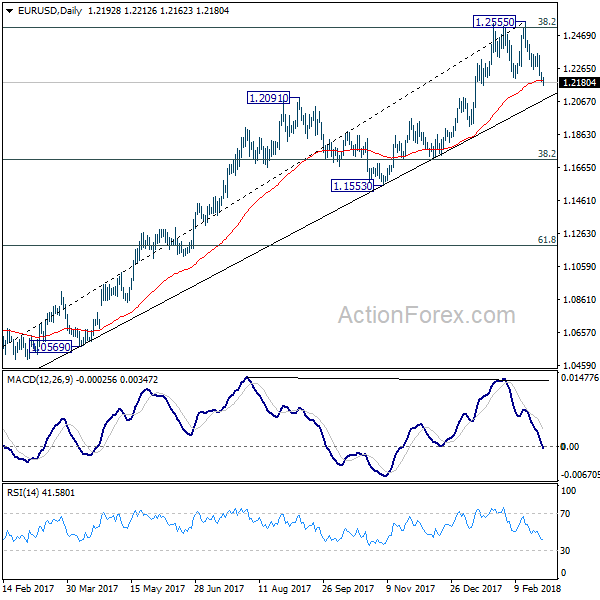

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.5553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits M/M Jan | 0.20% | -9.60% | -9.50% | |

| 23:30 | JPY | Jobless Rate Jan | 2.40% | 2.80% | 2.80% | |

| 23:30 | JPY | Tokyo CPI Core Y/Y Feb | 0.90% | 0.80% | 0.70% | |

| 23:50 | JPY | Monetary Base Y/Y Feb | 9.40% | 9.20% | 9.70% | |

| 7:00 | EUR | German Retail Sales M/M Jan | 0.70% | -1.90% | ||

| 7:00 | EUR | German Import Price Index M/M Jan | 0.40% | 0.30% | ||

| 9:30 | GBP | Construction PMI Feb | 50.5 | 50.2 | ||

| 10:00 | EUR | Eurozone PPI M/M Jan | 0.40% | 0.20% | ||

| 10:00 | EUR | Eurozone PPI Y/Y Jan | 1.60% | 2.20% | ||

| 13:30 | CAD | GDP M/M Dec | 0.10% | 0.40% | ||

| 15:00 | USD | U. of Mich. Sentiment Feb F | 99.5 | 99.9 |

USD/JPY Likely To Extend Declines Below 106.00

Key Highlights

- The US Dollar recovered slightly this week against the Japanese Yen, but upsides were capped by 107.60.

- There is a major resistance zone forming near 107.60 on the 4-hours chart of USD/JPY.

- The US Initial Jobless Claims figure for the week ending Feb 24, 2018 posted a decline from the last revised reading of 220K to 210K.

- Tokyo's Consumer Price Index ex Food and Energy increased 0.9% in Feb 2018 (YoY), more than the forecast of 0.8%.

USDJPY Technical Analysis

The US Dollar recovered above 107.50 this week against the Japanese Yen. However, the USD/JPY pair failed to retain gains and declined back below the 107.00 support.

It seems like the pair failed to break a major resistance zone near 107.60-80 and started a downside move. However, the pair is still above the 106.00 support area, which is a positive sign.

Looking at the 4-hours chart, it looks like the recent failure was near a bearish trend line with current resistance at 107.20. Moreover, there is a declining channel forming with resistance at 107.40. Lastly, the 100 simple moving average (red, 4-hour) is positioned near 107.45.

Therefore, it seems like there is a crucial upside barrier forming around 107.50. A break and close above 107.50 could open the doors for a push towards the next major resistance at 108.50.

On the downside, the 106.00-106.10 region is a key support. If the pair fails to stay above 106.00, it could move back in the bearish zone.

Recently in the US, the Initial Jobless Claims figure for the week ending Feb 24, 2018 was released by the US Department of Labor. The market was looking for a rise from the last reading of 222K to 226K.

The actual result was on the positive side, as there was a decline in the claims to 210K. Moreover, the last reading was revised down to 220K.

The overall market sentiment is slightly negative for the US Dollar. Pairs such as EUR/USD and GBP/USD were seen recovering above key resistance levels.

Economic Releases to Watch Today

- German Retail Sales for Jan 2018 (YoY) – Forecast +3.5%, versus -1.9% previous.

- UK's Construction PMI for Feb 2018 – Forecast 50.5, versus 50.2 previous.

- Canadian GDP for Q4 2017 (Annualized) – Forecast +2.0%, versus +1.7% previous.

- BOE's Governor Carney speech.

A Dizzying Day For Markets

Dizzying Markets

Jay Powell certainly dialled down the hawkish rhetoric before the Senate Finance Committee in the second part of his “Humphrey Hawkins” testimony.While the dollar has backpedalled on the responsively dovish remarks equity markets didn’t acknowledge the softer language as major stock indexes were trumped by the President imposing tariffs on steel and aluminium imports, all but assuring an escalation of global protectionist policies and a possible outright trade war. A trade tantrum has left global equity indices in a sea of red.

A dizzying day for markets, which were turning positive until Trumps ” America First ” tariff torpedo struck Wall Street sending markets plummeting. In concert, both Fixed income and Gold rallied as investors piled into safer investments.

Oil Markets

Oils markets had a tough go of it this week as concerns about rising Shale production dominated traders psyche. But at the end of the day, the WTI 60 dollar floor looks well supported by the OPEC compliance narrative. And with dollar looking a bit fragile after Jay Powell soft-shoed back on is a hawkish day one delivery, prices have bounced convincingly higher.

Oil traders are latching on to a possible re-emergence of weaker dollar /oil price correlation narrative as currency markets start tracking towards the psychologically crucial DXY 90.00 support level.

Gold Markets

With the balance of risks skewed towards testing the critical $1303 level overnight, gold investors needed nerves of steel to stay in the game. But patience was rewarded when Powell dialled back hawkish inference, and prices rallied hard on the Trump’s ” tariff torpedo ” as investors flocked to haven assets. Gold sentiment has gone through an upside-down week, but underlying support from both risk aversion and a probable uptick in inflation should keep the $1300-1303 floor in check, even more so if the weaker USD narrative comes back with a vengeance.

All eyes will be on China trade-related headlines which could lead to a high level of investor angst. With Senior Level Politburo ministers in the US attempting to diffuse trade wars, the coincidental timing of Trump’s trade tariffs is about as big of a political snub as it gets and we should expect some retaliation from mainland

Currency Markets

Japanese Yen

JPY crosses are feeling the pressure from the global equity market sell-off as the Yen’s haven appeal remains in vogue. Also, Boj continues to go about business while quietly tapering asset purchase. With equity market looking lower, all things being equal, we should expect downside pressure to remain on USDJPY

The Euro

Happy to have taken a week off on Euro positioning despite missing a good buying on dip opportunity. Although history suggests the Euro will gain significant momentum after EU political wobble, the big dollar didn’t play out as planned this week .The EURUSD market remains in range trade stasis awaiting a definitive hawkish shift from the ECB. But it’s as sure of a bet as one can get in FX markets that the ECB will continue to march towards policy normalisation and the EUR will remain bid on dip

The Australian Dollar

The Aussie has picked itself off the canvas, but given its prominent position in the global supply, possible regional trade war escalation will continue to weigh on sentiment.AUD is the worst performer among the G10 overnight, trading down towards 0.7730 following weaker Australian CAPES numbers. And with Risk trading very poorly, the market will continue to favour short Aussie until a definitive USD sell-off re-emerges.

FX Asia

Traditionally there has been a very high correlation between regional currencies and export performance, and given the amount of compliance leading up to last nights trade tariff event, investors need to tread carefully in the local market as the regional markets are very export sensitive.But given the lack of an exacting crystal ball narrative how a possible trade war will play out, it’s not the best of time to jump into the EM Asia FX muck just yet, and probably more prudent waiting for the emergence of the dollar downtrend before re-engaging in local positions.

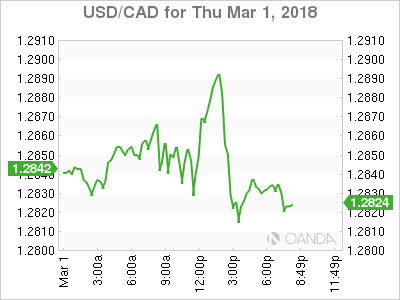

USDCAD Canadian Dollar Flat After Trade Triggered Volatility

The Canadian dollar had a bumpy ride on Thursday. A better than expected current account deficit was positive for the loonie at the start of the North American trading session, but after some mixed message on trade by the US it was reported that US President Donald Trump will impose tariffs on steel and aluminium imports next week. The imports could be as high as 25 percent for steel and 10 percent for aluminium. The move came against opposition from within the Republican party but there was little anybody could do to prevent Trump from fulfilling one of his campaign promises.

Canadian Foreign Affairs Minister Chrystia Freelander said that if the US imposes the tariffs it would have to retaliate. Canada is the biggest buyer of American steel, with about 50 percent going north of the border which could end up hurting the very industry Trump seeks to protect. Mexico has told through sources that is would have no option but to retaliate with tariffs. The US exports more steel to Mexico than it imports. Looking beyond Canada the move by the US is another shot across the bow to China which ironically has seen steel exports fall in recent years.

The US has pushed a protectionist trade agenda with the steel tariffs the biggest step taken so far. The fate of NAFTA remains uncertain with very little progress during the 7 rounds of talks. The current round in Mexico City will end in March 5 with some potential comments addressing the just announced steel and aluminum tariffs.

The USD/CAD gained 0.01 percent on Thursday. The currency pair is trading at 1.2829 after a volatile 24 hours that brought the loonie close to the 1.29 price level. Comments from US President Donald Trump on trade triggered a sell off of the Canadian currency. US stocks also retreated as the one two punch of a potential trade war and higher interest rates hit indices. The USD/CAD ended up almost flat as the market awaits more details on the tariffs that could end up with the US issuing exceptions for certain trade partners, which Canada almost surely on that list.

The USD was trading higher during Fed Chair Jerome Powell’s testimony in front of the Senate Banking committee. Tuesday’s comments before Congress were taken as hawkish by the market and while not walking them back today Powell set a more neutral tone pointing out there is no evidence of the US economy is overheating or higher wages. NY Fed President William Dudley said that gradual will still apply to four rate hikes this year. Wages have not grown at the same rate as the economy which is a concern from some voting Fed members as they cite that lack of inflationary pressure as the main reason the central bank should slow down its rate hike path. Previous Chair Yellen preferred to be ahead of the curve as eventually inflation would catch up. Powell appears to agree with Yellen’s assessment with the Fed anticipated to announce a 25 basis point rate hike on March 21.

The loonie has been under pressure touching weekly lows and will close out the week with the release of the Canadian gross domestic product (GDP). Growth has slowed down in the second half of the year and the monthly GDP data point is forecasted to come in at 0.1 percent. Given the softness of Canadian retail sales it could even end up being a contraction which would be negative for the currency, specially as trade remains a sensitive topic.

Market events to watch this week:

Friday, Mar 2

Tentative GBP Prime Minister May Speaks

4:30am GBP Construction PMI

8:30am CAD GDP m/m

Tariffs Trip Up Dollar

Stocks tumbled and the US dollar followed after Trump finally announced harsh trade tariffs. The euro was the top performer while the US and Australian dollars lagged. Japanese CPI and comments from Carney are up next. The Premium trade shorting DAX30 was closed at 12040 from 12470 entry for a 430 pt gain. Several alternative options on locking gains were shared to subscribers.

Earlier this week we wrote about the US twin deficits. Many analysts have emphasized that they are a large and growing problem. We don't dispute that, but an even bigger problem reared its head on Thursday: How Washington will react to those deficits.

We got a taste of the answers on Thursday after Trump announced that he will use national security provisions to slap tariffs on steel and aluminum imports. The duties on imported steel will be 25% and they will be 10% on aluminum. Trading partners have already said they're planning to take counter-measures.

The move by Trump shouldn't come as a huge surprise – he's been threatening it throughout his time in office. But there was some hope that his words were hollow and that he could be convinced otherwise.

The growing fear in markets is that this is just the start of a trend. Risk aversion hit for the third day as the S&P 500 fell 36 points to 2677. The US dollar slumped on the news across the board. In particular, USD/JPY sank down to 106.20 and is now less than 100 pips from the February low.

Aside from yen strength, the FX market will likely struggle with how to deal with anti-free market measures from Washington and the threat of a trade war.

At the same time, the Fed is trying to navigate mixed signals. The PCE report was in-line with expectations aside from a 0.1 pp beat on personal income. Core PCE inflation was just 1.5% y/y and has been below target on a year-over-year basis in 96 of the past 100 months. However there are some positive signs with 3-month annualized inflation hitting 2%.

More notably, the ISM manufacturing index rose to 60.8 compared to 58.7 expected. That's the highest since 2004 and the commentary in the report was littered with anecdotes about capacity shortages. Prices paid rose to the highest since May 2011.

It was also the second day of testimony from Powell and it had a slightly-more dovish tinge with an emphasis on low wage inflation. Still, he continued to express confidence that prices and wages will rise.

Elsewhere, Japan will get a look at CPI numbers for Tokyo at 2330 GMT. The consensus is for a 1.4% y/y rise but that falls to 0.5% y/y excluding fresh food and energy. Monetary base data is due 20 minutes later. Another event to watch is an appearance from Carney at midnight GMT in Edinburgh.

US: Manufacturing Activity Strengthens in February to a New Cycle High

The Institute for Supply Management (ISM) index of manufacturing for February rose 1.7 points to 60.8 - a new cycle high - beating market expectations of a slight decline to 58.7. This marks the 18th consecutive month that the index has been in expansionary territory.

The underlying details of the report were mixed, with the headline index driven by a strong advance in employment (+5.5 to 59.7), inventories (+4.4 to 56.7 - a cycle high), and supplier deliveries (+2.0 to 61.1). Although both production and new orders declined, they still remain near cycle highs that were reached at the end of last year.

Prices paid rose 1.5 points to 74.2, also a new cycle high.

The spread between new orders and inventories - a good leading indicator of activity - narrowed to 7.5 (-5.6 points) in February. Overall this indicator remains consistent with manufacturing activity continuing to expand through the first quarter of 2018.

Key Implications

The U.S. manufacturing sector continues to surprise to the upside, as demand for U.S. manufactured goods remains robust. Moreover, comments by survey participants were optimistic, suggesting that demand is being supported by tax cuts, and that capacity pressures, exchange rate volatility, and component shortages are pushing up input prices.

Alongside strong domestic demand come encouraging signs of robust foreign demand. New export orders surged to a cycle-high, and PMI manufacturing surveys reported this morning suggest that global demand for manufactured goods remains strong in many parts of the world. This bodes well for first quarter global trade volumes and economic activity more broadly.

Gold Resumes Slide ahead of Speeches from Powell, May

Gold has posted sharp losses in the Thursday session, after a brief pause on Wednesday. In North American trade, the spot price for an ounce of gold is $1308.40 down 0.76% on the day. In economic news, Thursday is quite busy. Personal Spending slowed to 0.2%, matching the forecast. Unemployment claims dropped to an impressive 210 thousand, well below the estimate of 222 thousand. Next up, Fed chair Jerome Powell testifies before the Senate Banking Committee. On Friday, the US publishes UoM Consumer Sentiment. Brexit will also be in focus, as Prime Minister May speaks about Britain's departure from the EU.

Jerome Powell will be on center stage on Thursday, as he testifies before the Senate Banking Committee. Powell addressed the House Finance Committee on Tuesday, and his remarks were decidedly hawkish. Fed chair said that the current policy of gradual rate increases would continue. He added that the economy was strong and that he expected inflation to move up to the Fed target of 2 percent. Importantly, Powell did not address the question of an acceleration of rate hikes, but his hawkish stance has increased the likelihood that the Fed will increase it projection from three to four rate hikes this year. Any hints that Fed will quicken its pace of rate hikes would be bullish for the US dollar.

Gold tends to rise in times of uncertainty, and a crisis is brewing up between London and Brussels, after the EU published a draft of the legal framework of the Brexit agreement. The May government responded by saying it could not accept the draft. Two items in particular have raised the ire of London. First, the proposal that EU would keep Northern Ireland in the bloc's customs union, which could mean a border between Northern Ireland and the UK. Second, that the European Court of Justice (ECJ) would have the final say in any disputes over the Brexit agreement. May wasted no time responding to the EU proposal, saying that any type of border between the UK and Northern Ireland would threaten the constitutional integrity of the United Kingdom. May is unlikely to accept a role for the ECJ after Brexit, as this would be seen as undermining British sovereignty. Meanwhile, the Europeans dismissed May's proposal that a final trade deal would allow some divergence with EU regulations in certain industries, but the Europeans have dismissed this as 'cherry picking', which they say is a non-starter. May will lay out her post-Brexit vision of relations with the EU in a speech on Friday and if the Europeans pour cold water on her plan, nervous investors could snap up gold, a traditional safe-haven asset.

British Pound Under Pressure over Brexit Spat

The British pound has inched lower in the Thursday session. In North American trade, GBP/USD is trading at 1.3745, down 0.11% on the day. In economic news, British Manufacturing PMI ticked lower to 55.2, just above the estimate of 55.1 points. In the US, Personal Spending slowed to 0.2%, matching the forecast. Unemployment claims dropped to an impressive 210 thousand, well below the estimate of 222 thousand. Next up, Fed chair Jerome Powell testifies before the Senate Banking Committee. On Friday, the US publishes UoM Consumer Sentiment. In the UK, Brexit will be in focus, as Prime Minister May speaks about Britain's departure from the EU. As well, Britain releases Construction PMI and Mark Carney will address a conference in Edinburgh.

Are the Brexit talks about to hit the rocks? The pound took a dip on Wednesday, after the EU published a draft of the legal framework of the Brexit agreement. The May government responded by saying it could not accept the draft. Two items in particular have raised the ire of London. First, the proposal that EU would keep Northern Ireland in the bloc's customs union, which could mean a border between Northern Ireland and the UK. Second, that the European Court of Justice (ECJ) would have the final say in any disputes over the Brexit agreement. May wasted no time responding to the EU proposal, saying that any type of border between the UK and Northern Ireland would threaten the constitutional integrity of the United Kingdom. May is unlikely to accept a role for the ECJ after Brexit, as this would be seen as undermining British sovereignty. Meanwhile, the Europeans dismissed May's proposal that a final trade deal would allow some divergence with EU regulations in certain industries, but the Europeans have dismissed this as 'cherry picking', which they say is a non-starter. May will lay out her post-Brexit vision of relations with the EU in a speech on Friday and if the Europeans pour cold water on her plan, the pound could continue to lose ground.

Jerome Powell will be on center stage on Thursday, as he testifies before the Senate Banking Committee. Powell addressed the House Finance Committee on Tuesday, and his remarks were decidedly hawkish. Fed chair said that the current policy of gradual rate increases would continue. He added that the economy was strong and that he expected inflation to move up to the Fed target of 2 percent. Importantly, Powell did not address the question of an acceleration of rate hikes, but his hawkish stance has increased the likelihood that the Fed will increase it projection from three to four rate hikes this year. Any hints that Fed will quicken its pace of rate hikes would be bullish for the US dollar.

Dollar Trying to Extend Rally as Jobless Claims Dropped to Near Five Decade Low

Quick update: Dollar tries to rise further after ISM manufacturing beat expectation. But momentum remains indecisive.

Dollar is trying to ride on strong job data to extend recent rally. Initial jobless claims dropped 10k to 210k, lower than expectation of 226k. That's the lowest level in nearly five decades since December 1969. Four week moving average dropped to 220.5k, also the lowest since 1969. Continuing claims rose 57k to 1.93m in the week ended February 17. Personal income rose 0.4% in January, above expectation of 0.3%. Personal spending rose 0.2%, in line with expectation. Headline PCE was unchanged at 1.7% yoy, core PCE unchanged at 1.5% yoy. Both met expectation. Also released, Canada current account deficit narrowed to CAD -16.4b in Q4. Focus will turn to round two of Fed Chair Jerome Powell's testimony.

Technically, EUR/USD is trying to dip further away from 1.2205 key support, which indicates trend reversal. USD/CHF is also pressing equivalent level at 0.9469. For today, New Zealand Dollar is the strongest into US session, followed by Dollar. Aussie and Loonie are the weakest. For the week. Yen remains the strongest one, followed by Dollar. Canadian is the weakest, followed by Sterling and than Aussie.

EC Tusk warned friction inevitable for Brexit

European Council President Donald Tusk is meeting UK Prime Minister Theresa May in London today. May expressed her intention to make post Brexit trade "as frictionless as possible. Tusk responded by warning that "friction is an inevitable side-effect of Brexit." And ultimately, the post Brexit relationship between UK and EU would be determined by respective "red lines". Tusk added that "we acknowledge these red lines without enthusiasm and without satisfaction, but we must treat them seriously, with all the possible consequences."

EU published the draft Brexit treaty yesterday and the border of Irelands have sudden become the sticky point. Tusk said that he was "absolutely sure that all the essential elements of the draft" would be accepted by the 27 remaining EU members. And he added that that "until now, no one has come up with anything wiser than that" referring to the proposal of keeping Northern Ireland in EU's customs union. But May has already warned that such proposal would "threaten the constitutional integrity of the UK" by creating a border down the Irish Sea." May will deliver her highly anticipated speech on Brexit tomorrow.

Released in European session, Eurozone unemployment rate was unchanged at 8.6% in January. PMI manufacturing was revised up by 0.1 to 58.6 in February. UK PMI manufacturing dropped to 55.2 in February, down from 55.3 but beat expectation of 55.0. M4 money supply rose 1.5% mom in January. Mortgage approvals rose to 67k in January. Swiss PMI manufacturing rose 0.2 to 65.5 in February. Retail sales dropped -1.4% yoy in January GDP grew 0.6% qoq in Q4.

BoJ Kataoka warned on premature stimulus exit

BoJ board member Goushi Kataoka urged that "to influence inflation expectations, it is essential that policy coordination between the government and the BOJ ... is firmly ensured through action by both entities." And he noted that " there is still a long way to go before considering a change in monetary policy stance." He warned against premature stimulus exit as that could drag Japan back into deflation. Kataoka is the persistent sole dissenter in BoJ since joining last year, pushing for more aggressive easing.

Released from Japan, capital spending rose 4.3% in Q4, above expectation of 3.0%. PMI manufacturing was revised up by 0.1 to 54.1 in February. Consumer confidence dropped 0.4 to 44.3 in February.

Caixin China PMI manufacturing hit six-month high

The Caixin China PMI manufacturing rose 0.1 to 51.6 in February, above expectation of 51.3. The index focuses on small to mid-size manufacturers hit a six-month high. Zhengsheng Zhong, director of macroeconomic analysis at CEBM Group, a subsidiary of Caixin noted that "for now, the durability of the Chinese economy will persist. Looking ahead, whether demand generated from the beginning of work in March will gain strength will be key in determining China's economic direction for 2018."

Australia private capital expenditure unexpectedly dropped -0.2% in Q4, comparing to expectation of 1.0% rise. However, that's probably due to the large upward revision in the prior quarter, from 1.0% to 1.9%. New Zealand terms of trade dropped -0.2% qoq in Q4, below expectation of 0.5% qoq.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2173; (P) 1.2207 (R1) 1.2227; More....

As noted before, the break of 1.2205 key support is taken as a tentative sign of trend reversal, after being rejected by 1.2516 key fibonacci level. Intraday bias remains on the downside for deeper fall. Sustained trading below 1.2205 will confirm and target 38.2% retracement of 1.0339 to 1.2555 at 1.1708. On the upside, above 1.2354 minor resistance will dampen this bearish case and bring retest of 1.2555 high instead.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.5553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Terms of Trade Index Q/Q Q4 | -0.20% | 0.50% | 0.70% | 1.30% |

| 23:50 | JPY | Capital Spending Q4 | 4.30% | 3.00% | 4.20% | |

| 00:30 | AUD | Private Capital Expenditure Q4 | -0.20% | 1.00% | 1.00% | 1.90% |

| 01:30 | JPY | PMI Manufacturing Feb F | 54.1 | 54 | 54 | |

| 01:45 | CNY | Caixin PMI Manufacturing Feb | 51.6 | 51.3 | 51.5 | |

| 05:00 | JPY | Consumer Confidence Index Feb | 44.3 | 44.8 | 44.7 | |

| 06:45 | CHF | GDP Q/Q Q4 | 0.60% | 0.50% | 0.60% | 0.70% |

| 06:45 | CHF | GDP Y/Y Q4 | 1.90% | 1.70% | 1.20% | |

| 08:15 | CHF | Retail Sales Y/Y Jan | -1.40% | 1.10% | 0.60% | 0.70% |

| 08:30 | CHF | PMI Manufacturing Feb | 65.5 | 64.1 | 65.3 | |

| 08:45 | EUR | Italy Manufacturing PMI Feb | 56.8 | 58 | 59 | |

| 08:50 | EUR | France Manufacturing PMI Feb F | 55.9 | 56.1 | 56.1 | |

| 08:55 | EUR | Germany Manufacturing PMI Feb F | 60.6 | 60.3 | 60.3 | |

| 09:00 | EUR | Eurozone Manufacturing PMI Feb F | 58.6 | 58.5 | 58.5 | |

| 09:30 | GBP | Mortgage Approvals Jan | 67K | 62K | 61K | 62K |

| 09:30 | GBP | M4 Money Supply M/M Jan | 1.50% | 0.40% | -0.60% | |

| 09:30 | GBP | PMI Manufacturing Feb | 55.2 | 55 | 55.3 | |

| 10:00 | EUR | Eurozone Unemployment Rate Jan | 8.60% | 8.60% | 8.70% | 8.60% |

| 13:30 | CAD | Current Account Balance (CAD) Q4 | -16.4B | -17.8B | -19.3B | -18.6B |

| 13:30 | USD | Personal Income Jan | 0.40% | 0.30% | 0.40% | |

| 13:30 | USD | Personal Spending Jan | 0.20% | 0.20% | 0.40% | |

| 13:30 | USD | PCE Deflator M/M Jan | 0.40% | 0.40% | 0.10% | |

| 13:30 | USD | PCE Deflator Y/Y Jan | 1.70% | 1.70% | 1.70% | |

| 13:30 | USD | PCE Core M/M Jan | 0.30% | 0.30% | 0.20% | |

| 13:30 | USD | PCE Core Y/Y Jan | 1.50% | 1.50% | 1.50% | |

| 13:30 | USD | Initial Jobless Claims (24 FEB) | 210K | 226K | 222K | 220K |

| 14:30 | CAD | RBC Canadian Manufacturing PMI Feb | 55.6 | 55.9 | ||

| 14:45 | USD | US Manufacturing PMI Feb F | 55.3 | 55.8 | 55.9 | |

| 15:00 | USD | Construction Spending M/M Jan | 0.00% | 0.20% | 0.70% | 0.80% |

| 15:00 | USD | ISM Manufacturing Feb | 60.8 | 58.7 | 59.1 | |

| 15:00 | USD | ISM Prices Paid Feb | 74.2 | 70 | 72.7 | |

| 15:30 | USD | Natural Gas Storage | -71B | -124B |

GOLD: Tumbles Lower, Extends Weakness

GOLD: The commodity retains its downside short term as it sold off on Thurs leaving risk of more upside pressure. On the downside, support comes in at the 1,300.00 level where a break will turn attention to the 1,290.00 level. Further down, a cut through here will open the door for a move lower towards the 1,280.00 level. Below here if seen could trigger further downside pressure towards the 1,270.00 level. Conversely, resistance resides at the 1,310.00 level where a break will aim at the 1,320.00 level. A turn above there will expose the 1,330.00 level. Further out, resistance stands at the 1,340.00 level. All in all, GOLD looks to strengthen further.